Scouting the Tape - June 6, 2026

(Unique) macro idea generation and (insightful) market thoughts.

Well I wrote this whole piece on Tuesday through Thursday of last week before Friday’s bloodbath. I’ve had some travel and a busy schedule that held up its release until now. As I reopened the piece and set out to update it following Friday’s market debacle, I paused and thought it might be more meaningful for me to look back on it in its original form in the future. While I realize it may be incrementally less useful in the very near-term, I think the ideas discussed have staying power and will just require attention paid to the tactics and timing around execution. I can always (and will likely) update the points in future writings. So from here on is my pre-Friday write up.

I continue to believe the coming weeks and months will be rich in opportunity. In the next two weeks alone we have 3 central bank meetings, inflation data and one of the biggest IPOs of all-time. I suggest keeping your head on a swivel as I think there are some trend changes afoot and my gut is telling me to listen to the messages the market is trying to send.

Bitcoin is flashing red alert.

Scouting the Tape readers have been alerted of our cautious crypto stance over the last few weeks, noting the DAT problems and large sellers distributing coins. We have been fortunate to be seeing this market’s movements quite well over the past few months.

Quinn Thompson@qthomp

Quinn Thompson@qthomp

Quinn Thompson @qthompWhat if SOLBTC is the new ETHBTC?1:13 PM · Jun 4, 2026 · 8.02K Views2 Replies · 25 Likes

Quinn Thompson @qthompWhat if SOLBTC is the new ETHBTC?1:13 PM · Jun 4, 2026 · 8.02K Views2 Replies · 25 LikesWhere do we go from here? Well I hate to say it but I feel pretty confident that the multi-month outlook remains negative. With an onslaught of record IPOs, waning liquidity and deteriorating consumer health, I see little potential for crypto’s struggles to be resurrected anytime soon. Macro aside, the idiosyncratic MSTR and quantum problems are yet to be resolved.

I elaborated on my bewilderment with the decisions coming out of the Microstrategy headquarters. Their actions over the last year make absolutely no sense to me. And now BMNR seems to want to go down the same path pursuing a death spiral. Truly unbelievable behavior.

Quinn Thompson@qthompSTRC is now approaching one of the worst drawdowns since its launch. The majority of times it traded this low (albeit small sample size) required 50 bps dividend rate increases instead of the usual 25 bps. It's my view that Strategy will and probably should raise the dividend Quinn Thompson @qthomp“Steady”…not sure the market agrees but let’s see. For the month of June it appears Strategy will be prioritizing MSTR owners over STRC owners. https://t.co/XJJ2yHOIda11:58 PM · Jun 3, 2026 · 32.5K Views24 Replies · 12 Reposts · 138 Likes

Quinn Thompson @qthomp“Steady”…not sure the market agrees but let’s see. For the month of June it appears Strategy will be prioritizing MSTR owners over STRC owners. https://t.co/XJJ2yHOIda11:58 PM · Jun 3, 2026 · 32.5K Views24 Replies · 12 Reposts · 138 LikesMy recommendation is to avoid the crypto market for the summer as it tends to struggle during the coming months even when there isn’t a barrage of severe headwinds in its way. Pick it back up in late Q3 and see where things stand and my guess is you’ll save yourself a lot of brain damage.

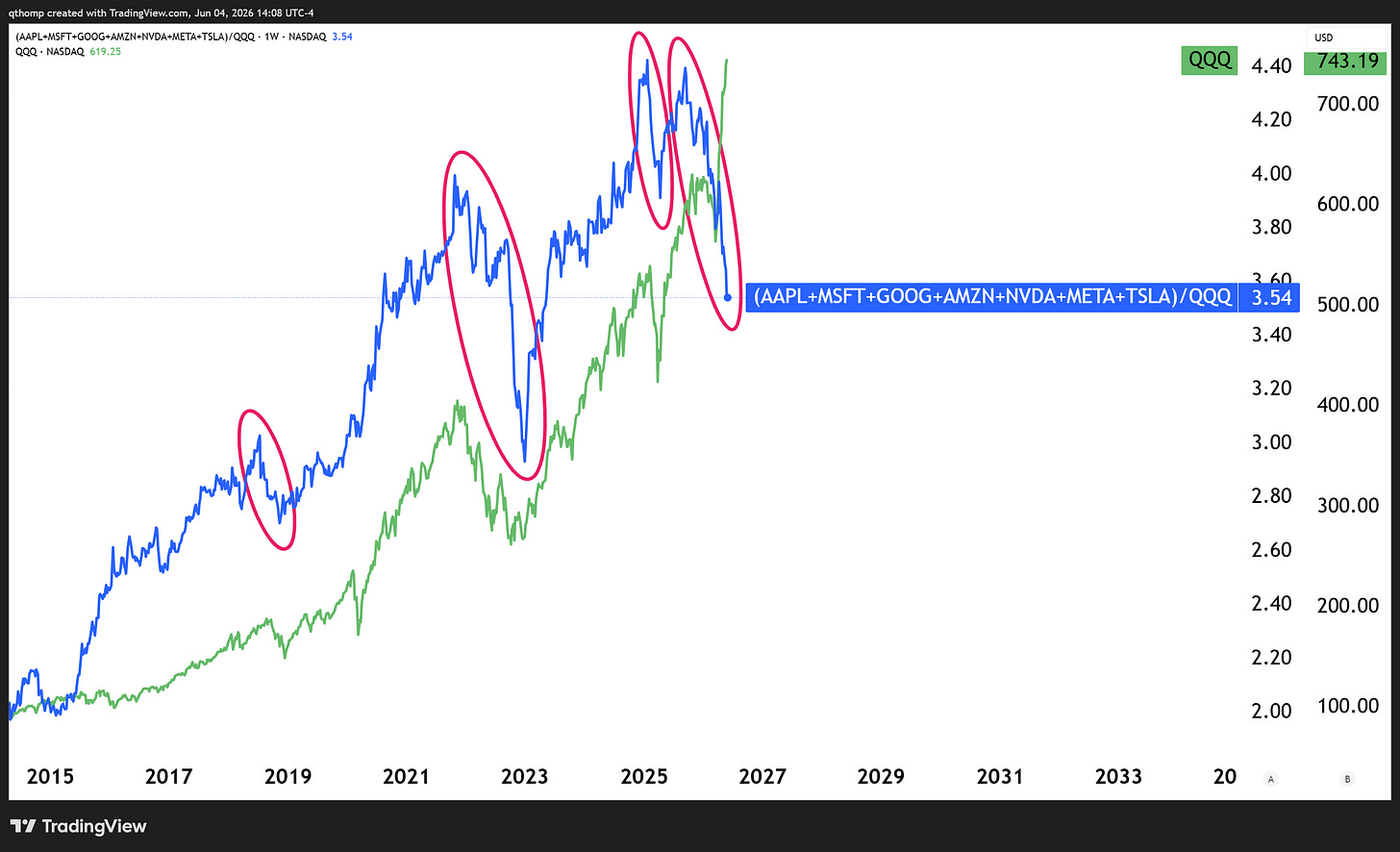

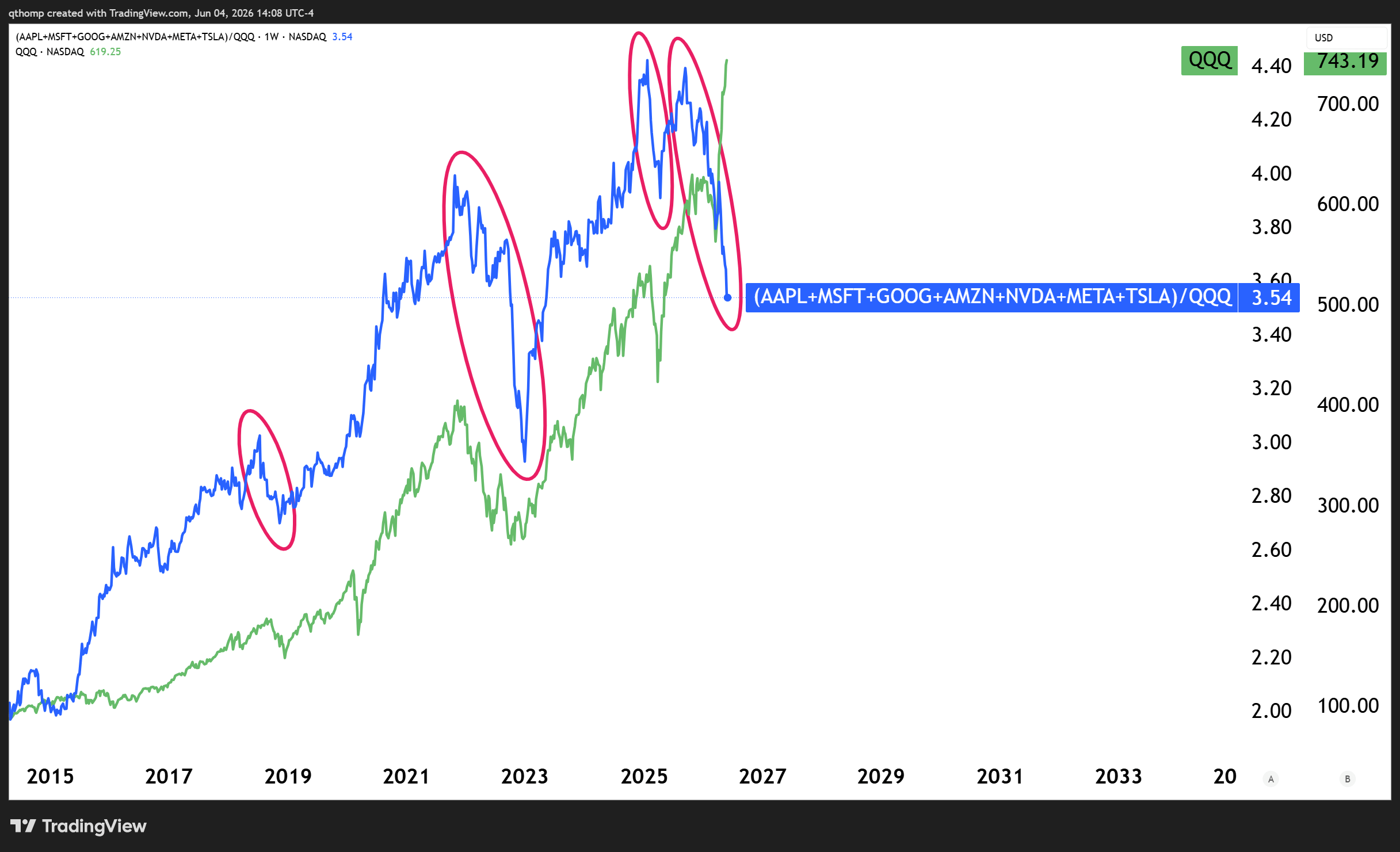

We are witnessing one of the largest divergences in Bitcoin and tech stocks in recent history.

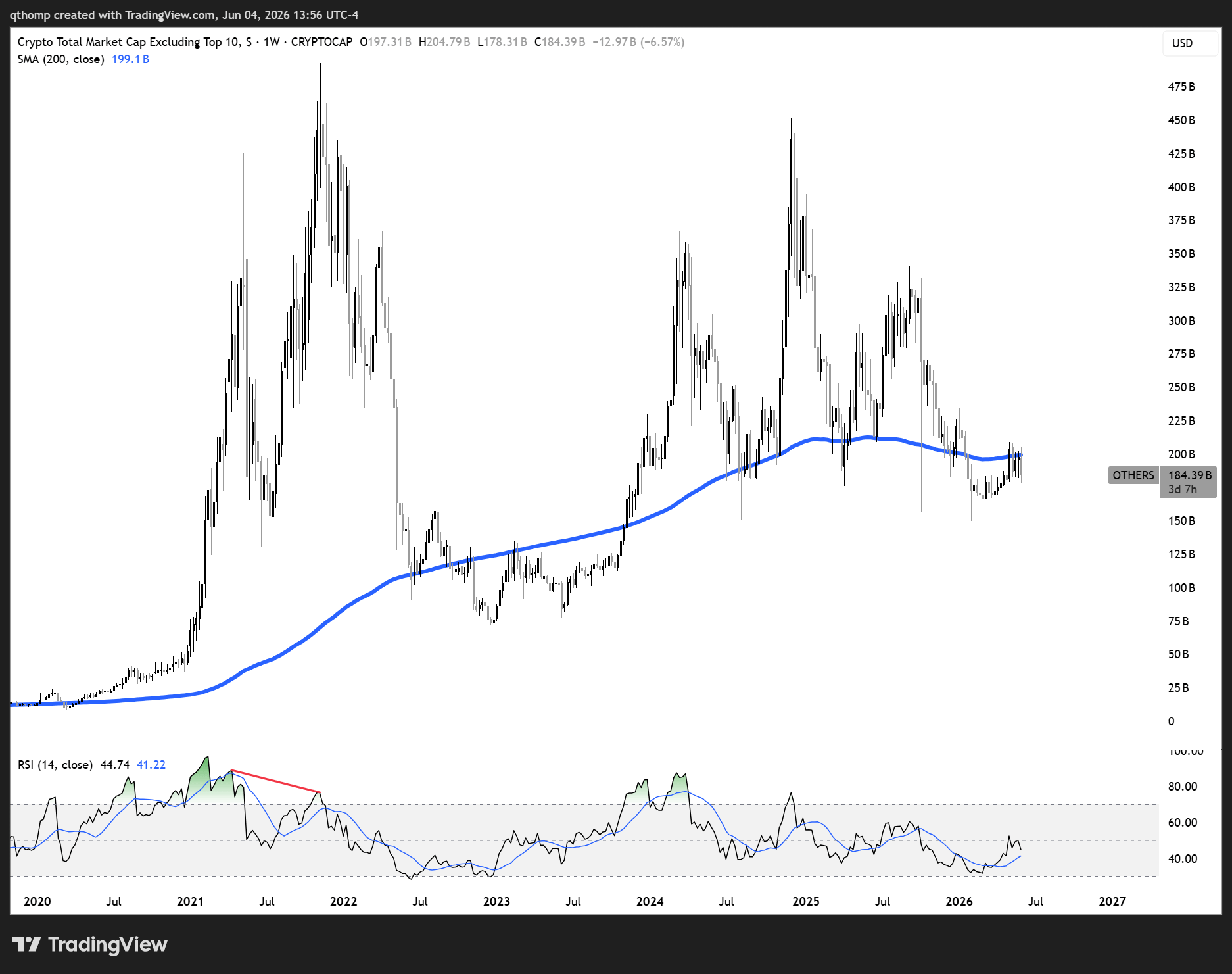

I’ll leave you with two more simple charts that both say exit stage left.

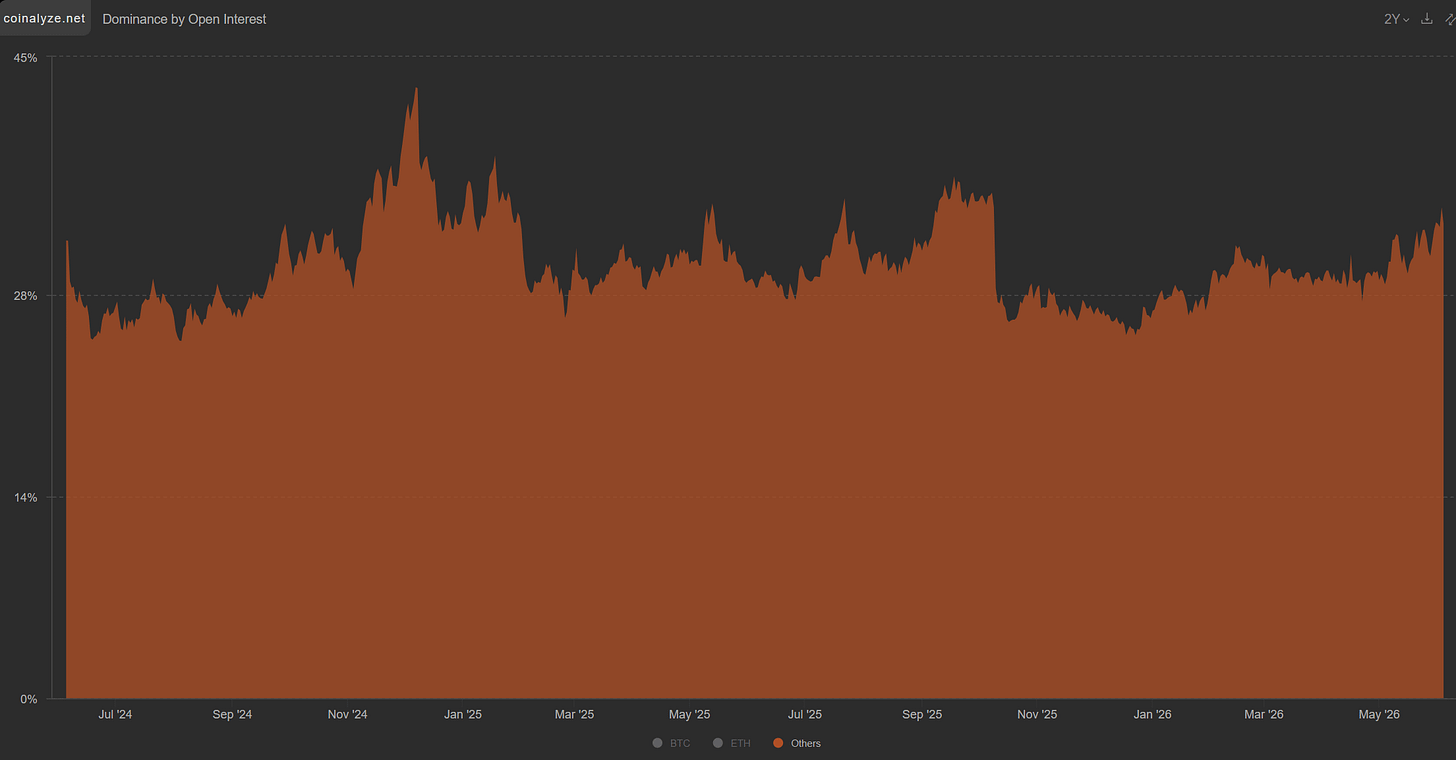

OTHERS underside rejecting the 200wma and putting in a lower high RSI.

Alt dominance as a percentage of open interest is at levels that usually coincide with market peaks. Keep in mind this is surge is coming deep into a decisive bear market, a time when selling strength is the most prudent action.

The ongoing technology divergence commands your attention.

If you take the time to research further or better understand any sections from this post, make it this one. If I may suggest, it may be worth your while to review recent Scouting the Tape issues to set the stage with what’s going on in Japan, recent sentiment data and investor positioning.

Also if you didn’t see our thoughts on the upcoming IPO math and the problem it represents for the indices, check it out. As the first IPO of the bunch (SpaceX) comes in the next week, this becomes increasingly important. The following are a few charts I’m finding very interesting going into this event.

Let me start with the head scratcher out of the gates. There has never before been a divergence this large in Mag7 relative performance versus Nasdaq and the Nasdaq itself. This makes sense because those 7 stocks represent 37% of the Nasdaq 100 index, which means the other 63% of market cap weight is carrying the index (think semiconductors, chips and memory).

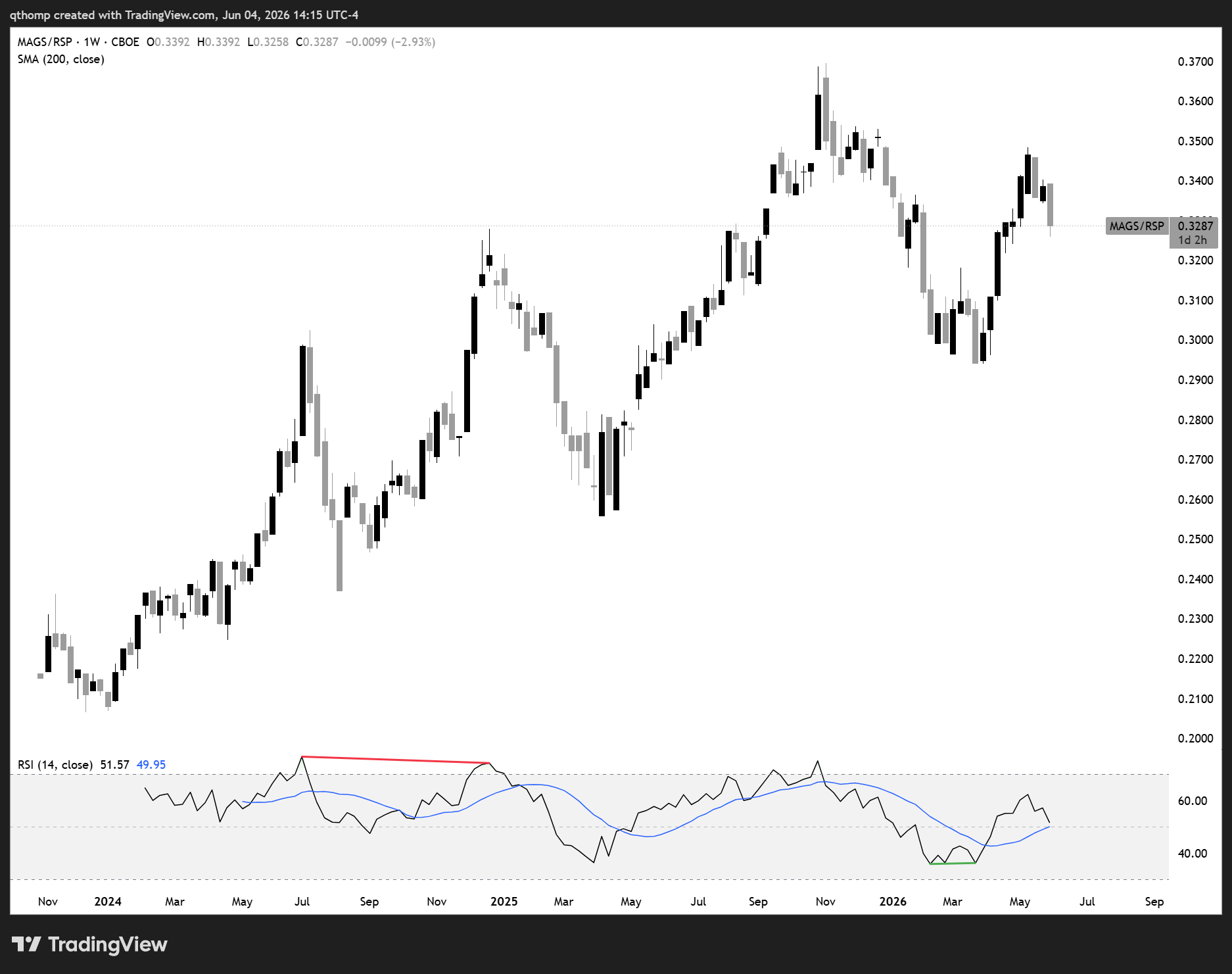

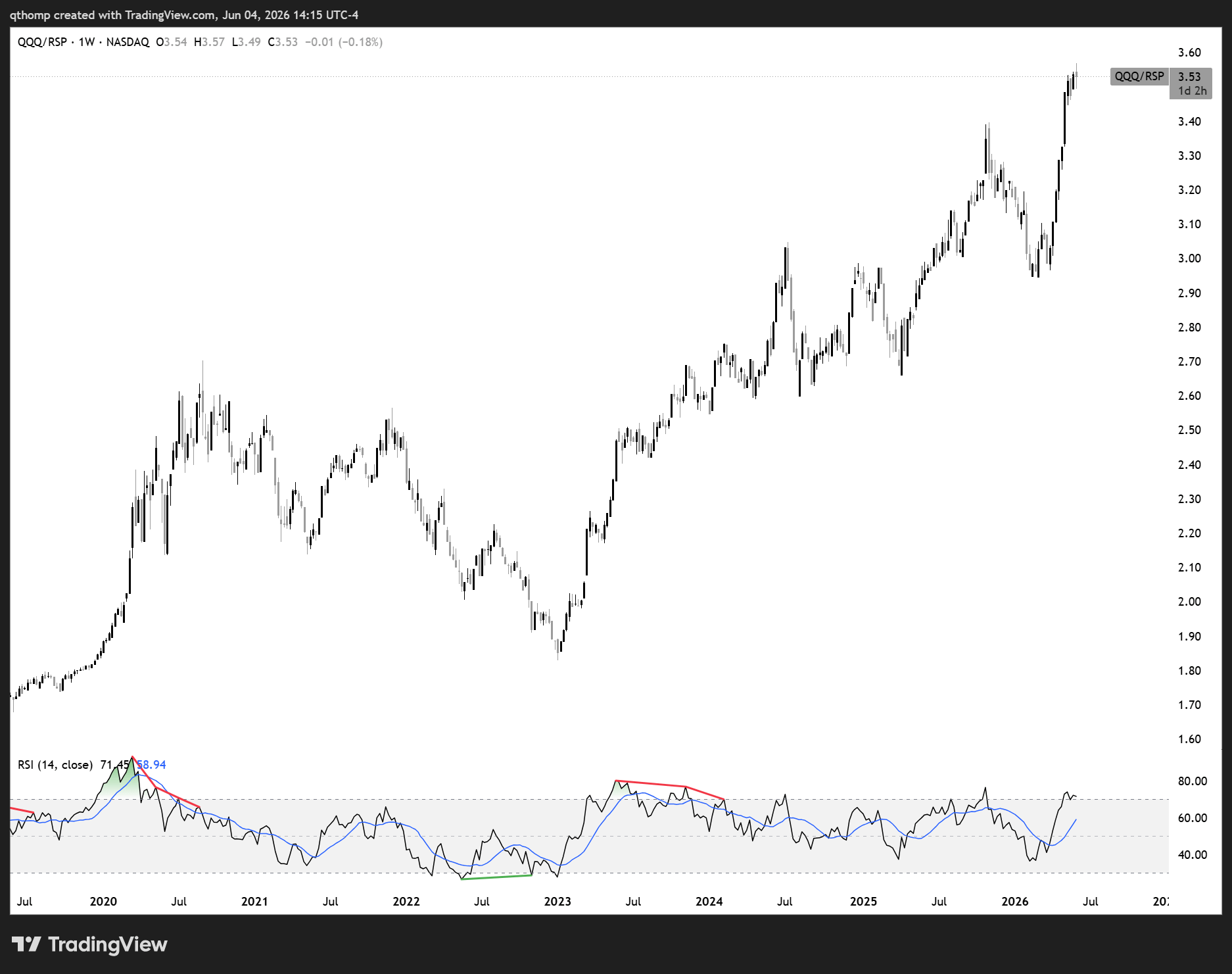

Technology stocks as a whole have trounced ‘real economy’ or ‘main street’ over the last few months on all measures. Both QQQ/RSP and MAGS/RSP have been very strong. Said another way, tech concentration risks are flashing warning signs.

Now back to this Mag7 and Nasdaq divergence. There may be multiple interpretations of this.

MAGS is dominated by hyperscalers who are spending immensely on AI capex commitments while QQQ has more chip and semiconductor names who are beneficiaries from receiving those capex dollars.

Another interpretation is that the other 93 companies in the Nasdaq 100 are doing the heavy lifting, which is often a classic late-cycle behavior where investors, fearing the top-heavy giants are exhausted, rotate into the "second-tier" or "supply chain" names to keep the rally alive.

Historically, the healthiest bull markets have come when the leaders lead. It has often been a warning sign when that is not the case. If the Mag7 generals continue to fall because their capex is too high, presumably they will eventually have to cut that spending, at which point the semiconductor and AI supply chain beneficiary trade will be in jeopardy.

I’ll pose a few questions to help you see the side of the thesis you find yourself on.

Given the $3T+ in new IPO supply we discussed earlier, do you think the other 93 stocks in the QQQ have the liquidity to support both those new IPOs and their current outperformance, or is this a top before the dilution hits?

With 3 new >$1T companies arriving to the public markets and competing for Mag7 capital and mindshare, do you think the conditions are ripe for MAGS to start leading to the upside again and carry the whole market with them?

The dilemma I see is how the hyperscalers could regain equity market leadership with declining free cash flow, rising debt levels and lower share repurchases all tied to their capex spending. The only path for that to occur in my mind is a reduction in said capex spending which would put a fork in the semiconductor and AI capex beneficiary trade, thus bringing down the technology complex as a whole. The other consideration is that the gains from the valuation mark ups of the private AI companies are accounting for significant portions of hyperscaler earnings as PauloMacro has been discussing. A reduction in their capex spend would be interpreted negatively for OpenAI, Anthropic, et al and come back to hurt them in this way too.

Said another way, the ever increasing capex commitments are creating a prisoner’s dilemma for the hyperscalers. Their balance sheet quality is deteriorating with growing lease and purchase commitments and debt issuance.

Path A (keep spending): They continue to see declining free cash flow and share buybacks, causing their equity to continue lagging.

Path B (cut spending): They regain free cash flow and start to restrengthen their balance sheets but at the direct expense of the broader tech indices due to the recent semiconductor leadership, ultimately hitting their share prices both indirectly, and directly as a result of lower valuations on their OpenAI, Anthropic and other AI company holdings.

I think the AI circular reference memes might make a comeback soon.

Kuppy@hkuppy

Kuppy@hkuppy

*Walter Bloomberg @DeItaone$CRWV - COREWEAVE SHARES UP 9% PREMARKET AFTER NVIDIA INVESTS $2 BLN IN CO1:15 PM · Jan 26, 2026 · 29.4K Views9 Replies · 14 Reposts · 174 Likes

*Walter Bloomberg @DeItaone$CRWV - COREWEAVE SHARES UP 9% PREMARKET AFTER NVIDIA INVESTS $2 BLN IN CO1:15 PM · Jan 26, 2026 · 29.4K Views9 Replies · 14 Reposts · 174 Likes

Policymaker reaction functions.

The other week I wrote to a client a similarity I see among both the oil to $200 and AI singularity camps - that is ignoring policymaker reaction functions.

I posited that while at first glance, the shrinking labor force and rising layoffs might be deflationary in a vacuum, but in a political system that relies on stability, increasing the number of adults with nothing to do is destabilizing and the response to AI induced layoffs, and AGI if we get there, are extremely inflationary and require all sorts of stimulus to address politically and socially.

It’s the same thing with perma oil bulls. They are correct that if left unaddressed, the commodity supply problems could cause large price spikes and ruptures throughout the financial system. However, while not ideal, Trump can take a really bad egg-on-the-face style deal to ensure gas prices don’t stymie his midterm odds. At the same time, they have authorized releasing the SPR down to operational minimum levels which will last into midterms. Pair these two aspects with the Iran War being one of the unanimously most unpopular decisions of his 6 years in office while his approval ratings are the lowest ever in those 6 years. This creates a probability distribution that favors oil not being a big deal again before midterms.

On this point, there is a clear growing pitch in sentiment and actions opposing big tech and AI.

“Resist and Unsubscribe”

Quinn Thompson@qthompA "Resist and Unsubscribe" campaign has been launched by @profgalloway targeting the big tech and corporate monopolies with White House influence. Don't forget what we wrote back in December... ..."Will large swaths of voters favor the 'support AI growth at all costs' policy

Quinn Thompson @qthompA few weeks ago on @ForwardGuidance I called $NVDA a national security threat. The US stock market has a Mag7 problem. Concentration risks are mounting as the top 10% of US stocks now represent ~80% of total US equity market cap. It begs the question - does the US have a https://t.co/mtvWKVKbeR7:56 PM · Feb 3, 2026 · 9.63K Views3 Replies · 1 Repost · 28 Likes

Quinn Thompson @qthompA few weeks ago on @ForwardGuidance I called $NVDA a national security threat. The US stock market has a Mag7 problem. Concentration risks are mounting as the top 10% of US stocks now represent ~80% of total US equity market cap. It begs the question - does the US have a https://t.co/mtvWKVKbeR7:56 PM · Feb 3, 2026 · 9.63K Views3 Replies · 1 Repost · 28 Likes“War on Waymo”

Mounting datacenter opposition has led to 140+ activist groups across 24 states delaying or blocking over ~$64 billion in development projects.

It wasn’t long ago that Trump was leaning into this notion to attract voters ahead of midterms. I would expect him to be forced to go back to this well over the coming months.

Quinn Thompson@qthompTRUMP: MICROSOFT WILL MAKE MAJOR CHANGES BEGINNING THIS WEEK TO ENSURE AMERICANS DON'T PAY FOR THEIR POWER CONSUMPTION IN FORM OF HIGHER UTILITY BILLS TRUMP: TECH COMPANIES MUST PAY FOR DATA CENTER ELECTRIC BILLS TRUMP: HAVE MUCH TO ANNOUNCE IN COMING WEEKS ON DATA CENTERSQuinn Thompson @qthompA few weeks ago on @ForwardGuidance I called $NVDA a national security threat. The US stock market has a Mag7 problem. Concentration risks are mounting as the top 10% of US stocks now represent ~80% of total US equity market cap. It begs the question - does the US have a https://t.co/mtvWKVKbeR12:20 AM · Jan 13, 2026 · 34.3K Views5 Replies · 74 Likes

Weird market moves in the exchange landscape.

The recent declines CME, CBOE and ICE have been pinned on the recent CFTC perpetual futures approvals. Peak to trough has been quite dramatic and has me wondering if there’s more to it than what meets the eye. Not my domain though.

Negligible Capital@negligible_cap$CBOE and $CME have been getting smoked the last couple days since the CFTC approved US perp futures for Kalshi and Polymarket. Per TD, the approval likely creates more competition in the retail market per the sellside, and is curtailing the multiple on some exchanges $CBOE down

Negligible Capital@negligible_cap$CBOE and $CME have been getting smoked the last couple days since the CFTC approved US perp futures for Kalshi and Polymarket. Per TD, the approval likely creates more competition in the retail market per the sellside, and is curtailing the multiple on some exchanges $CBOE down 1:57 PM · Jun 2, 2026 · 25.1K Views4 Replies · 12 Reposts · 80 Likes

1:57 PM · Jun 2, 2026 · 25.1K Views4 Replies · 12 Reposts · 80 LikesMaybe it’s nothing, but it does sort of give me private credit sell off vibes earlier this year. I don’t love the omen of key financial market infrastructure breaking down in a big way.

There are other weird things going on like the retail sell off we noted a few weeks ago. I don’t have any actionable recommendations here because neither are my area of expertise but it is interesting to me.

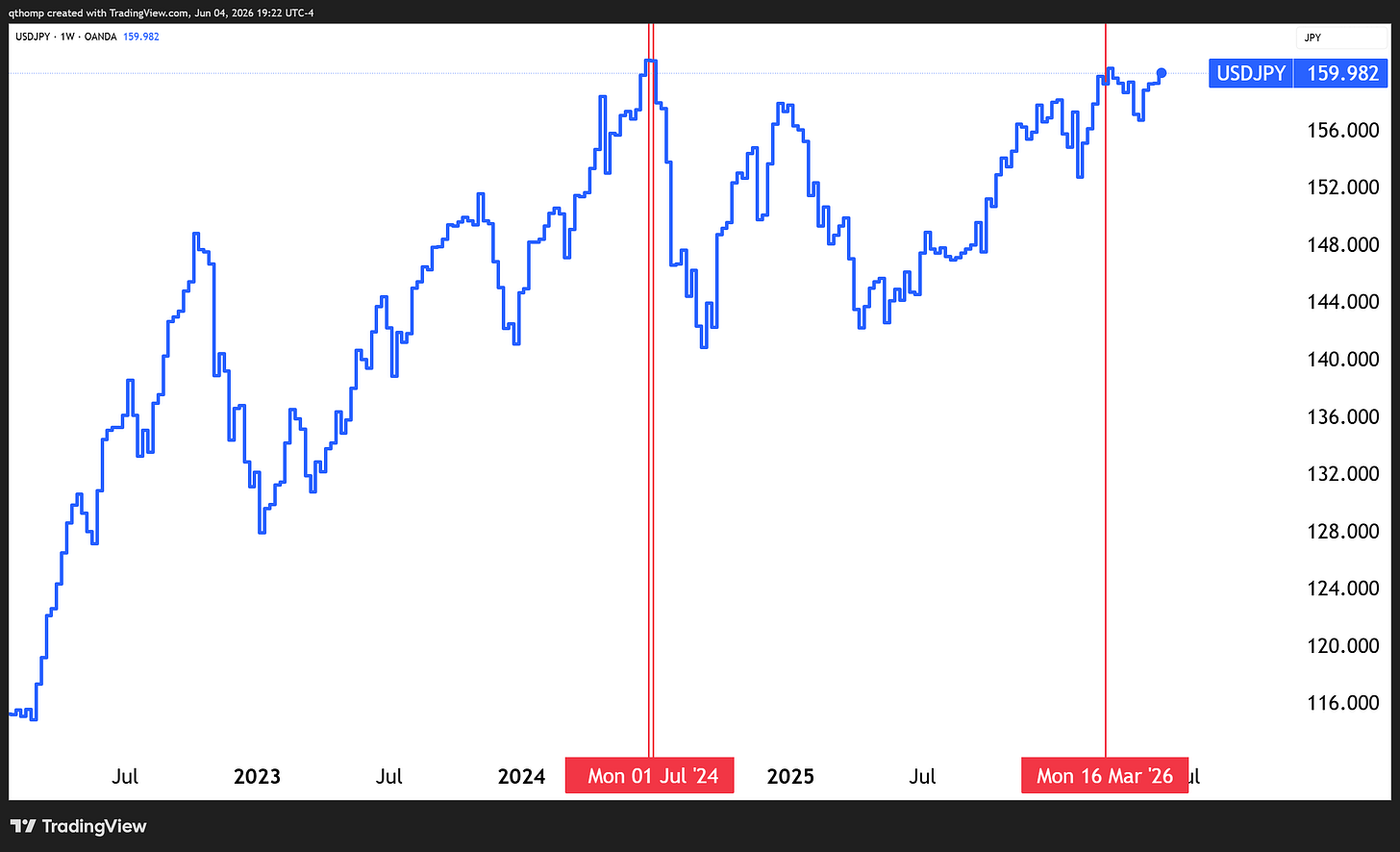

USDJPY

Let this serve as my weekly reminder to keep Japan on your radar. USDJPY is flirting with its 4th highest weekly close ever in almost 50 years. There is a BOJ meeting the day before the FOMC in two weeks and I would imagine they try to strengthen the Yen. If they don’t use that week as an opportunity, I would expect the market to send a message with a breakout above 160, something I don’t think Japanese policymakers want to see.

I continue to believe upside in the recent winning trades will be limited over the coming months. The volatility suppression of the last few months has made it difficult to play the short side in much of anything but I think that will start to change going forward.