Scouting the Tape - Mar 1, 2026

(Unique) macro idea generation and (insightful) market thoughts.

In our world of rapid news flow, we are overwhelmed with information, much of which is noise. I say this as a reminder in times like these where increasing velocity has a tendency to reduce our aperture. It’s important to be plugged into the stream of markets but stay grounded in your bigger picture and fundamental views so as to not get too near-sighted around any one event. Stay vigilant, question everything and reduce your intake of noise as best possible.

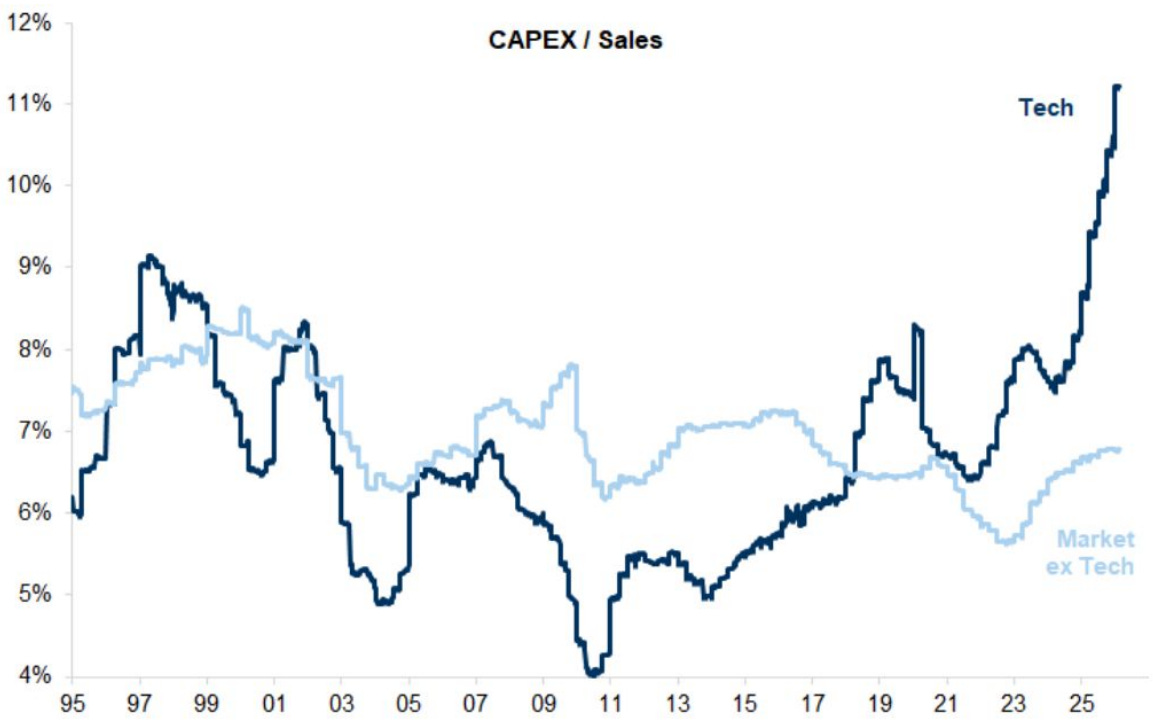

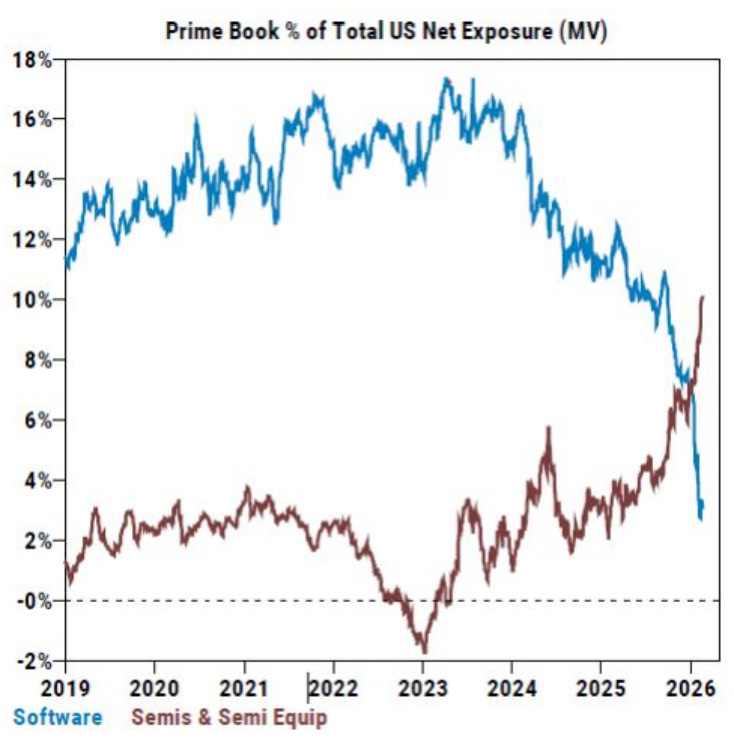

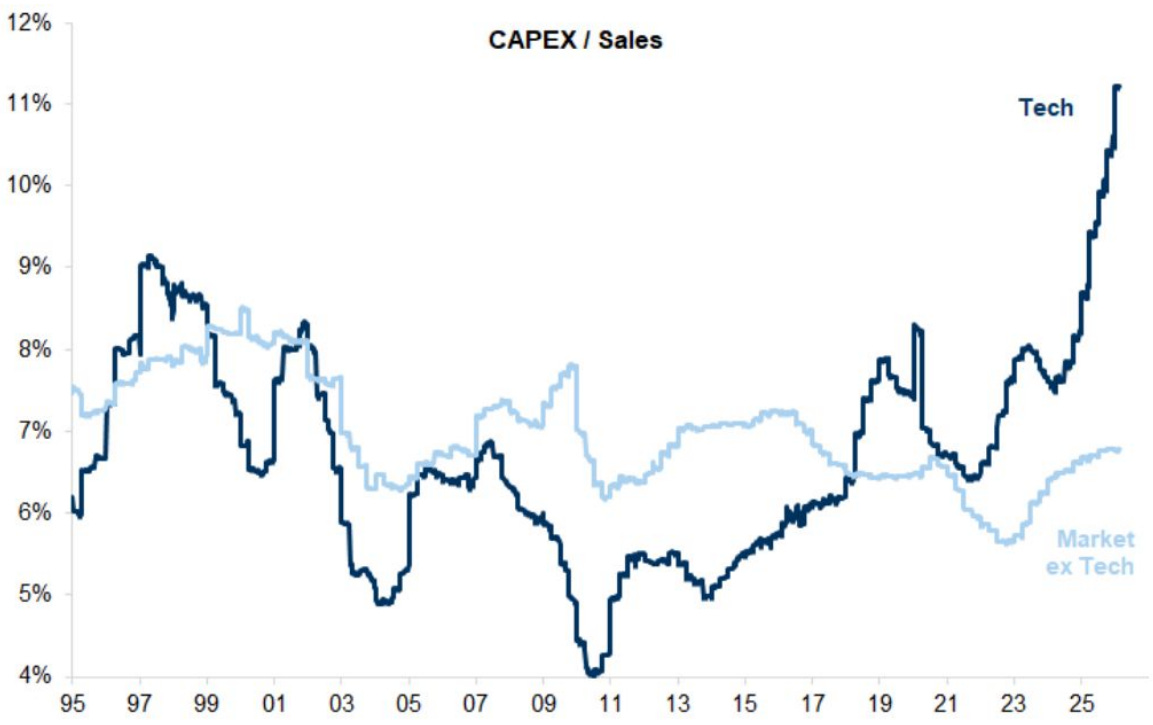

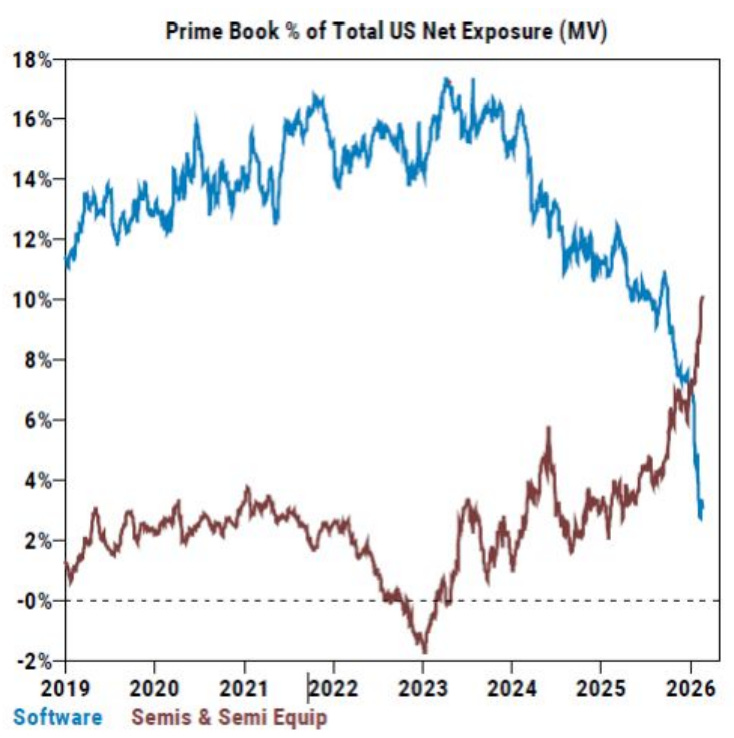

I think semis have topped for a very long time.

I have been tweeting on this topic and talking about it on Forward Guidance for many weeks now. Positioning is extremely crowded into the sector at a time when forward looking rates of change should begin rolling over.

Hyperscaler spenders have underperformed the equal weight S&P 500 by -25% since their peak in late October. If you’re pointing to “AI capex” as your bull thesis, you’re late. The trade has played out and the next order of business is for these hyperscaler spenders to reduce spend in order to try and slow/stop share price declines. Semi’s are the next on the chopping block.

Everyone is all in.

Heading into midterms, political winds are likely to blow against datacenter expansion as we’ve already been seeing. Electricity is the hottest component of CPI for the last year and now with oil prices waking up too, keeping a lid on this for consumers will be a top priority. Mix in job losses starting to accumulate on the back of AI adoption gains and it becomes a fairly easy bipartisan issue for both sides to rally behind.

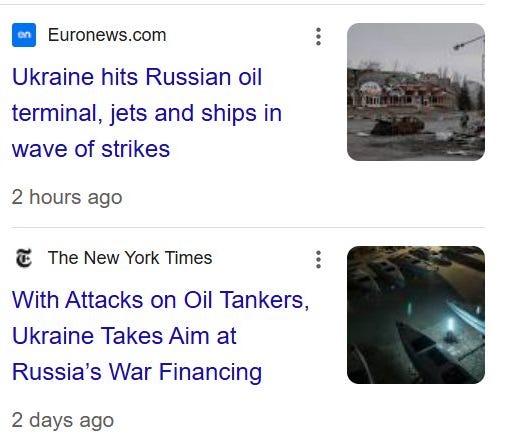

This oil move is more than just Iran.

I originally posted the oil long in late December ahead of the Venezuela intervention.

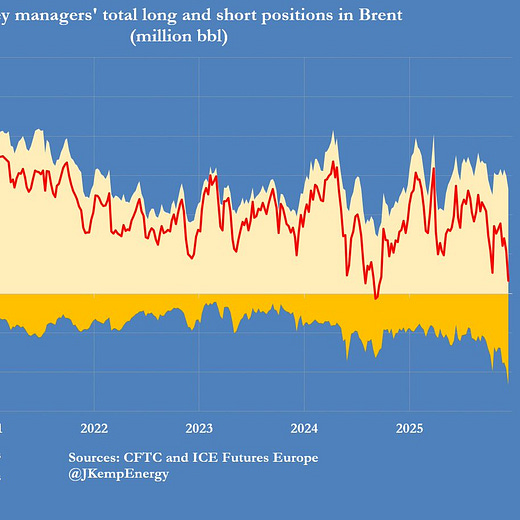

Quinn Thompson@qthompLong oil and related equities $USO $IGE $XLE $OIH $XES "Investors have turned exceptionally bearish about the outlook for crude oil prices...funds held a net long position of just 33 million barrels...the sixth-lowest for all weeks since the start of 2011." @JKempEnergy

Quinn Thompson@qthompLong oil and related equities $USO $IGE $XLE $OIH $XES "Investors have turned exceptionally bearish about the outlook for crude oil prices...funds held a net long position of just 33 million barrels...the sixth-lowest for all weeks since the start of 2011." @JKempEnergy

6:37 PM · Dec 22, 2025 · 22.1K Views14 Replies · 5 Reposts · 78 Likes

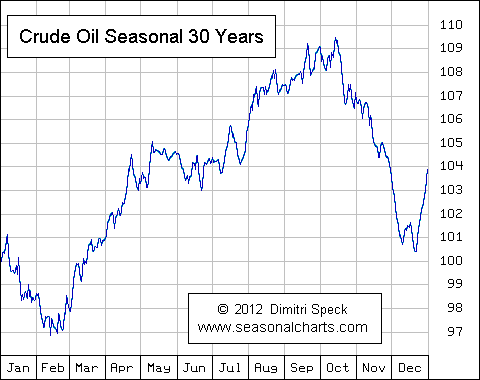

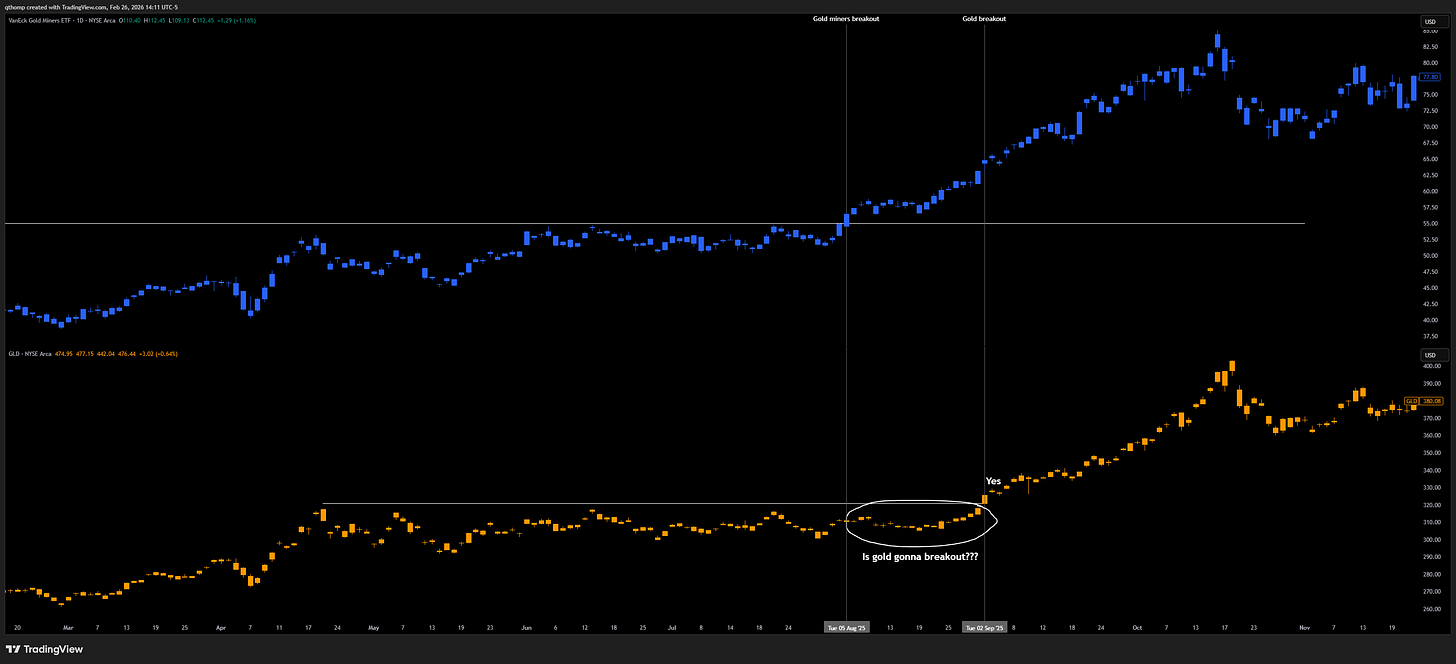

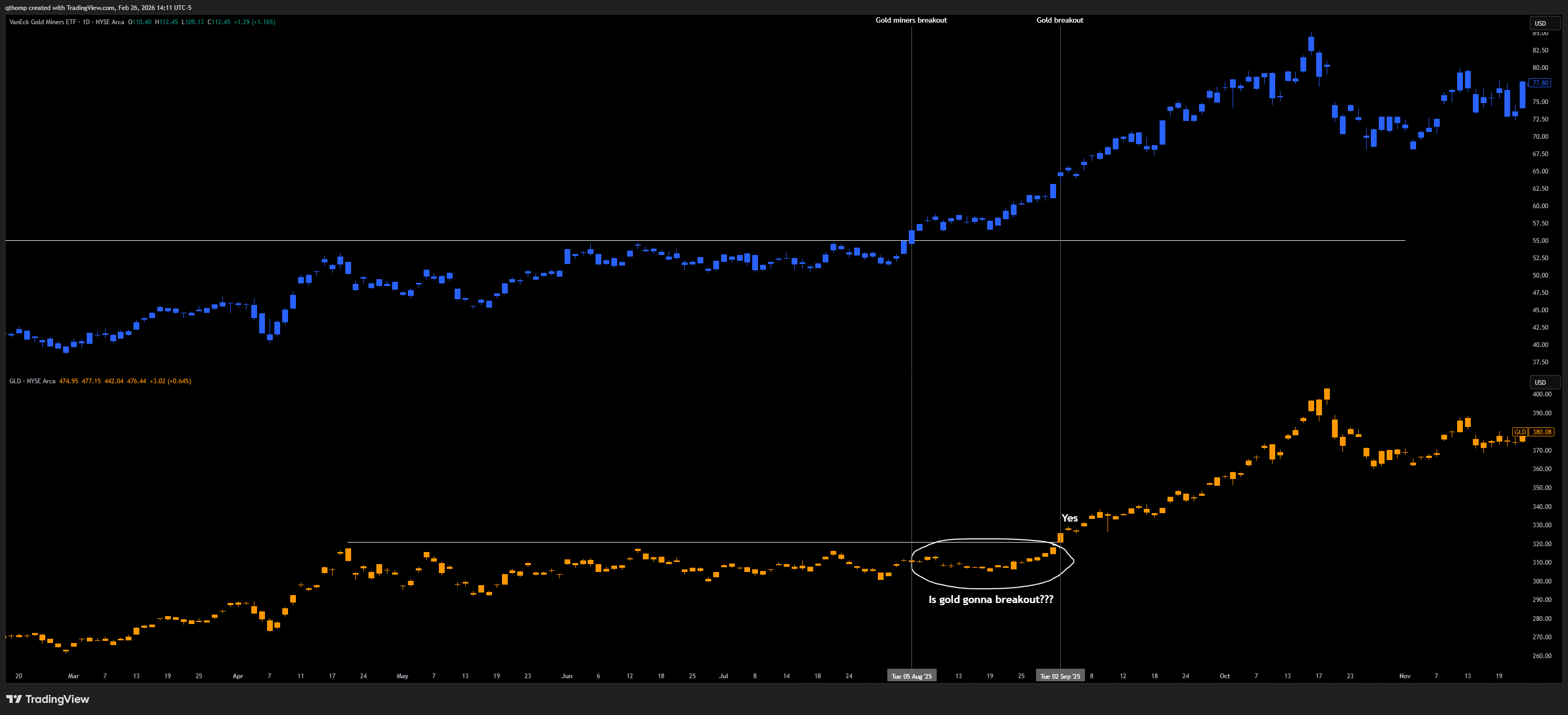

6:37 PM · Dec 22, 2025 · 22.1K Views14 Replies · 5 Reposts · 78 LikesI am reminded of the GDX breakout last summer preceding gold’s breakout by about a month that had a lot of anxious eyes on it wondering if gold will follow. We all know what gold has done since. The recent move in XLE has been decisive as well, up over +20% in less than 2 months to start the year. While yes there is obviously some geopolitical premium in the price of oil right now, I’d trust this move longer-term.

Heck, who’s to say the geopolitical premium should even go away anytime soon given seemingly every week there’s a headline of Ukraine and Russia hitting another oil pipeline or refinery. After all, Russia is still the 3rd largest oil producer in the world.

On Friday afternoon in the chat, I posted about a new long I started building this week which is now a large position for me. We like a basket of natural gas exposure here as prices have fallen back into value territory with many catalysts and ways to win still ahead. Our names are EQT, AR, RRC, CRK, CNX, EXE.

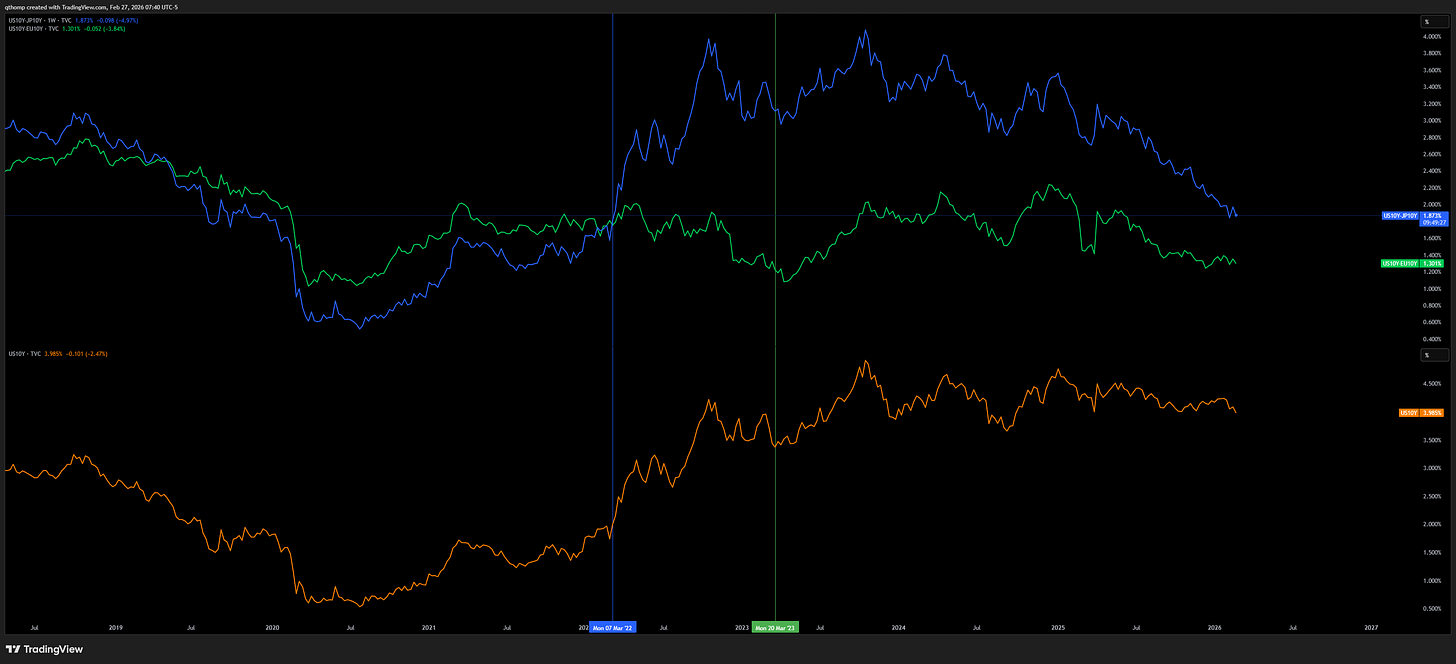

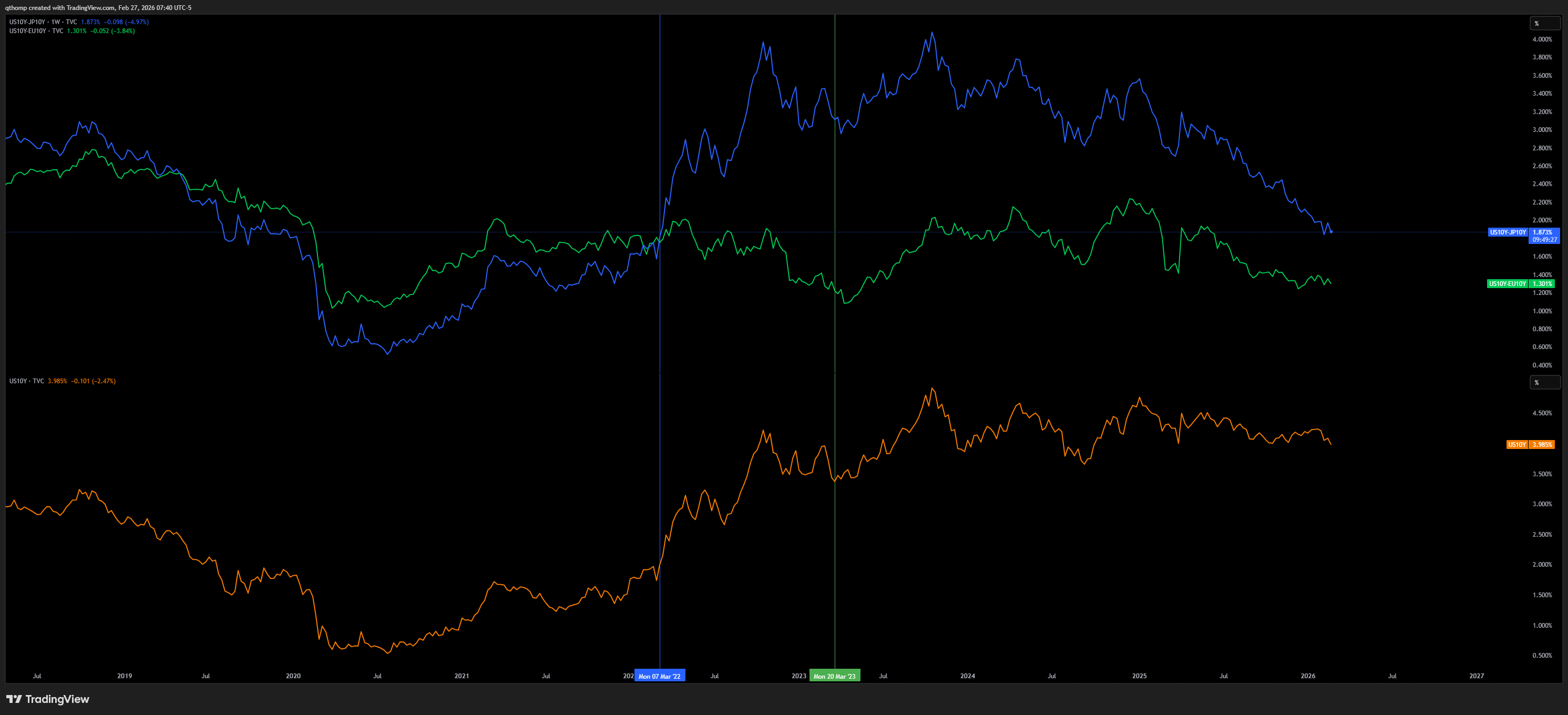

Don’t be lulled into Treasuries.

US 10y nominal yield differentials versus Japan and Europe are at their lowest since March 2022 and March 2023, respectively. Both of those proved to be horrendous times to own Treasuries.

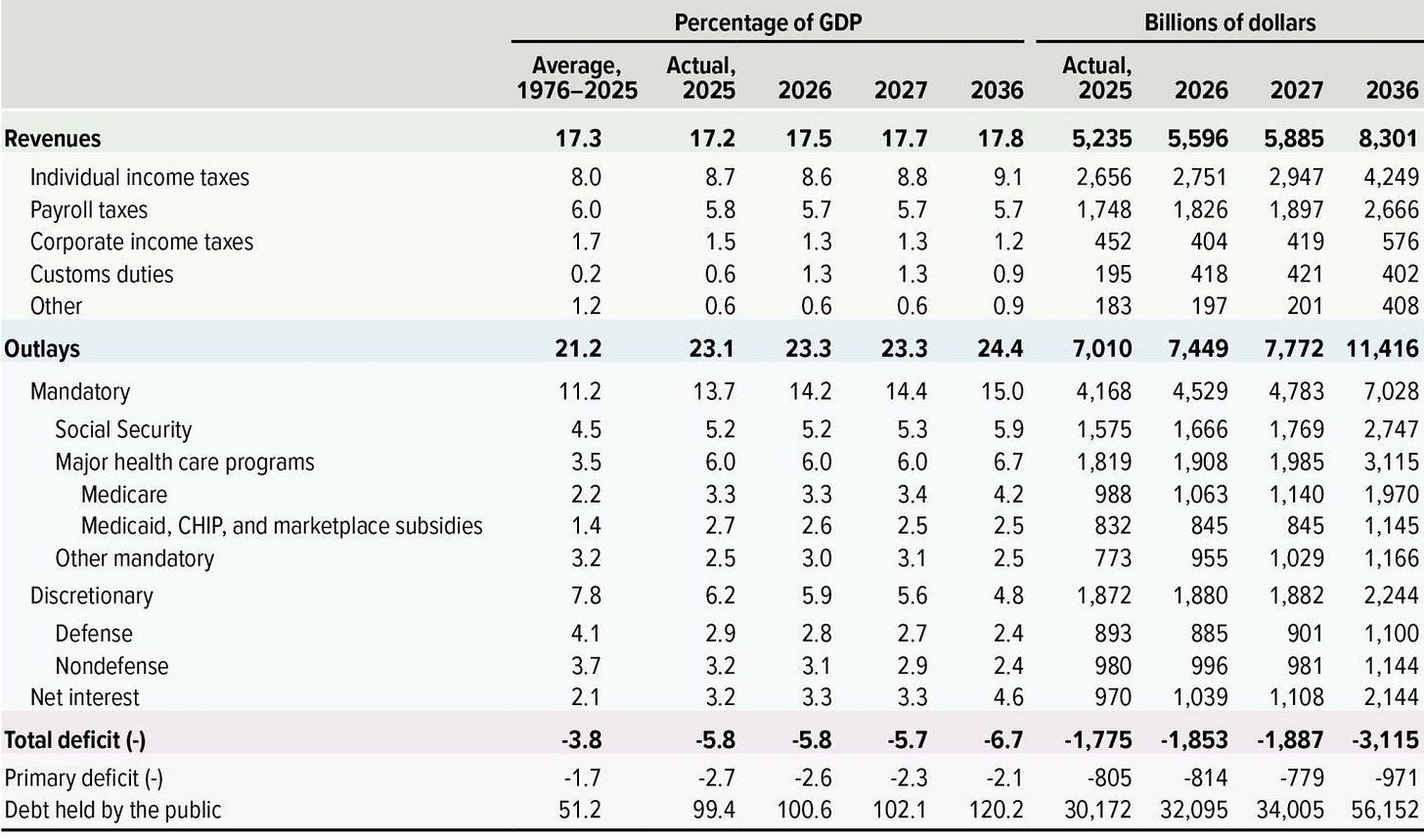

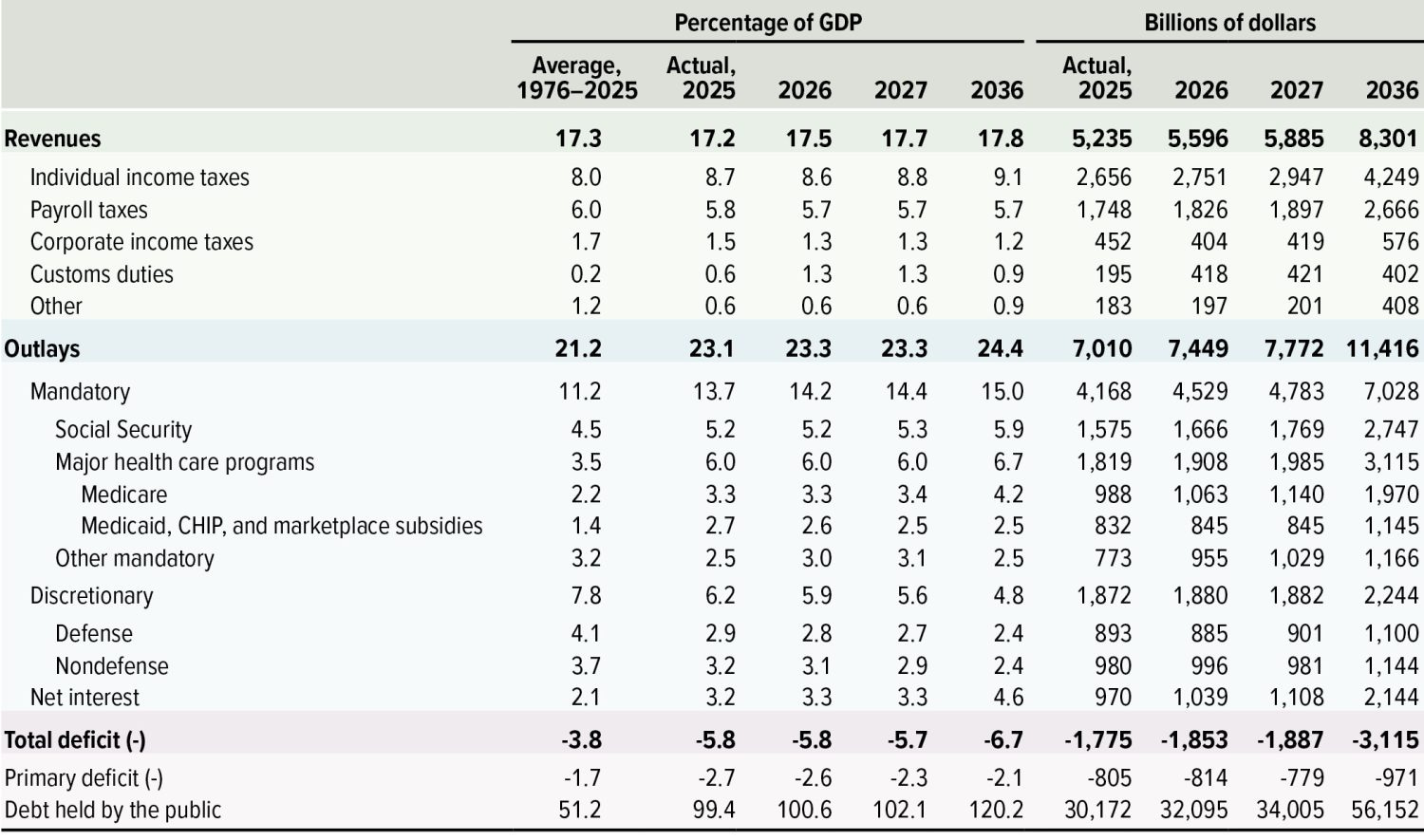

In the short-term assets trade off sentiment and flows, in the long-term they trade off fundamentals. What’s changed? Sentiment has turned fearful as AI advancements have created new risks of mass labor displacement leading to layoffs. We also have the Fed resuming $500B per year in balance sheet expansion to support the sovereign bond market alongside a recent QRA hinting at coordination with the Treasury to further alleviate long duration pressures. Long-term, the picture has not changed and the deficits are still not in check. The recent updated CBO forecasts are still showing consistent 5.5-6.0% deficits with no end in sight. If anything, job losses make matters worse as the government collects less income and capital gains tax revenues. The picture is bleak and owning bonds will not save you. Gold is the new risk off safe haven.

Quinn Thompson@qthompThis month the CBO released their first updated budget projection since January 2025. In short, there is no solution in sight to reduce the fiscal deficit. 7:29 PM · Feb 23, 2026 · 3.85K Views3 Replies · 1 Repost · 34 Likes

7:29 PM · Feb 23, 2026 · 3.85K Views3 Replies · 1 Repost · 34 Likes

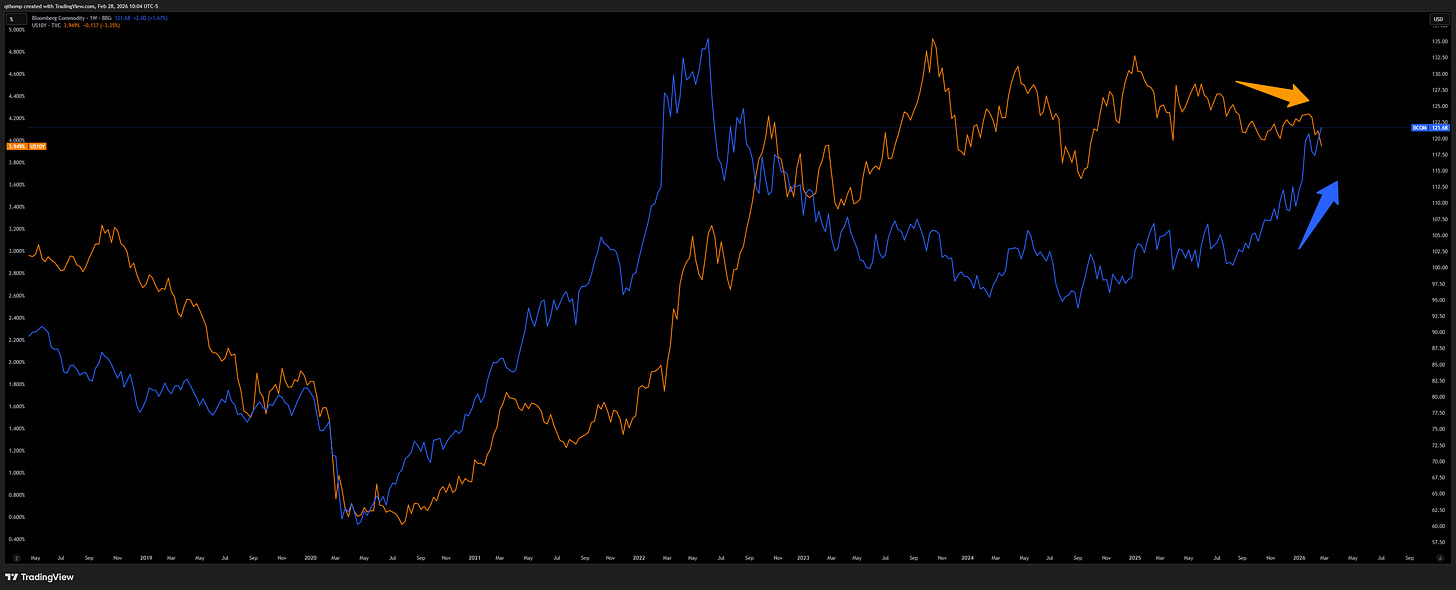

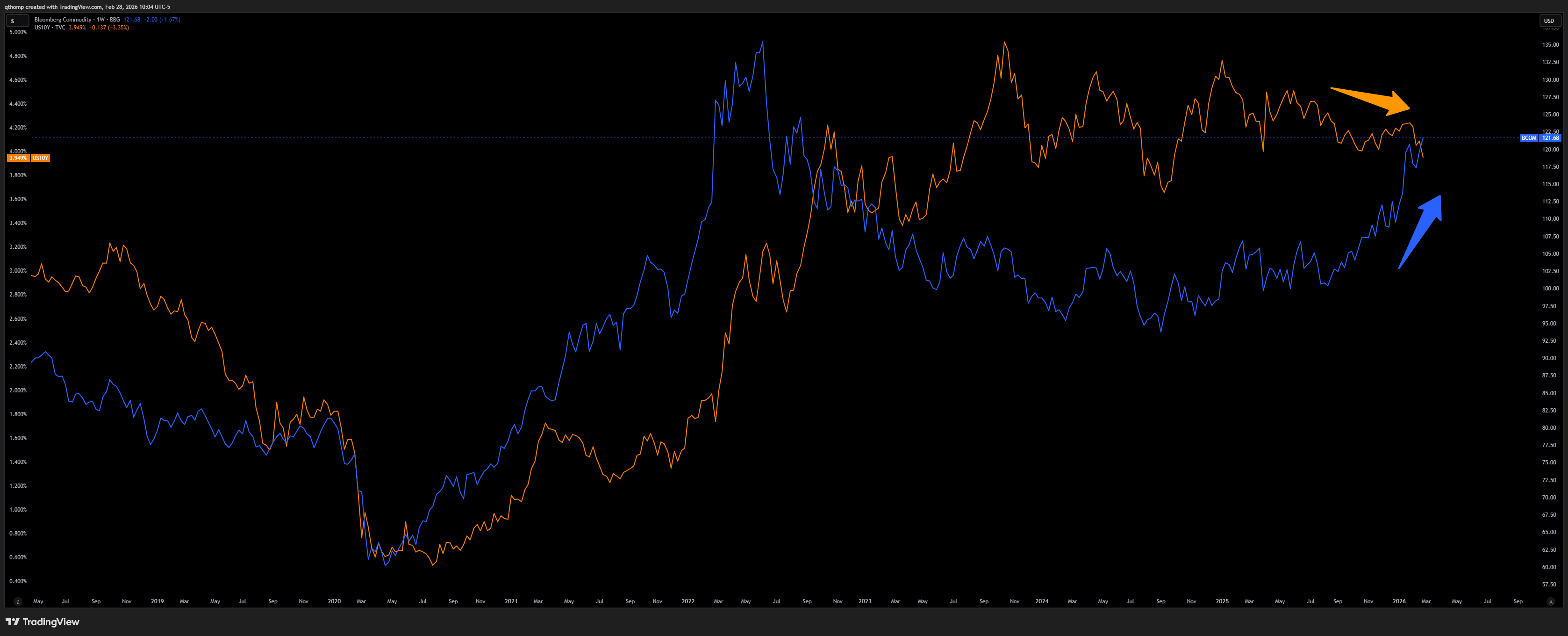

I question how long this divergence with commodities can last.

Market structure is such that we are less likely to see a violent move lower, but that does not mean we don’t move lower.

I have noticed many pointing out the level of hedging, put skew and short selling in the market as a reason to be bullish. My take is more nuanced. While yes, this market structure limits how quickly and violently the market can unravel, it does not prevent the direction of travel altogether.

Similar to 2022, I think we are entering a structurally higher volatility environment which is not surprising to anyone given the plethora of boiling pots out there.

Hedging metrics and put skew are elevated - many investors are seeing the same risk factors. I’ve been writing for a few weeks now that this sell off is going to frustrate the hell out of people - it’s a slow bleed for a reason. The Fed is behind the curve, the labor market is still weakening and there is no new fiscal stimulus yet announced. This also shouldn’t surprise anyone as 2022 was a bad year for financial markets but great for main street and ultimately helped Biden significantly outperform in midterms.

How to play this environment? Expect violent rotations to continue and it may help to focus on a long/short portfolio in many instances instead of outright short. If it feels like every time the Nasdaq is on the precipice of breaking down, that’s the hedged market structure for you. But that doesn’t mean it can’t slowly grind down, burning put holders theta and frustrating short sellers with the constant down, up, down chop. Invest in assets in bull markets, charts going from bottom left to top right. Short assets in bear markets, charts going from top left to bottom right.

This week we have labor market data ending with NFP on Friday. No strong views on the month to month reports but if I were to guess there’s greater risk of showing weakness and maybe some reversal of January’s gains, rather than strength. I think between this and other signs of problems across the markets and economy, Fed cut odds for April/June could increase and lead to yield curve steepening. The curve remains too flat and nominal yields too low.

On top of that we have the Iran situation ongoing. While I saw many celebrating the decimation of Iran’s leadership as a bullish catalyst on fintwit, I disagree. While we didn’t see any worst case outcomes (yet) in the attacks, I don’t think any of it is bullish. It’s still a net positive for commodity prices and all else equal that’s bad for financial assets and economic growth. Regime change in a hostile country with 90 million people does not resolve in a weekend.

Come join us in the chat. One thing you’ll notice is I have my core views, theses and biases that I structure my book around. For smaller and newer ideas, I sometimes have a ‘throw shit at the wall and see what sticks’ approach in my trading. I use the chat to try and offer a glimpse into my real-time thinking. It’s my hope that it is additive to readers’ processes, offering differentiated views and thought provoking ideas. It’s pretty cool to see some of these daily threads getting 100-200+ replies. Participation is what creates healthy and flourishing environments that help everyone be better. I appreciate all of you who are active in the community.

Thanks Quinn. As always, appreciate you sharing your insights.

thanks Quinn, great insights.