Scouting the Tape - Mar 13, 2026

(Unique) macro idea generation and (insightful) market thoughts.

If I could summarize my current view as succinctly as possible, I’d say:

It’s time to stop buying the little dips. The big dip is coming.

If you’ve been following our work, you know we’ve been the big ugly bear over the last few weeks, emphasizing caution. fejau and I recorded another Forward Guidance episode yesterday and the link is below. Please send Tyler get well wishes as he is out sick and could not make this one.

Why agricultural commodities are a screaming buy.

Wheat, corn, sugar, soybeans and all agricultural commodities have traded well following the start of the Iran war.

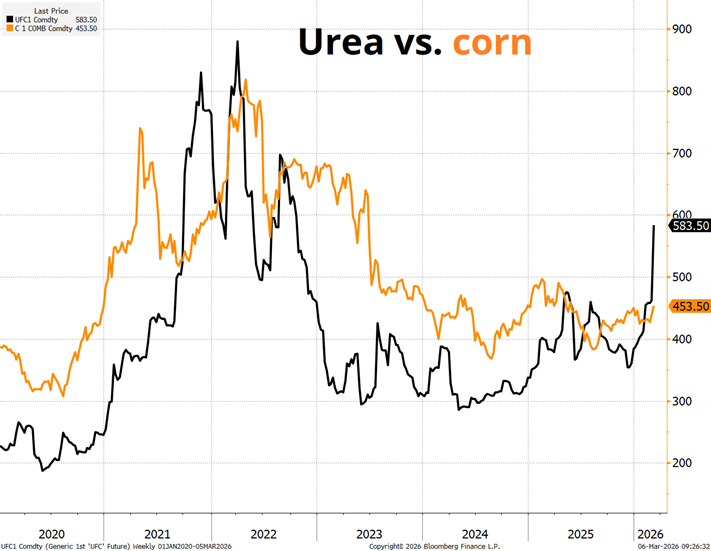

Unlike oil where developed countries have strategic reserves and the ability to restart production at any time, agricultural commodities have particular seasons dictated by weather. We are approaching the spring peak for fertilizer demand in March to May where 50-75% of annual fertilizer is applied just before or during planting. This is why it’s a problem that ~1/3 of the world’s seaborne fertilizer trade passes through the Strait of Hormuz and for individual types like Urea and Sulfur, its closer to 50%.

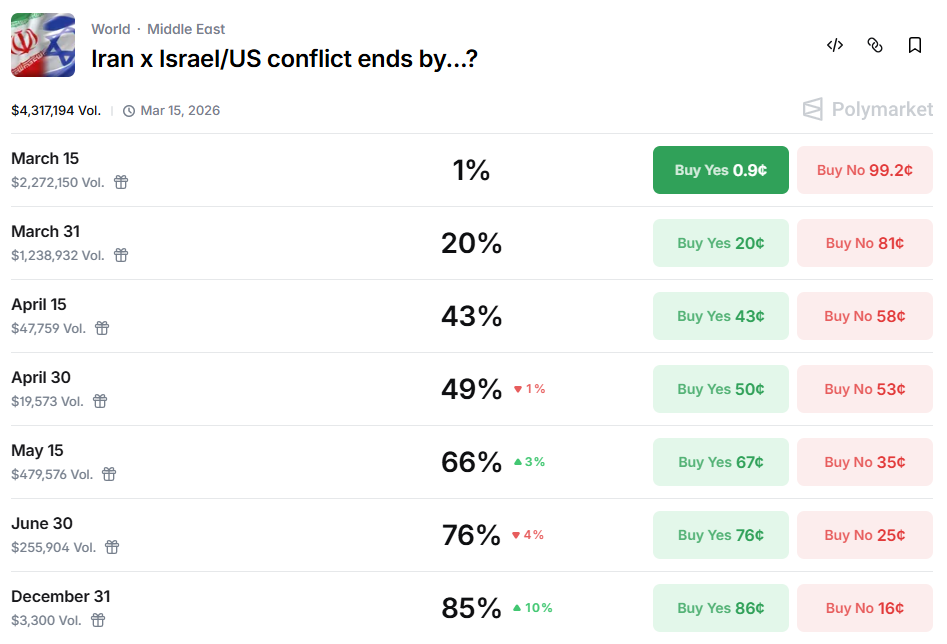

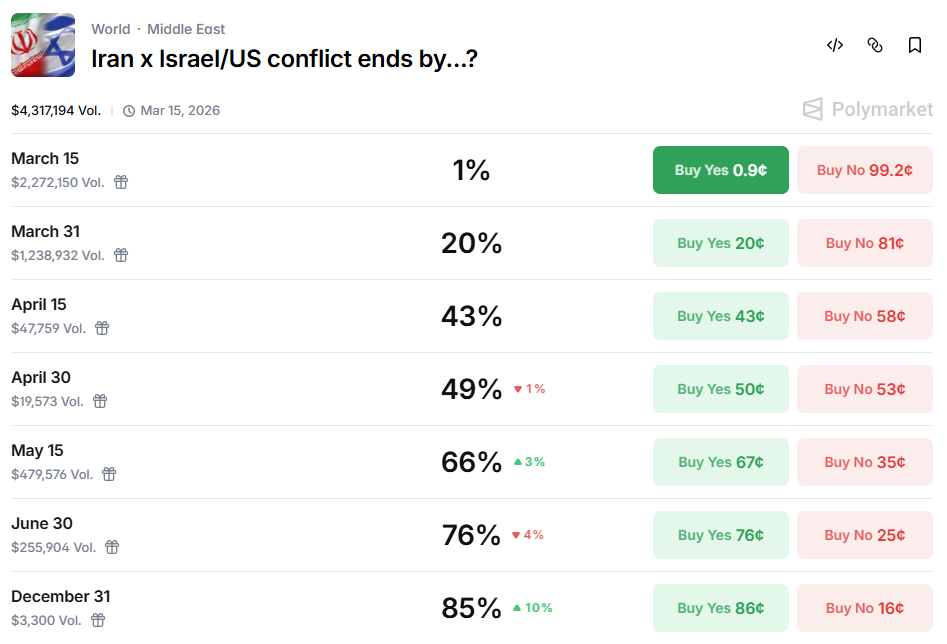

Current Polymarket odds show the Iran conflict to end in ~May. This is a massive problem if the Strait of Hormuz doesn’t open until May.

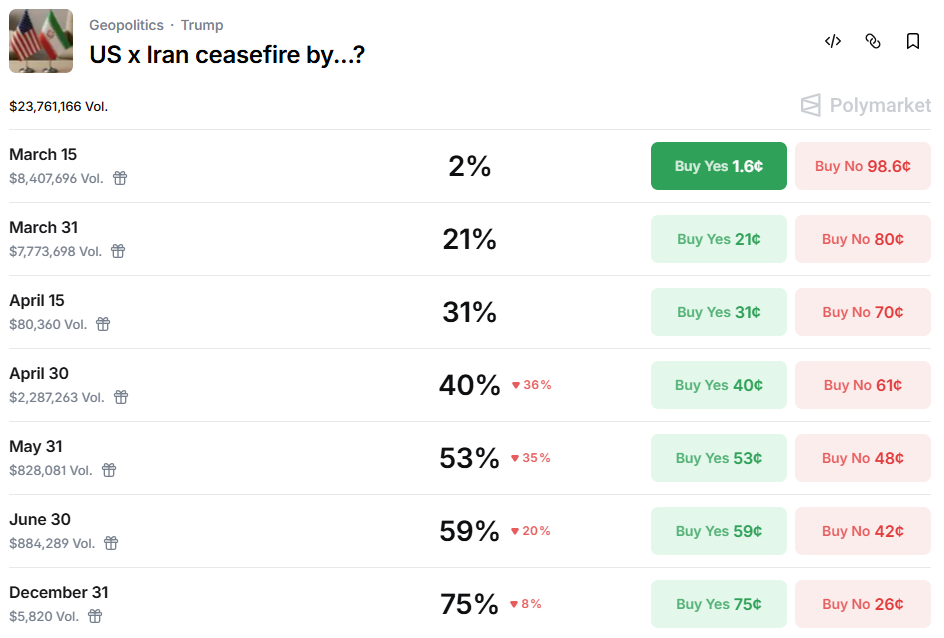

With a ceasefire by ~June.

Food prices tend to follow oil prices.

*Walter Bloomberg@DeItaoneHORMUZ CLOSURE CRIPPLES FOOD SECURITY UN Trade and Development warns the Strait of Hormuz disruption—traffic down 97%—is spiking energy, fertilizer, transport, and insurance costs, echoing Covid-19 and Ukraine war shocks. With 20% of global oil/LNG and one-third of seaborne

*Walter Bloomberg@DeItaoneHORMUZ CLOSURE CRIPPLES FOOD SECURITY UN Trade and Development warns the Strait of Hormuz disruption—traffic down 97%—is spiking energy, fertilizer, transport, and insurance costs, echoing Covid-19 and Ukraine war shocks. With 20% of global oil/LNG and one-third of seaborne 4:23 PM · Mar 10, 2026 · 82.2K Views33 Replies · 155 Reposts · 572 Likes

4:23 PM · Mar 10, 2026 · 82.2K Views33 Replies · 155 Reposts · 572 LikesThere is another key element to price action and the long thesis that most aren’t connecting the dots to.

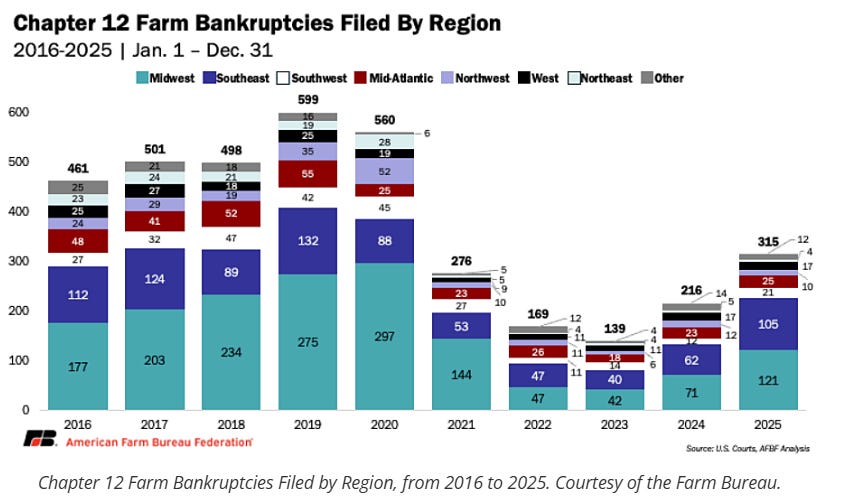

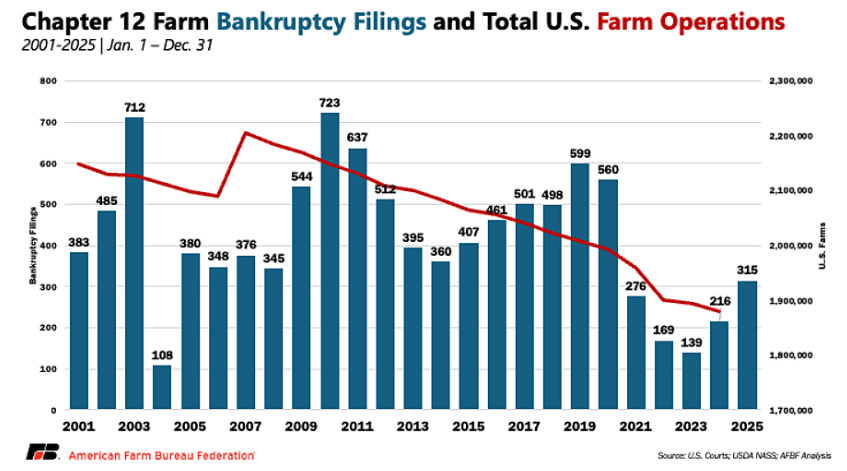

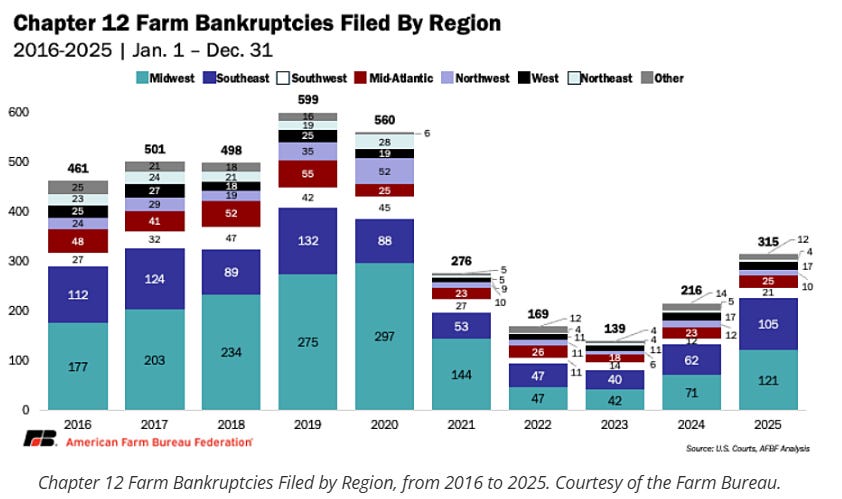

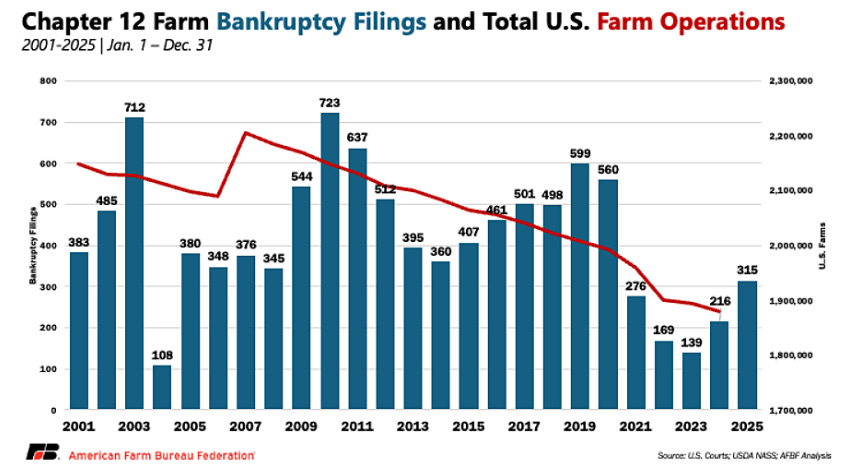

Farm bankruptcies are accelerating as they face the most severe gap between their production costs (seeds, fertilizer and fuel) relative to market prices received for their crops (corn, soybeans, etc.).

The financial squeeze is severe as the volume of new farm operating loans rose nearly 40% in Q4 and over 20% in 2025. This comes at a time when total US farm operations have been in a secular decline for multiple decades. There is no relief in sight.

The US farming industry is in a recession, full stop, and the only way out is higher prices for their agricultural production.

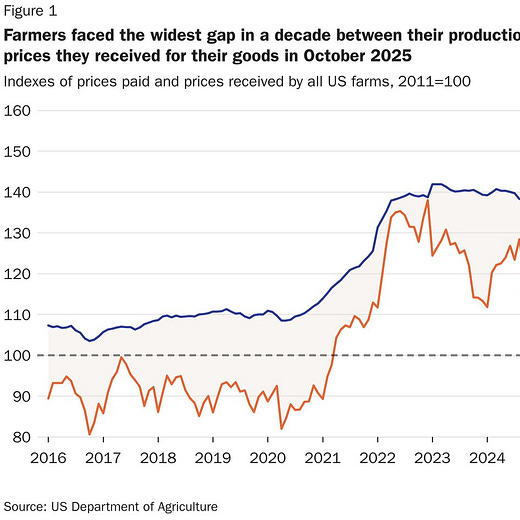

Scott Lincicome@scottlincicome"Farm bankruptcies in the first half of 2025 exceeded the total for all of 2024. In October 2025, the gap between farmers’ production costs and the prices they received for their goods was the widest in a decade.... Erratic tariff policies squeeze farmers from both sides."

Scott Lincicome@scottlincicome"Farm bankruptcies in the first half of 2025 exceeded the total for all of 2024. In October 2025, the gap between farmers’ production costs and the prices they received for their goods was the widest in a decade.... Erratic tariff policies squeeze farmers from both sides."

6:20 PM · Jan 23, 2026 · 30.9K Views17 Replies · 175 Reposts · 348 Likes

6:20 PM · Jan 23, 2026 · 30.9K Views17 Replies · 175 Reposts · 348 Likes

So to put it all together, you have a massive supply shortage induced price spike in two key agricultural inputs (fuel and fertilizer) on the doorstep of peak spring planting season while farmers are in one of the worst agricultural recessions ever faced. Food is also not like oil where as prices go up people can fly and drive less as demand can be more elastic. It’s behind oxygen and water as the most bare necessities with inelastic demand.

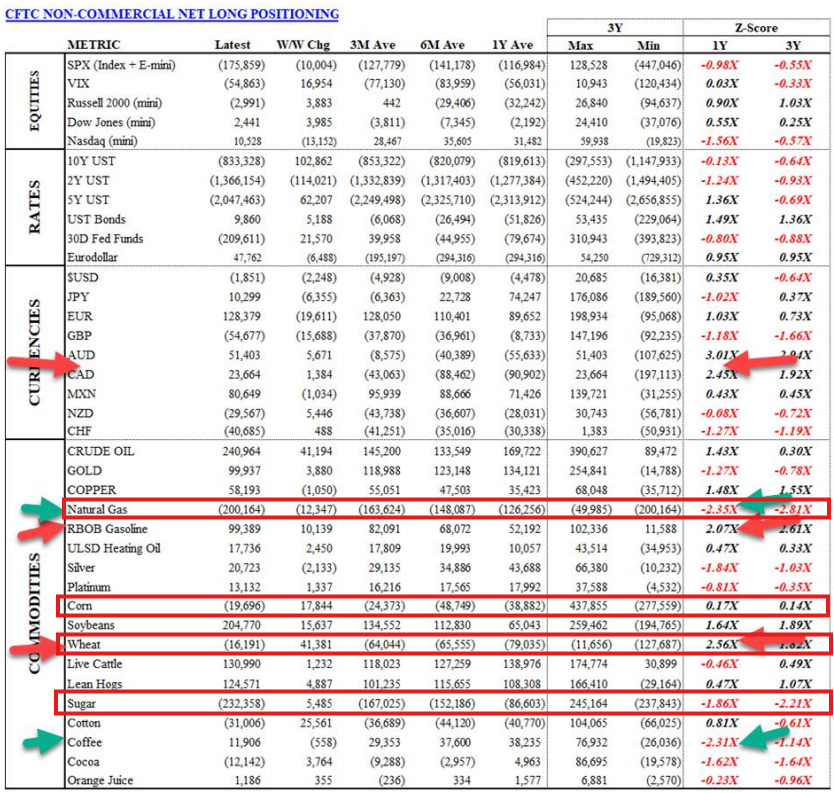

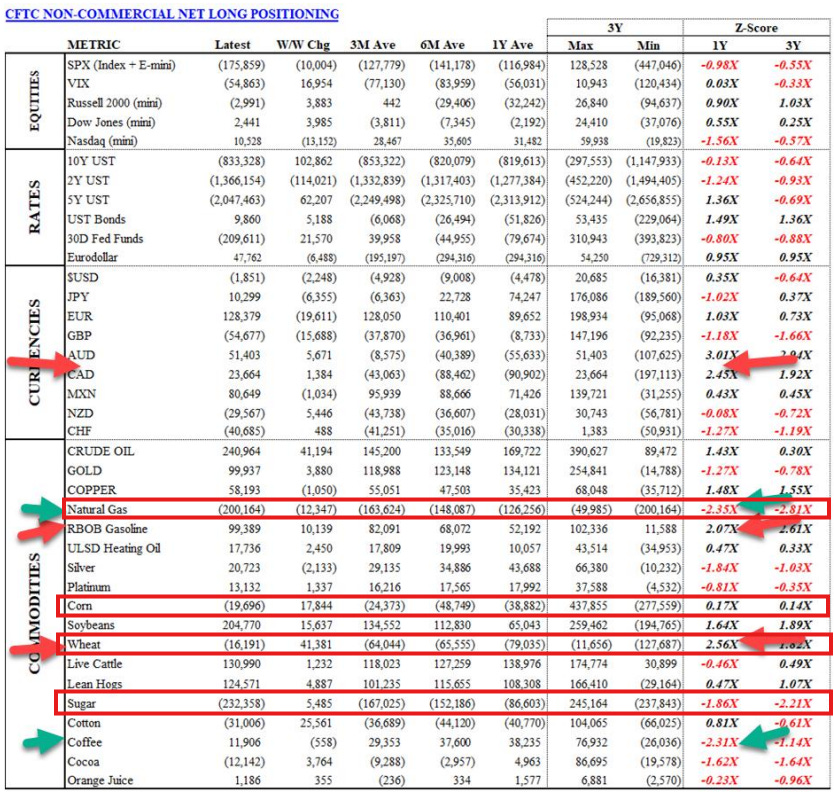

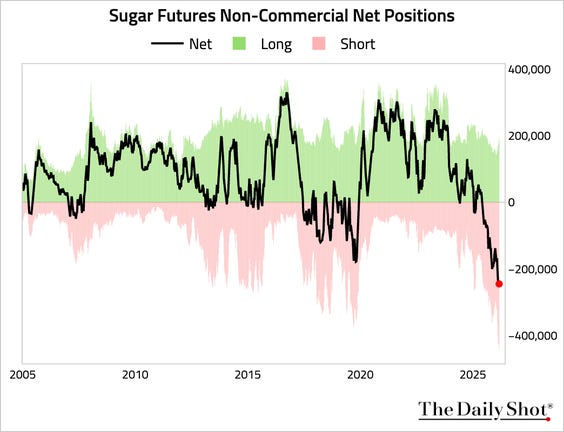

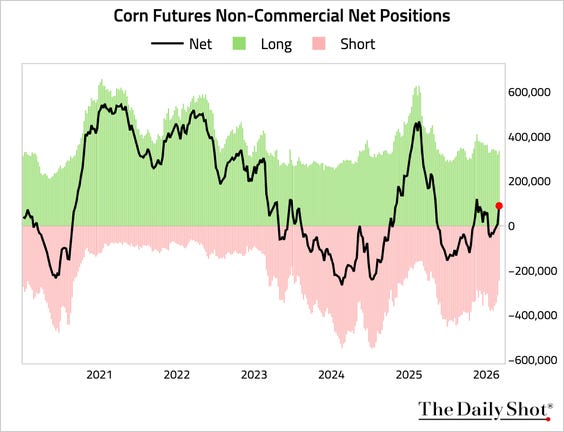

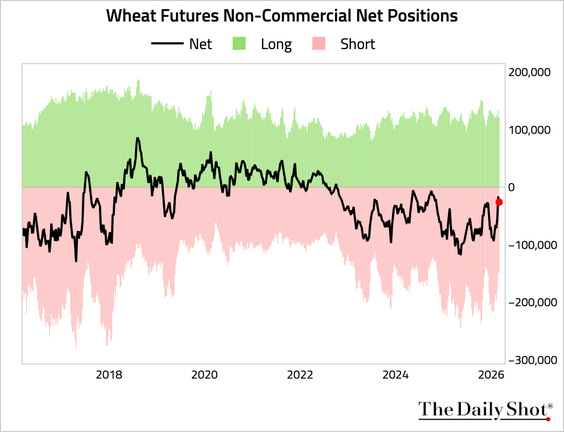

Non-commercial net long futures positioning is still short in most of these assets.

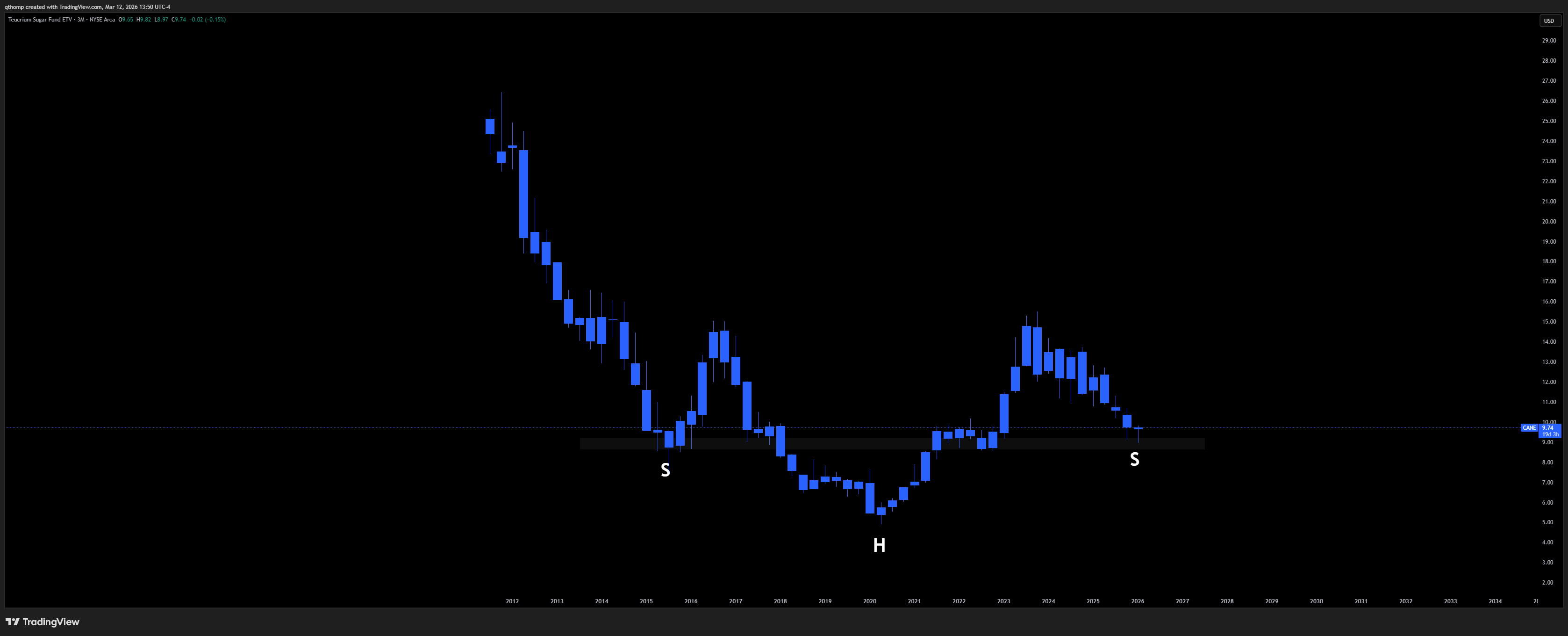

Sugar

Corn

Wheat

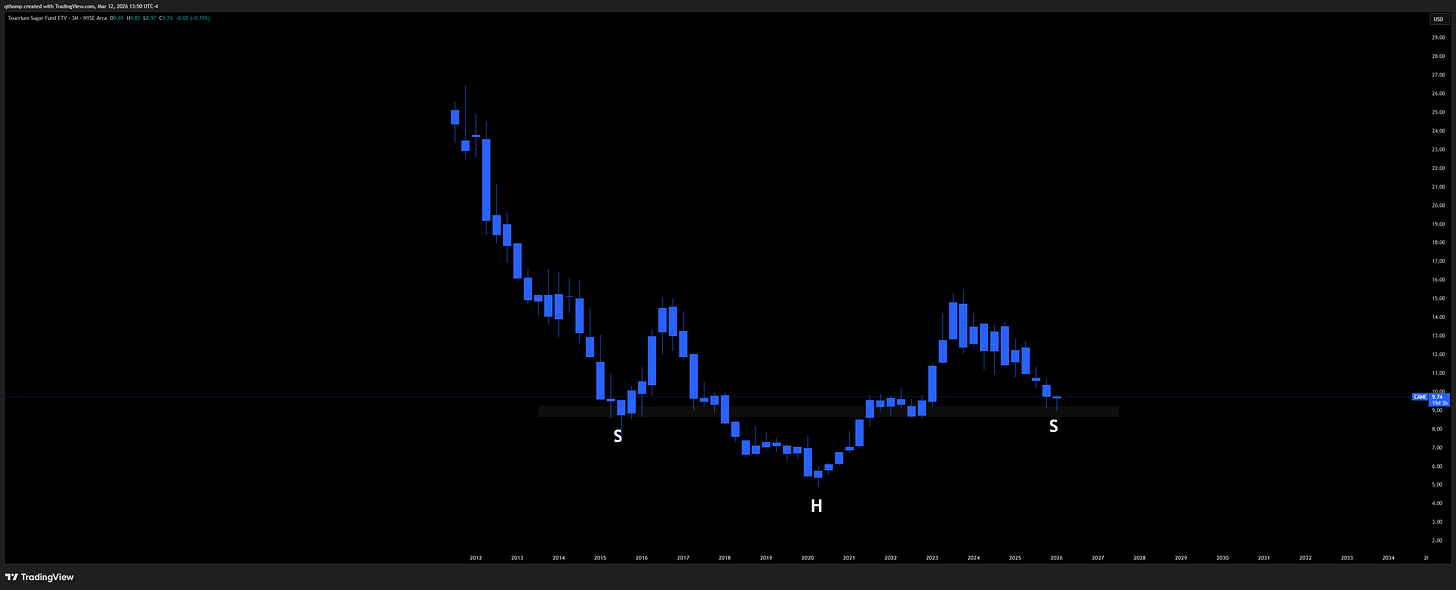

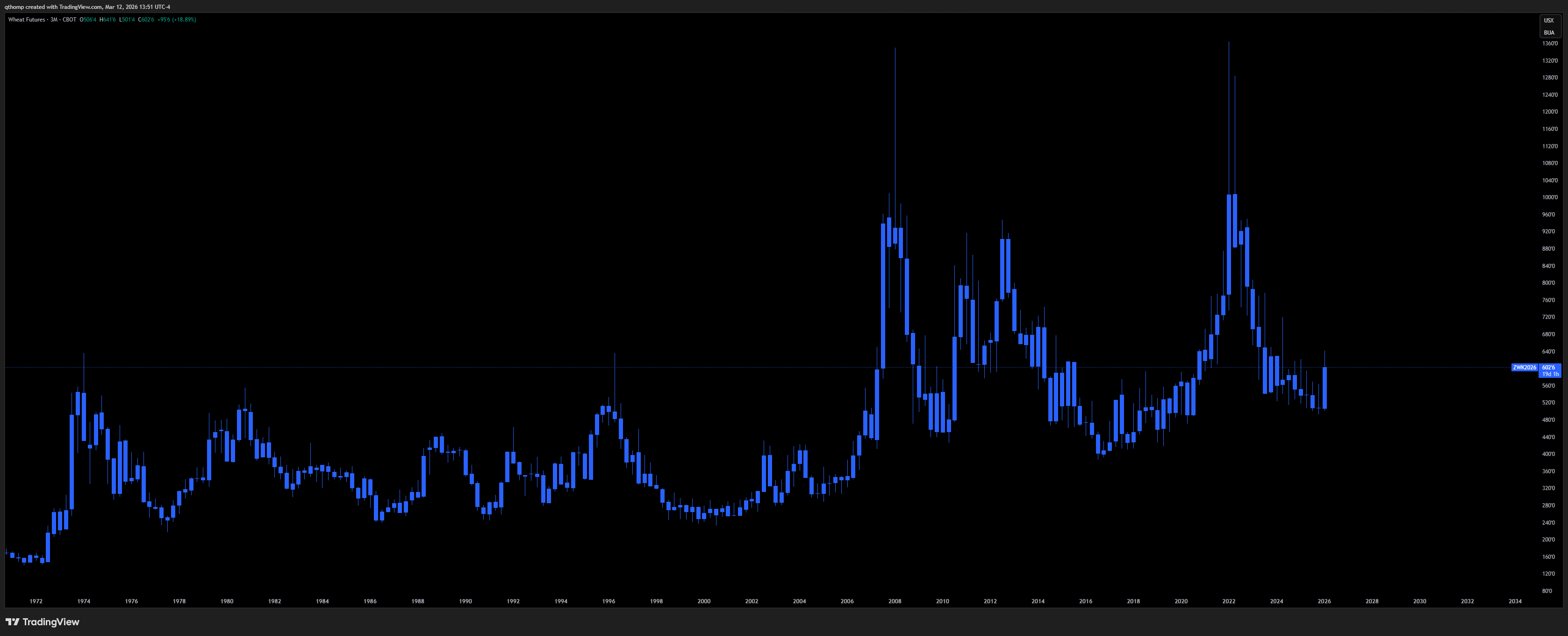

The only cure for this dilemma is higher food prices, which is why we are long the whole complex - wheat, corn, soybeans, sugar. This complex is our largest long position and it’s not close. Some of these long-term charts look insane.

CANE - sugar

CORN

WHEAT

Oil and gas equity dynamics.

I want to call attention to a few considerations around oil and gas equities that have me still bullish the sectors.

Quinn Thompson@qthomp@dampedspring To your point about L/S positioning, can kind of see it play out on the gap ups in front month futures and equities falling. I hear you on long-term forward curve mattering most. Interesting to see the point in the price rise where $XLE stopped going up. I'm not as long them as

Quinn Thompson@qthomp@dampedspring To your point about L/S positioning, can kind of see it play out on the gap ups in front month futures and equities falling. I hear you on long-term forward curve mattering most. Interesting to see the point in the price rise where $XLE stopped going up. I'm not as long them as 7:54 PM · Mar 6, 2026 · 11.2K Views1 Reply · 12 Likes

7:54 PM · Mar 6, 2026 · 11.2K Views1 Reply · 12 LikesThere is no immediate help coming from US producers.

Quinn Thompson@qthompThe low level of active US oil and gas rigs indicate a quick ramp in production is unlikely without sustained high oil prices and higher E&P company share prices.

Quinn Thompson @qthomp@dampedspring To your point about L/S positioning, can kind of see it play out on the gap ups in front month futures and equities falling. I hear you on long-term forward curve mattering most. Interesting to see the point in the price rise where $XLE stopped going up. I'm not as long them as7:00 PM · Mar 8, 2026 · 7.29K Views35 Likes

Quinn Thompson @qthomp@dampedspring To your point about L/S positioning, can kind of see it play out on the gap ups in front month futures and equities falling. I hear you on long-term forward curve mattering most. Interesting to see the point in the price rise where $XLE stopped going up. I'm not as long them as7:00 PM · Mar 8, 2026 · 7.29K Views35 LikesIt should be everyone’s base case that this conflict is more akin to Russia-Ukraine than it is like previous multi-day Israel-Iran skirmishes.

Quinn Thompson@qthompOil is +30% since this tweet Quinn Thompson @qthompThere is a lot to be learned from markets following the Russia-Ukraine invasion, except this conflict is larger and more complex. Russia (140M ppl) invaded Ukraine (40M ppl). This conflict involves more countries, supply chains, resources and critical geography.1:21 PM · Mar 9, 2026 · 5.97K Views31 Likes

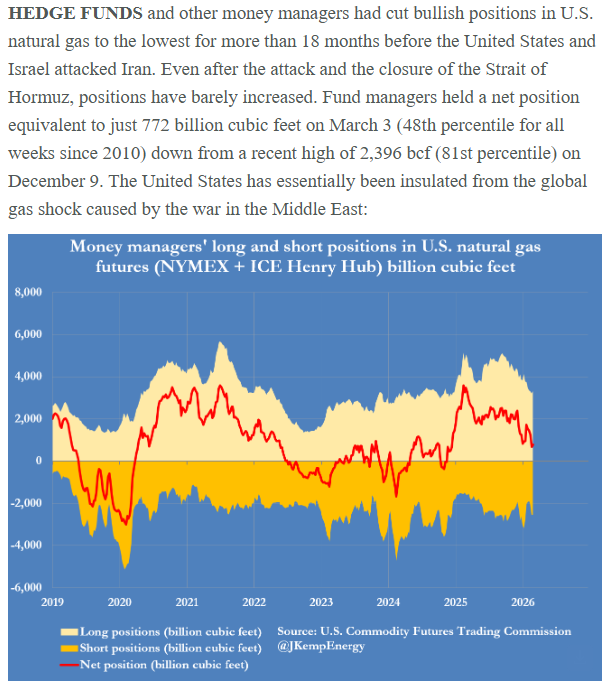

Quinn Thompson @qthompThere is a lot to be learned from markets following the Russia-Ukraine invasion, except this conflict is larger and more complex. Russia (140M ppl) invaded Ukraine (40M ppl). This conflict involves more countries, supply chains, resources and critical geography.1:21 PM · Mar 9, 2026 · 5.97K Views31 LikesMeanwhile no one trading US natural gas seems to care.

And in Asia and Europe, natural gas is trading for over 5x the cost of the same molecule in the US which has to do with 1) the US being the largest oil and gas producer in the world but 2) developed countries in Asia and Europe were running the lowest inventory stockpile levels in years going into this.

Quinn Thompson@qthompEuropean natural gas is trading at >5x US natural gas prices. Last time this was the case was August 2024. $EQT $AR $RRC $CRK $CNX $EXE Quinn Thompson @qthompI don't think people appreciate how low global natural gas inventories are - Europe in particular, but SK and others too. The rise in LNG has allowed for less stockpiling but opens up shortage risks in times like these. Long $EQT $AR $RRC $CRK $CNX $EXE and my coal basket too. https://t.co/EzkuR5HWYs4:08 PM · Mar 3, 2026 · 5.75K Views1 Reply · 1 Repost · 33 Likes

Quinn Thompson @qthompI don't think people appreciate how low global natural gas inventories are - Europe in particular, but SK and others too. The rise in LNG has allowed for less stockpiling but opens up shortage risks in times like these. Long $EQT $AR $RRC $CRK $CNX $EXE and my coal basket too. https://t.co/EzkuR5HWYs4:08 PM · Mar 3, 2026 · 5.75K Views1 Reply · 1 Repost · 33 Likes

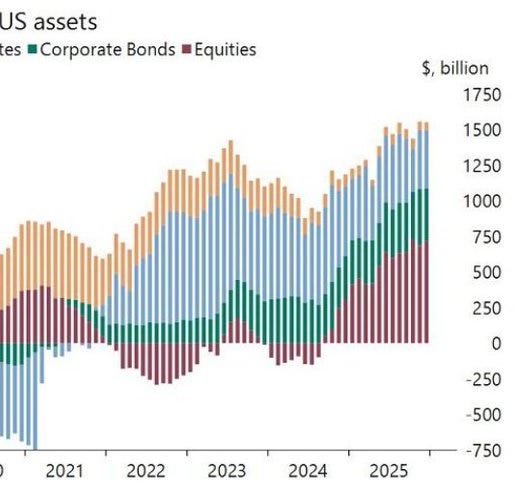

Which currency is the safe haven?

Piggybacking off my prior energy point, the below gives a sense of how big of a problem Japan has. I talked about this in last week’s Scouting the Tape as well.

Quinn Thompson@qthompIt's going to be something to watch what Japan does here. Look the other way as their currency goes to zero while their bond market implodes and stocks blow off? Or intervene to prevent a future inflation problem? My bet is on the latter. Oil is +10% in Yen already YTD. 8:26 PM · Jan 13, 2026 · 16.5K Views5 Replies · 1 Repost · 62 Likes

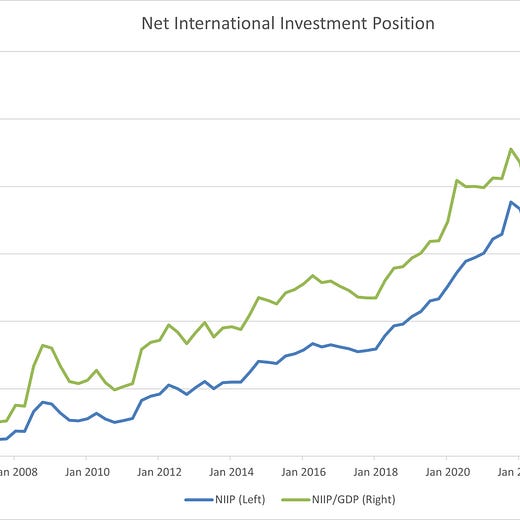

8:26 PM · Jan 13, 2026 · 16.5K Views5 Replies · 1 Repost · 62 LikesOn the other hand, the balance of global capital flows creates a major headwind for the US dollar and denominated assets. Given this problem and the challenges facing US bonds that I’ve discussed in the past, I really don’t like being long dollars either.

Quinn Thompson@qthomp@fejau_inc I want to agree given the US is the world's most dominant energy power as the largest oil and gas producer globally. However, my argument for this time being different is that the Net International Investment Position in US assets has never been larger both outright and as a %

7:34 PM · Mar 8, 2026 · 13.5K Views4 Replies · 4 Reposts · 66 Likes

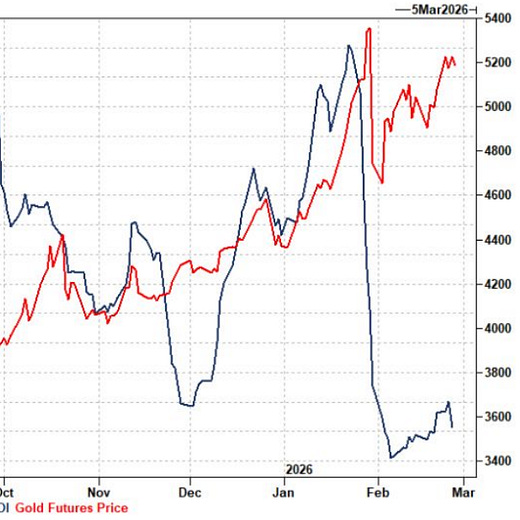

7:34 PM · Mar 8, 2026 · 13.5K Views4 Replies · 4 Reposts · 66 LikesWell that leaves us with the only non-printable store of value / currency as gold. For these reasons above and no end in sight to the underlying fundamental drivers of the issues at hand, you will not see me get bearish gold anytime soon. I also love that positioning has been flushed. My base case from here is that the dollar rises and that could cause some short-term pain for gold, but I do like how it is trading nonetheless.

Quinn Thompson@qthompNew @ForwardGuidance chartbook just dropped for this week's episode. Wanted to call out a few we did not discuss live on the pod. Takeaway: Gold positioning length has been absolutely flushed (and these charts are few days old, before the recent DXY spike). Long $GLD $GDX

6:46 PM · Mar 6, 2026 · 10.4K Views5 Replies · 2 Reposts · 67 Likes

6:46 PM · Mar 6, 2026 · 10.4K Views5 Replies · 2 Reposts · 67 LikesIt really does seem like 2026 is going to be a game of hot potato across commodities. You probably should do yourself a favor and just put every single commodity ticker on your watchlist right now. It’s quite remarkable to finally see this all play out in real-time - it truly is a time to buy stuff you can’t print. Etch that into your brain and keep your head on a swivel for the next rotation. I think agriculture has a lot of room to run from here and my focus is there, but my guess is over the next few weeks we also get amazing buying opportunities in others. This is the place to be in 2026.

Bonds-R-F’d.

This is just your weekly reminder that long duration sovereign bonds are a horrible place to store wealth.

Quinn Thompson@qthompWelcome, how may I help you?

Skanda Amarnath @IrvingSwisherBefore adding in geopolitical inflation risk, goods inflation outside food and energy is already running about 3% faster than what prevailed for most of the last 3 decades Much of this is tariffs, but bottlenecks from the AI boom are also starting to weigh more heavily3:00 PM · Mar 11, 2026 · 5.36K Views1 Reply · 52 Likes

Skanda Amarnath @IrvingSwisherBefore adding in geopolitical inflation risk, goods inflation outside food and energy is already running about 3% faster than what prevailed for most of the last 3 decades Much of this is tariffs, but bottlenecks from the AI boom are also starting to weigh more heavily3:00 PM · Mar 11, 2026 · 5.36K Views1 Reply · 52 Likes

Short $NVDA.

I discussed two weeks ago that I believe semiconductors are topped, especially relative to the market. NVDA is potentially the most vulnerable name out there as it comprises nearly 8% of the S&P 500.

I love the risk / reward of a $192 weekly close stop loss with a $140-$150 price target and take profit level.

Quinn Thompson@qthompGot another chance to short $NVDA at $186 this morning. I will stop posting these daily reminders once it cascades through its 200 DMA. Quinn Thompson @qthompWith a stop loss at $192, where $NVDA has not been able to break out above, the risk is $10 from here with $40 upside (short) down to $142. Great risk / reward. Oh by the way, $NVDA is 7.7% of $SPY. Make sure you know what you own.2:38 PM · Mar 13, 2026 · 4.54K Views4 Replies · 35 Likes

Quinn Thompson @qthompWith a stop loss at $192, where $NVDA has not been able to break out above, the risk is $10 from here with $40 upside (short) down to $142. Great risk / reward. Oh by the way, $NVDA is 7.7% of $SPY. Make sure you know what you own.2:38 PM · Mar 13, 2026 · 4.54K Views4 Replies · 35 Likes

I really hate to be this big of a bear. Anyone who knows me knows I am a big optimist. I love life and the future couldn’t be brighter. But one of the gifts I’ve been given is that I don’t really care about consensus or falling in line and I am inclined to seek truth above all. Always keep an open mind.

Maximum caution ahead as we traverse March before possibly seeing some reprieve in April. I believe the path of least resistance for equities remains down, bonds remain a terrible investment and correlations across the market are rising making even the secularly winning sectors vulnerable to risk off moves. We prefer a long / short portfolio with agricultural commodities and energy on the long side and technology, semiconductor equities and bonds on the short side.

Have a nice weekend y’all. I wish health, peace and love to everyone. Stick together.

Thanks for the insight! I don’t work in this space, so the information you provide is extremely helpful for someone like me.