Scouting the Tape - Mar 7, 2026

(Unique) macro idea generation and (insightful) market thoughts.

I’m going to kick this week’s piece off with a quick ask. If you’ve enjoyed or benefited from reading these weekly blogs, please forward it to or share it with 3 friends who you think might also like it and tell them to sign up too. Thank you.

This market environment is one where my average hold period is down to effectively day trading and the importance of being nimble and open minded to changing information is as critical as ever.

We recorded our latest Forward Guidance on Thursday after the close but for most up to date real-time views, join the chat.

There’s a policy shift ongoing that is not being heavily discussed.

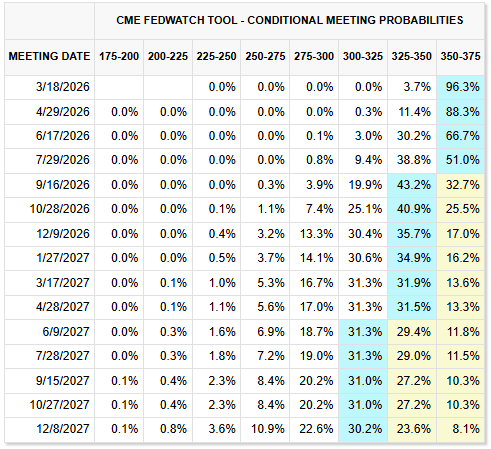

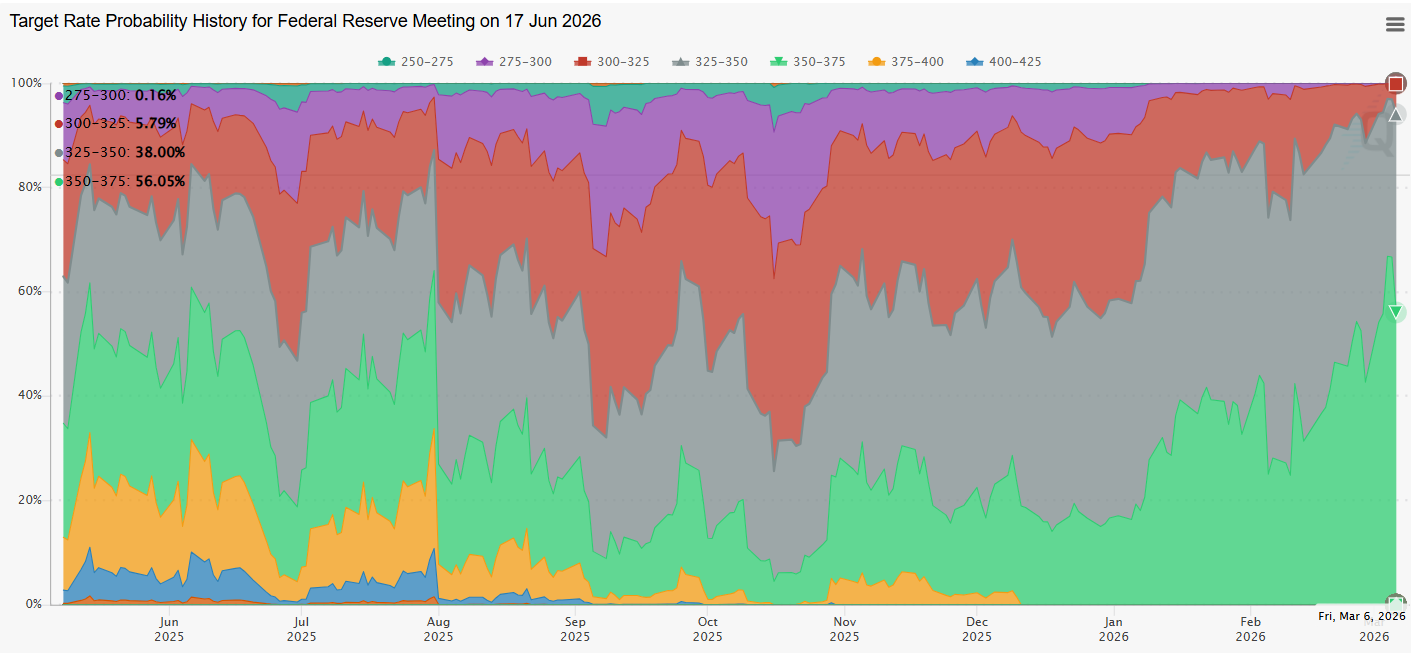

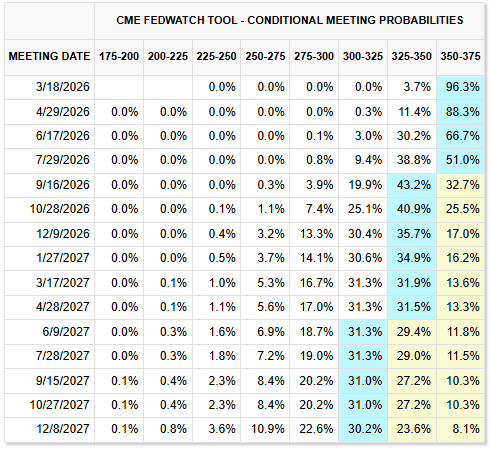

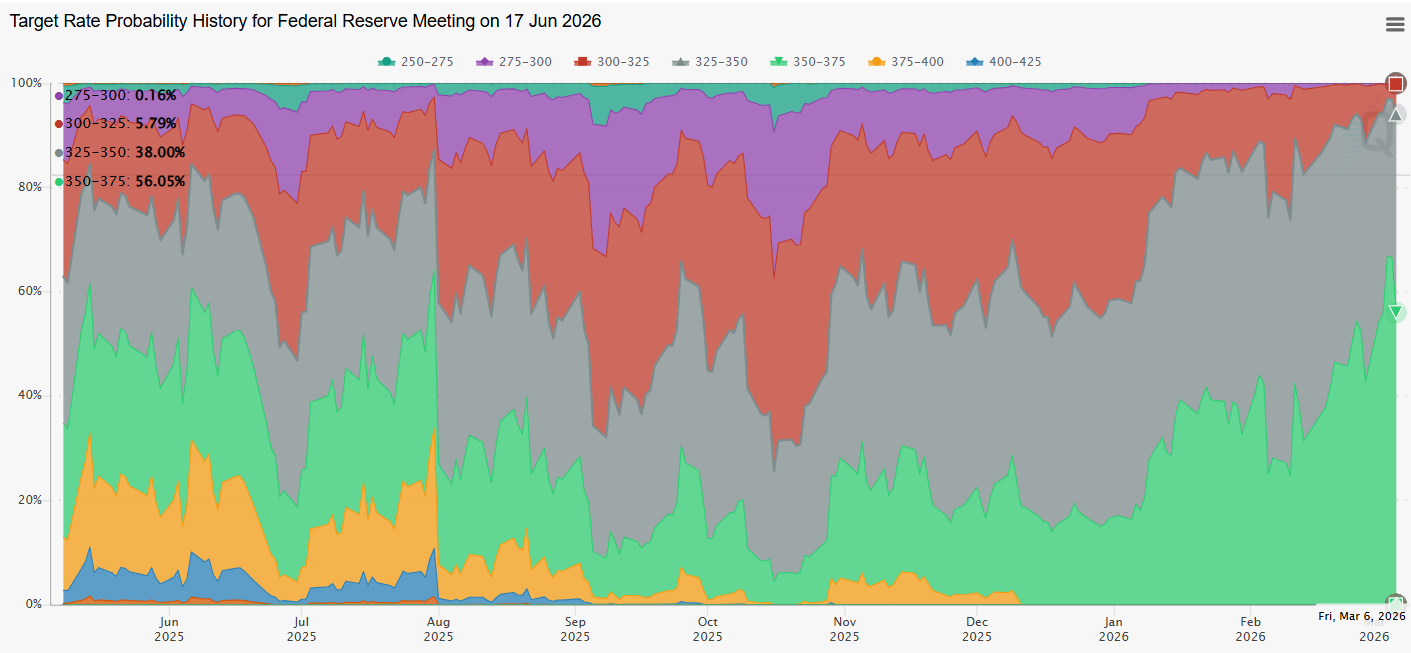

Consensus now sees the first rate cut as coming in September.

And we’ve seen a continued backing up of 1H rate cut odds.

Now I know there have been a lot of 2022 comparisons thrown around - it’s hard not to given the Q1 war analog creating a commodity price spike, sticky inflation and falling Fed accommodation - but this may be the most 2022-like condition yet and it is not good for the liquidity and risk asset outlook.

My inflation outlook is that there is little to no downside left and I have an upward drift bias on commodities. Given the Fed already views the Fed Funds rate as around or near the upper bounds of neutral, no inflation progress is problematic for them. The other side of their mandate, the labor market, is undoubtedly weak but cuts to combat it are likely to make the inflation problem worse - the Fed is as boxed in as ever. Their third mandate, market stability is becoming more and more likely as the instigating factor for Fed support which means we need to see equity markets continue to correct lower before any action.

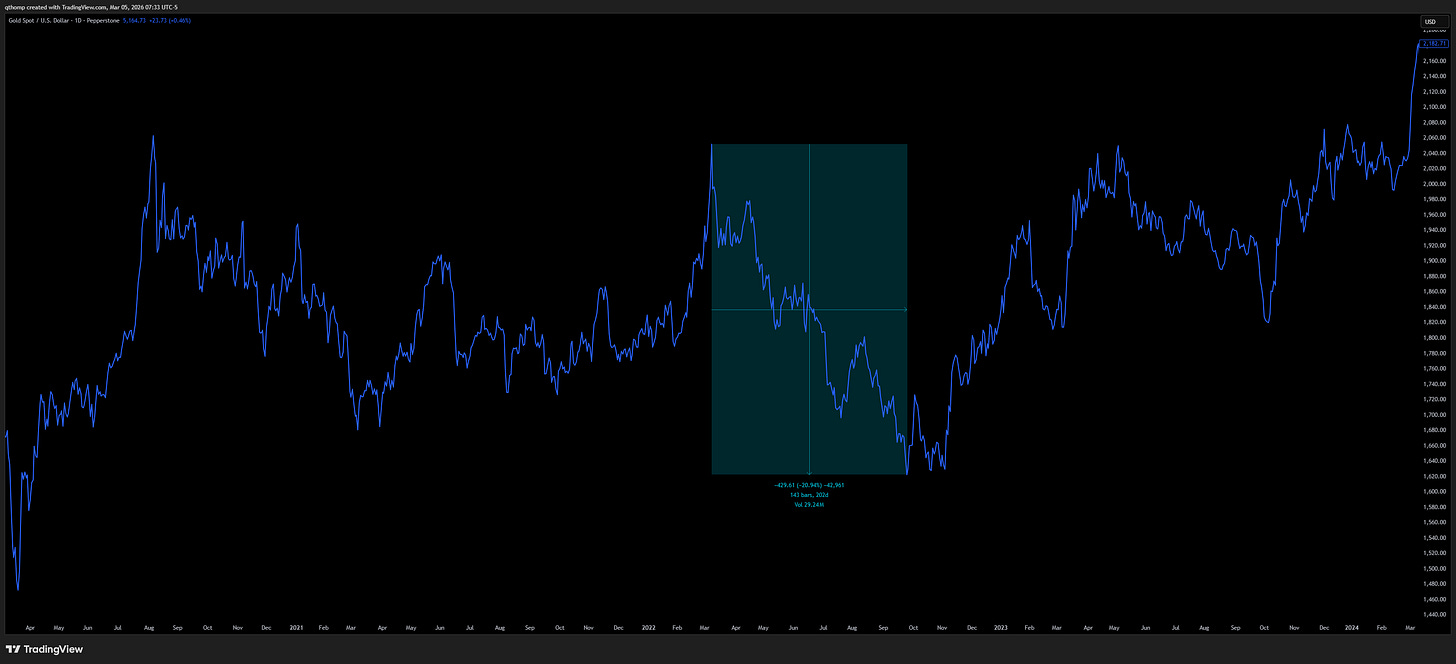

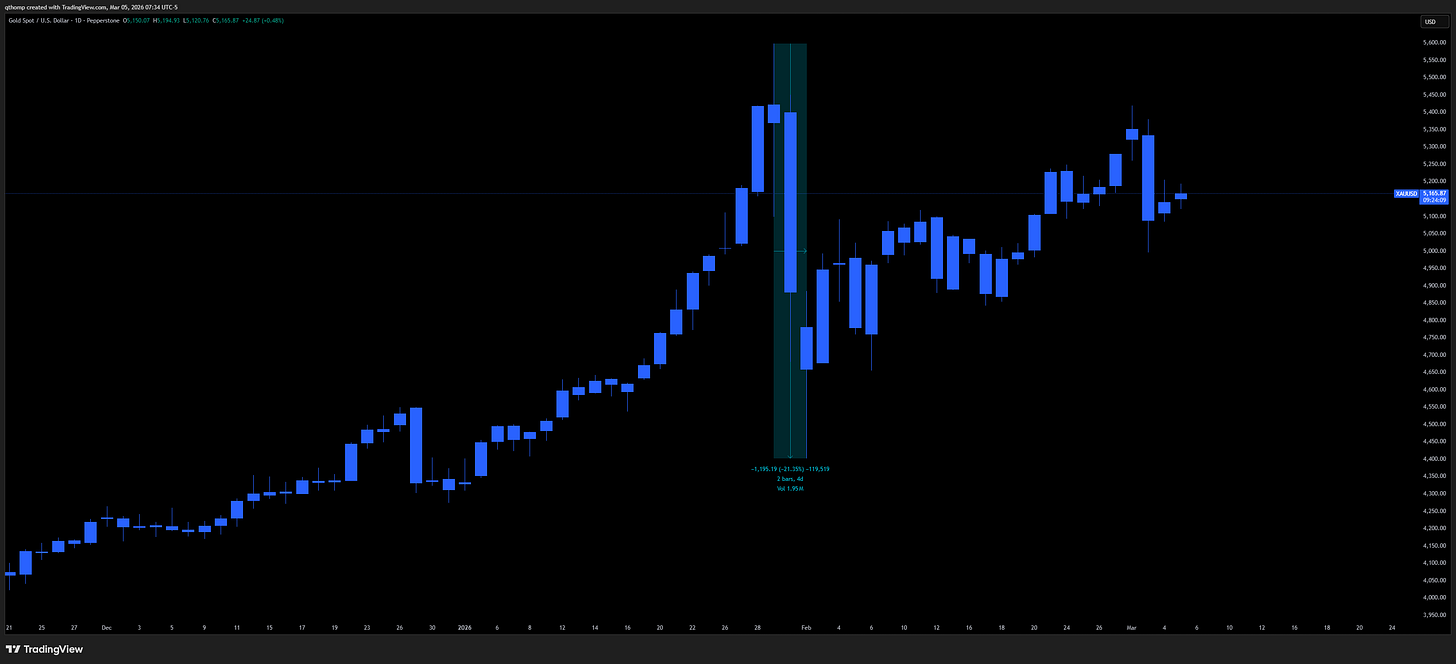

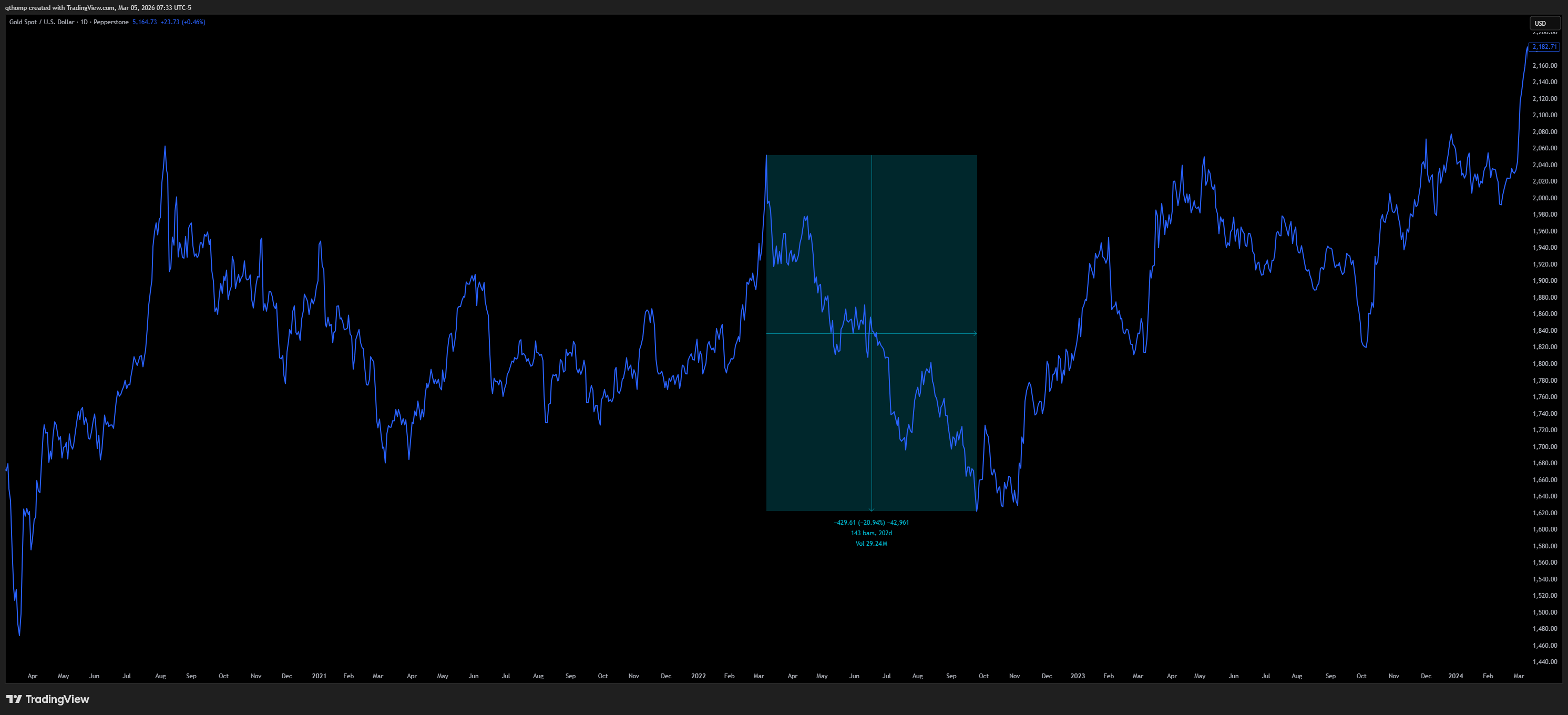

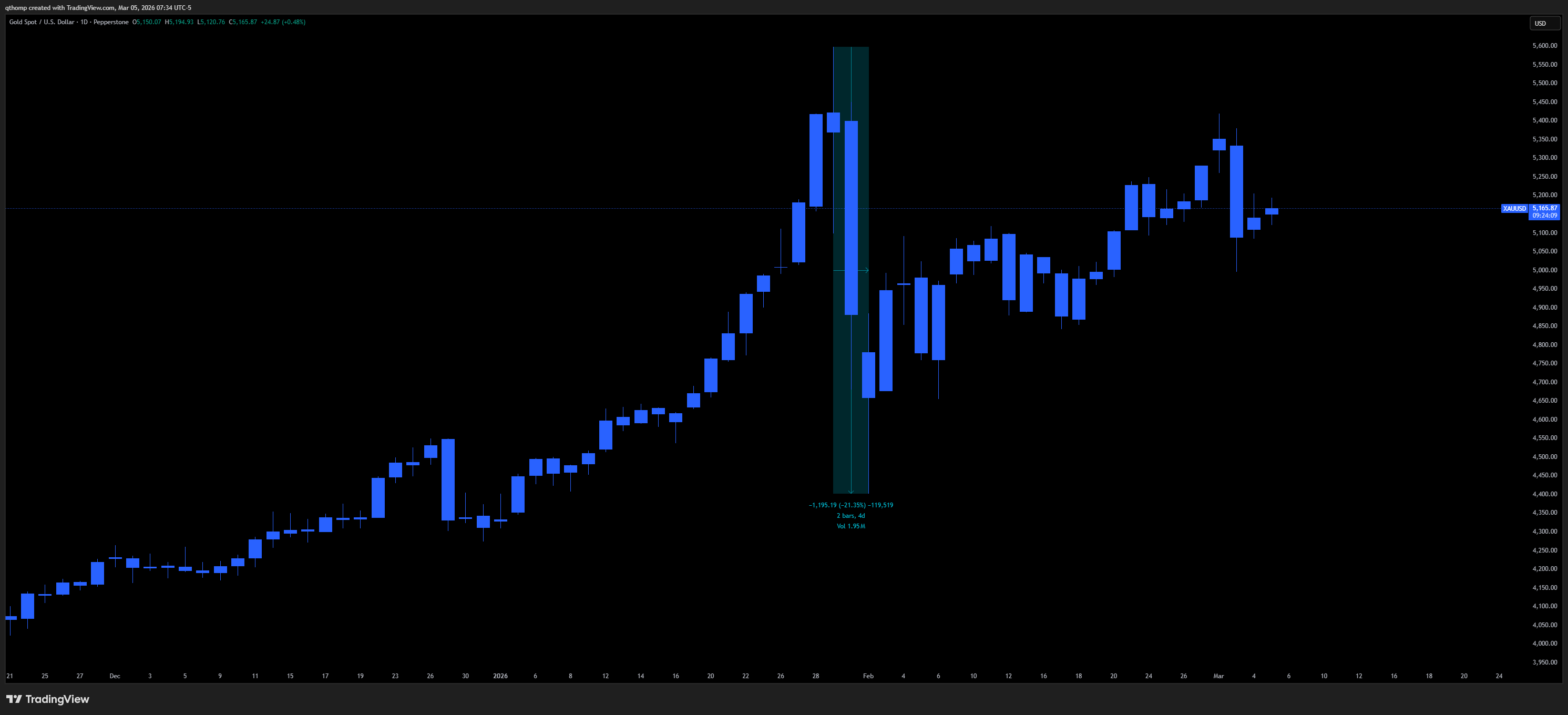

I’ve been discussing for awhile now that I think the ‘run it hot’ narrative will be tested. With no new material midterm-driven stimulus measures enacted nor meaningful Fed liquidity support, the two key ingredients for ‘nothing stops this train’ are missing. Given that, even the winning gold and metals trades can be tested. After all, gold had a -21% drawdown in 2022.

Which is ironic, because we’ve already had the same exact drawdown in 2026. I guess this is why they say history rhymes.

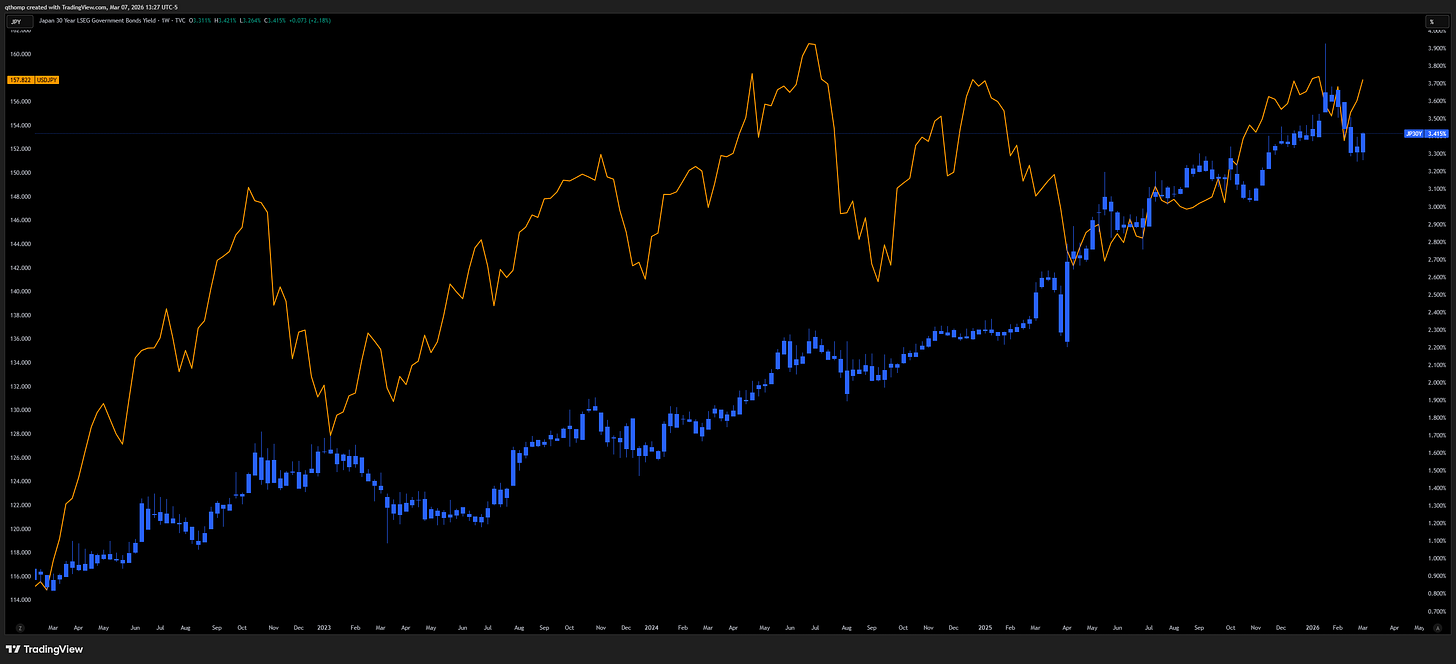

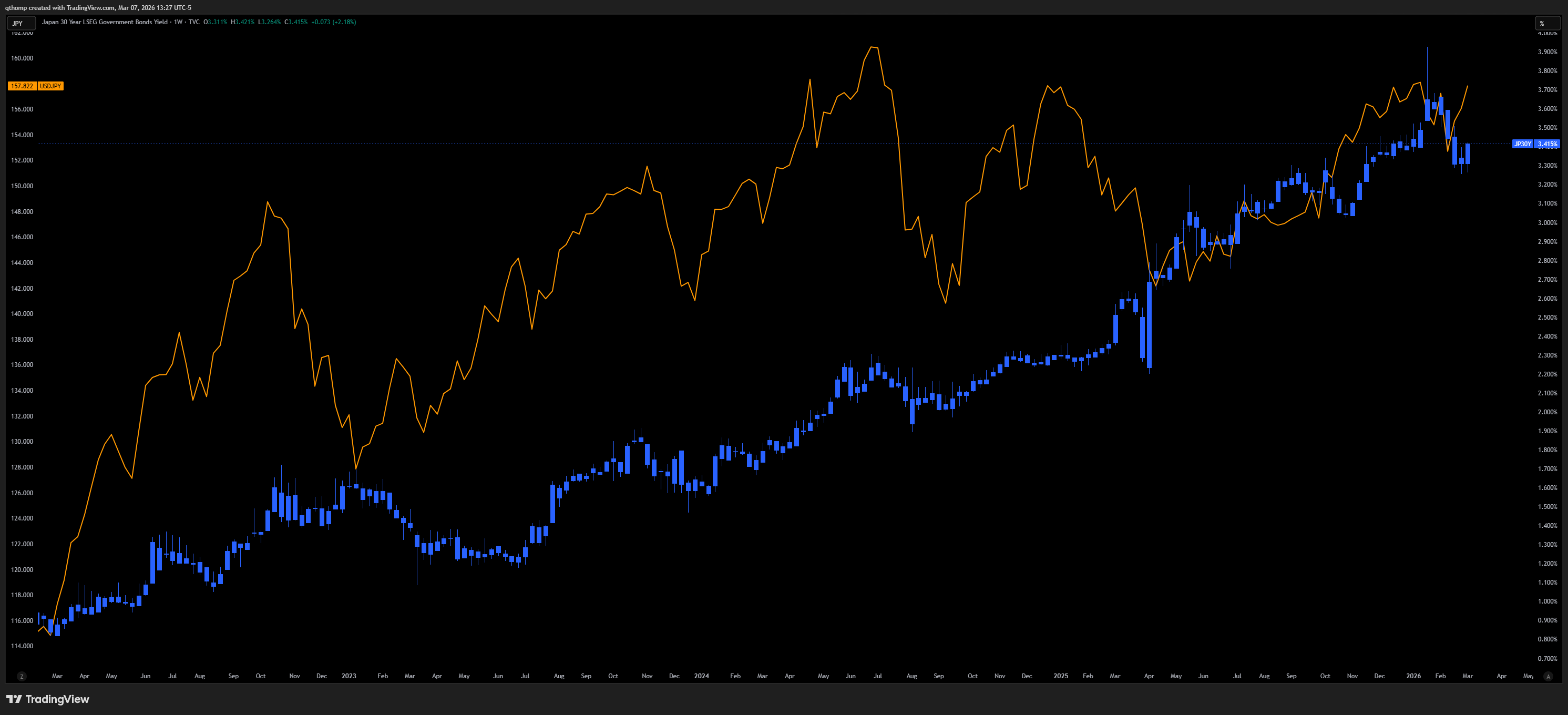

US-Japan decision time.

Policymakers have a decision to make:

Defend 158 USDJPY to suppress global bond yields and fight inflation, or

Let 158 USDJPY breach and with it global bond yields and inflation go too.

The Yen is back to its ~158 level that has been defended on numerous occasions over the past few years.

Now pretend you are a monkey and know nothing about financial markets and then look at this chart.

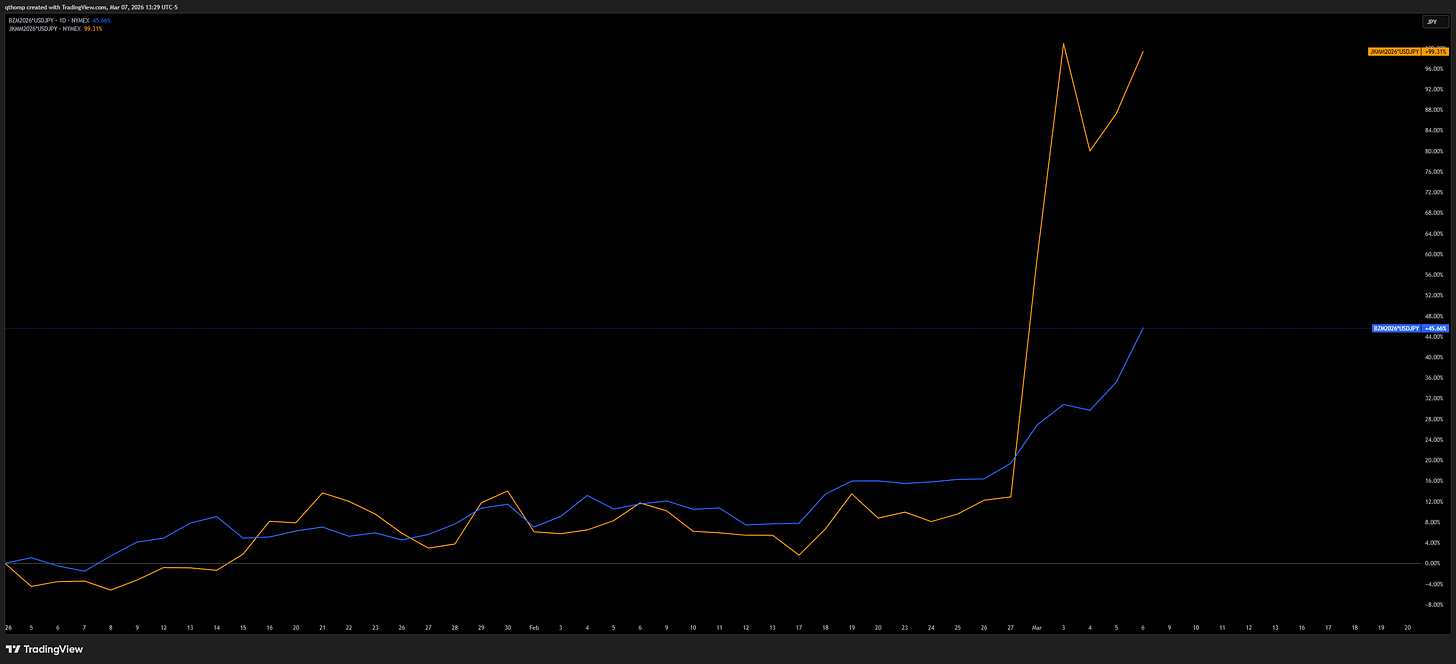

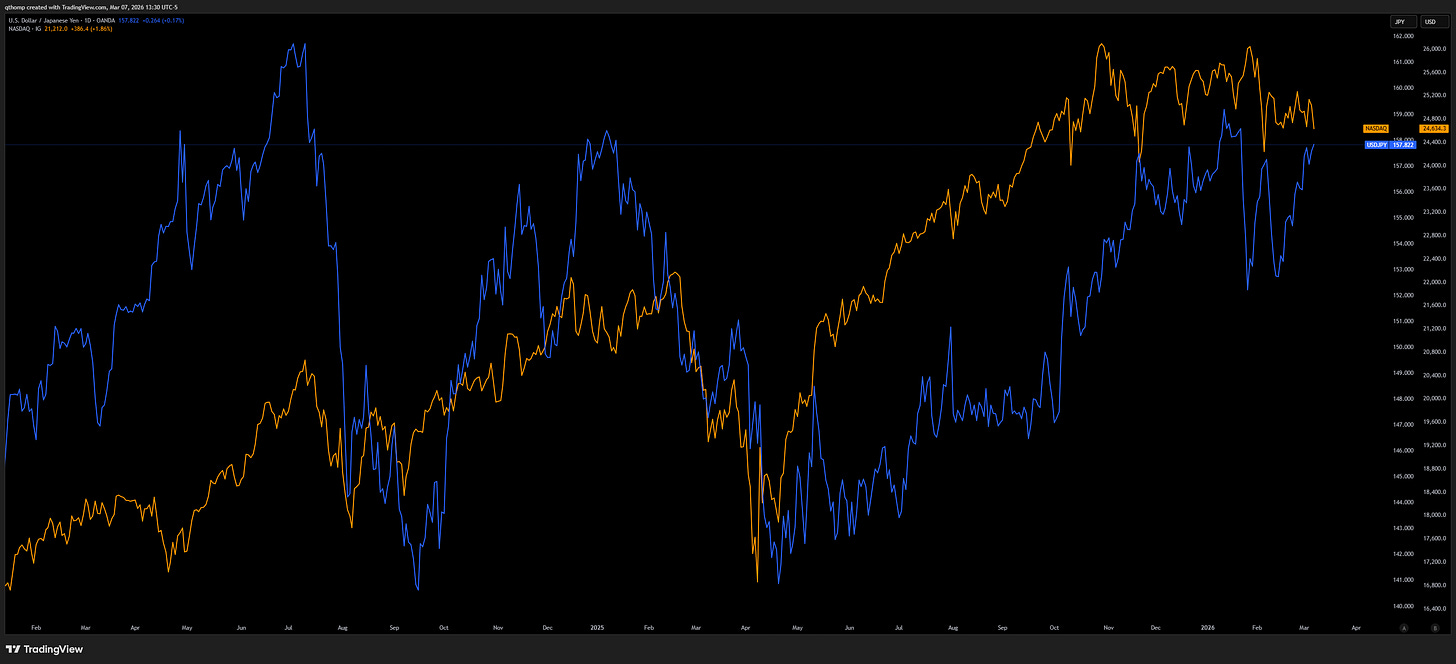

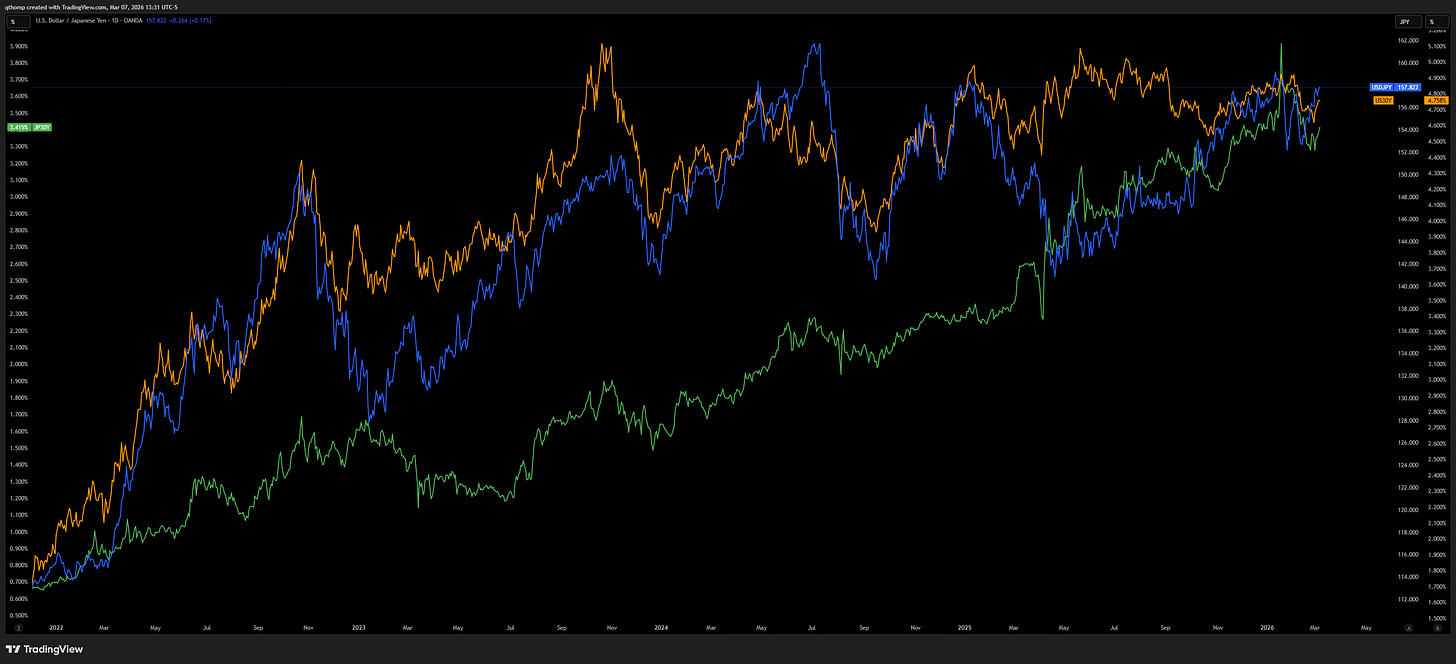

Now for them overlayed.

What are they considering in making such a decision?

Domestic inflation in Japan is already likely to be a problem - June delivery of natural gas and oil are +100% and +45% YTD, respectively. Continued weakening of the yen only makes this problem worse.

Bond market instability which can stem from too loose monetary policy risks spillover into equity markets.

Policymakers have a decision to make:

Defend 158 USDJPY to suppress global bond yields and fight inflation. In this case we likely see equity markets down.

Let 158 USDJPY breach and with it global bond yields and inflation go too. In this case we would see Japanese bond yields move higher and drag global yields along with them.

Combatting a few popular AI narratives.

I want to revisit a topic I wrote about a few weeks ago before the recent leg up in AI fears. Deflation is politically unpalatable and I will explain why from a few angles. Most of the AI job loss takes I have read do not account for societal, market and political reaction functions and that is a problem for accurately predicting outcomes.

The recent rapid acceleration in AI innovation and adoption is a biproduct of government policy. I spoke about it in last week’s Forward Guidance but let me add some detail.

Since 2021, we’ve had the CHIPS Act, National AI Research Resource, Inflation Reduction Act, Executive Order 14179, Executive Order 14318, Executive Order 14363, The "Winning the Race” AI Action Plan and Federal Preemption and AI Litigation Task Force. All of these have been executive, fiscal and/or federal initiatives to stimulate and incentivize AI innovation and acceleration.

Monetary policy has also been a massive accelerant as uneven Fed policy has suppressed long end yields via large balance sheet intervention in long duration bonds to support financial markets while coming at a cost via abnormally high inflation and front end interest rates that has hurt Main Street and small businesses.

The main point I want to make is while the technology and VC community will tell you otherwise as they believe they live in their own world, the truth is the AI acceleration has been created and fostered by government policy, full stop. The speed of innovation would be multiples slower without it. Why this is problematic is because it has come at the direct expense of the majority of the population who does not benefit from it. Said another way, government has chosen policy to speed run the demise of Main Street, small businesses and the average worker. This is not sustainable over a long period of time.

Just as quickly as the hand that giveth, the hand can taketh away. We’re already seeing datacenter pushback in both blue and red states equally - from DeSantis to Sanders/Warren. As we approach 2028 presidential election where for the first time ever younger generation voters will equal or outnumber boomers, the asset price first approach to policy will be tested.

None of this is to say AI adoption will decrease - it obviously will only increase given its huge productivity increases. But there is much more to asset prices than that and the market is forward looking. Just like previous technological bubbles didn’t see an end to their adoption, quite the opposite actually, but they did stymie asset prices for periods of time following the peak hype cycle.

As mentioned last week, I think semiconductors have topped for a very long time.

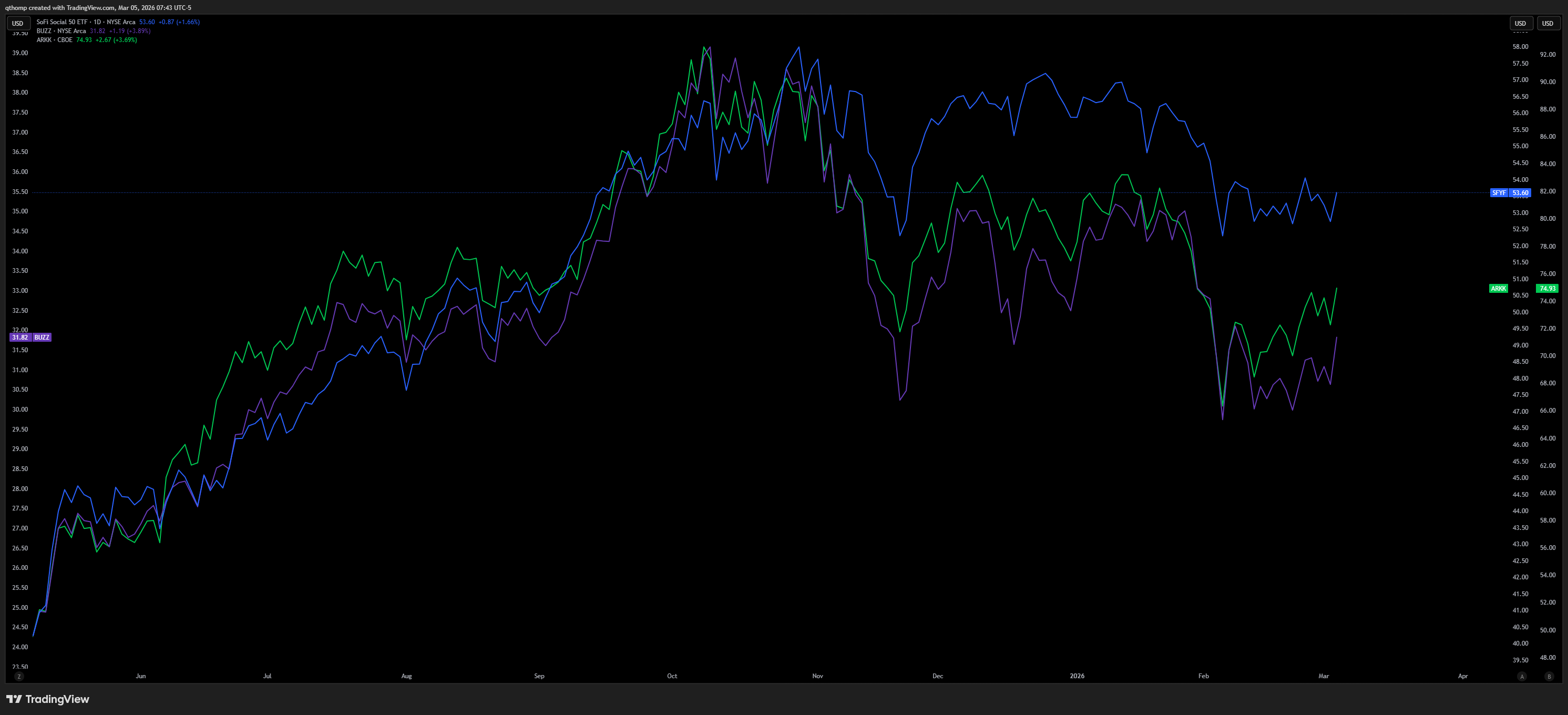

It’s no longer just Mag7, but there is nowhere safe in equities.

For the last few weeks I’ve been discussing the problems I see for small caps given they have already priced in all of the economic data improvements we are seeing.

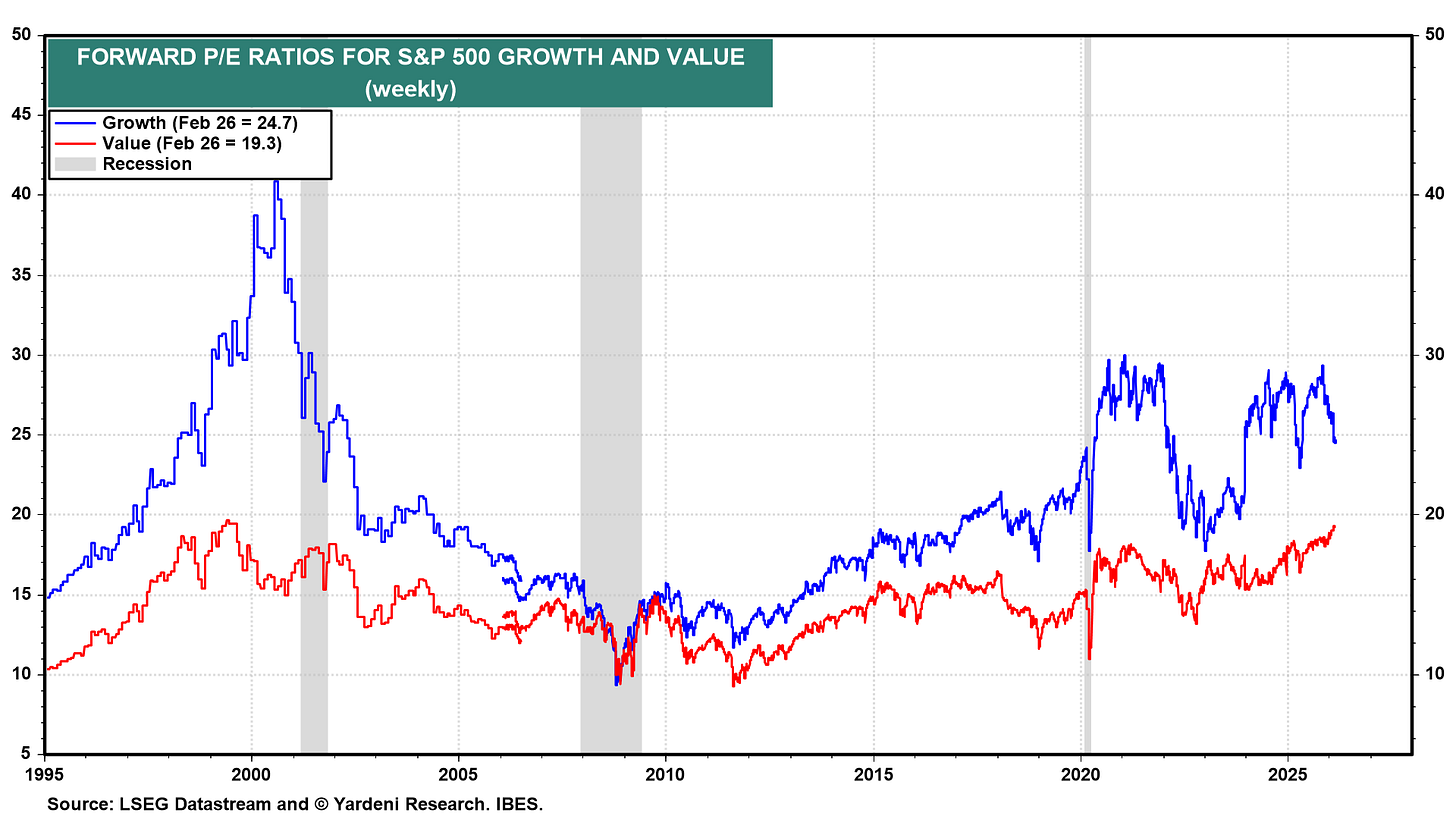

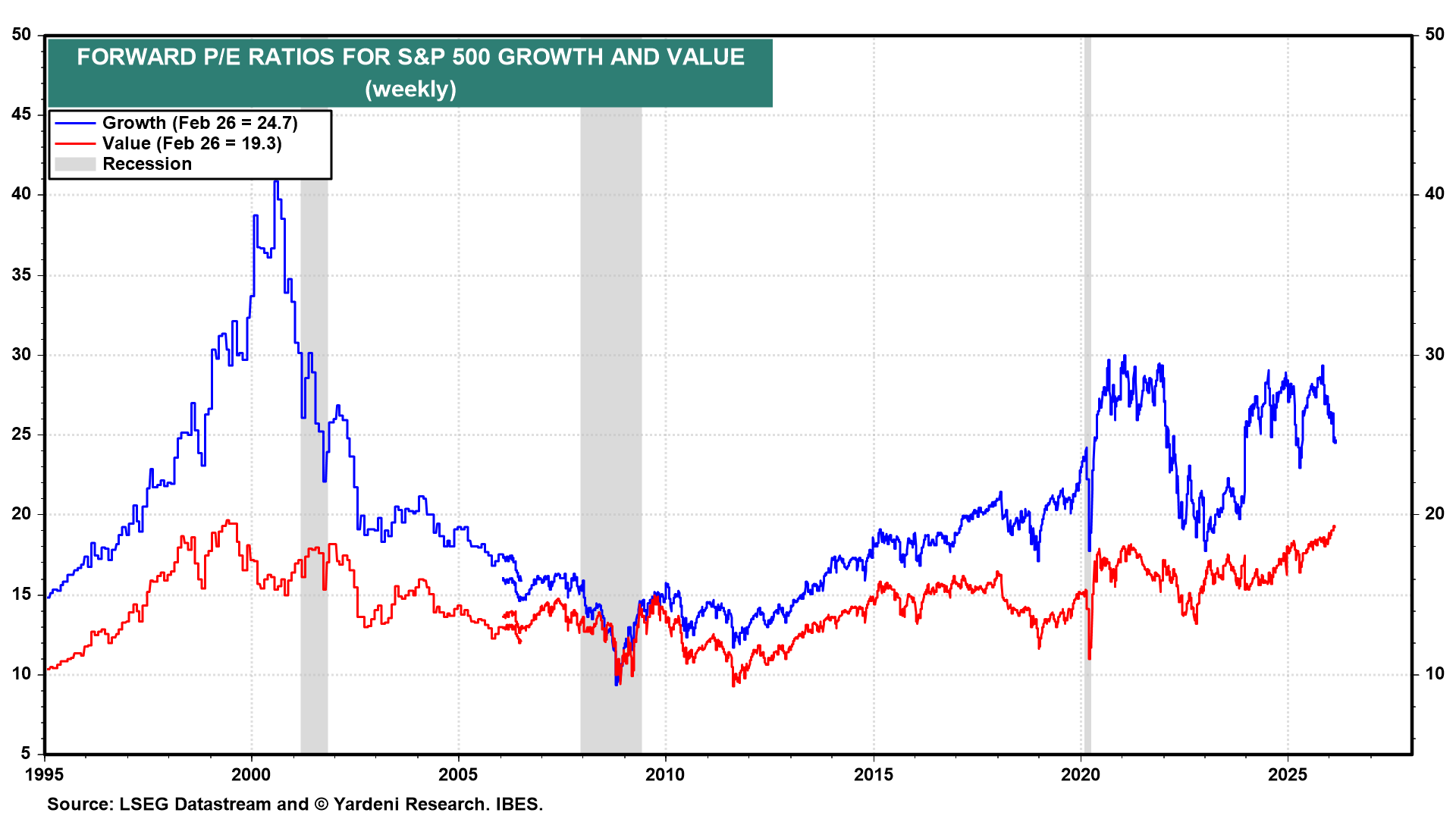

With all the talk of the AI and tech bubble, value forward P/E ratios are the highest since 1999!

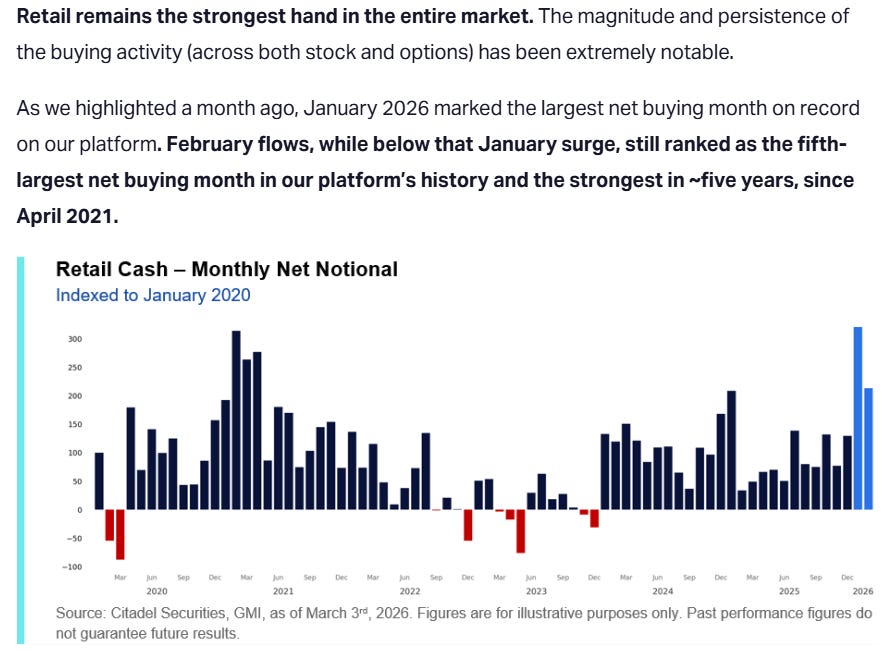

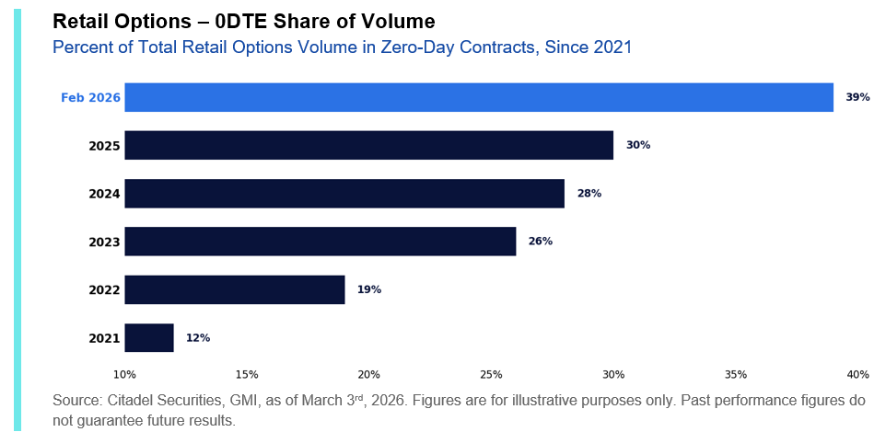

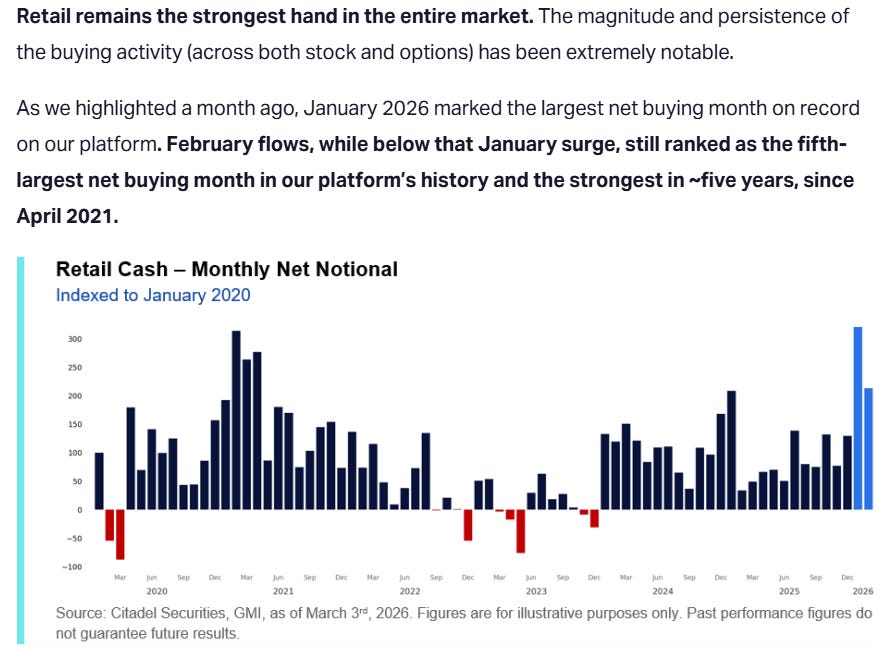

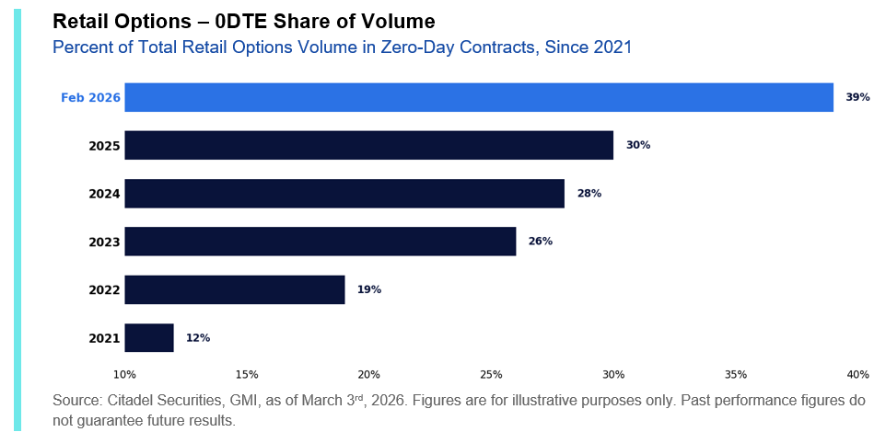

Then I see data like this from Citadel’s Scott Rubner around retail activity continuing to increase.

Which becomes an even bigger head scratcher when, despite record buying, all the retail baskets look like garbage.

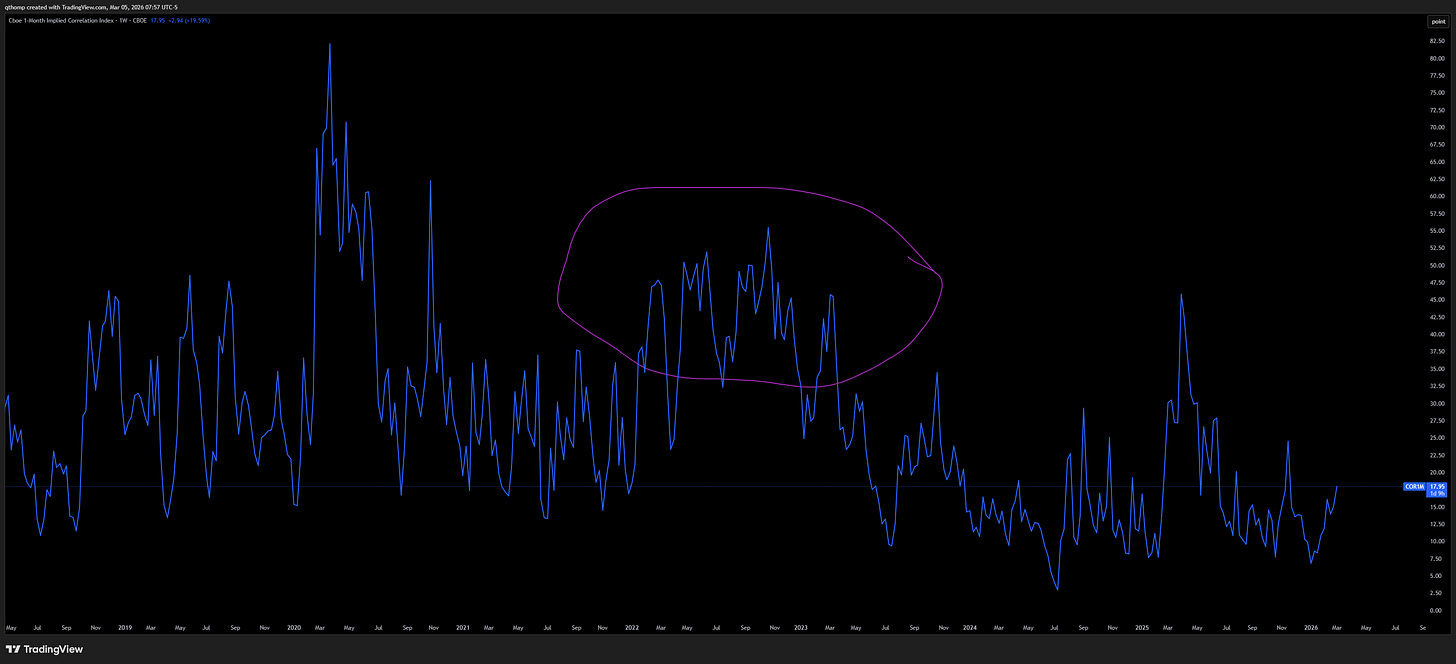

Anyone active in markets knows this chart is going to make its impact heard in markets at some point, the question is when.

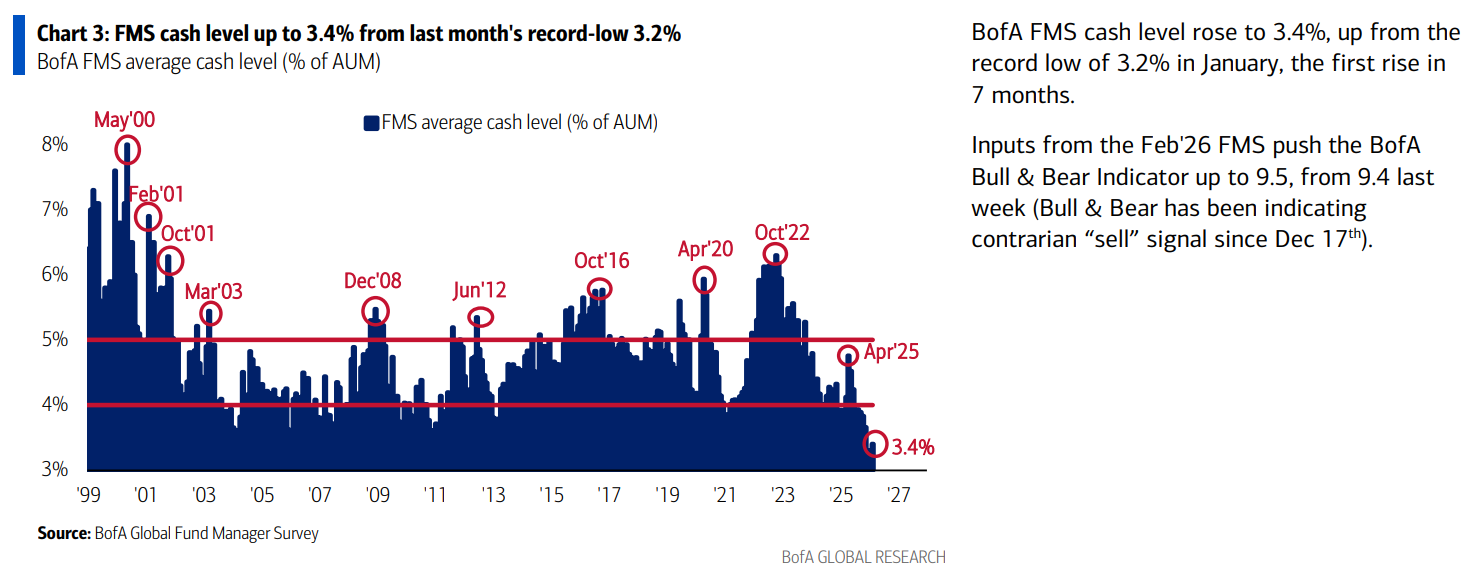

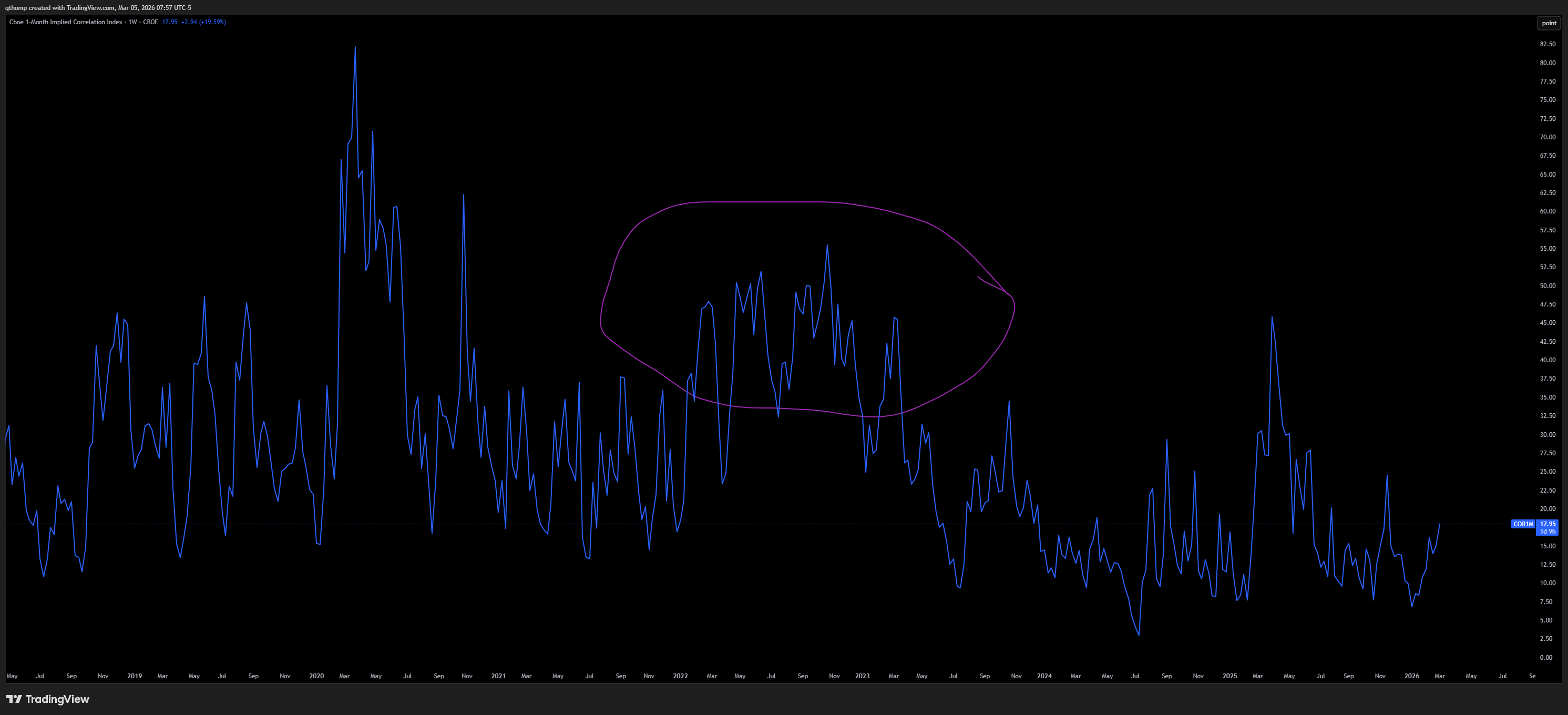

As we all are playing hot potato across violent sector rotations, it’s important to remember that cash is a position, and sometimes the best position. There is a lot of room for stock market correlations to increase off the record low base that has formed. Heck, even another 2022 analog for you. In simple terms, this means everything down together where not even metals are safe should be on your 2026 bingo card.

If you’ve been following our work, you know for weeks now we have been suggesting maximum caution. That view continues as we traverse the month of March before possibly seeing some reprieve in April. I believe the path of least resistance for equities remains down, bonds remain a terrible investment and correlations across the market are rising making even the secularly winning sectors vulnerable to risk off moves. We prefer a long / short portfolio with metals, energy and agricultural commodities and related equities on the long side and technology, semiconductor equities and bonds on the short side.

Last week’s labor data ended with a bang on Friday’s abysmal NFP report. This week we get CPI on Wednesday and JOLTS on Friday, neither of which are likely to be positive. Our base case is that inflation is generally done going down and more likely to rise in coming months while the labor market continues its deterioration. I would venture to guess Rick Rieder isn’t all that upset about not getting the Fed chair nod given the shit storm that is brewing.

Good luck out there and I hope everyone has a great week. Join us in the chat for more great dialogue.

Great insight Quinn and very much appreciating your real time updates on chat. FG and your substack are my go-to right now. One comment though...on your charts, it's really hard to read the size font even when I zoom in.

Point 3 in the AI narrative section is a brilliant point