Scouting the Tape - May 10, 2026

(Unique) macro idea generation and (insightful) market thoughts.

Happy Sunday y’all. Aren’t weekends a lot nicer when the VIX is at 17 versus when it’s hugging 30?

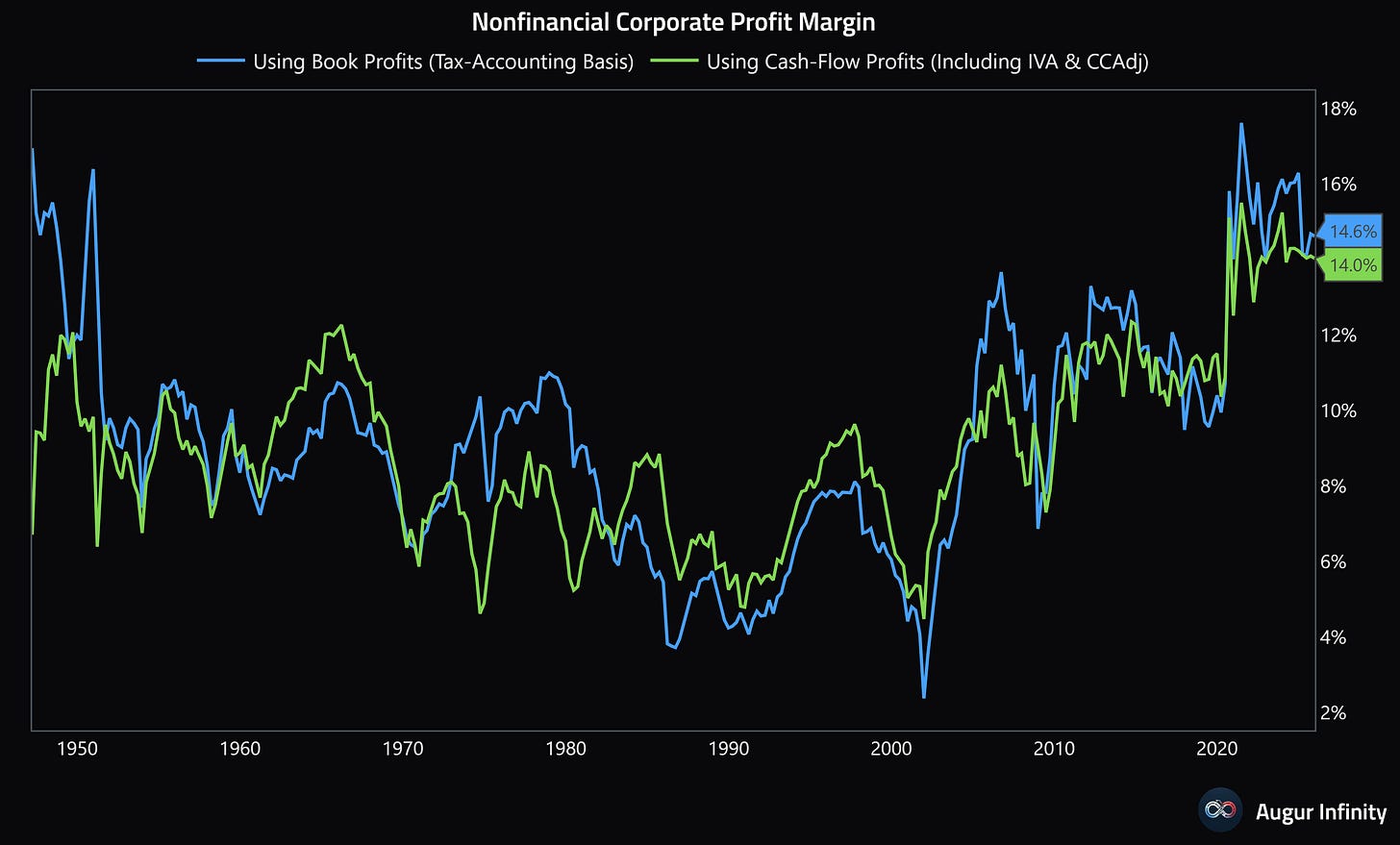

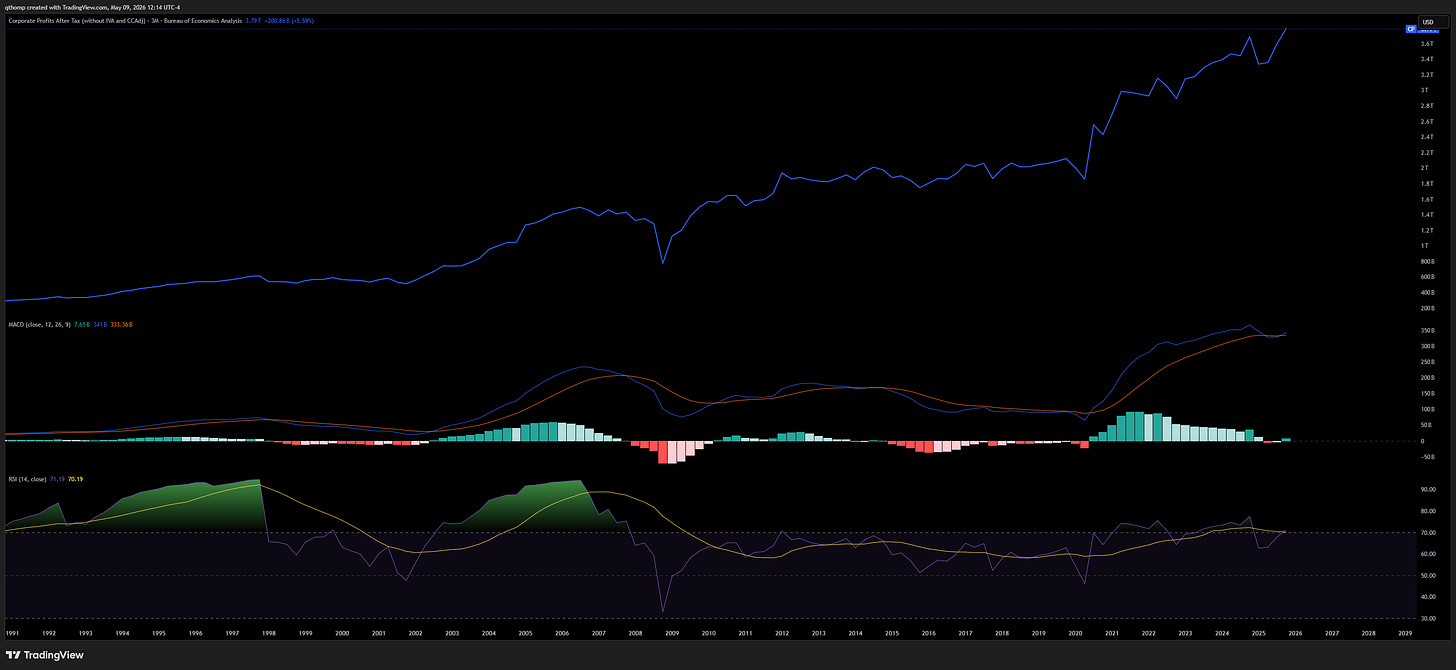

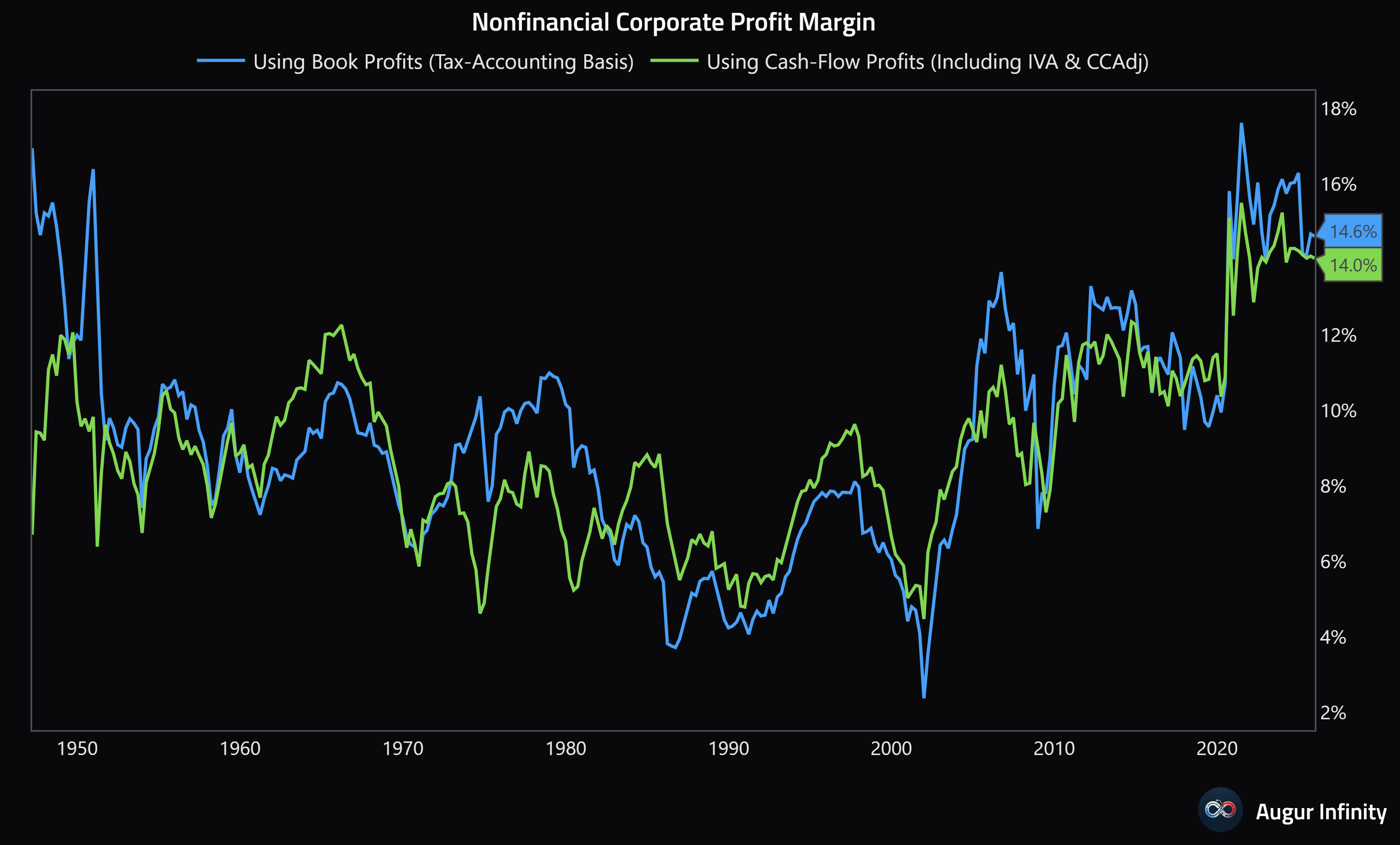

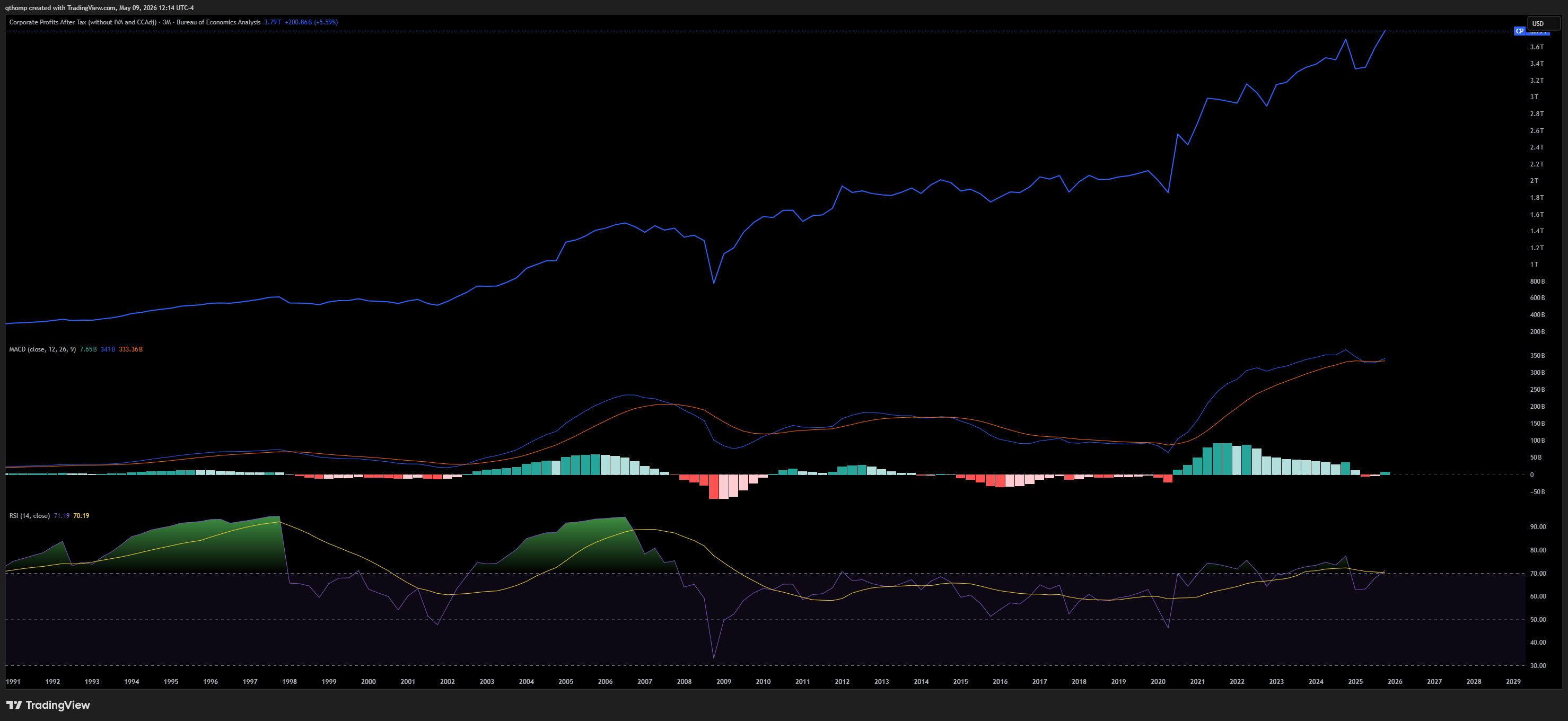

The bubble in US corporate profits.

It’s interesting how divisive the topic of whether or not stocks are in a bubble is. Bears point to high P/E multiples on record profit margins while bulls point to record EPS growth. Both are correct. Where I shake out is that the bubble is in corporate profits as a result of both fiscal and monetary policy supporting corporates and capital over labor for many years running. This explains why it is such a heated debate, because both camps are technically correct. With bulls arguing that stock prices are supported by record profits and earnings and bears belief that this imbalance is unsustainable, both can be true.

All-time high profit margins corroborate this view. Dissidents will point to rapid technological innovation as the driver of a structurally higher corporate profit plateau, I would point to the government policies that allow that to be the case - mega cap tech monopolies, the rise of duopolies/oligopolies across every sector and continued tax/fiscal policy that favors the large at the expense of the small.

Notice something changed after 2020 when the US government doubled its money supply on the spot and started putting corporate debt on its central balance sheet. No wonder corporate profits exploded.

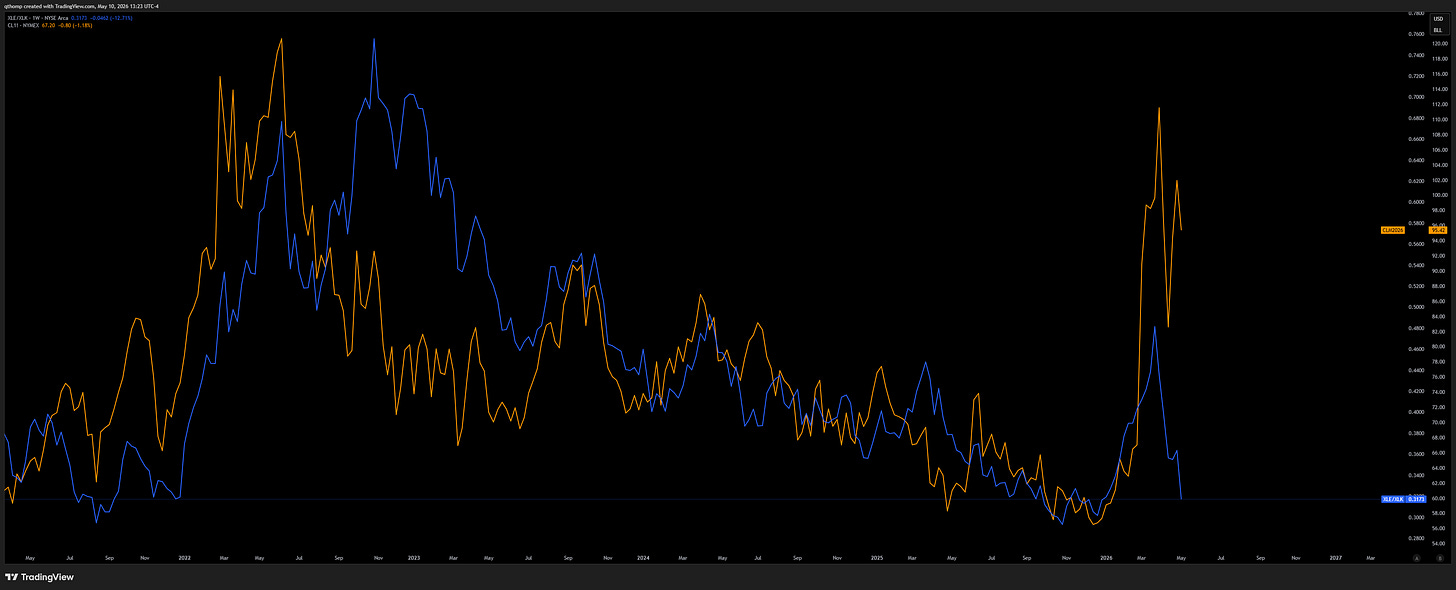

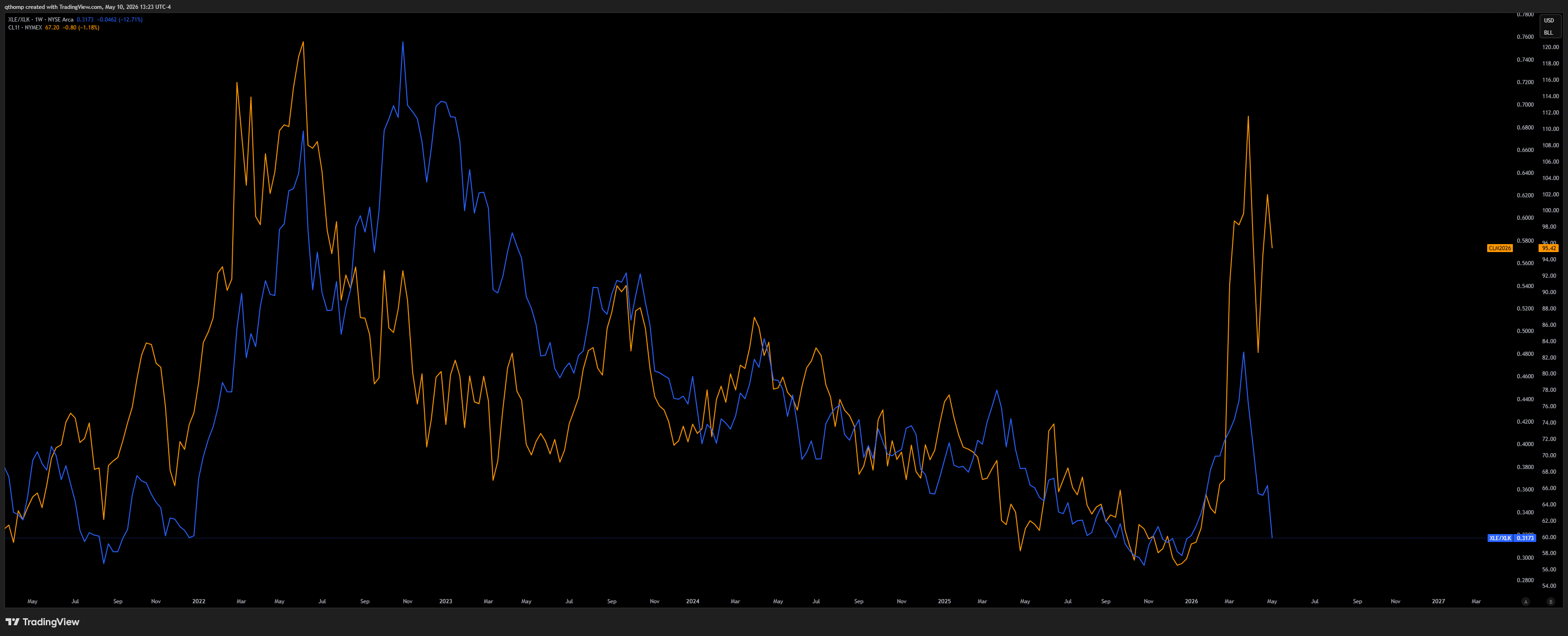

Divergence between oil prices and XLE/XLK.

Looking back over the past number of years, it is not normal to see such a large divergence between the price of oil and the ratio of oil stocks (XLE) to tech (XLK). A large gap has opened up between the two and I would bet it closes, but trade structure and timing are obviously critical.

I am a believer that the lasting impacts of the supply shock will keep oil prices elevated for longer than the market currently has priced in.

Forward Guidance@ForwardGuidanceThe market may be underpricing the second-order shock to oil. @qthomp argues that even if the strait reopens, sovereign restocking could create another leg of demand. Longer-dated oil may be where the market is still asleep.4:07 PM · May 8, 2026 · 5.37K Views1 Reply · 6 Reposts · 39 Likes

Forward Guidance@ForwardGuidanceThe market may be underpricing the second-order shock to oil. @qthomp argues that even if the strait reopens, sovereign restocking could create another leg of demand. Longer-dated oil may be where the market is still asleep.4:07 PM · May 8, 2026 · 5.37K Views1 Reply · 6 Reposts · 39 LikesThe long December oil futures trade we wrote about in the beginning of April played out well and I still like it.

Lately I have been focusing more on the oil and gas equities, particularly international exposure, which I also wrote about a few weeks ago. XOM is an example of an international focused major that has pulled back -18% off its highs back to February 4th (pre-Iran War levels) right into the 100dma. I’m long it among a basket of names.

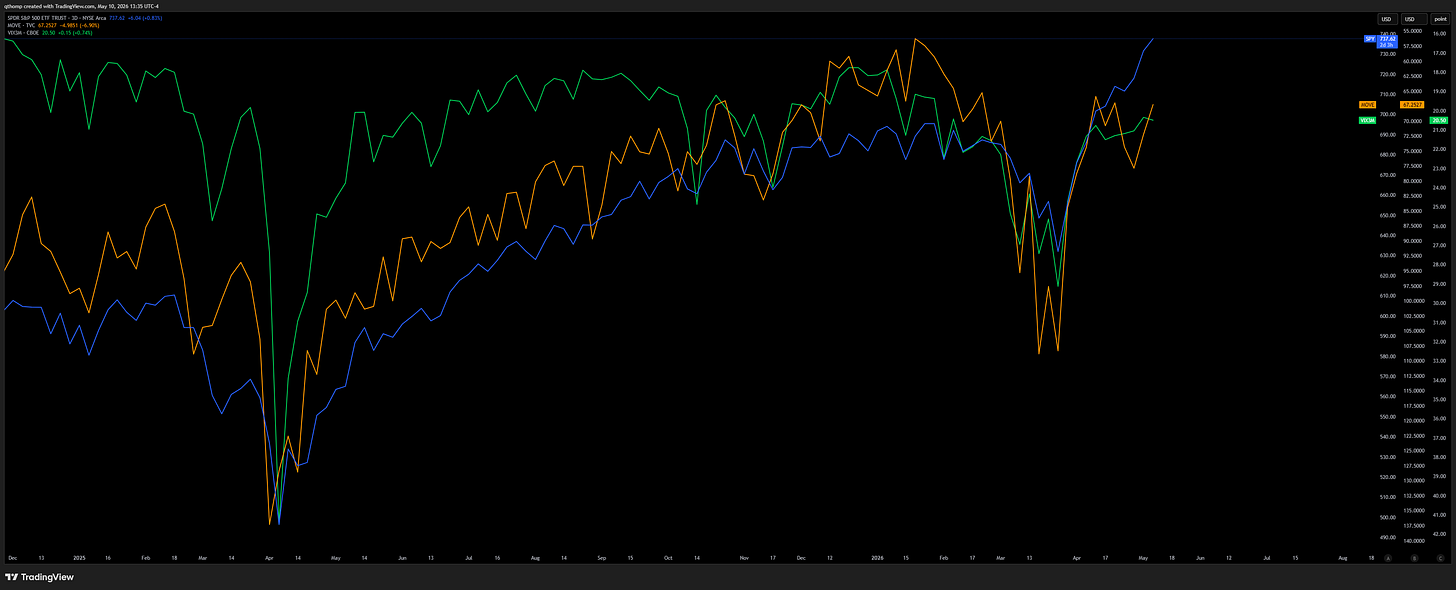

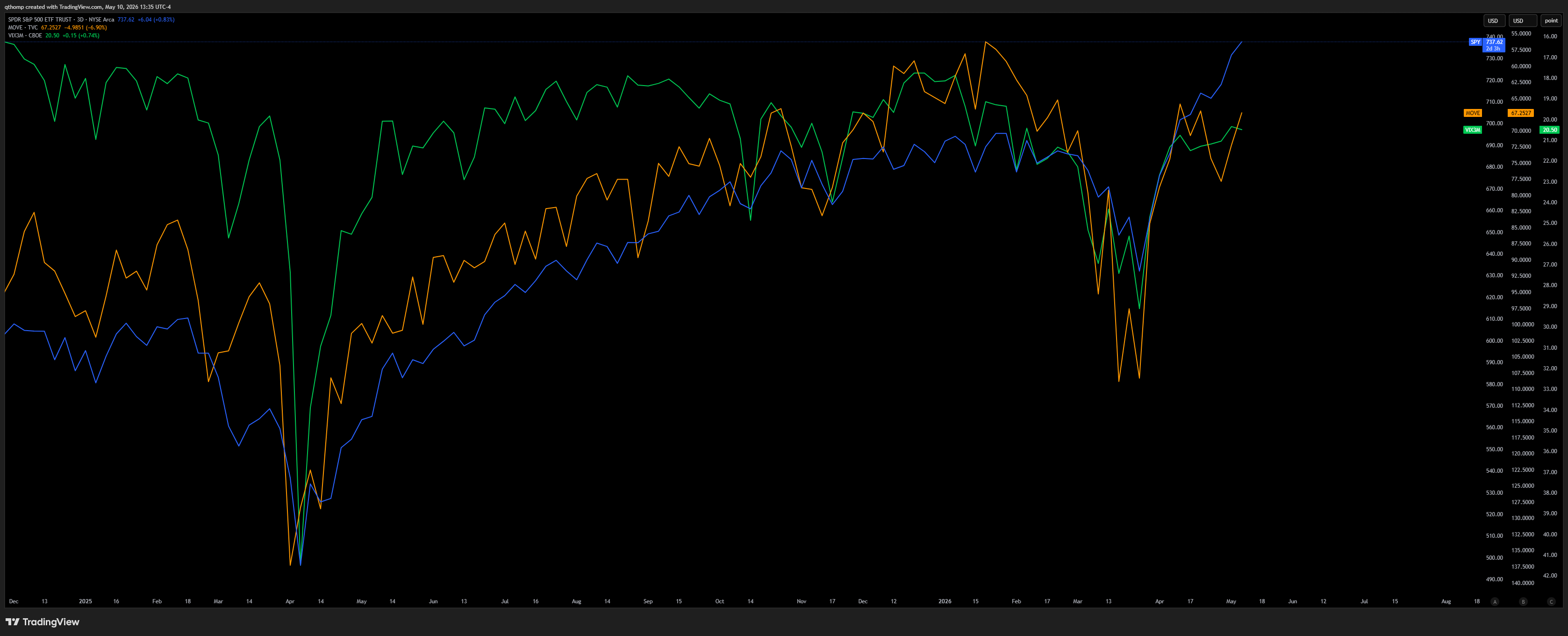

Divergence between equity indices and stock and bond volatility.

A potential divergence between equities moving higher while stock and bond volatility measures bottom out is also worth watching over the coming weeks. We’re now inside of 6 months from midterms so it is not surprising volatility would find a floor soon. Thus far nothing conclusive here but something to keep an eye on.

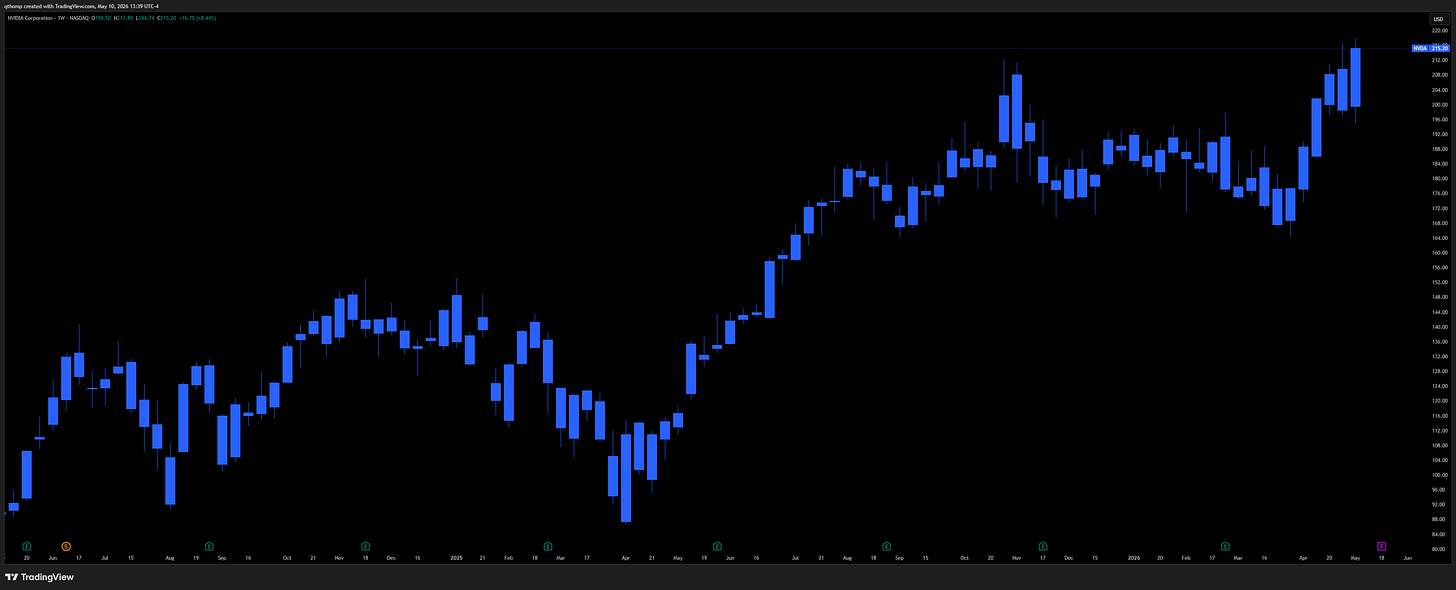

NVDA - the bull / bear battle ground.

I am infatuated by the NVDA chart. I’m not sure if it’s because it makes up 8% of the whole S&P 500 index or that its market cap fluctuates a few hundred billion each week without anyone batting an eye. Either way, the $5.3T behemoth is an important one to watch.

I would say bulls are currently in the driver’s seat as it closed at new weekly closing highs.

That said, the current ‘double top’ pattern is not new for the stock. Most notably it did this in November last year, closing at a weekly high but then not revisiting those levels for 6 months and testing a -22% peak to trough drawdown in between. January 2025 saw something similar. We’ll watch it play out together.

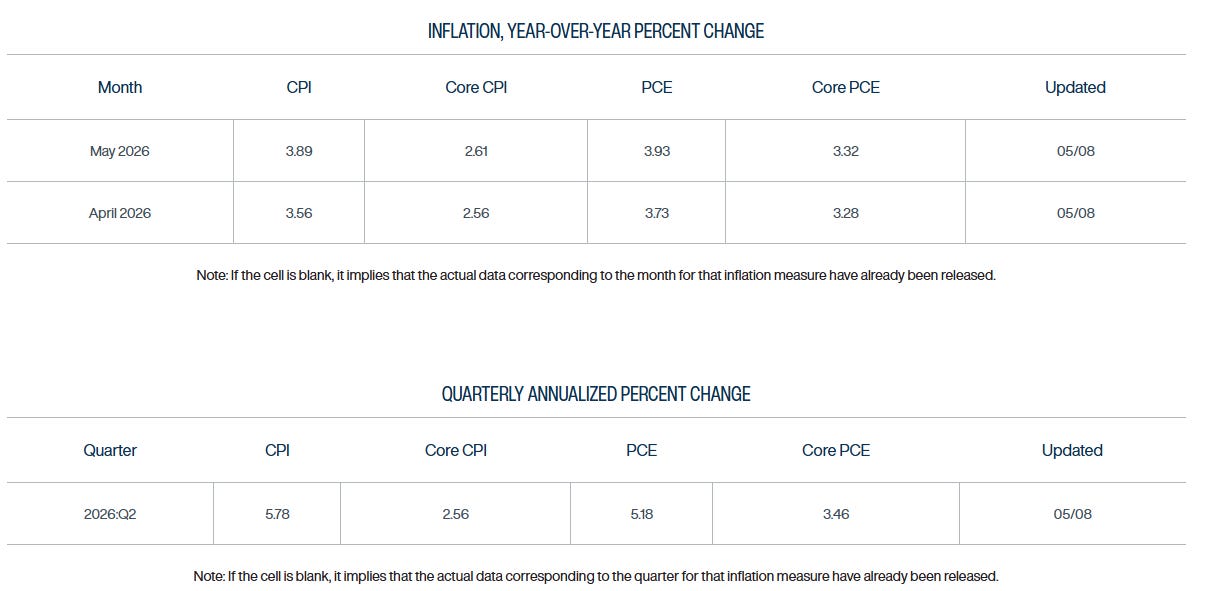

Financial conditions, monetary policy and gold.

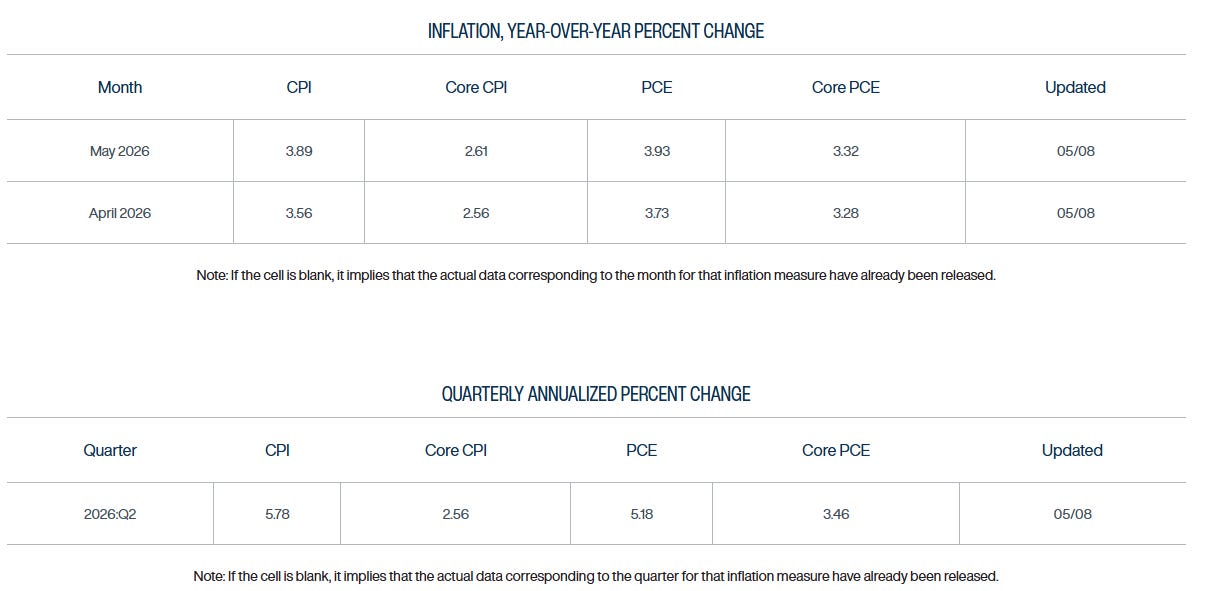

Over the last few weeks I’ve been frequently writing about the ongoing risks of overheating in the economy and how policy is too loose. A number of trolls on X have wrongly interpreted these ideas as me being bearish when I specifically compared the environment to 2020-2021. The reality is that this behavior should make you less bearish in the immediate term, but more bearish on longer horizons. When governments enable above trend growth and a worsening secular inflation environment, it feels good upfront but makes the ramifications harsher on the back end because they are forced to slam on the brakes harder than they would if they took the pain sooner. Literally 2022 to a tee.

Quinn Thompson@qthompGlobal policymakers are staring down the barrel of an uncontrollable situation. They are simultaneously attempting to devalue the dollar, suppress bond yields and manipulate commodity prices lower. They have succeeded in the short-term and it has felt like crack cocaine for

Quinn Thompson@qthompGlobal policymakers are staring down the barrel of an uncontrollable situation. They are simultaneously attempting to devalue the dollar, suppress bond yields and manipulate commodity prices lower. They have succeeded in the short-term and it has felt like crack cocaine for Quinn Thompson @qthompPolicymakers are running the economy so unbelievably hot right now that I am starting to think it has approached or surpassed recklessness. The Treasury has completely taken over control of the money supply and financial conditions with their ongoing ATI/YCC actions and most3:52 PM · May 1, 2026 · 39.4K Views26 Replies · 46 Reposts · 308 Likes

Quinn Thompson @qthompPolicymakers are running the economy so unbelievably hot right now that I am starting to think it has approached or surpassed recklessness. The Treasury has completely taken over control of the money supply and financial conditions with their ongoing ATI/YCC actions and most3:52 PM · May 1, 2026 · 39.4K Views26 Replies · 46 Reposts · 308 LikesYou don’t have to look further than the Fed’s own website to see that its baked in the cake that inflation will rise above 4% this year. There are many ways to play this environment, sometimes it makes sense to grab a seat at the casino table and play along, and other options include patiently playing the inflation protection trades that will work at a slower pace now while speculative fervor is high and work even better when it dies. Everyone has a different style.

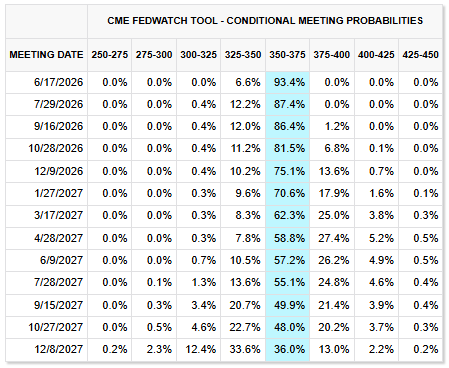

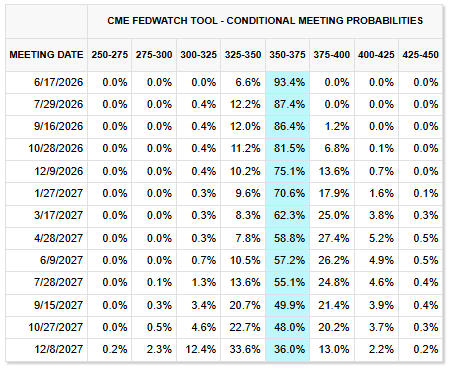

What’s clear, however, is that the market is saying it has no clue what is going to happen to the Fed Funds rate. I’d imagine without a Trump hand picked Fed chair, the odds of hikes would be higher, but most market participants believe the bar for this to happen is much higher under a less independent Fed. Unfortunately we won’t really get much more insight into the thinking here until June’s FOMC which is still over a month away.

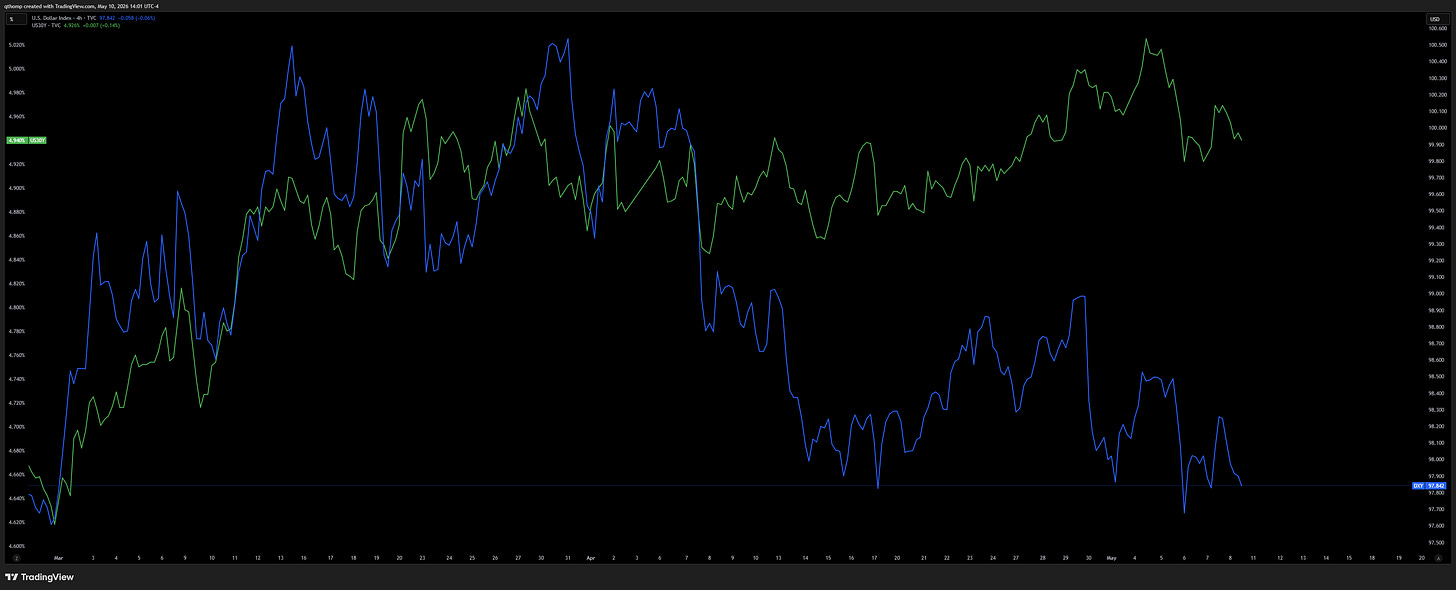

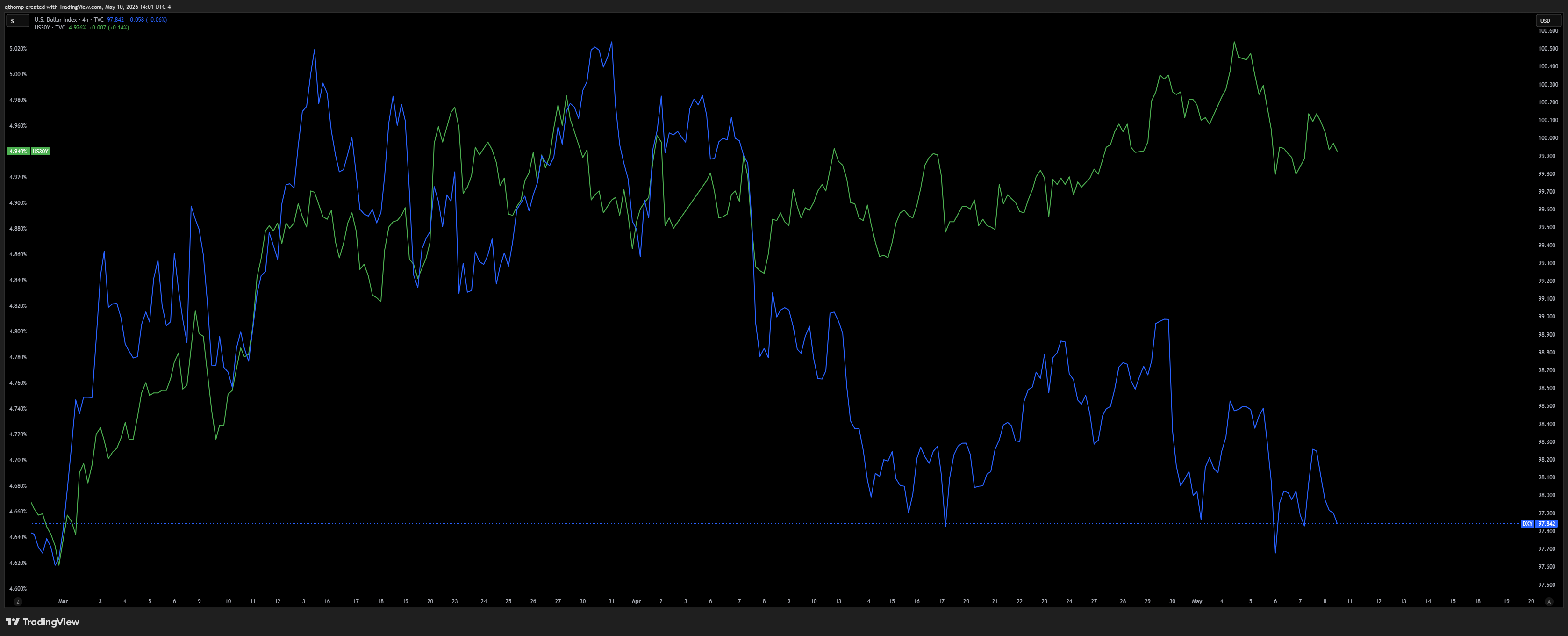

One relationship I am paying close attention to is dollar and yields, which in normal, healthy functioning times are often positively correlated. While too early to declare just yet, the recent dollar down, yields up has been interesting. Japan has been ground zero for what happens to a currency and sovereign bonds when policy is way too loose - yields up and currency down. If we listen, the market will tell us what it thinks about the current policy stance.

Given this is a global phenomenon happening across developed markets as everyone is allergic to hiking rates into a commodity supply shock, fiat to fiat crosses might not provide as much insight as normal. For this reason, keep an eye on gold too as it will continue to benefit from this globally coordinated ‘run it hot’ approach to growth and inflation. I am long.

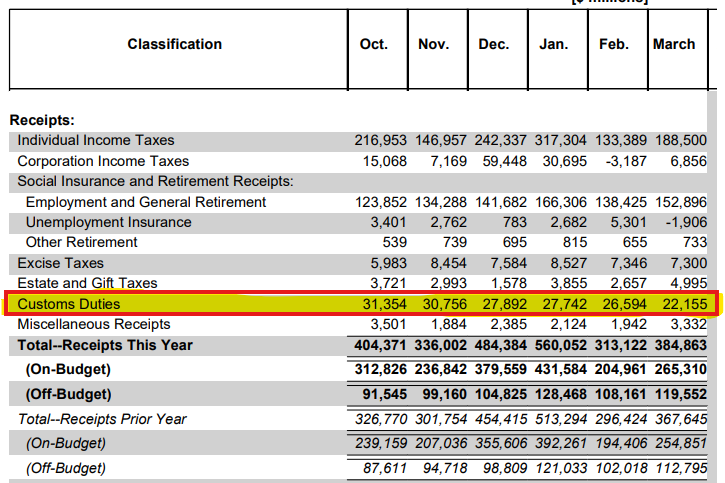

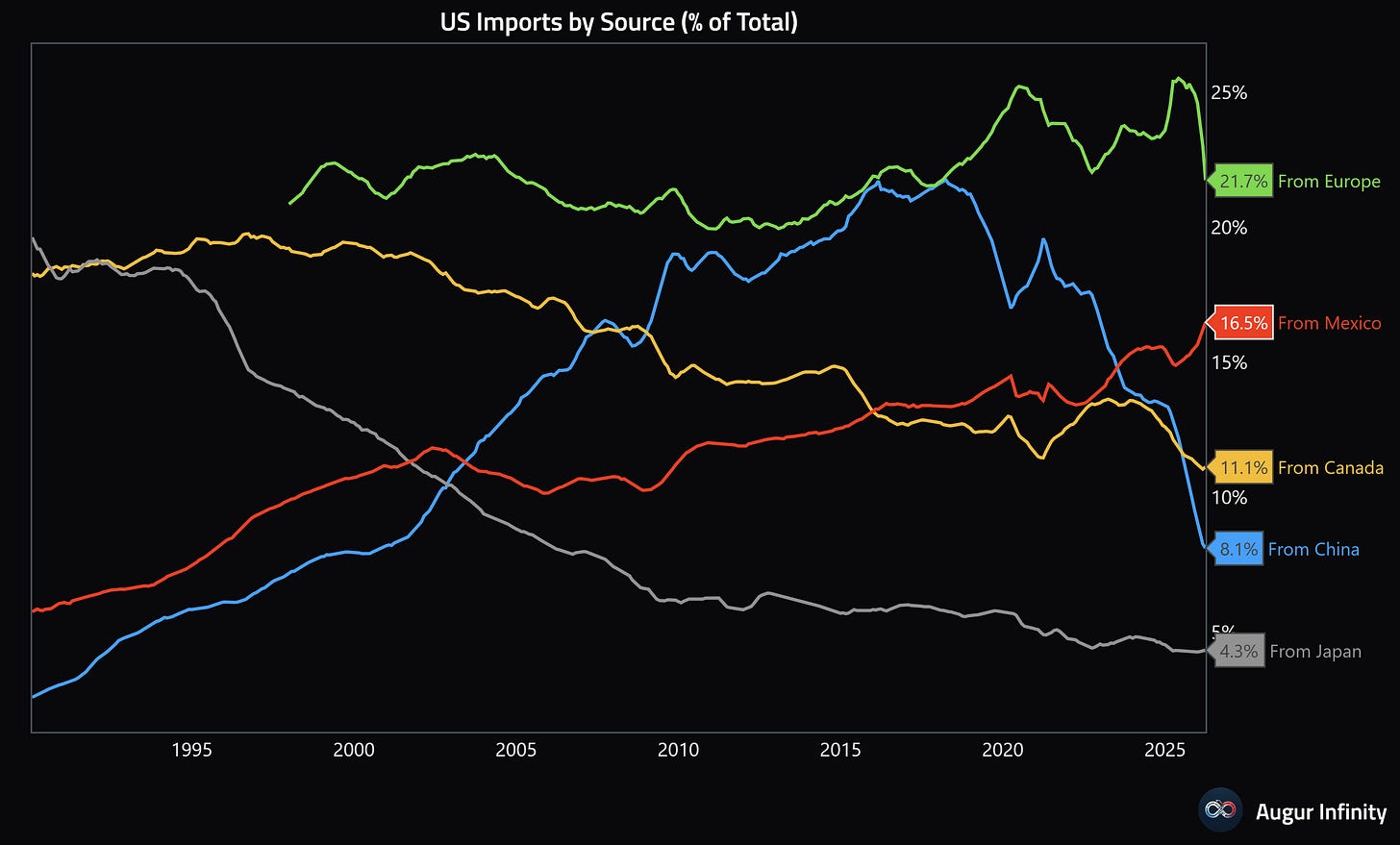

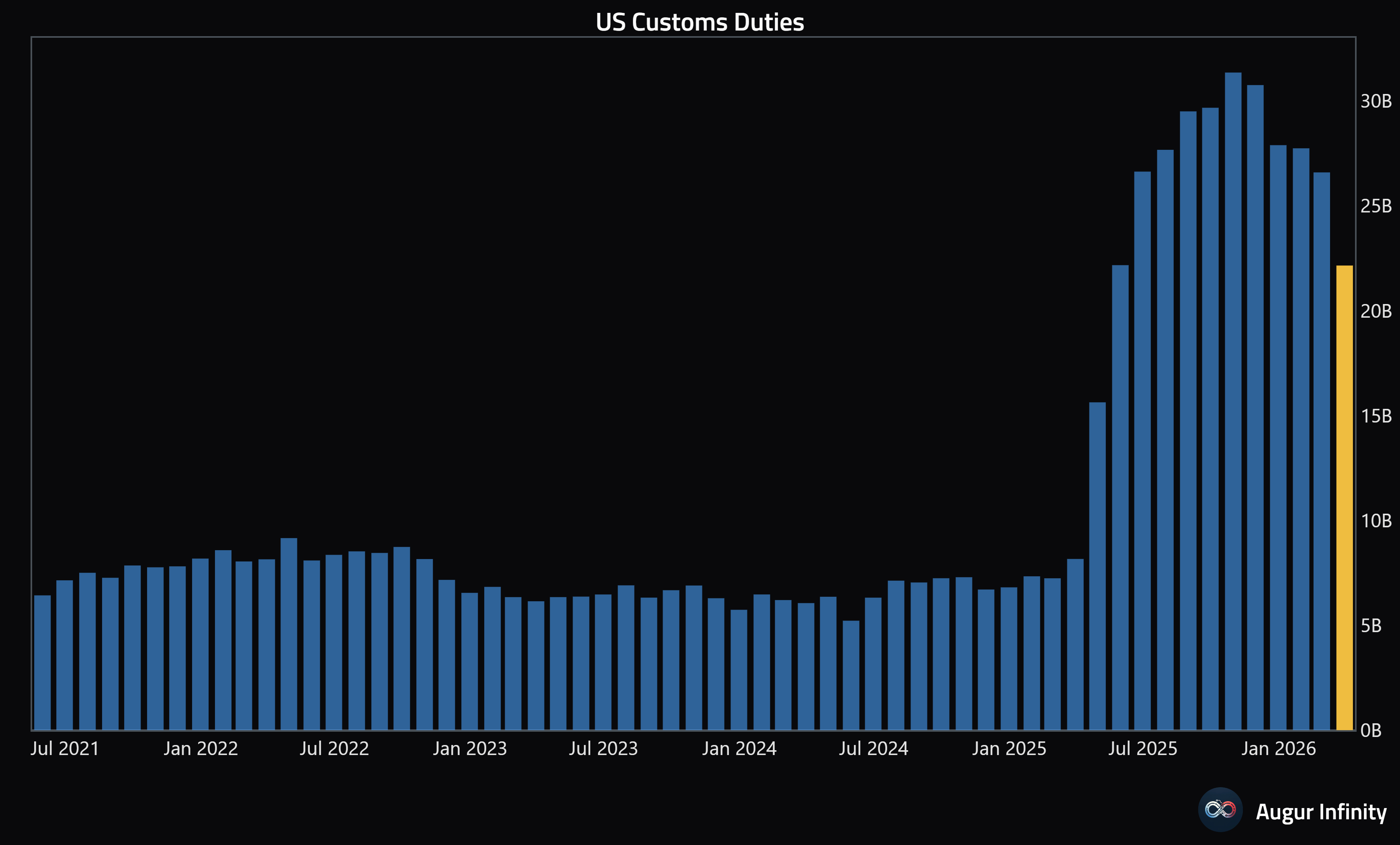

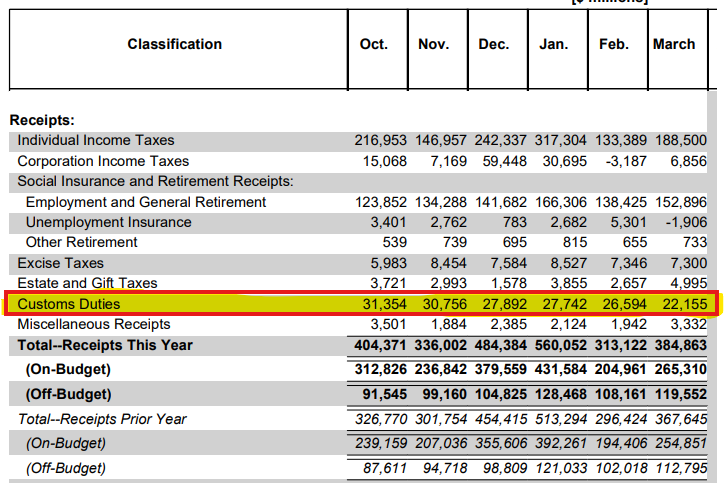

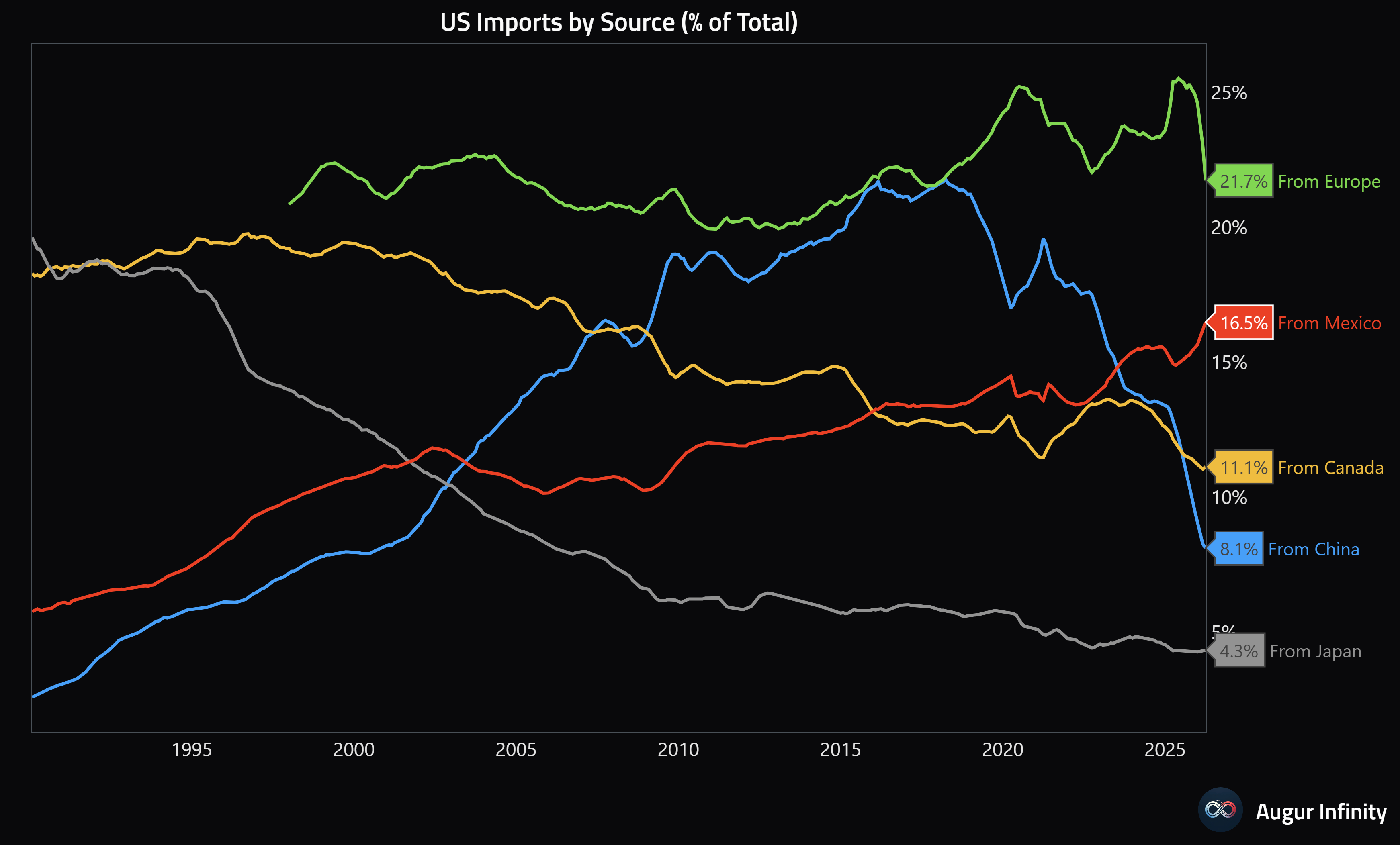

Declining tariff revenues heading into 2026’s first Trump-Xi summit.

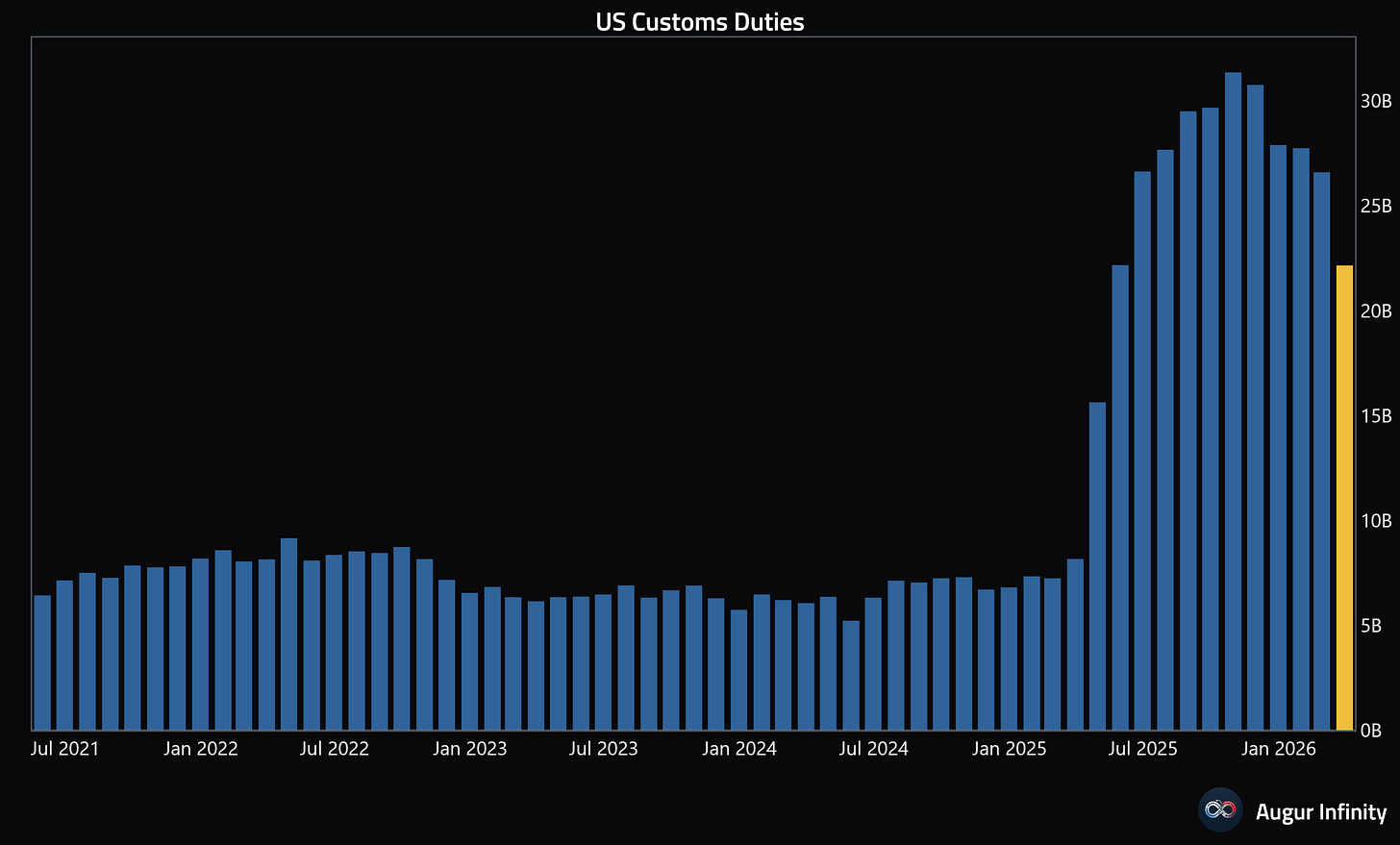

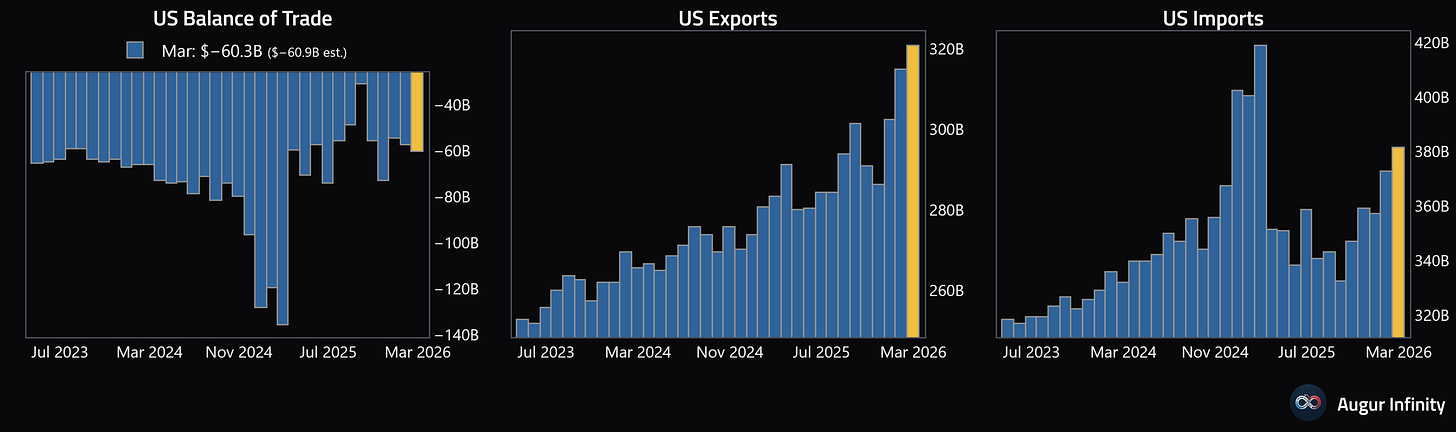

Among the list of failures the Iran war has made mainstream media forget about (eg Epstein files, Pam Bondi, affordability crisis), tariffs is one of them. Monthly tariff revenues are down over -30% since October 2025.

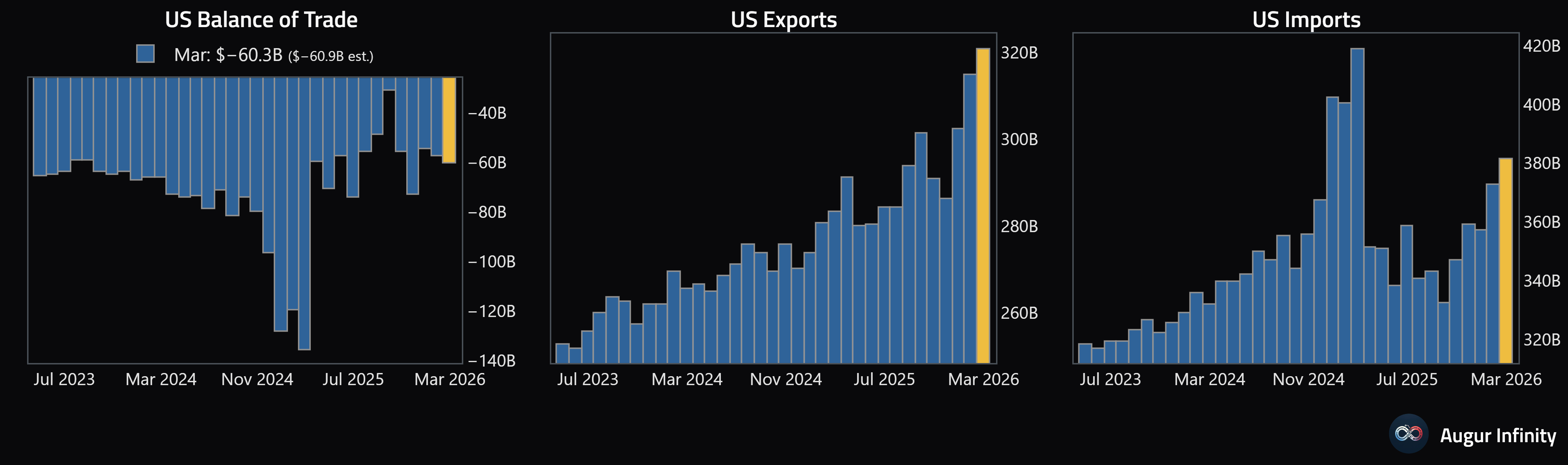

This decline in tariff revenues is ongoing despite a 7% increase in the monthly import volume which means the effective tariff rate has fallen even more.

This past week the Supreme Court struck down Section 122 tariffs which were the Trump administration’s replacement for the IEEPA tariffs which were previously struck down. It’s a nuanced headline because it only blocks the tariffs for two private importers and the tariffs remain in place for all other importers while the appeals play out. These tariffs expire in July and are likely to be replaced by Section 301 tariffs after that, with appeals and court cases dragging out well into 2027.

In 2023 and 2024 the US collected ~$80B in tariffs per year, that rose to $260B in 2025 and is likely to end 2026 somewhere in that same neighborhood. While it is nothing novel to say peak tariff hysteria is behind us, taking that one step further it may be the case that from here the majority of tariff risks lie to the downside which equates to upside growth / increased trade. Additionally, with supply chains now having over a year to adjust, it seems to me that the Trump-Xi meetings carry much lower stakes this year than last.

Hope everyone has a great week ahead. Tell your mom you love her today!

Just discovered your substack through the show and I am so happy to be learning from you guys. Keeps things level-headed when asset prices are going crazy.

Any recommendations on resources to learn from to become as well-informed as you guys?

Cheers!