Scouting the Tape - May 23, 2026

(Unique) macro idea generation and (insightful) market thoughts.

It’s been a quieter time in the markets for me. There’s a lot of things that don’t make sense, like equities for example. And there are other parts that are just uncertain and unknown at this juncture. I have a number of theses I think will work well over the back half of the year but it’s requiring patience for the right time and entries to put them on and grow conviction behind. In the meantime we’ll just keep our finger on the pulse and await some fat pitches like we capitalized on in Q1. As a macro-focused trader/investor and often contrarian-biased, I make most of my money in one or two multi-month stretches each year. It’s funny how patience and doing nothing is sometimes the most difficult posture.

Tyler and I recorded our first round up with the new haircuts. We missed Felix as he couldn’t make it this week. Thank you to everyone who helped raise $10,500(!!!) to support an amazing cause. You guys are the best.

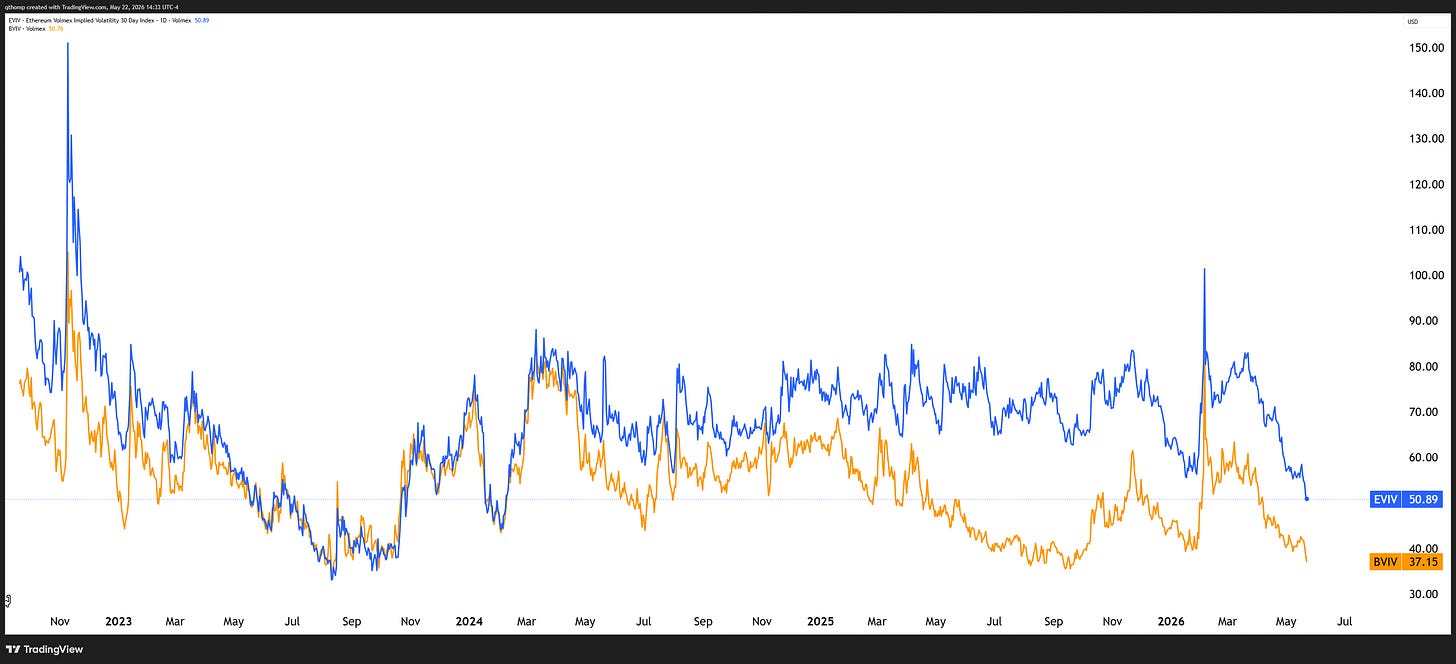

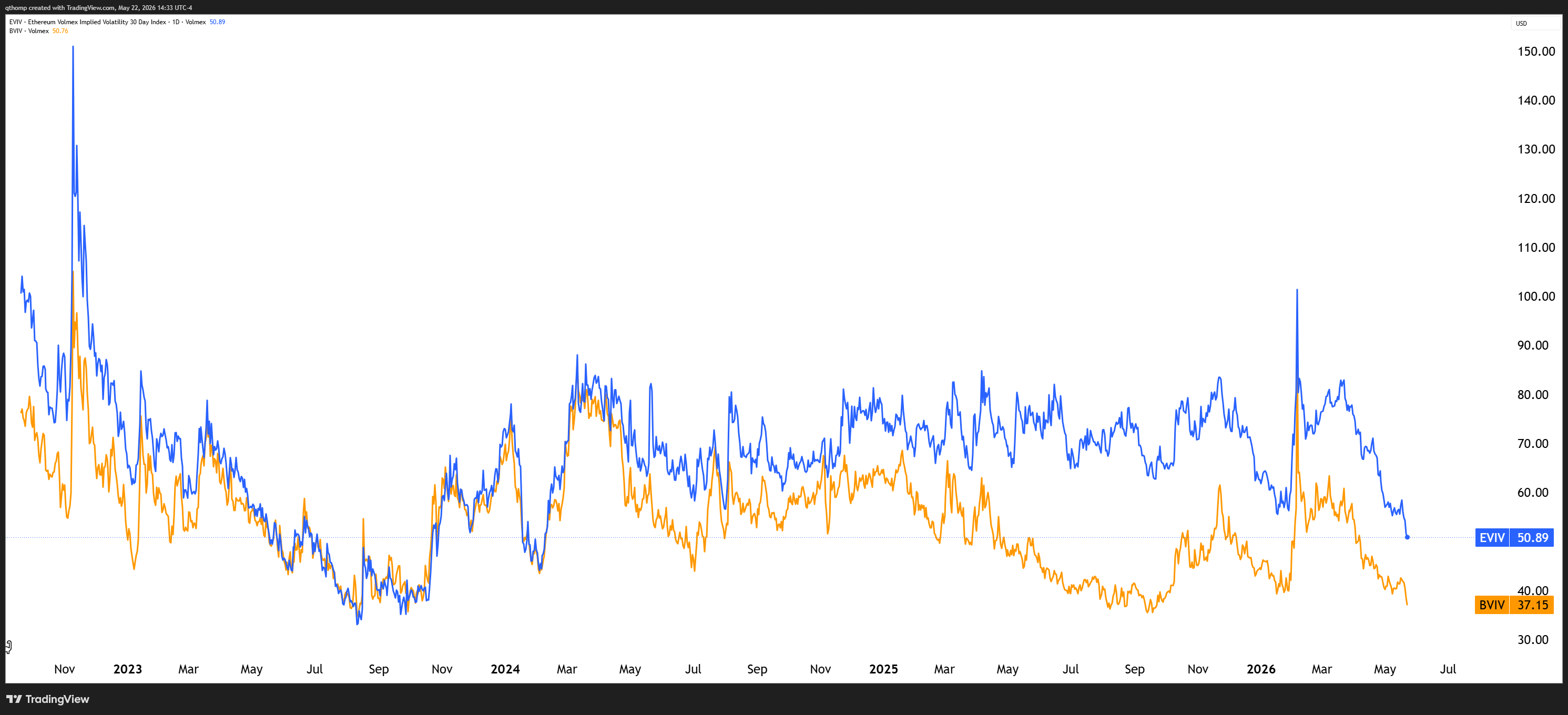

Ethereum implied volatility falls to nearly 2.5 year low.

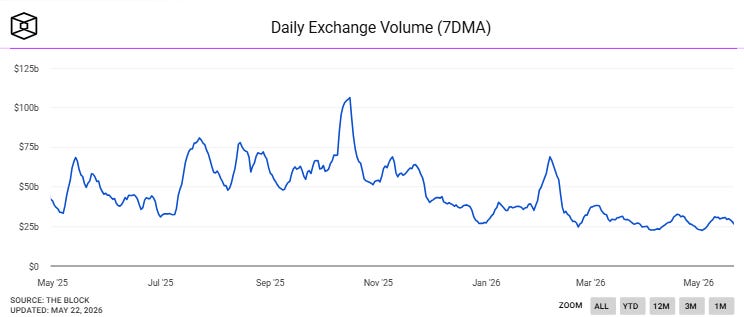

Crypto tends to struggle during summer months as volatility, a core attraction of the asset class, dissipates. It looks like that process is beginning as we head into the first holiday weekend of the summer as implied volatility metrics are plummeting.

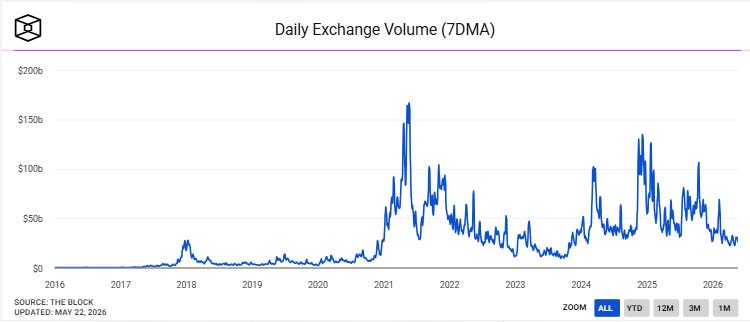

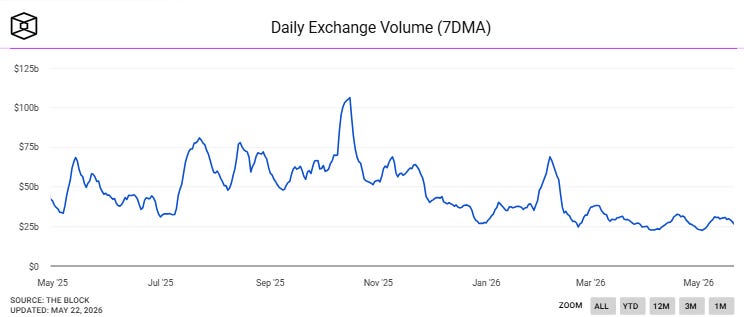

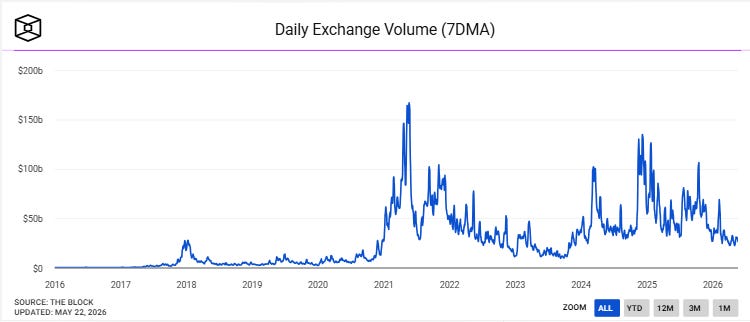

Looking at daily exchange volumes, the data tends to align. I’m not sure what resuscitates this over the coming months.

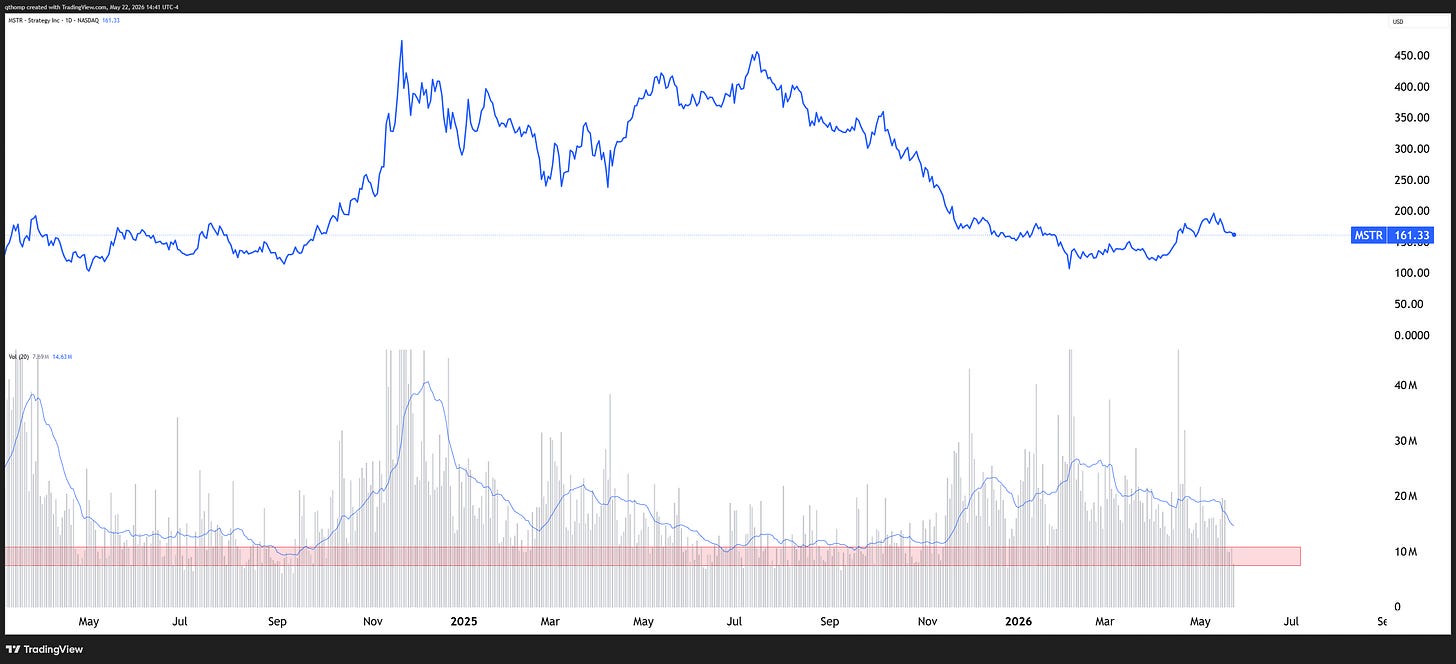

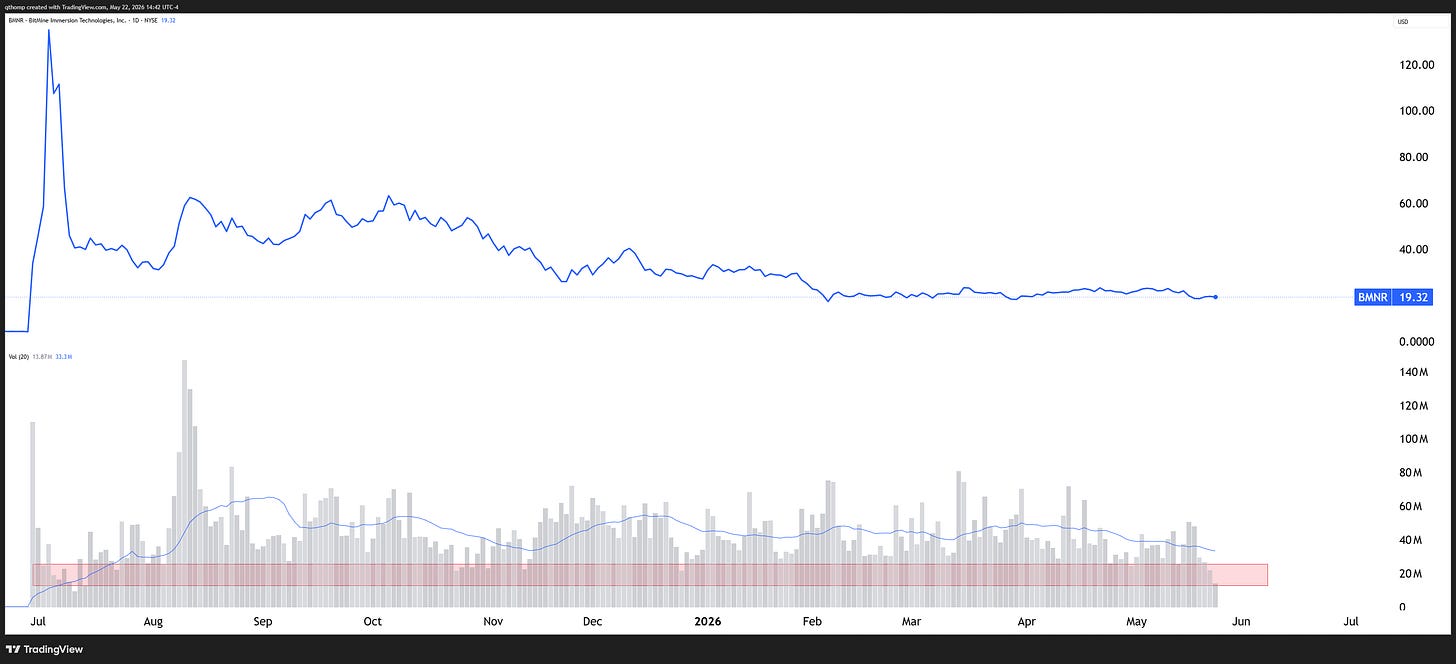

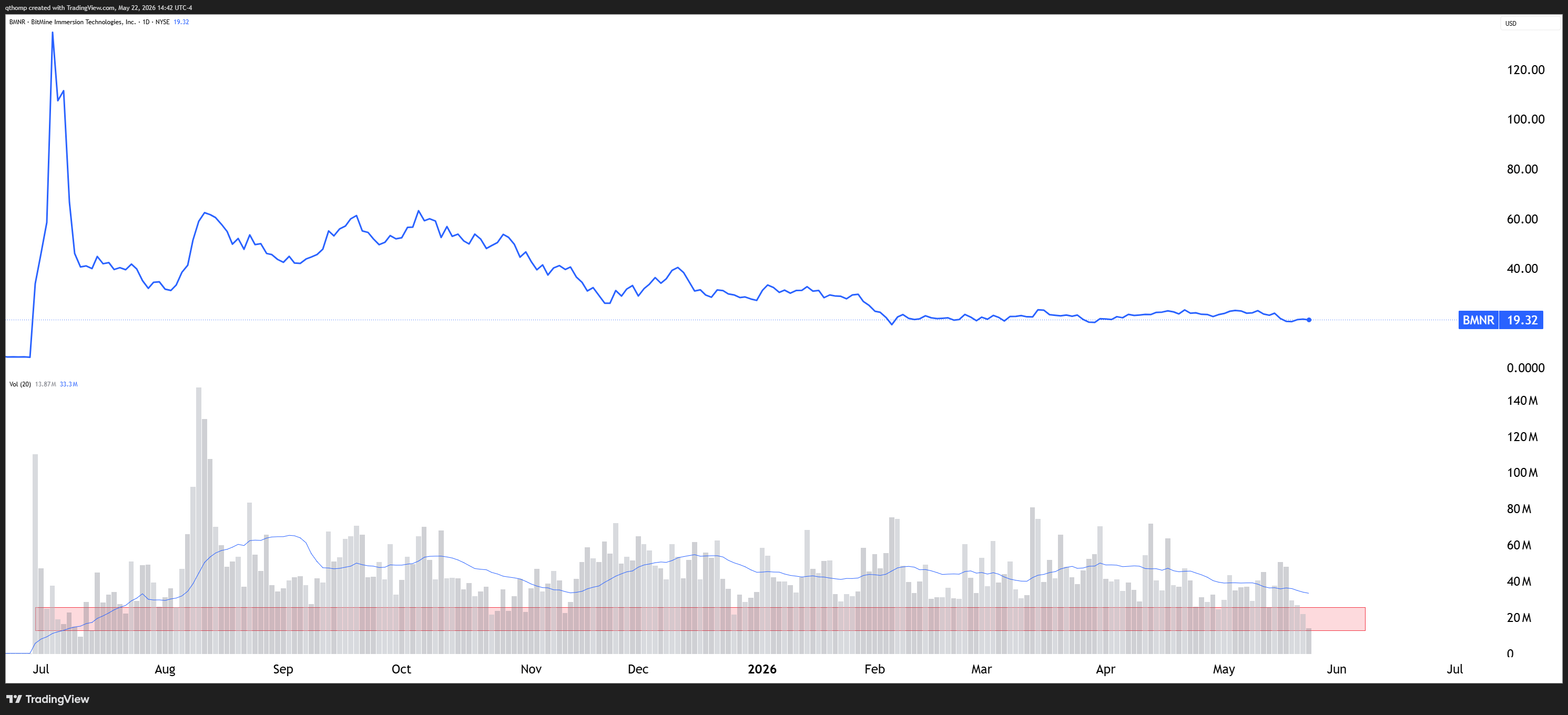

MSTR and BMNR trading volumes paint a similar picture. Lack of volume is problematic for them because it inhibits their ability to sell stock and buy more.

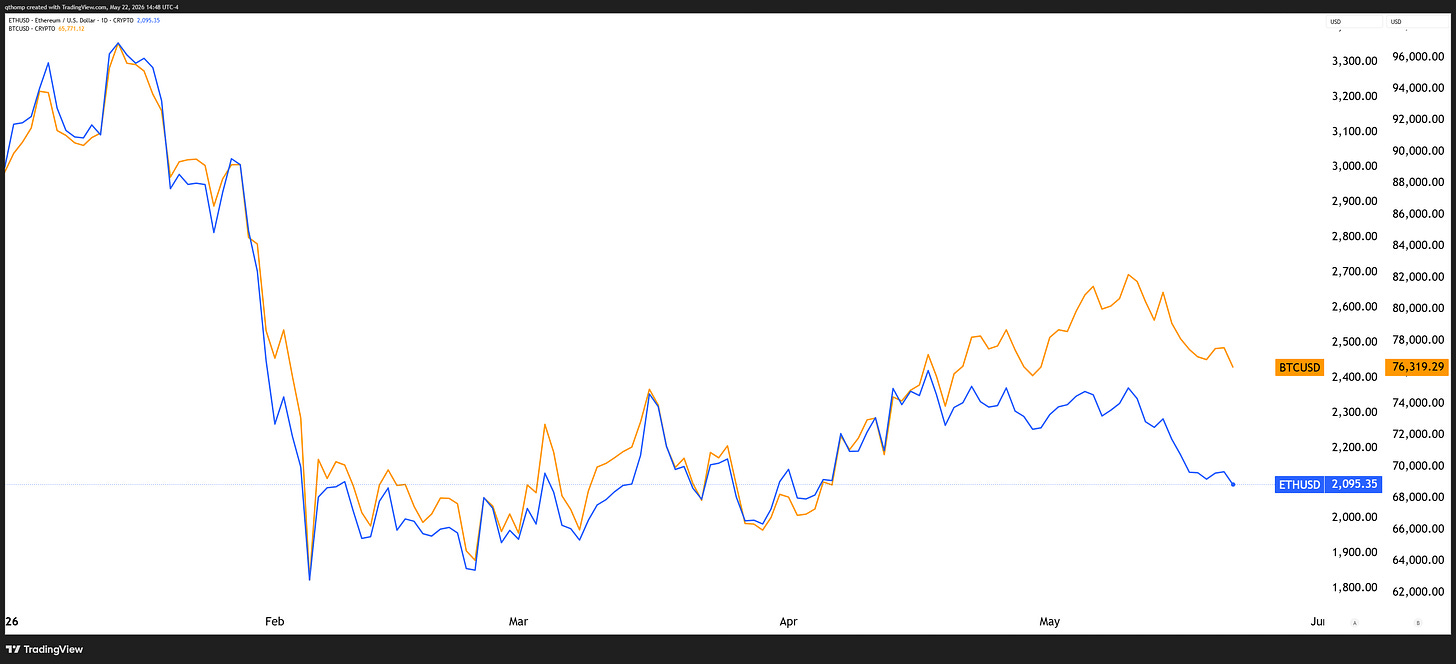

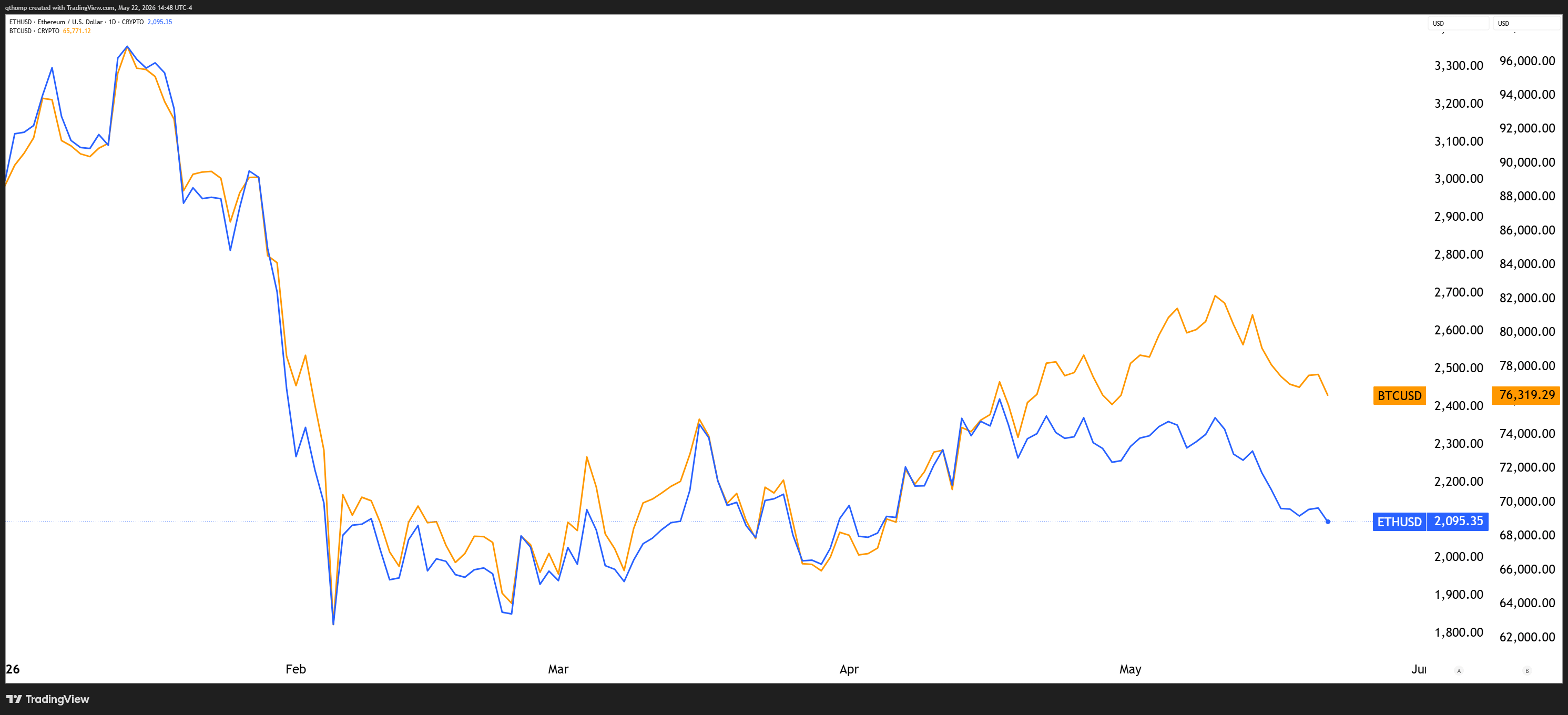

Below is the YTD charts of Bitcoin and Ethereum. Not a pretty picture considering MSTR has acquired over $13B of BTC and BMNR has acquired over $2B of ETH.

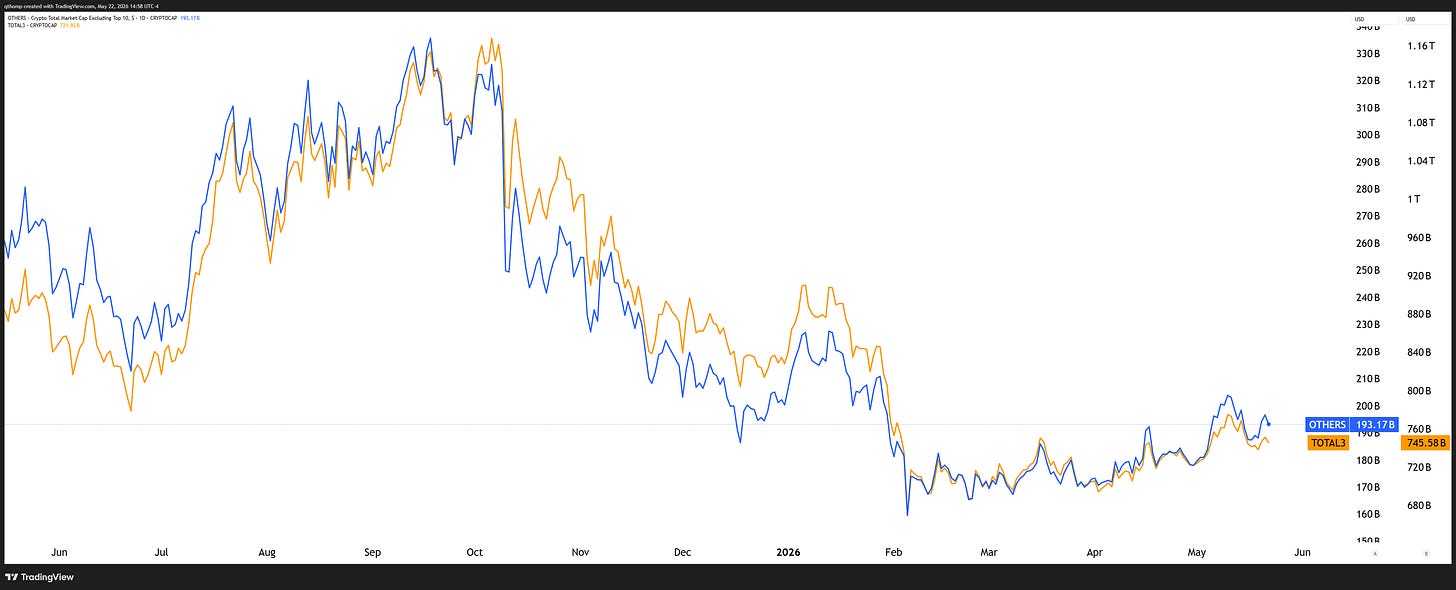

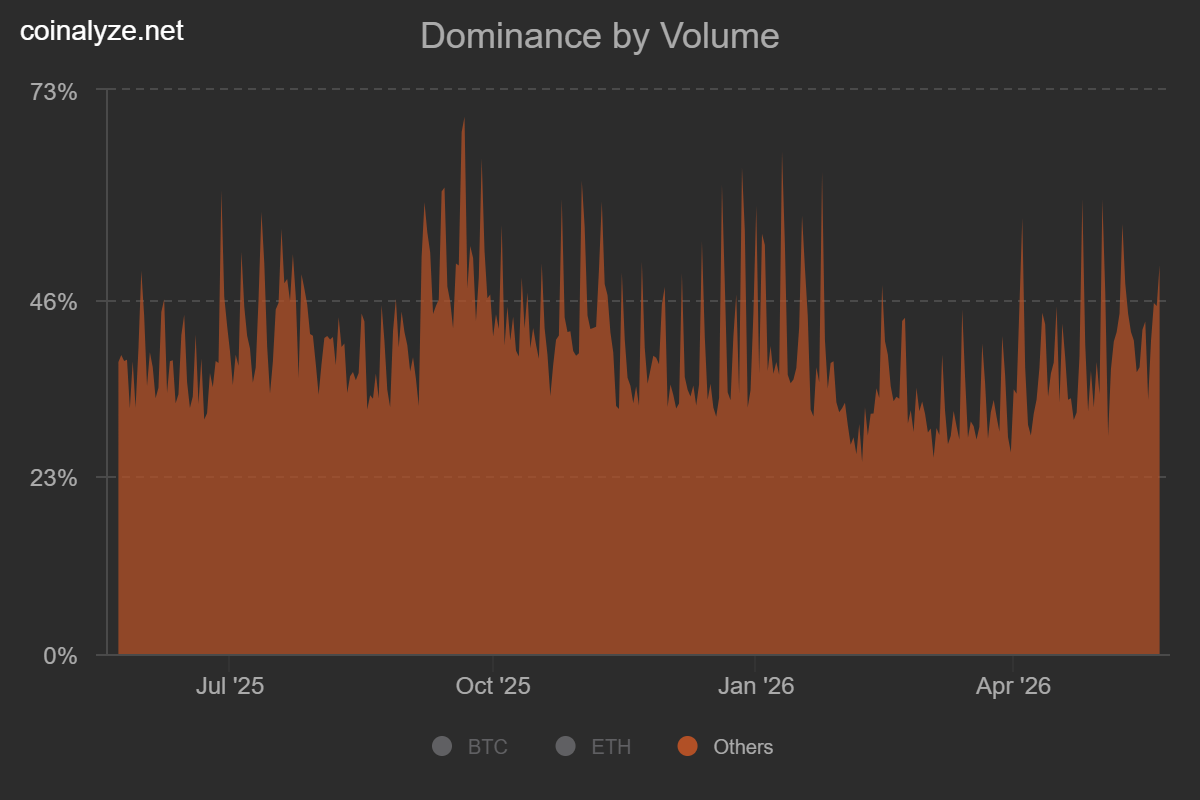

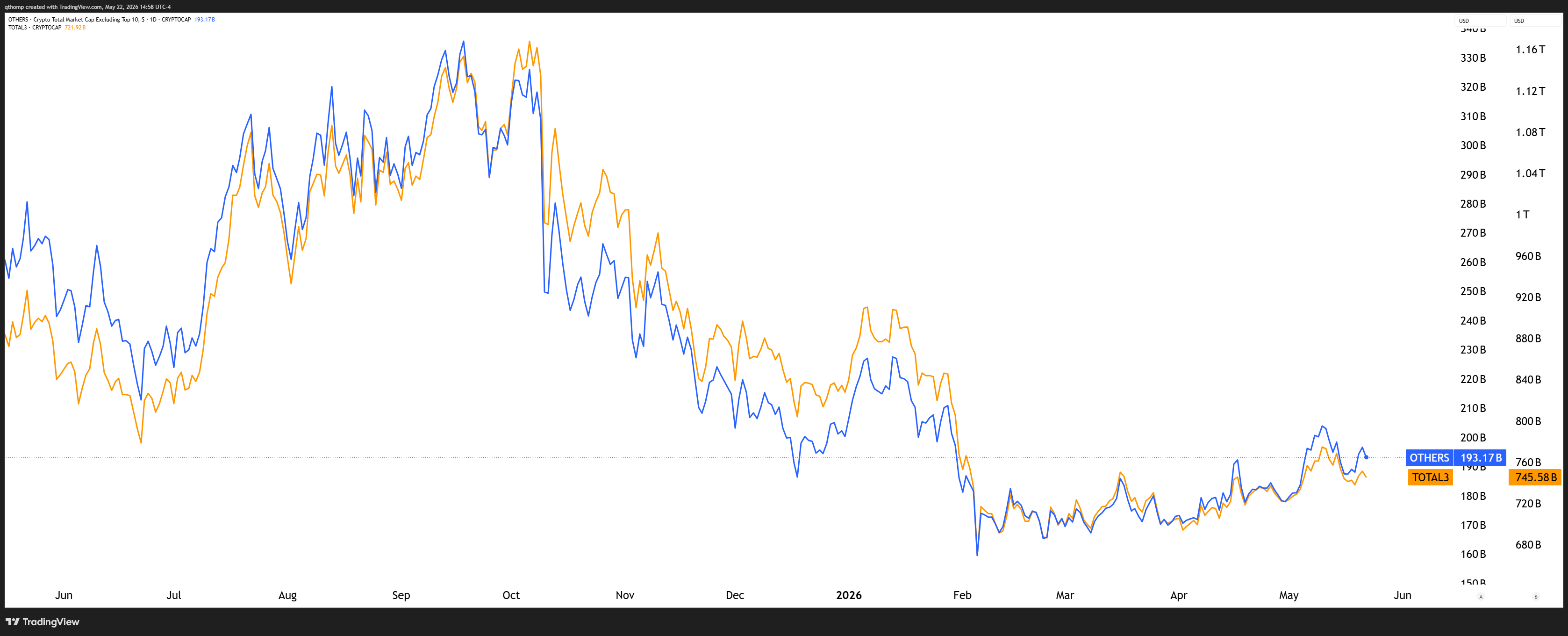

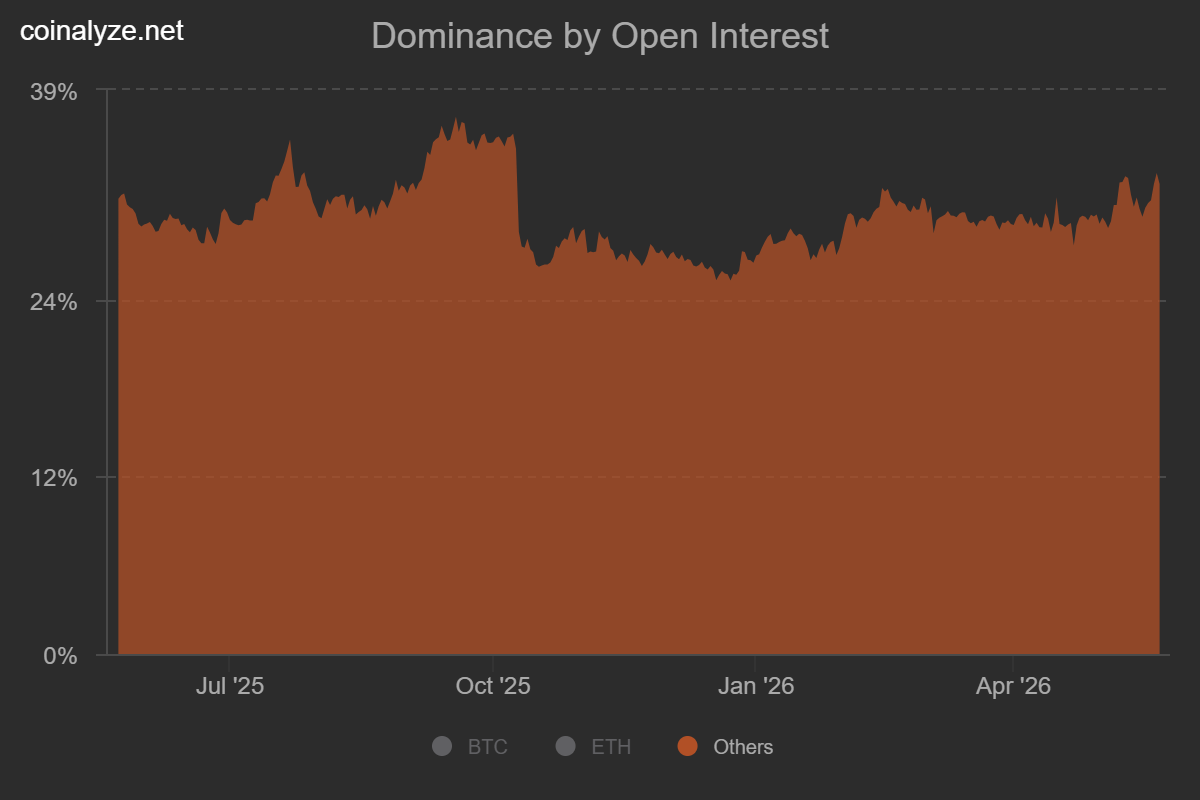

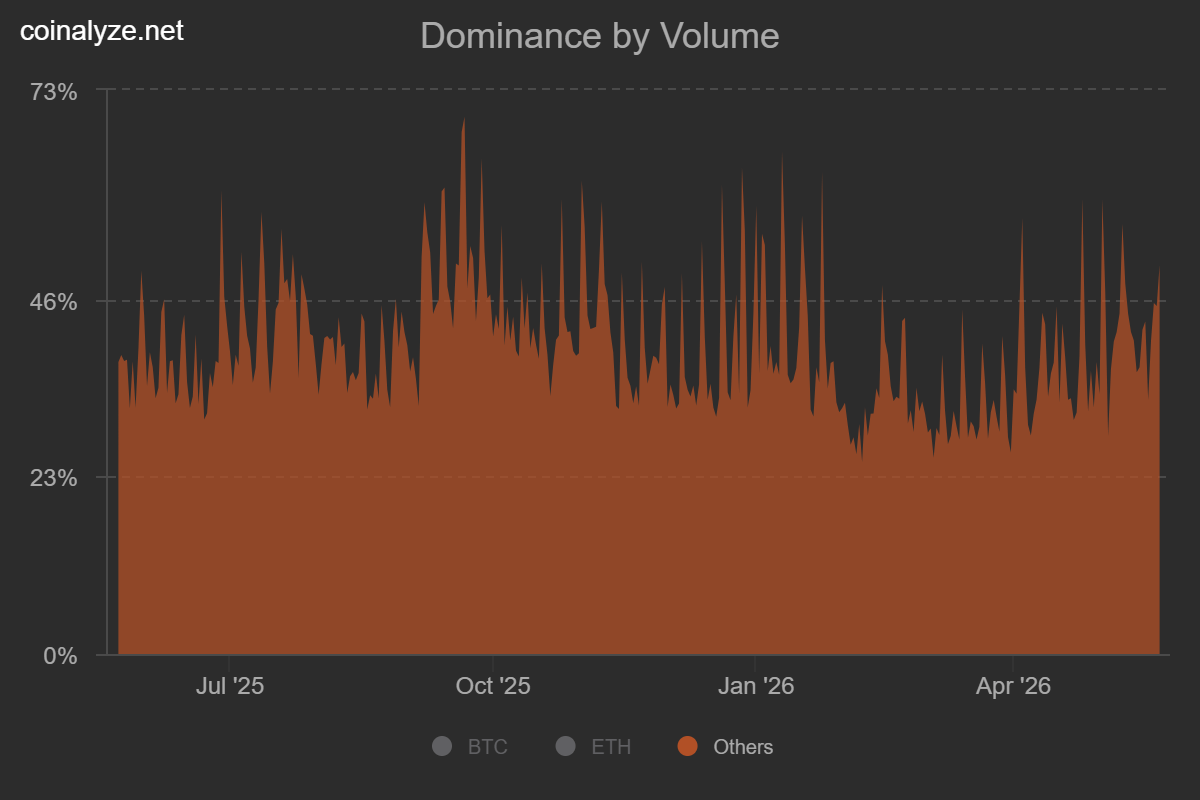

There have been a few pockets of strong performance across altcoins like HYPE, ZEC, VVV and NEAR for on the back of a variety of narratives ranging from traditional finance adoption, privacy and AI. Overall, OTHERS (total industry market cap excluding top 10 coins) and TOTAL3 (total industry market cap excluding BTC and ETH) are both still below their yearly opens and appear to be putting in a higher low.

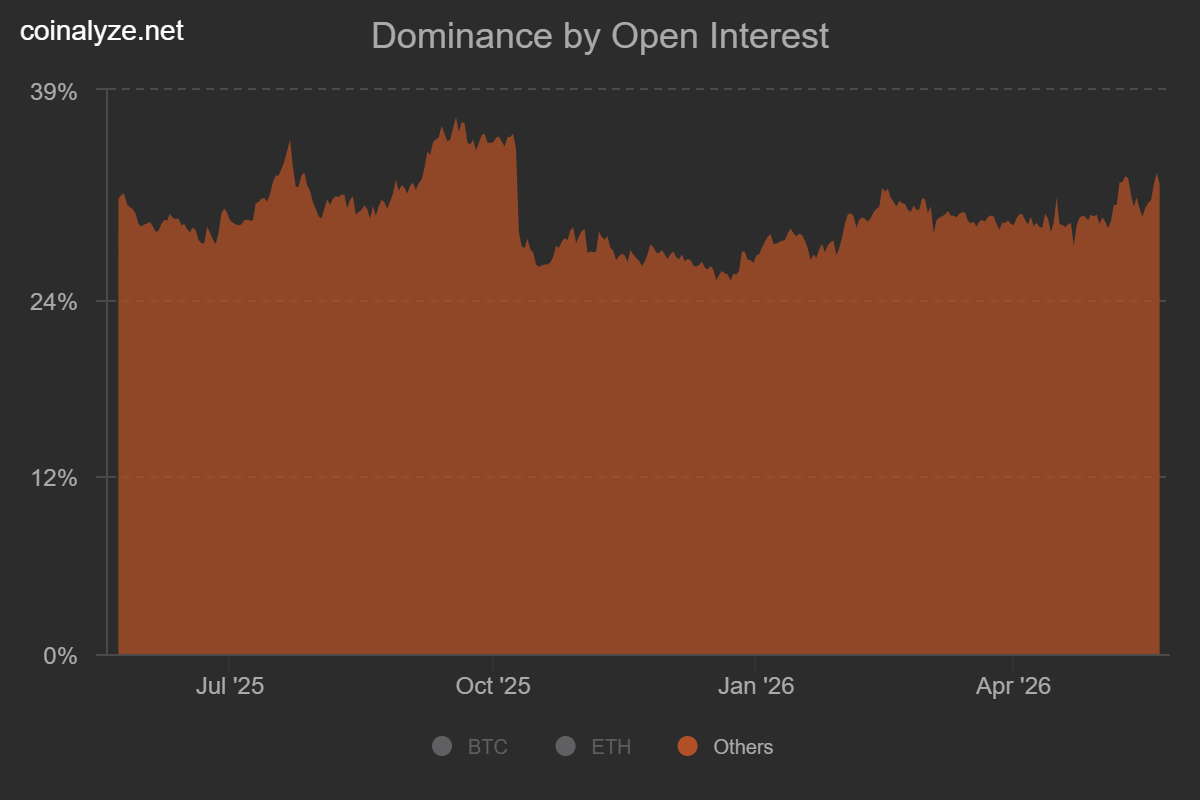

Measures looking at altcoins as a percentage of total trading volume and open interest are often good signals for frothiness and both are fairly elevated.

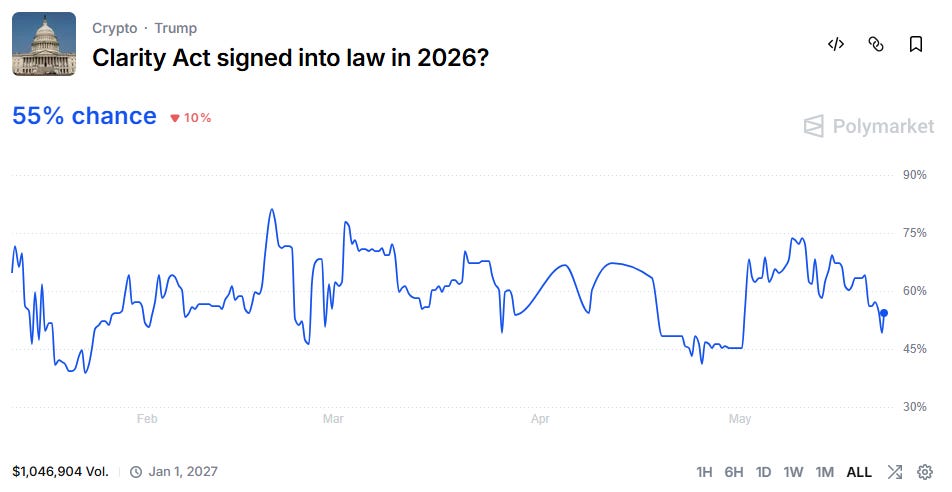

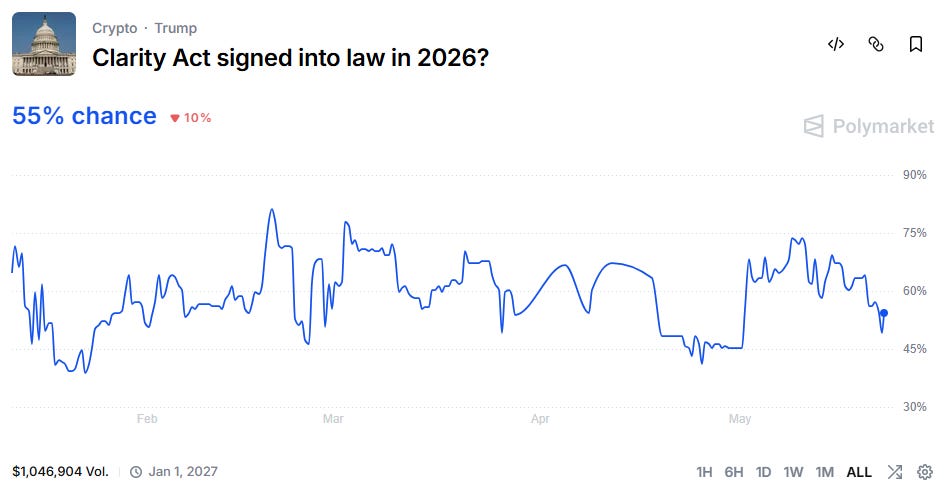

Maybe the passing of the Clarity Act, if it happens, can provide some relief. Whether that potential move sticks or is used as exit liquidity will likely be a good indicator of what’s to come over the summer months.

Warsh’s new Fed leadership is as clear as mud.

Is he going to be a hawk or dove? Where is the committee at? How will he navigate such a conflicting balance of Trump’s loose policy goals with a worsening inflation picture?

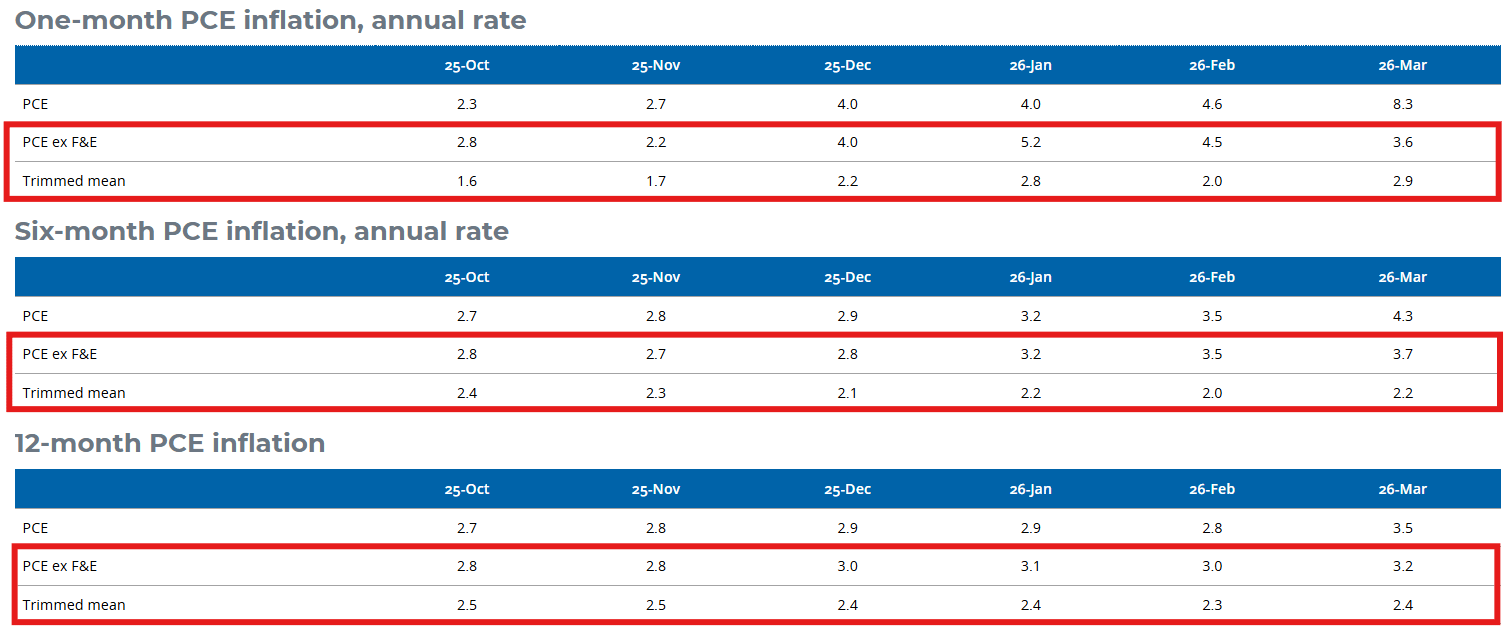

We know from Warsh himself that he is in favor of “improving” the Fed’s data tools and analytics. In particular he has a preference for using trimmed mean inflation measures as opposed to Powell’s favored PCE. That notion is oddly convenient given the discrepancy in the metrics of late and significantly lower readings using the trimmed mean methodology. The old running joke was that the Fed was going to start using CPI ex-everything as their benchmark inflation guide, but as we know in today’s world, there are no jokes and conspiracy theories any longer because they all come true.

DCP@DcpcooksNow is a good time to dig into Warsh’s preferred inflation gauge PCE was Powells gauge Does this impact the feds credibility is one of the questions we face going forwarddallasfed.orgTrimmed Mean PCE Inflation rate, March 20265:23 PM · May 21, 2026 · 5.67K Views6 Replies · 5 Reposts · 24 Likes

DCP@DcpcooksNow is a good time to dig into Warsh’s preferred inflation gauge PCE was Powells gauge Does this impact the feds credibility is one of the questions we face going forwarddallasfed.orgTrimmed Mean PCE Inflation rate, March 20265:23 PM · May 21, 2026 · 5.67K Views6 Replies · 5 Reposts · 24 Likes

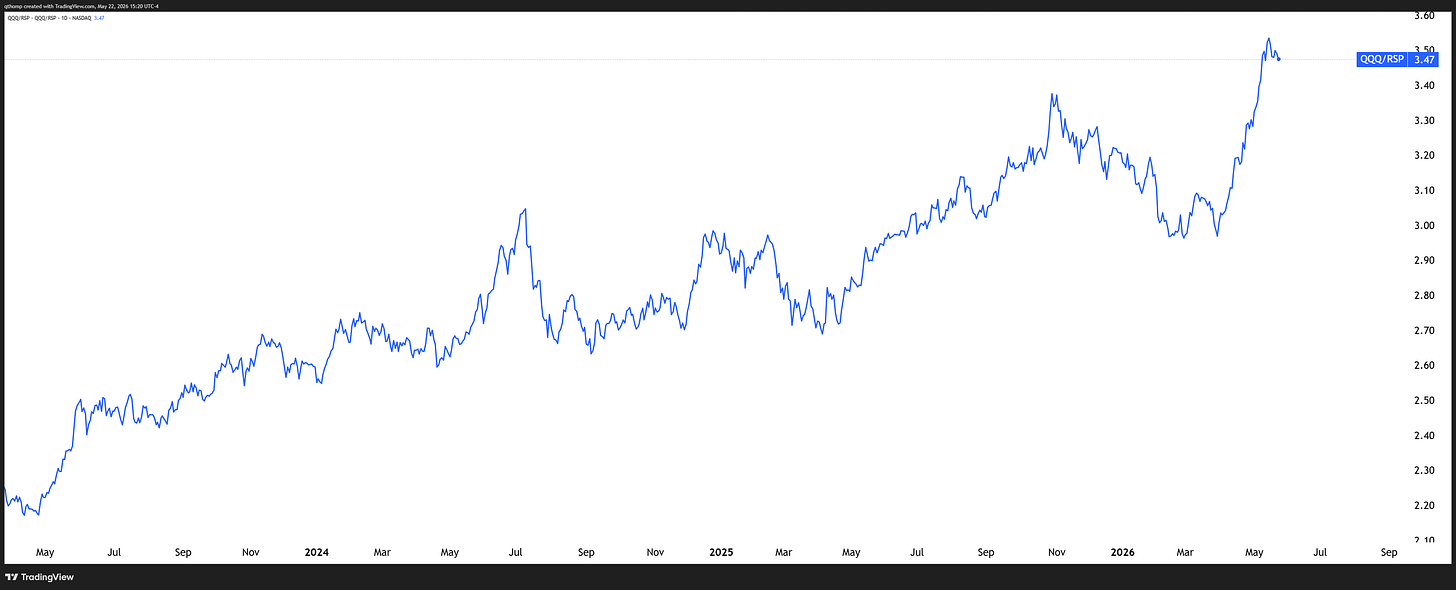

The situation is actually quite complex because of how interventionist Fed policy has become over the years, which has helped lead to one of the largest inequality problems ever witnessed in the nation’s history. There’s never been a bigger divergence between consumer sentiment surveys and the stock market.

𝐄𝐟𝐟𝐢𝐜𝐢𝐞𝐧𝐭 𝐌𝐚𝐫𝐤𝐞𝐭 𝐇𝐲𝐩𝐞@EffMktHypeeek

𝐄𝐟𝐟𝐢𝐜𝐢𝐞𝐧𝐭 𝐌𝐚𝐫𝐤𝐞𝐭 𝐇𝐲𝐩𝐞@EffMktHypeeek 2:12 PM · May 22, 2026 · 8.52K Views1 Reply · 1 Repost · 18 Likes

2:12 PM · May 22, 2026 · 8.52K Views1 Reply · 1 Repost · 18 LikesThis trend is becoming increasingly problematic for Trump as well because it’s coming from independents and republicans too, not just democrats.

Michael McDonough@M_McDonoughUniversity of Michigan Consumer Sentiment by Political Party Affiliation:

Michael McDonough@M_McDonoughUniversity of Michigan Consumer Sentiment by Political Party Affiliation: 2:12 PM · May 22, 2026 · 3.1K Views5 Reposts · 13 Likes

2:12 PM · May 22, 2026 · 3.1K Views5 Reposts · 13 LikesWarsh can actually help fix the problem by reducing the duration of the Fed’s balance sheet and let long end yields rise, thus steepening the yield curve and rebalancing the economy in favor of main street and small businesses who have been directly hurt by policies of the last few years. The problem is that rising yields is at direct odds with Trump and Bessent’s goals of propping up stocks.

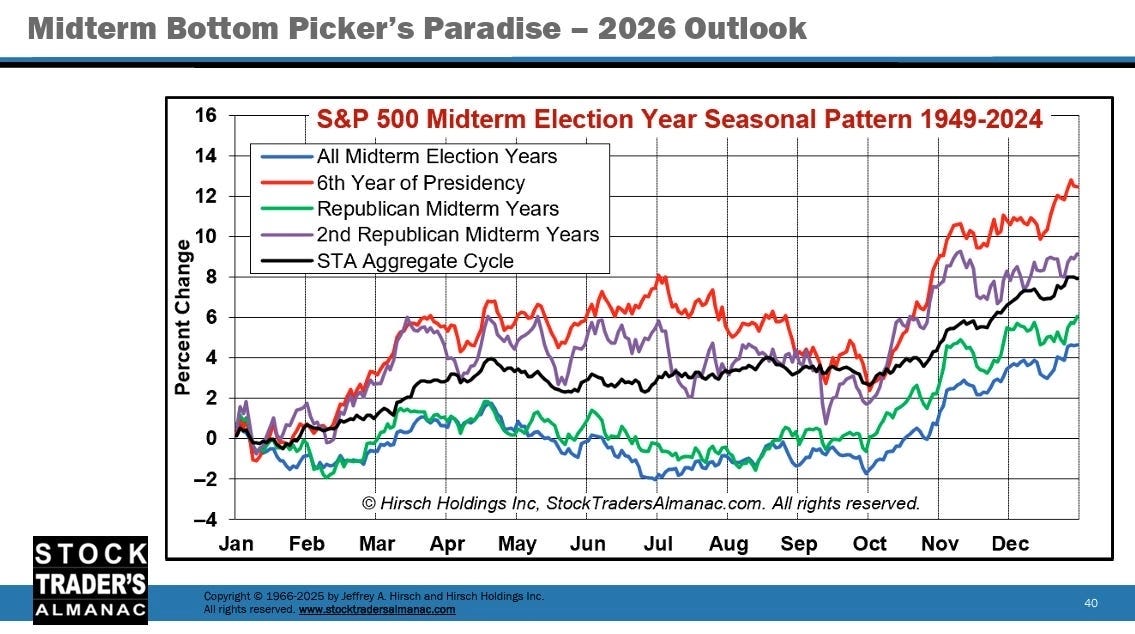

History would also be on Warsh’s side as during many midterm election years, the policy focus tends to follow that path to help main street in attempt to win over the hearts and minds of voters and stocks tend to lose. Thus far this administration has bucked that trend, which may come as a headscratcher to many because it continues to benefit the same few same mega cap tech and AI winners while coming at the direct expense of the many across main street.

Not too long ago Trump was announcing credit card interest rate caps and housing market stimulus measures aimed at the lower and middle class. With under 6 months until November’s midterms, it remains to be seen whether declining ratings and approval data will trigger a shift back in that direction.

Quinn Thompson@qthompThe first potential signs of another major Trump 🌮 His political capital amongst voters is "running on E" and he needs to divert attention away from the failed Iran War as his polling and rating numbers decline. He's already brought the largest aircraft carrier and strike

Quinn Thompson@qthompThe first potential signs of another major Trump 🌮 His political capital amongst voters is "running on E" and he needs to divert attention away from the failed Iran War as his polling and rating numbers decline. He's already brought the largest aircraft carrier and strike

Giovanni Staunovo🛢 @staunovo#Iran: Over the past 24 hours, 26 ships, including oil tankers, container ships, and other commercial vessels, passed through the Strait of Hormuz with the coordination and security of the IRGC Navy. Traffic through the Strait of Hormuz is being carried out with permission and in12:54 PM · May 20, 2026 · 27.6K Views7 Replies · 11 Reposts · 158 Likes

Giovanni Staunovo🛢 @staunovo#Iran: Over the past 24 hours, 26 ships, including oil tankers, container ships, and other commercial vessels, passed through the Strait of Hormuz with the coordination and security of the IRGC Navy. Traffic through the Strait of Hormuz is being carried out with permission and in12:54 PM · May 20, 2026 · 27.6K Views7 Replies · 11 Reposts · 158 Likes

Rates and bond market.

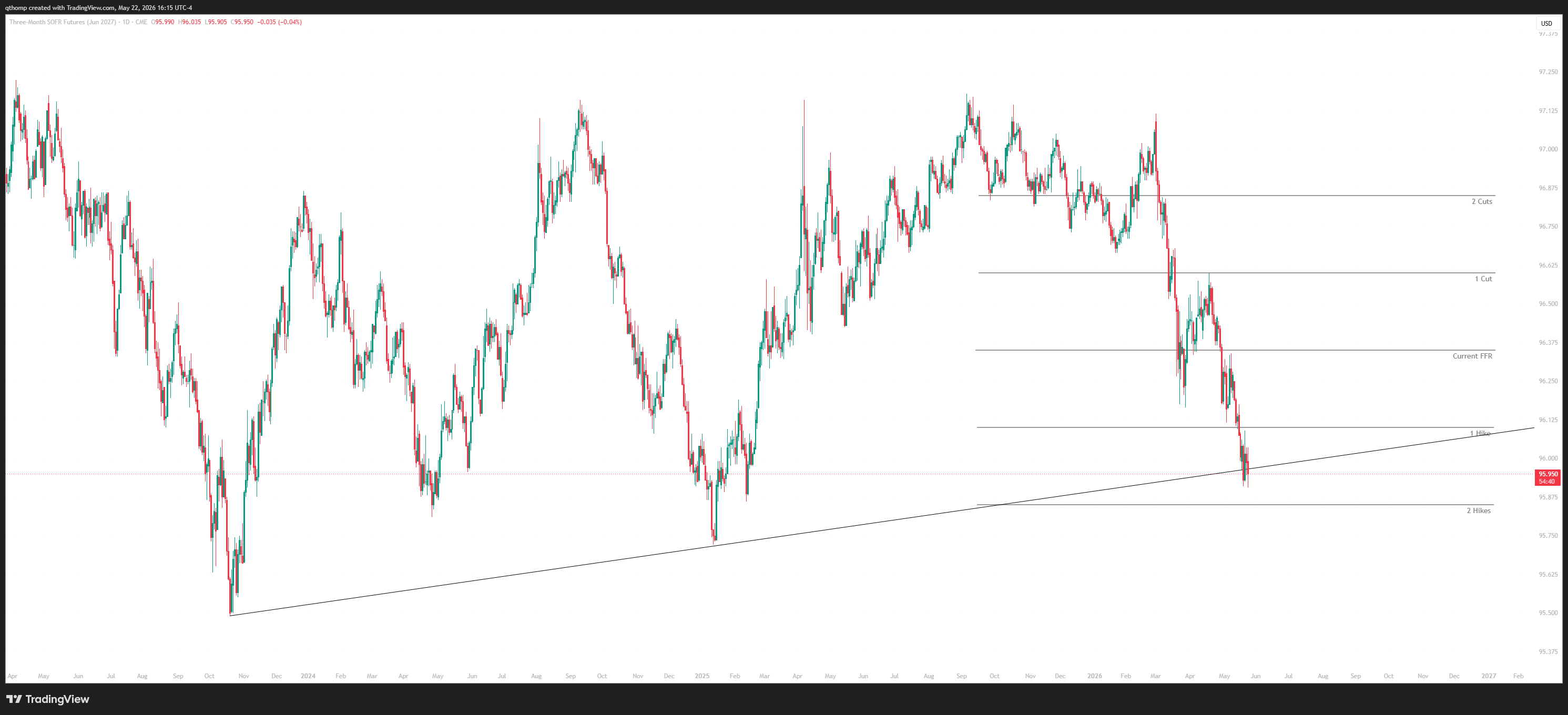

If you’ve been following our writing for the last few weeks you know we were shorting bonds on the basis of rising inflation amidst still okay growth and increasing pressure on central banks to turn hawkish. Last week I wrote about when it might be time to think about other parts of that trade and then this week I elaborated on that idea which got some pushback on X.

Quinn Thompson@qthompI’ve noticed some confusion around this tweet based on the interactions. Now more than ever, the discrepancies in moves across the yield curve will matter. We have been very short long duration bonds and elaborated at length why - that remains the case. SOFR futures are a very Quinn Thompson @qthompTime to start fading rate hikes. Global economy not nearly as strong as 2022 and consumer does not have cushion to absorb price hikes. Counterintuitively, it is exactly rising long end yields that are required to put the brakes on things to allow for looser FFR. The current10:20 AM · May 20, 2026 · 9.38K Views35 Likes

Quinn Thompson @qthompTime to start fading rate hikes. Global economy not nearly as strong as 2022 and consumer does not have cushion to absorb price hikes. Counterintuitively, it is exactly rising long end yields that are required to put the brakes on things to allow for looser FFR. The current10:20 AM · May 20, 2026 · 9.38K Views35 LikesI really liked this post from Variant Perception that does a good job of highlighting some key differences between 2022 and today. It is a much more two sided equation this go around given already higher real rates and a weaker economy.

Variant Perception@VrntPerceptionhot CPI + Hormuz = market fears of a 2022 stagflation redux But, our LPPL model last week triggered a Crash Exhaustion Buy on the 5y note future.

Variant Perception@VrntPerceptionhot CPI + Hormuz = market fears of a 2022 stagflation redux But, our LPPL model last week triggered a Crash Exhaustion Buy on the 5y note future. 2:31 PM · May 19, 2026 · 2.32K Views2 Replies · 3 Reposts · 27 Likes

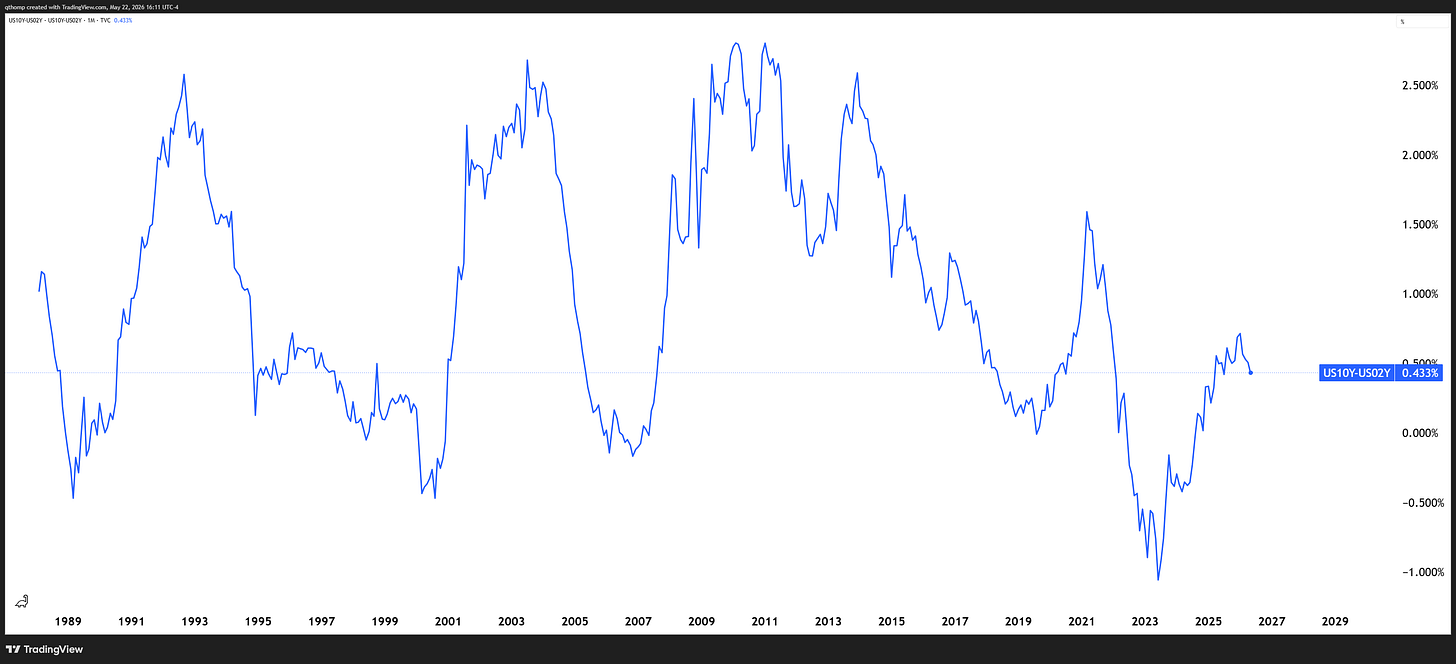

2:31 PM · May 19, 2026 · 2.32K Views2 Replies · 3 Reposts · 27 LikesIf the Fed and Treasury weren’t juicing markets so heavily via bond and currency market intervention, I think there is a case to be made to look through the energy price shock assuming it calms over the coming months. As I was mentioning earlier, if they removed the balance sheet accommodation and let the long end properly reprice 50-75 bps higher, that would help restrict policy enough to slow inflation and possibly allow for a looser Fed Funds rate. The problem is they are very unlikely to do that given the negative implications it would have on the market. But as of now, the 2s10s curve seems to me to be saying more of a growth problem than runaway inflation.

I haven’t pressed this position hard yet because I still think there is some wood to chop over the coming weeks as inflation prints will still show acceleration and the market is not showing many signs of being concerned about growth. I do think that changes though as we head into Q3. If the market gets to pricing in 2 hikes, I think that becomes a really attractive entry. There may also be better trades to express this view, like gold for example.

Hawkish vibes from an otherwise Trump ally in Waller is also along the lines of what you want to start seeing for this view to become increasingly priced in.

Nick Timiraos@NickTimiraosThis is a hawkish speech from Waller. While he doesn’t think hikes are needed in the near-term, he comes across as quite troubled by recent inflation developments. I’ll thread a few highlights:

Nick Timiraos@NickTimiraosThis is a hawkish speech from Waller. While he doesn’t think hikes are needed in the near-term, he comes across as quite troubled by recent inflation developments. I’ll thread a few highlights: 2:02 PM · May 22, 2026 · 73.6K Views28 Replies · 126 Reposts · 470 Likes

2:02 PM · May 22, 2026 · 73.6K Views28 Replies · 126 Reposts · 470 LikesThus far, credit spreads remain subdued, particularly in the higher rated parts of the market - which makes sense given the favorable policy conditions. There is a growing gap between the C rated junkier parts of the market and B rated paper that may be something to watch over the coming months. Historically this widening spread has preceded broader tightening conditions.

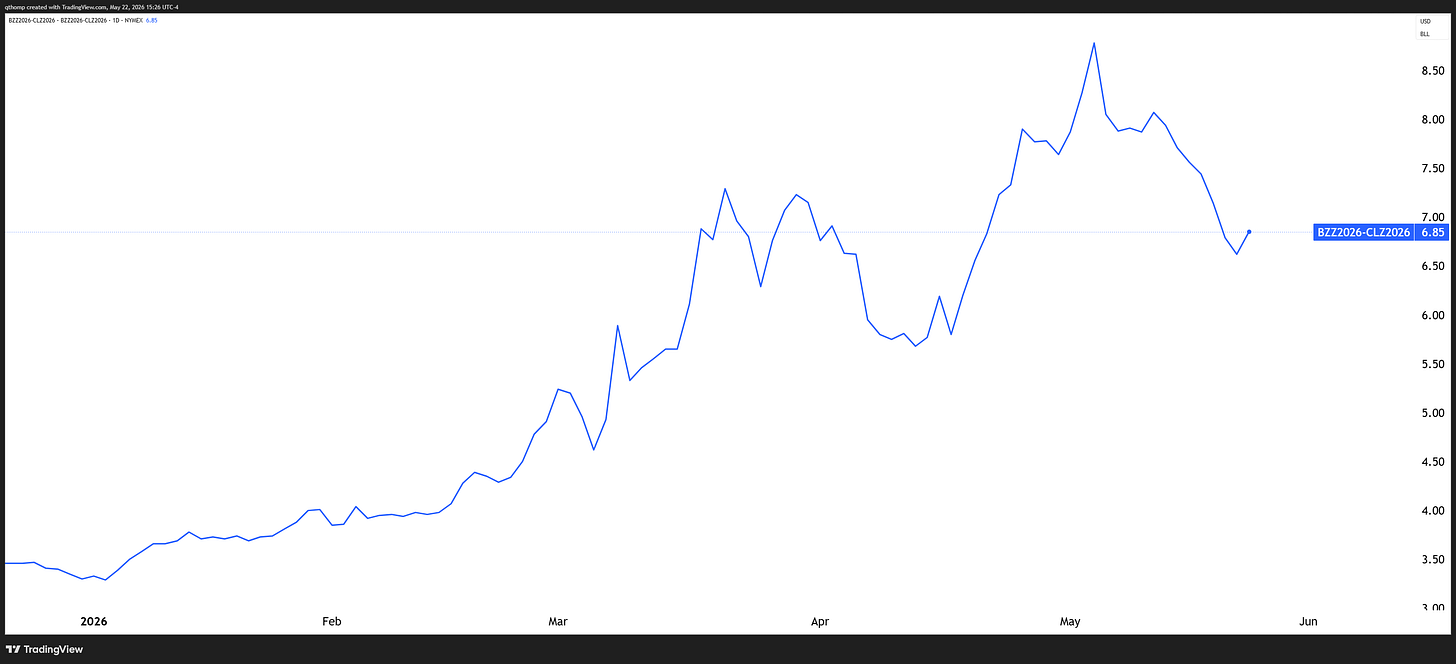

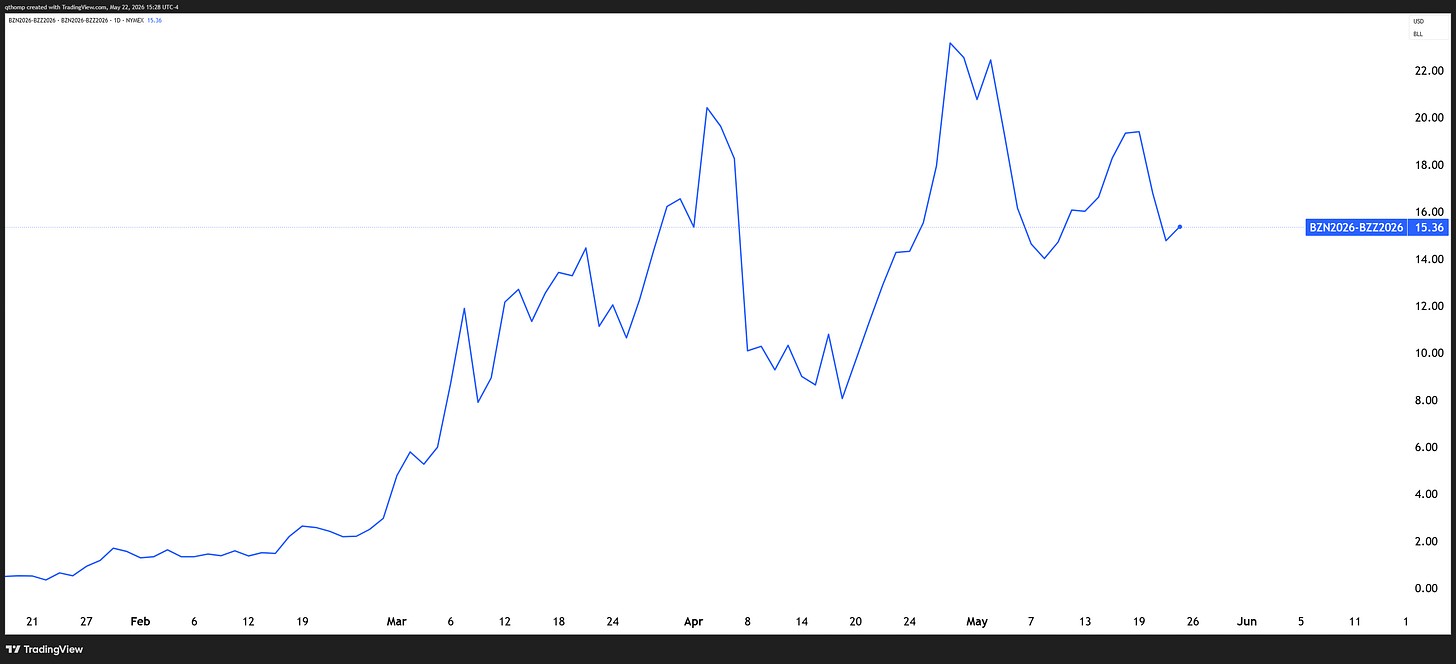

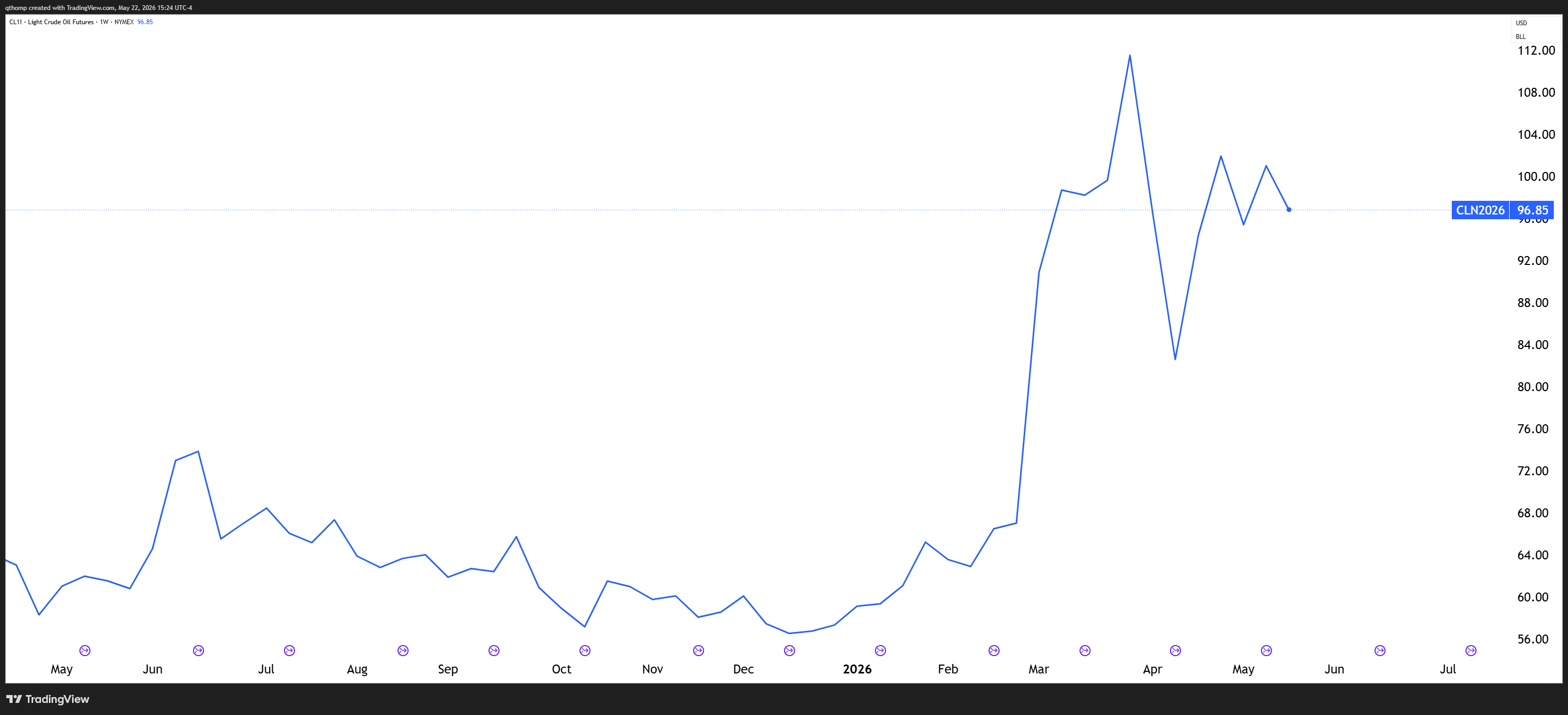

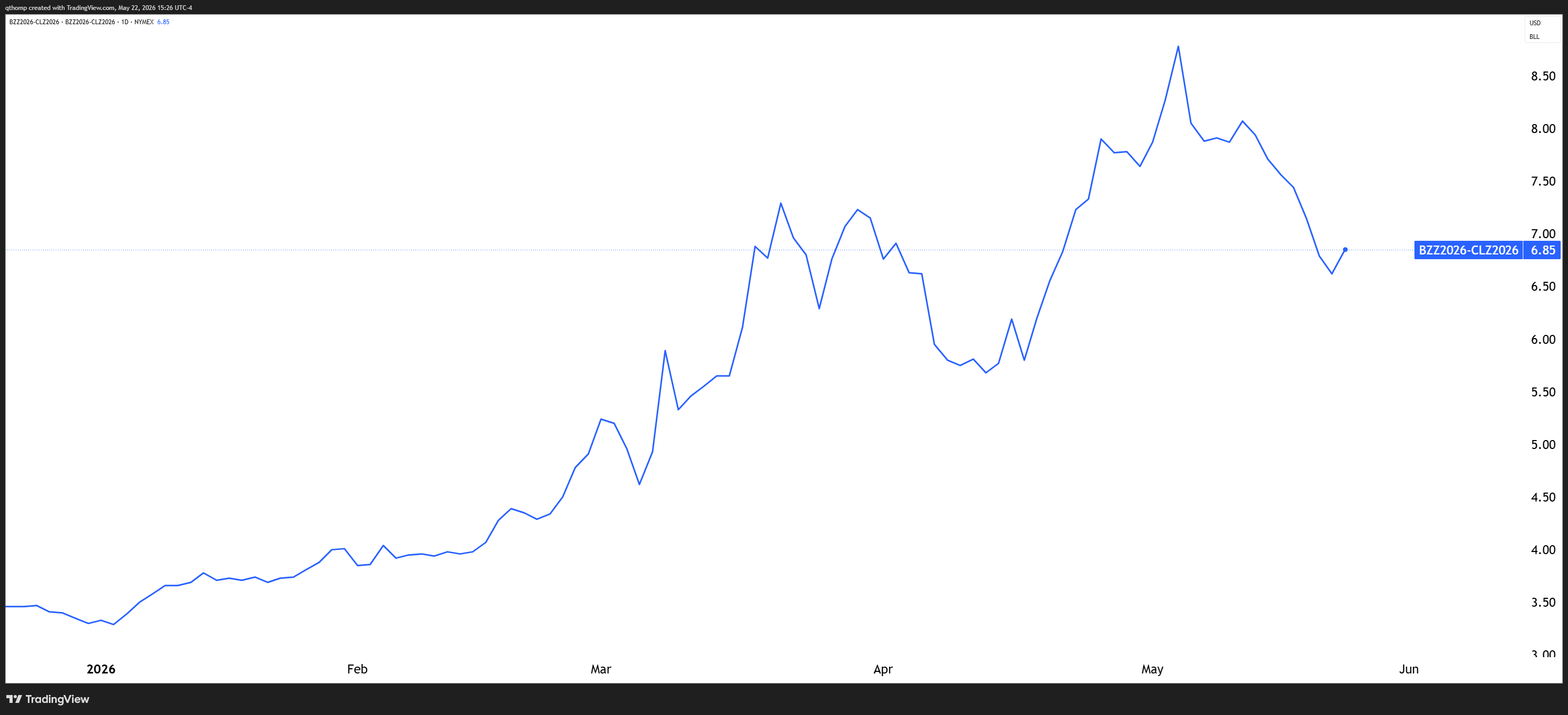

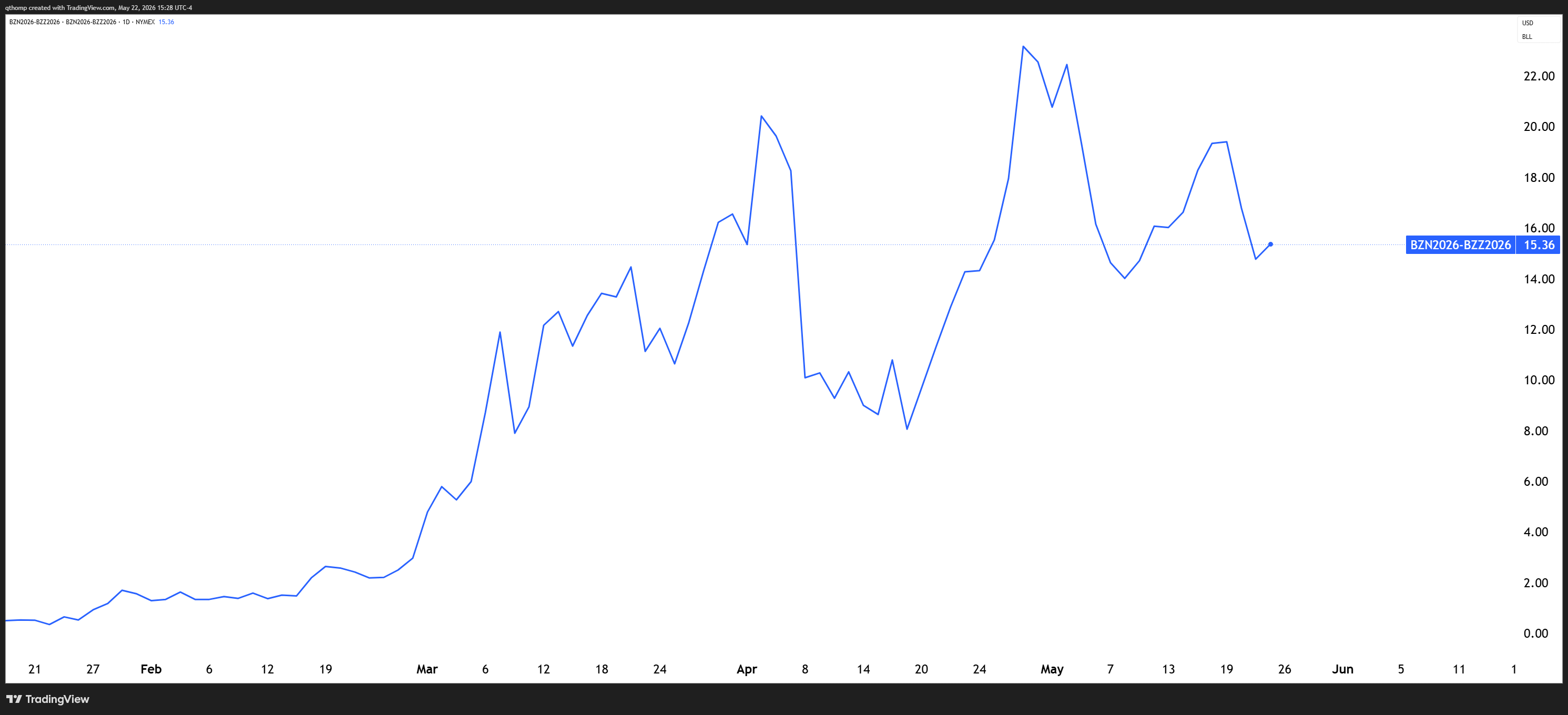

Oil market dynamics continue to chop up both bulls and bears.

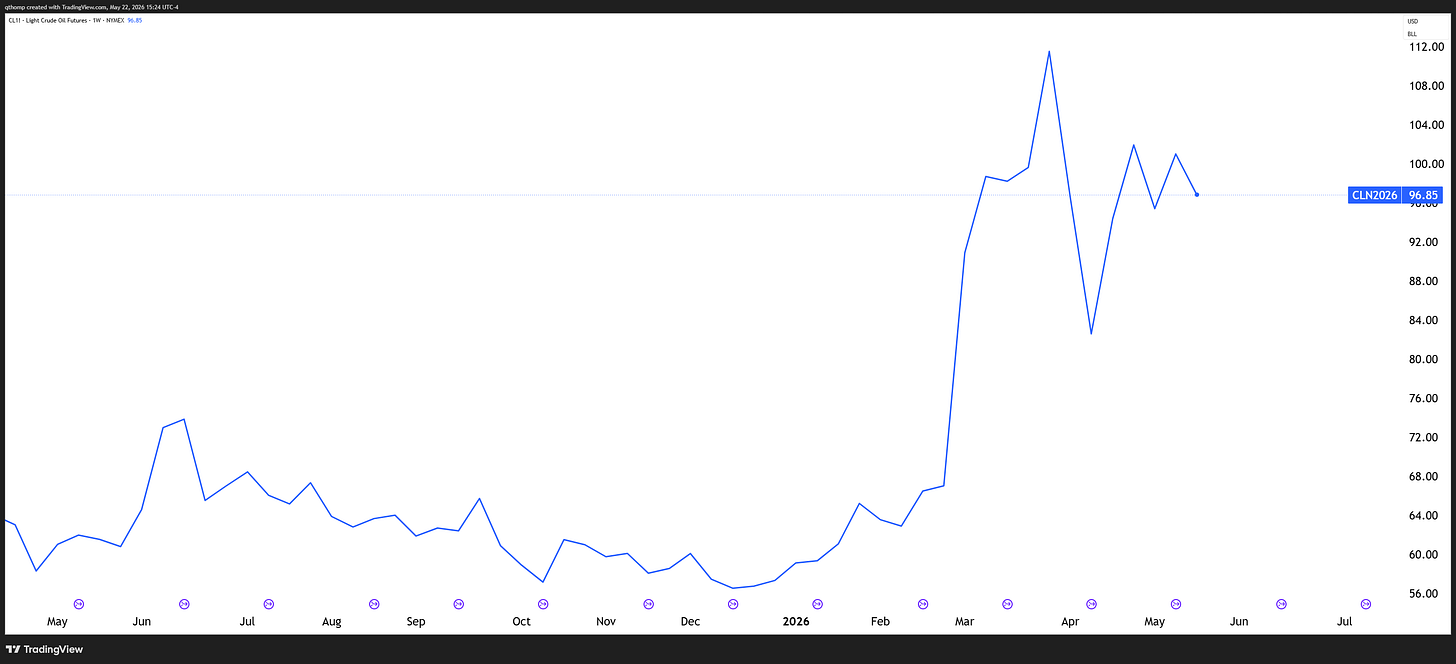

When I look at the weekly chart of WTI I just chuckle to myself. Just like the chart says, what a calm, cool and collected last 12 weeks it’s been.

Jokes aside, I continue watching Brent-WTI spreads that have come in meaningfully as the US has ramped up the exports of its crude reserves overseas to be the marginal supplier of last resort to Europe and Asia.

Time spreads have also come in for largely the same reasons as global physical shortages have been alleviated to some extent.

I’ve been writing about this stuff for the last few months and continue to believe there is attractive value in the internationally exposed parts of the oil and gas complex. Regardless of which direction the Iran War goes in the meantime, I think higher for longer oil prices are here to stay. Eventually the Strait of Hormuz will have to open up to some degree and why I think Trump is so confident in his ability to get gas prices down is because he will still keep throttling the SPR drains when that eventually happens to put as much downward pressure on crude as possible. Last time they did that though, XLE (as a proxy for oil and gas stocks) made higher lows in every consecutive year from 2021 through 2024. Equity investors will can look through the short-term flow dynamics better than the physical market can.

The markets ebb and flow. Sometimes they make perfect sense to you and no sense to your neighbor, and vice versa. It’s important to know your style and what environment you’re operating in. Flat is always a position. There will always be more opportunities and shots on goal.

I hope everyone has a great holiday weekend. If you get a chance, try a MURPH workout on Monday.

Thanks Quinn. I was genuinely surprised how well the skinhead suits you both ha ha.

Well written and clear to follow. Thanks for doing these.