Scouting the Tape - Apr 10, 2026

(Unique) macro idea generation and (insightful) market thoughts.

This week’s issue is a bit different than previous. Since I took a little break from posting I thought it could be useful to provide a lay of the land as I see things. As I have previously mentioned, I want to keep this a quality over quantity type of publication so sometimes when there’s less to say it’s best to recharge the batteries. You can also always find my latest thoughts on our weekly Forward Guidance podcast. Check out our latest below.

Dissecting The Taco

The timing of Trump’s Tuesday night announcement outside of regular market hours during low liquidity was deliberate to exacerbate the short squeeze

Trump’s high risk tolerance has been demonstrated again, as well as his ability to influence markets in the short-term

This is likely to once again boost his confidence

Despite this being a mixed bag outcome at best, loss at worst

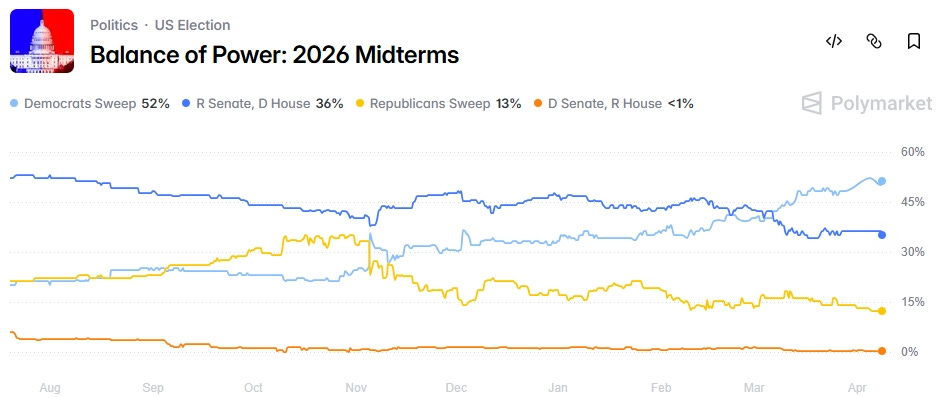

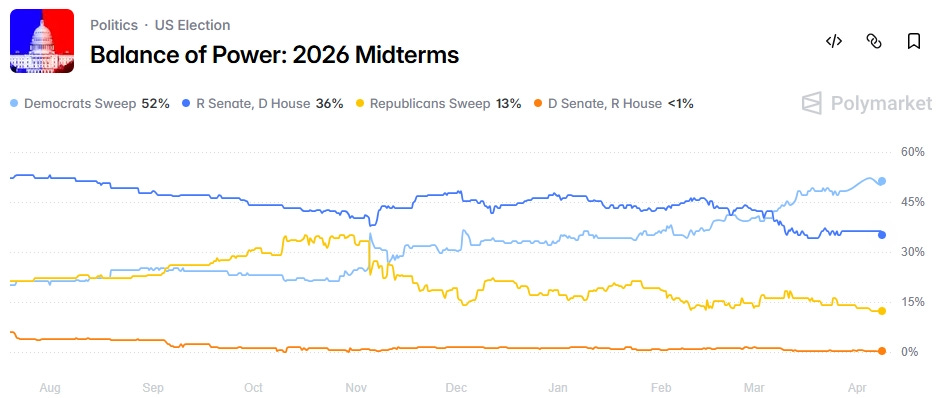

Midterm odds, polls & approval ratings likely drove this pivot more than markets

That could give clues as to how he prioritizes markets later in the year

The market can start to get back to caring about the macro more broadly versus just war headlines - the problem is it isn’t a pretty picture

Expect a better buying opportunity over the coming weeks

Oddly similar setup to 2025 with April risk off into May China meeting

Lots of opportunity out there

Focus on assets with strongest views

Take notes of material observations in aftermath of the taco, both strength and weakness

Stay nimble, emotionally balanced and unattached

Macro Outlook and Actionable Expressions

Labor market is weakening and will weigh (albeit slowly) on consumer. Consumption remains stable as savings rates are falling and households are increasingly utilizing wealth to maintain rate of expenditures. This is an unstable equilibrium however. The likely path is a continued deterioration of the job market as unevenly restrictive monetary policy constricts main street and small businesses, inflationary ripple of the oil shock creates demand destruction and AI advancements continue to eat into white collar workforce. All that said, more rapid job losses and concerns over the labor market may not surface until the second half of the year.

This implies a continued headwind on the credit markets and that you should be looking to sell credit risk, not buy it. Financials are a very interesting short category here particularly given no real bodies or contagion have surfaced from the private credit implosion. Likely some money to be made here.

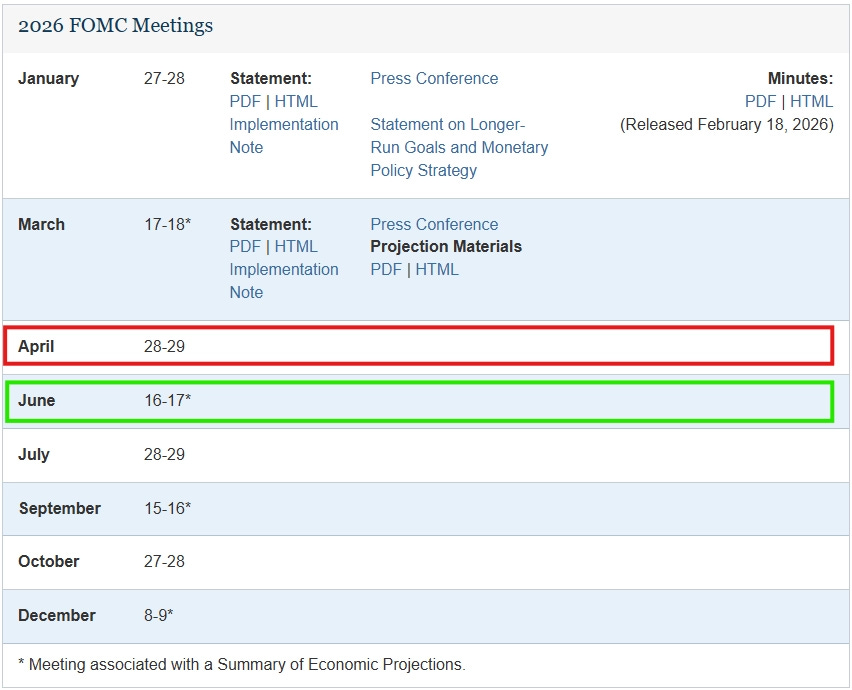

No one should be surprised if we do end up getting 1-2 cuts without a big market dump given the midterm election year under a Trump strong armed FOMC. However, even if that were to occur, there will be no visibility into it ahead of Warsh’s first FOMC meeting mid-June. This leaves a window of vulnerability, at least, leading into that, and very possibly beyond it given the risk that Warsh will not want to lose credibility and immediately cater to Trump’s demands.

The liquidity picture is weak as the inflation outlook has materially worsened. The Fed is doing ~$40B/month RMP (aka ~$500B/year of QE) which helps bolster front end liquidity but this is set to decline after tax day as per recent FOMC minutes. The continued heavy Treasury supply as a result of the fiscal deficit problem and Fed balance sheet duration tightening keeps a floor under long-term yields.

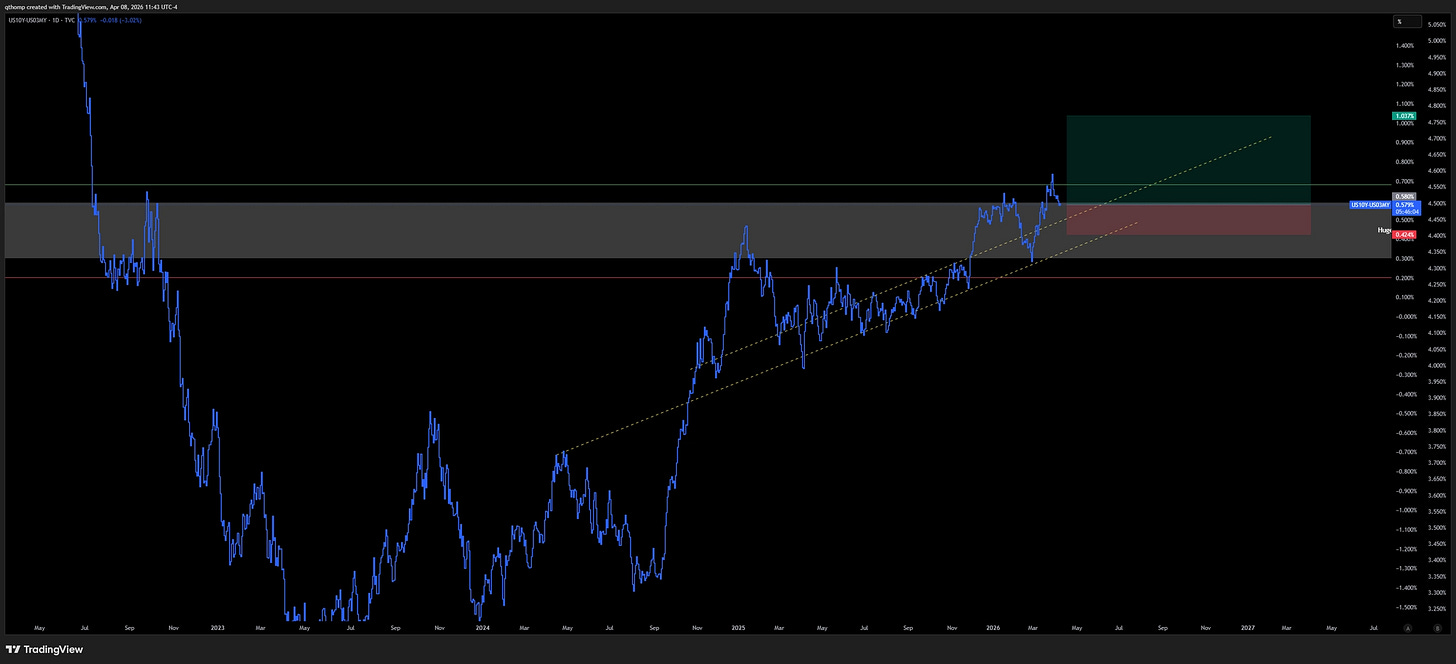

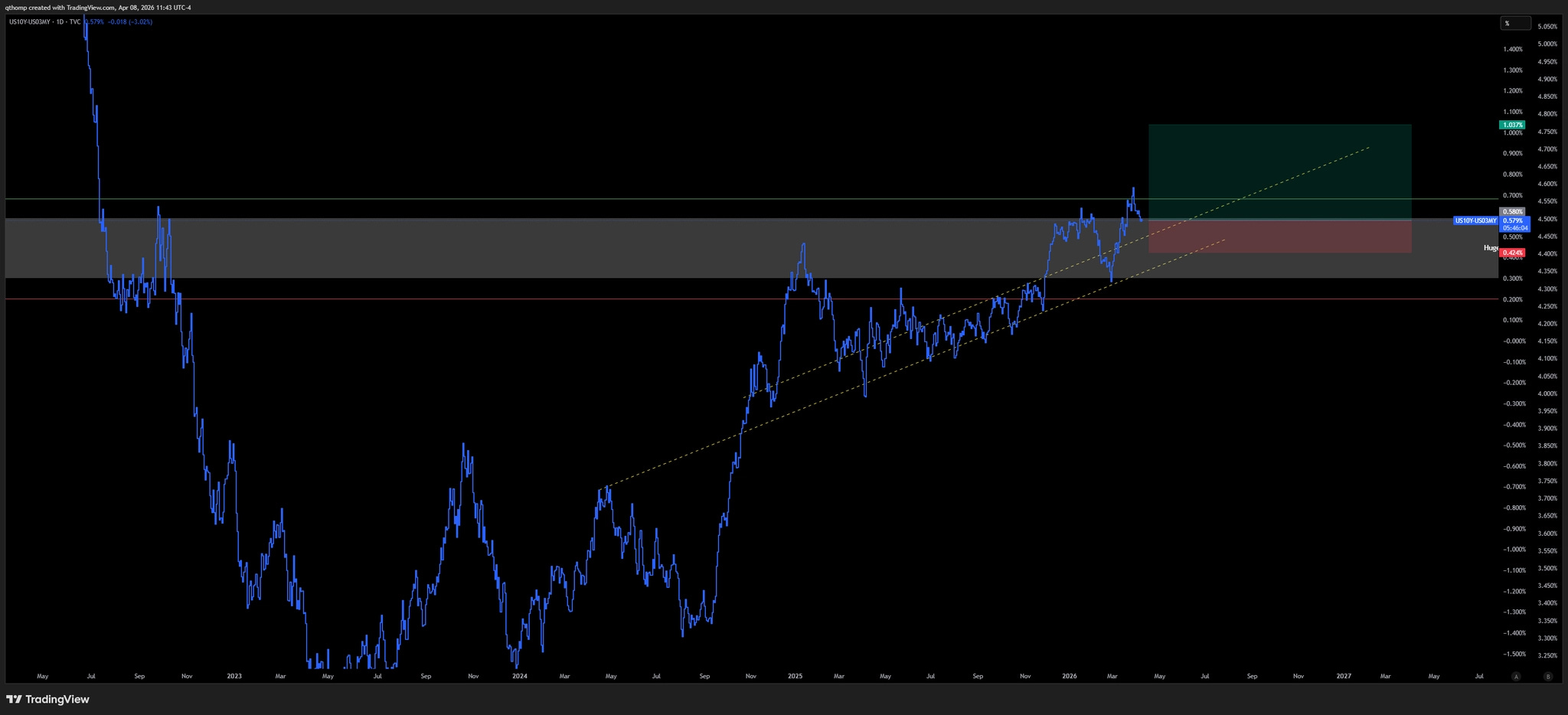

The steepener trade is approaching attractive entries. We see the current 10y-3m yield curve as a long that risks 15 bps to make 45 bps. We will be watching this closely over the coming weeks for buying opportunities via long SOFR futures and short bond futures.

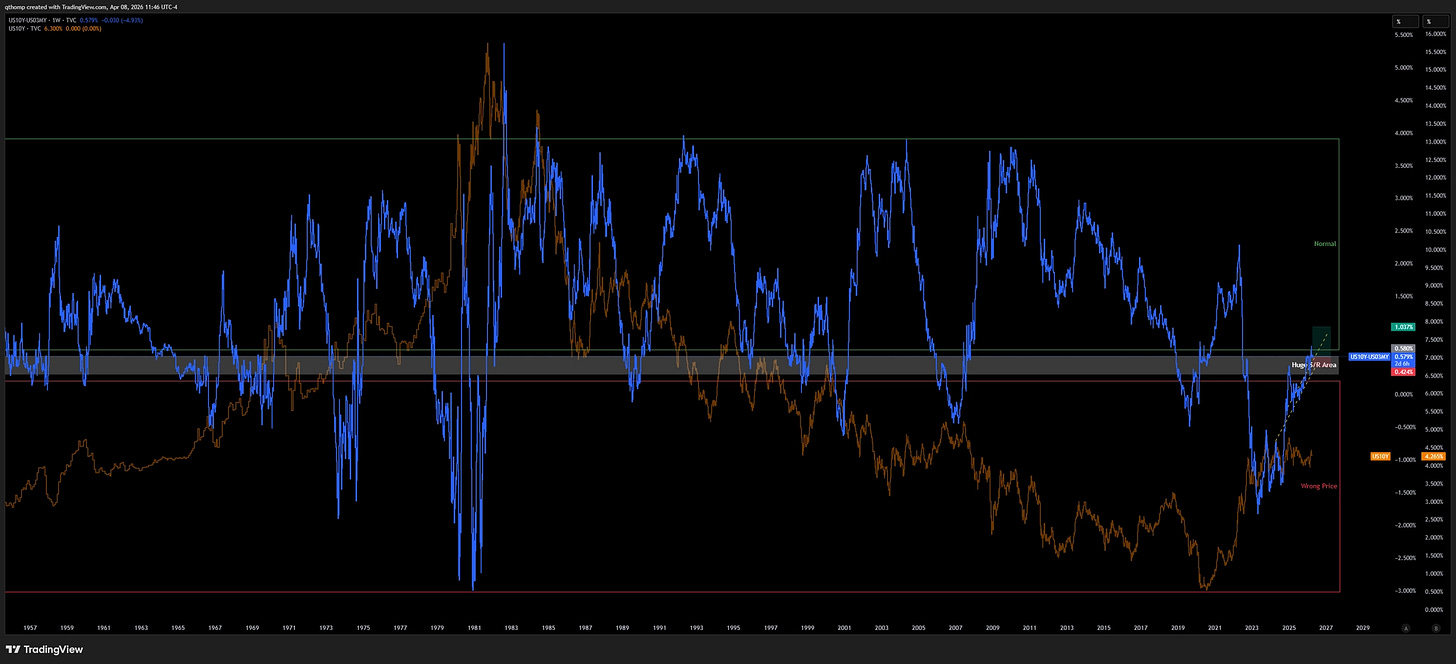

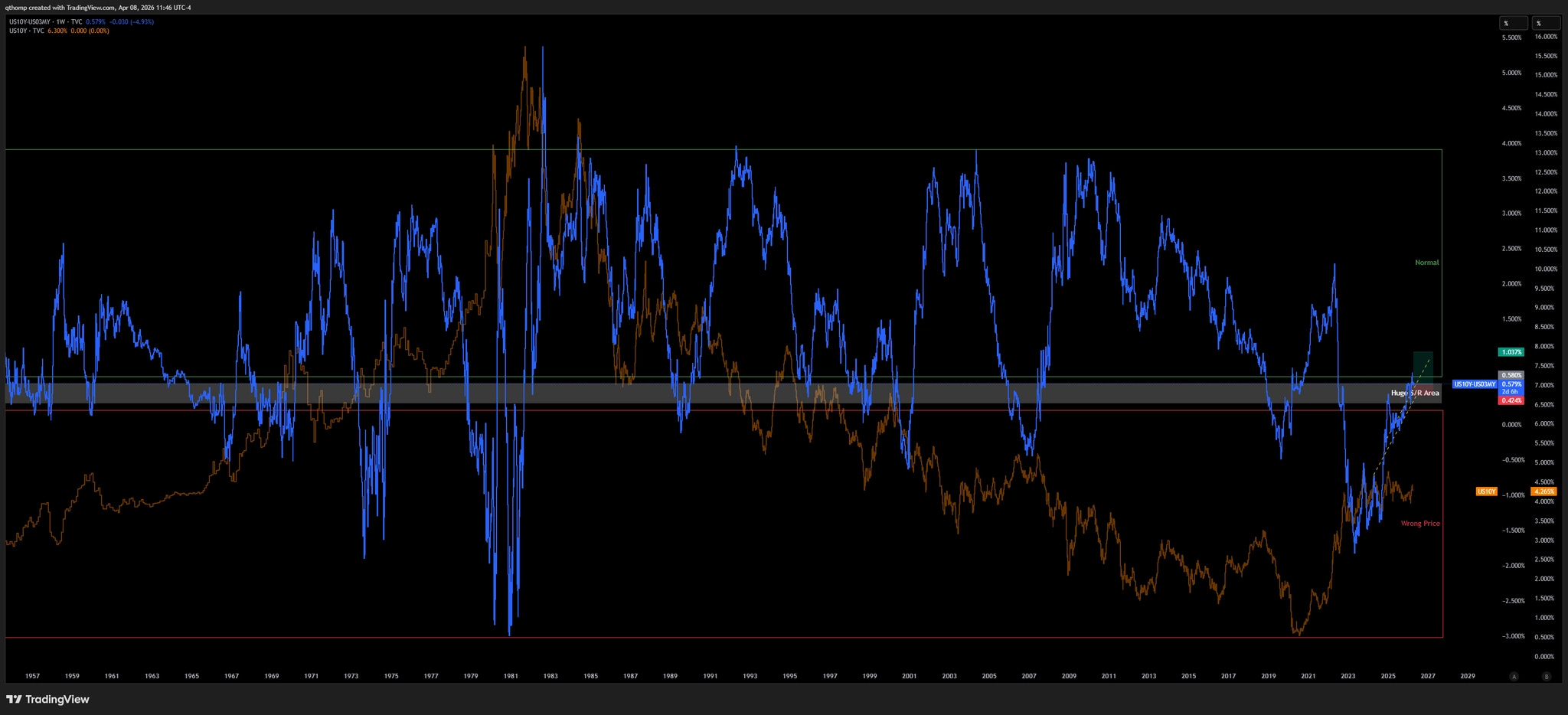

What many see as “cycle highs” in yield curve steepness that could mean revert lower, we see as going back to a normally sloped yield curve. See the same chart below, zoomed out.

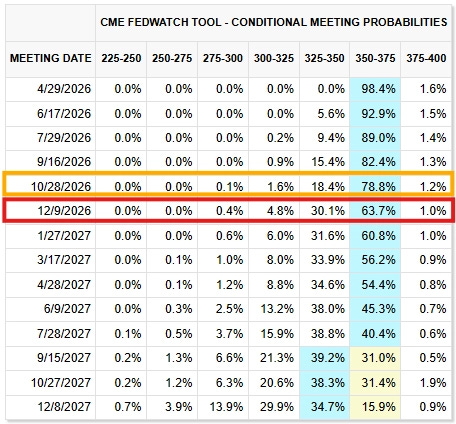

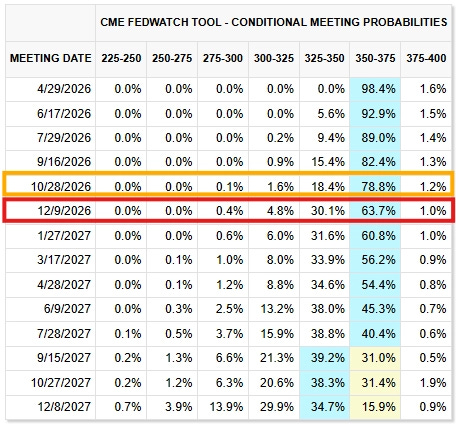

Fed Fund futures are trading in a tight range given heightened uncertainty as they await Warsh’s nomination approval, Powell’s next steps and Iran War resolutions.

~35% chance of at least 1 rate cut by December 9 FOMC

Like to focus on October 28 FOMC as that is the date where peak rate cut pressure culminates ahead of midterms. The current market pricing of a 20% chance of at least one cut by then actually seems fairly reasonable. More than one cut will require more material equity market weakness. It’s also important to keep in mind the risk that (albeit small) policymaker intervention is focused on the back end and continues to handcuff the Fed.

Given the upcoming inflation outlook is likely to be ugly, there is a reasonable case to be made that we see better entries on SOFR futures. Z6 entries below 96.35 create a strong asymmetric upside opportunity with little downside given hikes are extremely unlikely.

The optimal entries should come when equities are still trading well but inflation is surprising to the upside.

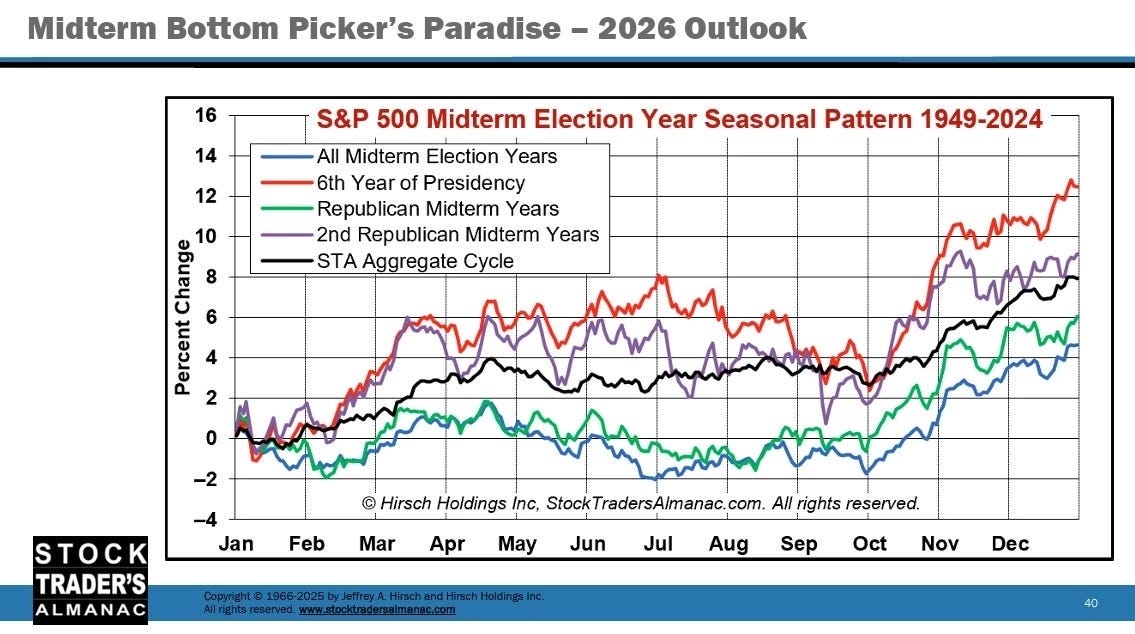

Tuesday, November 3 (US midterm elections) should serve as your event horizon north star.

The stakes couldn’t be higher and the direction of travel remains highly unfavorable for incumbents. This REQUIRES action.

What action exactly? Look to a combination of 1) historical incumbent policymaker approaches and 2) current direction of populist and societal winds. The simplest of these appear in the form of fiscal stimulus and handouts targeted at the middle class that juice the economy and “solve the affordability crisis”.

Because of this backdrop and expected behavioral patterns, there should be a prioritization given to 1) goods and services inflation protection, 2) monetary debasement and 3) fading the likelihood of a nominal recession. From an investment perspective, this looks like 1) industrial and operational commodities like metals and energy, 2) gold and 3) entering cyclically sensitive trades at attractive entries. The latter goes against the first point on a weakening labor market. Given this, in addition to historically elevated valuation multiples and credit market concerns, more care needs to be taken when expressing this view in the equity market.

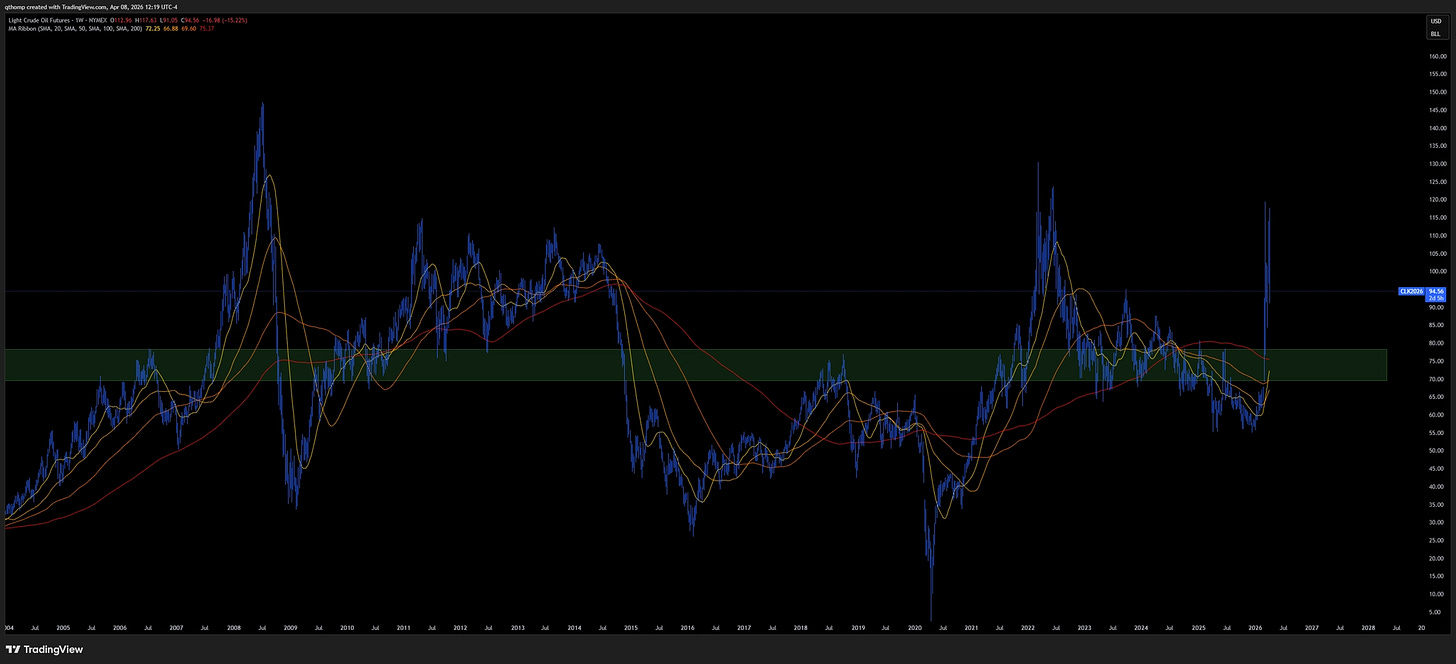

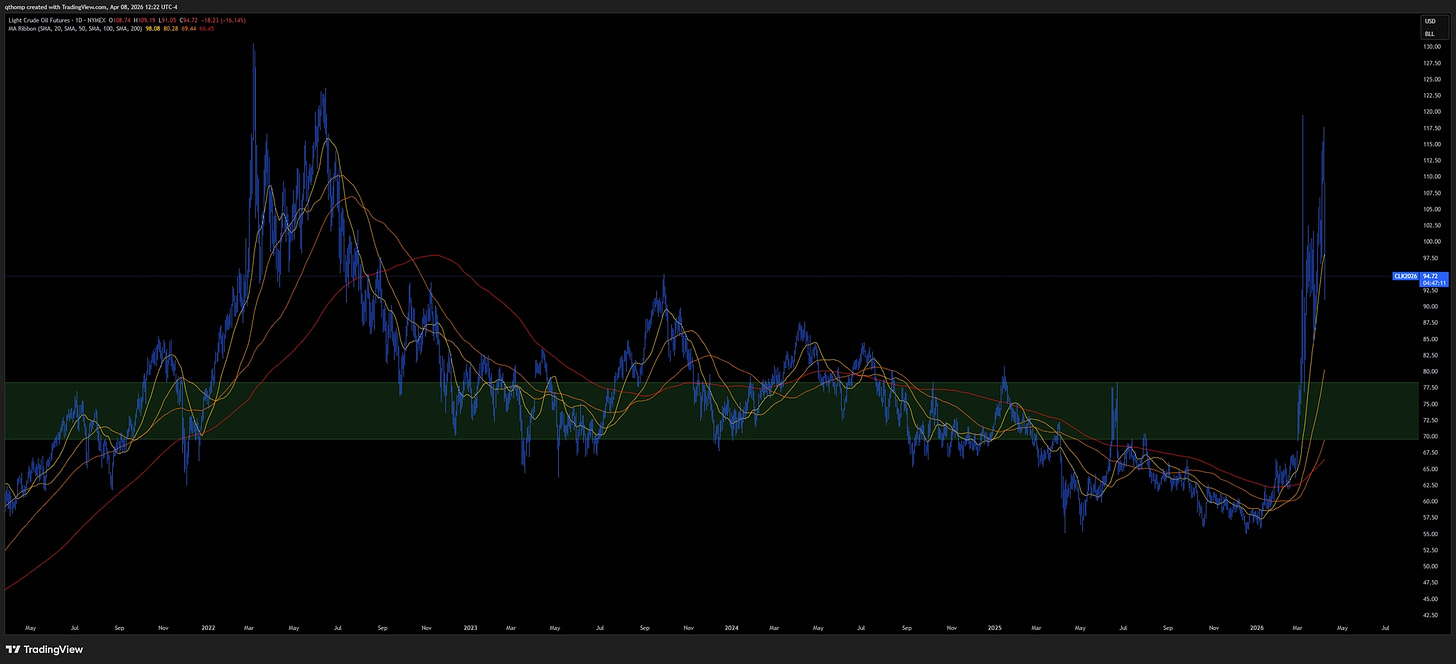

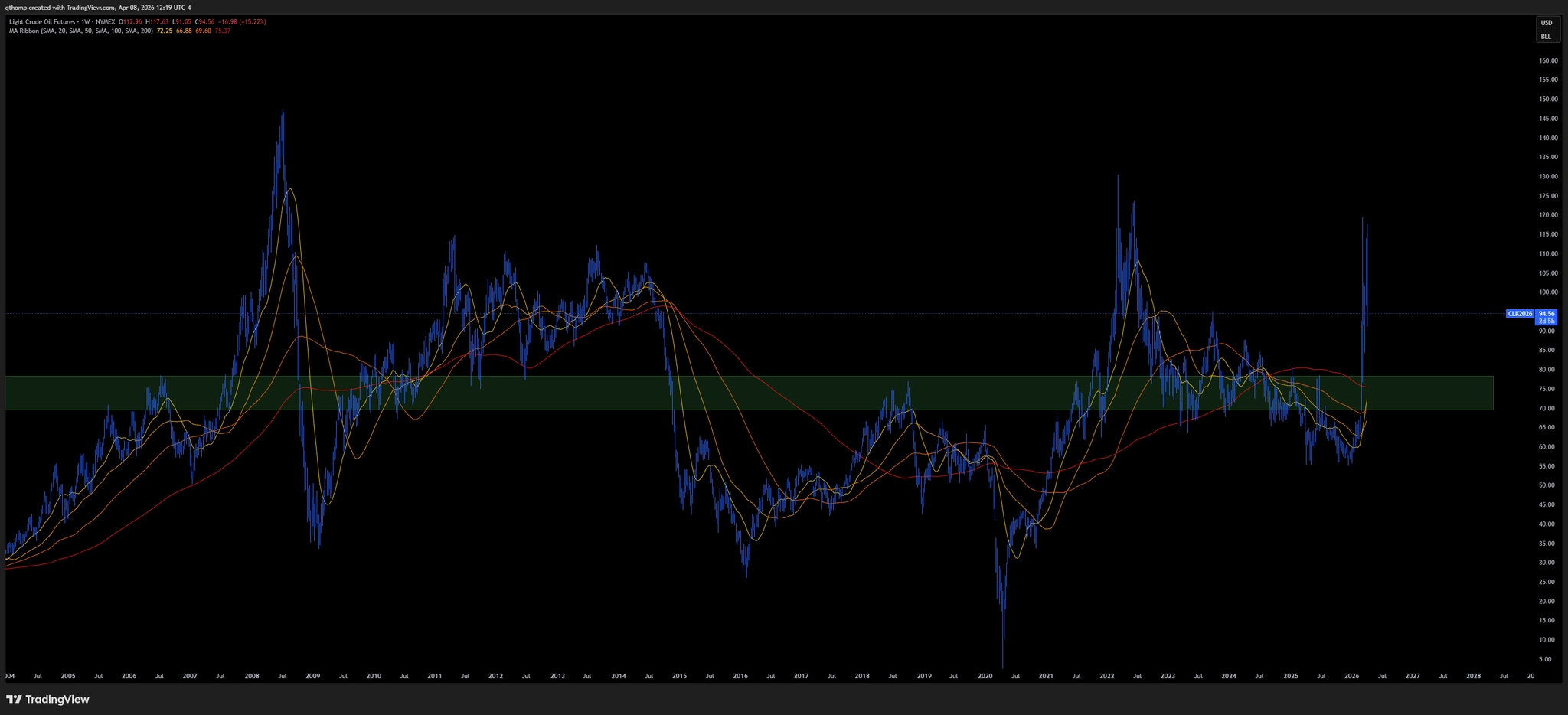

The Iran War couldn’t be more complex, but the simplicity as to what to do about it from an investment perspective is screaming at me.

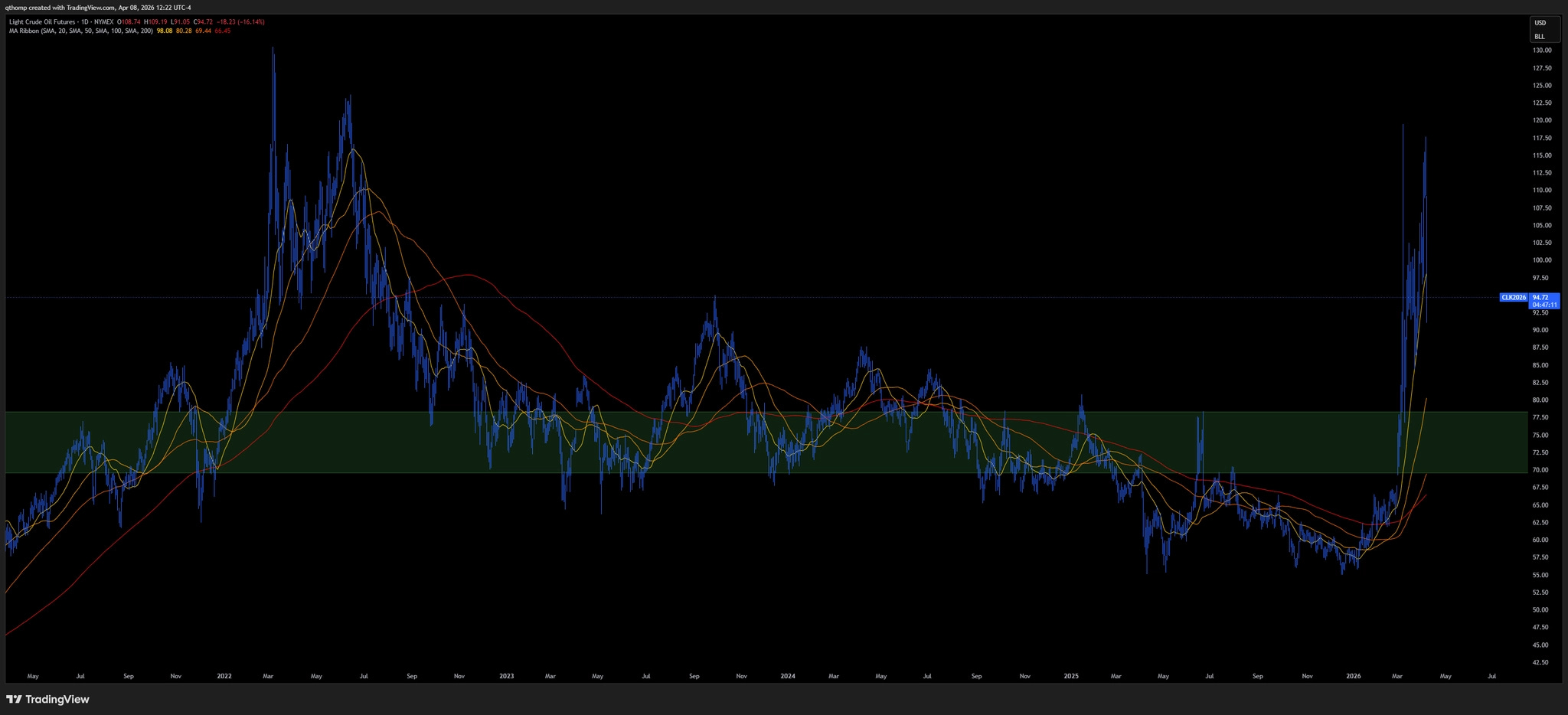

If I knew nothing about oil and simply looked at this chart, I’d be $75 bid all day long if price came back down to retest the breakout level which aligns with a 20 year support/resistance area while the moving averages all are curling up to catch it.

On a shorter-term daily chart, buying $75 looks like a fantastic way to risk $5 down to $70 to make $25 on a return to $100. I’m taking that bet every day of the week.

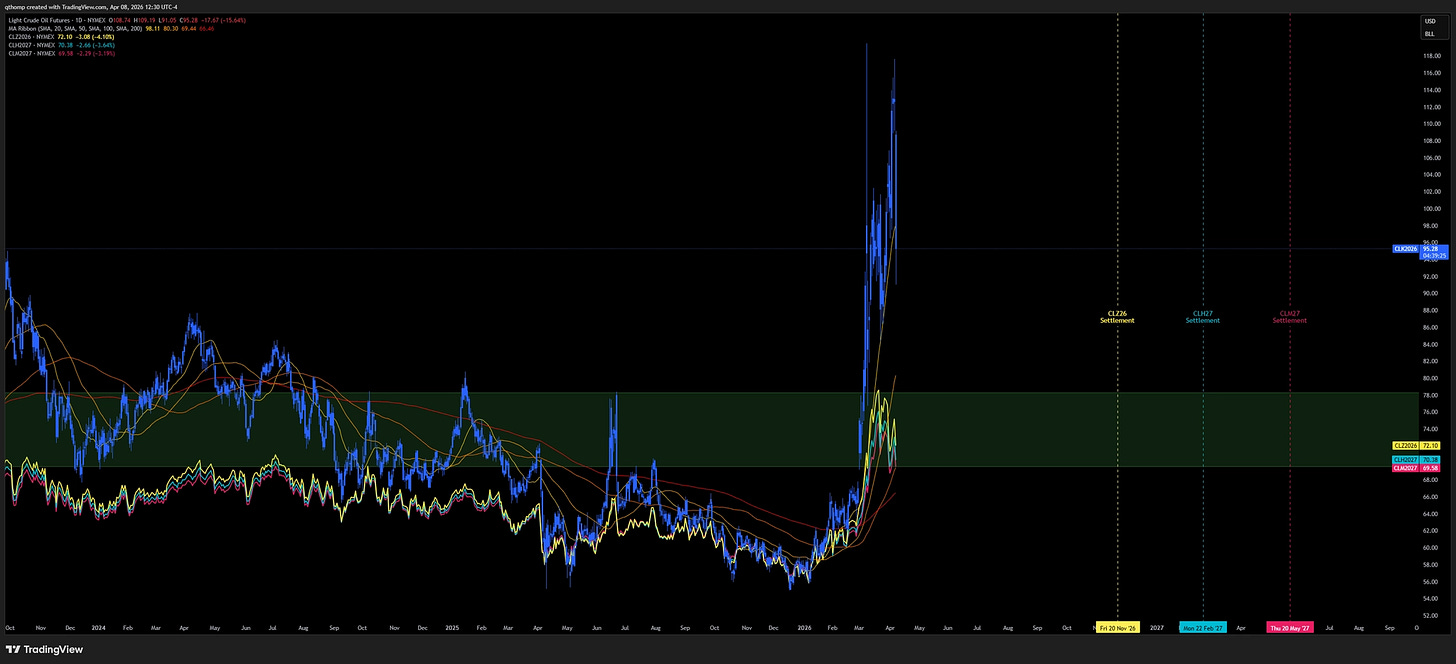

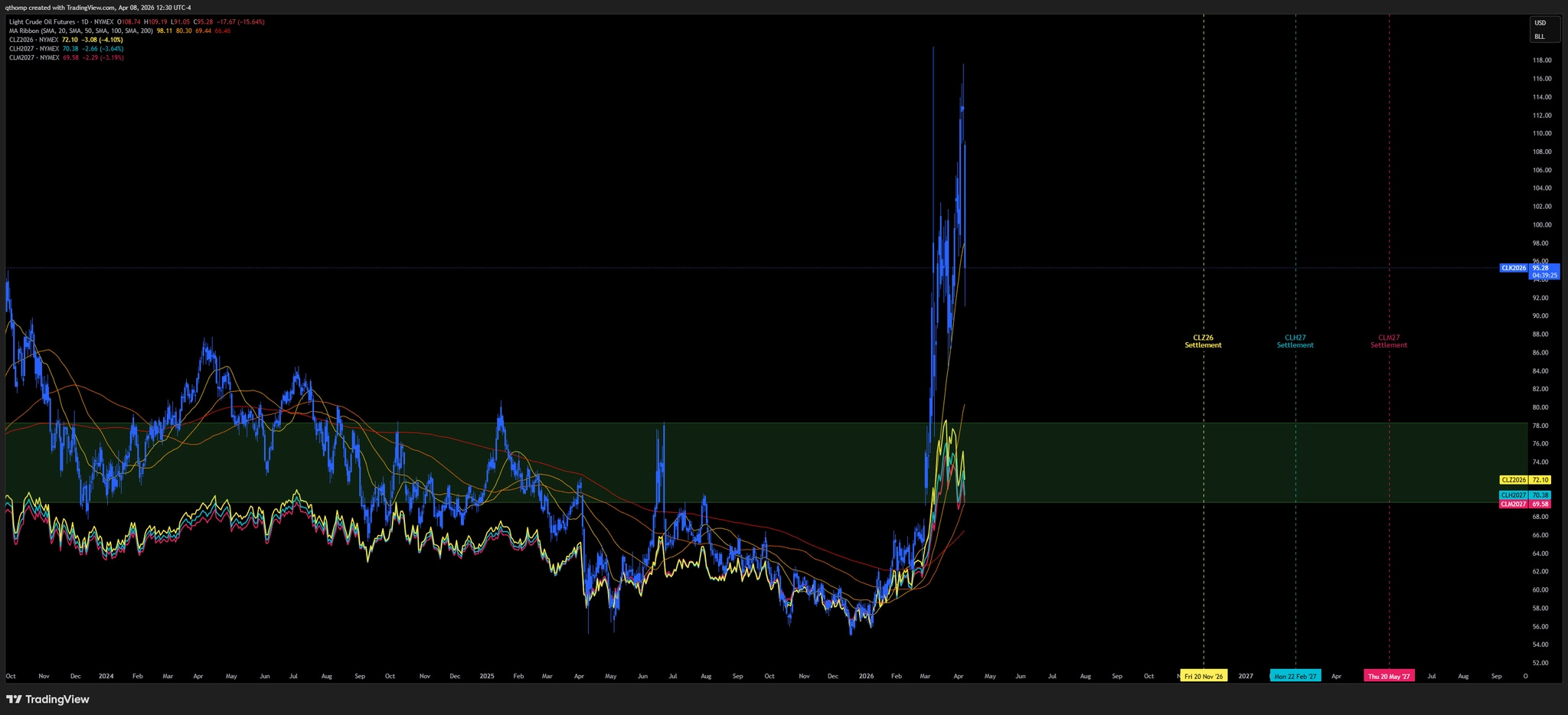

And now what if I said that you can actually take this trade today with a December 2026, March or June 2027 expiry with $72, $70 and $69 entries, respectively.

Why this makes sense?

Multi-month to multi-year demand destruction across Middle East from Iran

Perpetual Strait of Hormuz tolling at worst, 6-12 month stop/start environment until lasting resolution at best

Global policymaker response of relief , price caps, and strategic reserve drainage helps the trade by lowering near-term oil prices, supporting the economy and future demand while requiring reserves to be refilled in the future

Structural increase to scarcity premium applied to critical resources

Free call option on direct reheating of geopolitical tensions

US crude oil rig count remains negative YTD as severe backwardation has not been enough to stimulate production increases

What brings down the AI trade?

It’s likely we are either fully or partially in an AI productivity boom and it is a national security, technological innovation and strategic priority from the administration to try to maintain that. This secular tailwind has made Mag7, semiconductors and AI adjacent trades a safe haven for investors over the last 3 years. In a world that many might view as ‘increasingly going to shit’, this flight to safety may persist into early summer.

There is likely to be a point in time over the next 3-9 months where job losses (AI related or not) are causing enough problems in the economy whereby policy reaction function may reverse from recent historical precedent of supporting AI expansion at all costs. This timing also aligns with when broader macro conditions no longer work in the favor of the AI trade and fiscal and monetary policy response is also likely to be more supportive of other sectors and asset classes. This less favorable environment looks like a steeper yield curve and policy responses to help main street and small businesses over large corporations.

Said another way, there’s a world where the advancements of AI sew the seeds of its (share price) declines. This should come as a surprise to no one because 1) semiconductors are one of history’s most cyclical industries and 2) that’s how cycles work. Demand brings supply, profits bring competition, and together increased supply and competition increase input costs and reduce margins, negatively affecting forward revenue growth and earnings expectations and thus share prices.

The winners for the remainder of the year will sit at the intersection of multiple, high priority strategic interests

Geographic beneficiaries: Latam, Venezuela, Cuba, Greenland

Critical resource security: Industrial and scarce metals

Defense tech: Drones, space, autonomous

Power grid resilience and AI capex raw inputs: Oil and gas, uranium, power generation, related inputs

Inflation and debasement protection and anti-nominal recession: Gold, cyclicals, avoid bonds

Navigating the Near-Term

Expect a swing long opportunity for risk assets in the next 2-4 weeks - focus on winners and assets still in bull market uptrends, not bear market bounces

Trump-Xi meeting May 14-15 likely to be a ‘great success’

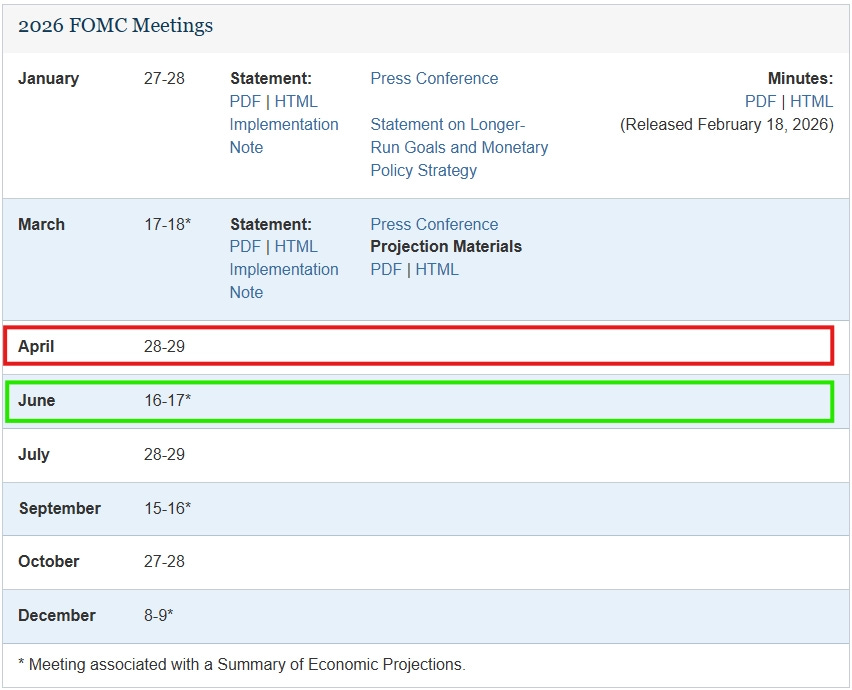

Powell’s last FOMC meeting is April 29th and Warsh’s first meeting is June 17. Are we setting up for a buy Powell’s departure and sell Warsh’s arrival?

Liquidity and growth outlook materially worsen from June to August, which aligns with historical midterm seasonality

Hope everyone has a great weekend and that it resembles this guy as much as possible.

Agricultural commodities still a buy? Corn wheat sugar?