Scouting the Tape - Mar 21, 2026

(Unique) macro idea generation and (insightful) market thoughts.

We are now 6 years post the historic March 2020 COVID meltdown and the market has become comfortably accustomed to a ‘number go up’ ‘buy the dip’ mentality. It is always at the most inopportune times that consensus sways so strongly to one side, creating a situation that somehow both everyone and no one saw coming. We are to the point where if you present a sound, research backed case as to why the outlook for risk assets is negative, you just get mocked and jeered instead of countered with facts based arguments or alternate cases.

Meanwhile, everything I look at continues to signal maximum caution over both the coming weeks and months to year. What feels so obvious to me seems so foreign and antagonistic to many. When I experience these periods of hardening conviction amongst an ever diverging sentiment and consensus, I just keep digging and re-underwriting. I try to step into ‘the shoes of an alien’ who knows nothing about the world we live in and is just seeing everything for the first time. It’s nearly impossible to eliminate all biases we carry, but attempting to put myself in an outside person’s brain to evaluate the landscape and assess the facts helps me to parse signal from noise.

Our latest Forward Guidance episode with chartbook download is linked here.

Simplifying the agriculture trade.

I remain very long agricultural commodities. I laid the thesis out in last week’s Scouting the Tape and have been discussing in chat before that. I want to offer a simple summary.

They are the biproduct of everything that is scarce right now. Within the final cost of corn, wheat and soybeans is the fuel it takes to plant, tend and harvest crops (oil and gasoline prices are vertical), the fertilizer it takes to grow crops (fertilizer prices are vertical), land, farming margins and financing costs. On top of that, US farmers have been in a severe recession with materially ramping bankruptcies and closures, setting the stage for production decreases there as well. All of this equates to higher prices for the end commodity. I think betting on the physical underlying ags is not only the simplest expression of the trade but also the highest upside with least downside.

Ags are not susceptible to the same demand destruction that oil is given you need food to live. There also is no strategic agriculture reserve.

The timing of the supply shock matters much more for ags than it does oil as well given we are entering peak spring planting season. When key commodity supplies come back online, oil can be restarted whenever, but you can’t plant crops out of season.

Lastly, remember what I wrote about the move in producers before the physical commodity. I pointed this out in both gold and oil. Linked here. A similar idea has been playing out in the ag space.

Iran thoughts and if/when the oil market becomes a forcing function?

I don’t really want to discuss the Iran war a whole lot but it’s important and necessary so I have a section about it. That said, the other topics I write about I think are more unique, interesting and unfortunately bearish. The main message is there is no near-term opening of the Strait. It is going to be a extended, ugly battle to get there. This is the stuff global crises are made of.

Trump could be playing a waiting game with developed country allies in Europe and Asia. We wrote about the US’s energy dominance last week and the record low natural gas inventory levels in Europe and Asia going into this year. The below chart provides useful context to how much of a problem this is for energy importing countries who are short commodities. Check our X feed for recent tweets about our short Japan, Korea and Europe positions.

Ole S Hansen@Ole_S_HansenCrude futures across New York, London, Dubai and Oman currently show a pronounced divergence, with WTI trading at a notable discount to benchmarks more closely linked to Asian demand. While part of this spread reflects differences in contract expiry and delivery timing, it does

Ole S Hansen@Ole_S_HansenCrude futures across New York, London, Dubai and Oman currently show a pronounced divergence, with WTI trading at a notable discount to benchmarks more closely linked to Asian demand. While part of this spread reflects differences in contract expiry and delivery timing, it does 8:28 AM · Mar 17, 2026 · 44.3K Views28 Replies · 91 Reposts · 421 Likes

8:28 AM · Mar 17, 2026 · 44.3K Views28 Replies · 91 Reposts · 421 LikesIt seems likely to me that once the market works through the large build up in floating crude stores (soon), most of which I believe is from sanctioned producers (eg Russia), the temperature on the Strait closure will turn up a notch.

Unintended Consequence@UnintendedCons5Crude on water might drop 100mmbbls this week

Unintended Consequence@UnintendedCons5Crude on water might drop 100mmbbls this week 12:13 PM · Mar 17, 2026 · 9.21K Views2 Replies · 21 Reposts · 106 Likes

12:13 PM · Mar 17, 2026 · 9.21K Views2 Replies · 21 Reposts · 106 LikesCoal switching was a big topic in 2025 and is likely to remain so in 2026.

Javier Blas@JavierBlasKeep an eye on coal, as more Asian nations turn to it to replace natural gas / fuel oil in power generation. Philippines said that it’s likely to burn more coal in the next few months. And India’s government said all was ready for “unprecedented” coal demand in 2026.

Javier Blas@JavierBlasKeep an eye on coal, as more Asian nations turn to it to replace natural gas / fuel oil in power generation. Philippines said that it’s likely to burn more coal in the next few months. And India’s government said all was ready for “unprecedented” coal demand in 2026. Javier Blas @JavierBlasSouth Korea is lifting a cap on coal-fired power generation (until now set at 80% of capacity) to offset the loss of LNG The flexibility of Asia to performan gas-to-coal switching (and its enormous coal-fired fleet) provides a layer of insulation that Europe didn't have in 20227:32 AM · Mar 17, 2026 · 105K Views26 Replies · 284 Reposts · 897 Likes

Javier Blas @JavierBlasSouth Korea is lifting a cap on coal-fired power generation (until now set at 80% of capacity) to offset the loss of LNG The flexibility of Asia to performan gas-to-coal switching (and its enormous coal-fired fleet) provides a layer of insulation that Europe didn't have in 20227:32 AM · Mar 17, 2026 · 105K Views26 Replies · 284 Reposts · 897 LikesSee our coal write up from February.

Distraction and diversion tactics from the administration are working.

Last March I was invited onto a crypto VC podcast amidst the market panic to talk macro. It was interesting to hear their perspective on what was going on because it differed a fair amount from how I was seeing the world. My main takeaway that did not resonate with them was that while tariffs were the pomp and circumstance, the equity market sell off was driven just as much if not more by other policy items like deficit spending cuts and immigration reduction that would put downward pressures on growth. That notion got laughed at but fast forward through 2025 and the tariffs remained but what didn’t was the firing of Elon, ending of DOGE and reversal in their 3% stated fiscal deficit target back to 5-6% deficits, all helping to recover the equity market.

The Chopping Block@_choppingblock🚨 Emergency Macro Episode! 🚨 We called in the big guns—@qthomp—because when the macro shifts, you need the real insights. No fluff. No filter. Just straight talk. Watch now. ⬇️ Timestamps 00:00 Intro 02:04 Trump's Strategic Bitcoin Reserve 04:42 Market Reactions & Opinions2:54 AM · Mar 12, 2025 · 51.3K Views13 Replies · 13 Reposts · 114 Likes

The Chopping Block@_choppingblock🚨 Emergency Macro Episode! 🚨 We called in the big guns—@qthomp—because when the macro shifts, you need the real insights. No fluff. No filter. Just straight talk. Watch now. ⬇️ Timestamps 00:00 Intro 02:04 Trump's Strategic Bitcoin Reserve 04:42 Market Reactions & Opinions2:54 AM · Mar 12, 2025 · 51.3K Views13 Replies · 13 Reposts · 114 LikesToday I see something very similar. The writing has been on the wall as the toolshed has largely been emptied. The Fed has used most of its rate cuts, liquidity facilities like the RRP are depleted and the positive fiscal impulse from OBBB is moving into the rearview amidst an already fragile and deteriorating labor market. With equity markets at all-time highs and record valuations, this is a bad setup that is unlikely to end well. So what do you do? Insert classic diversion and distraction tactic ahead of midterm elections. Now with the Iran War there is something for the administration to blame for the poor market performance and they have finally gotten the US population to stop talking about the Epstein files. When the War eventually ends, there will be a bounce in risk assets, maybe even a Fed cut or two, and everyone will think things are back to normal for risk assets. Maybe this will even all be timed to occur right before November. Generally speaking however, the problems at hand facing the equity market are more structural and heavy in nature today than around Liberation Day last year.

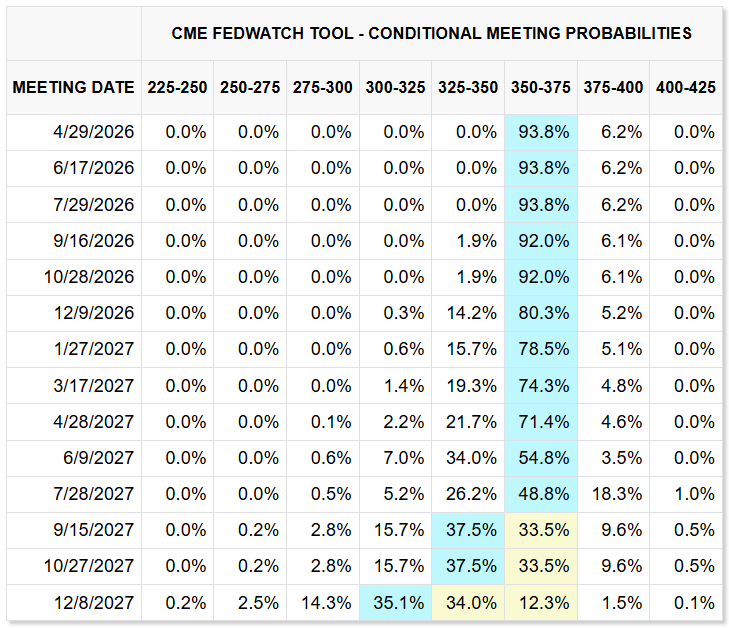

What gets the Fed to cut?

There is a lot of noise and uncertainty around the Fed’s policy path. This is unlikely to resolve anytime soon given the ongoing major commodity supply shock and transition of new Fed leadership in a few months. That said, I found it helpful to try to arrive at what I think would get the Fed to act.

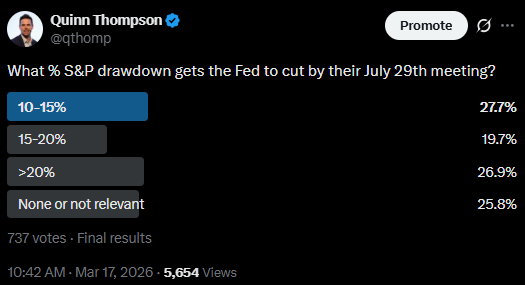

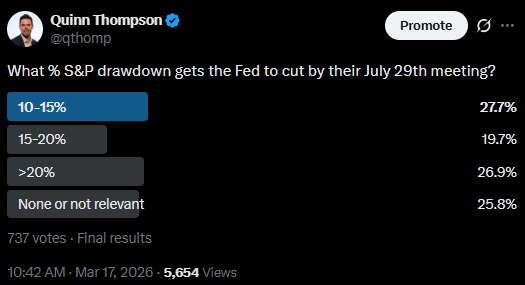

Probably the most straightforward catalyst would be a ~20% equity market correction as that has negative reflexivity that spillover to consumers via wealth effect and corporate investment/hiring.

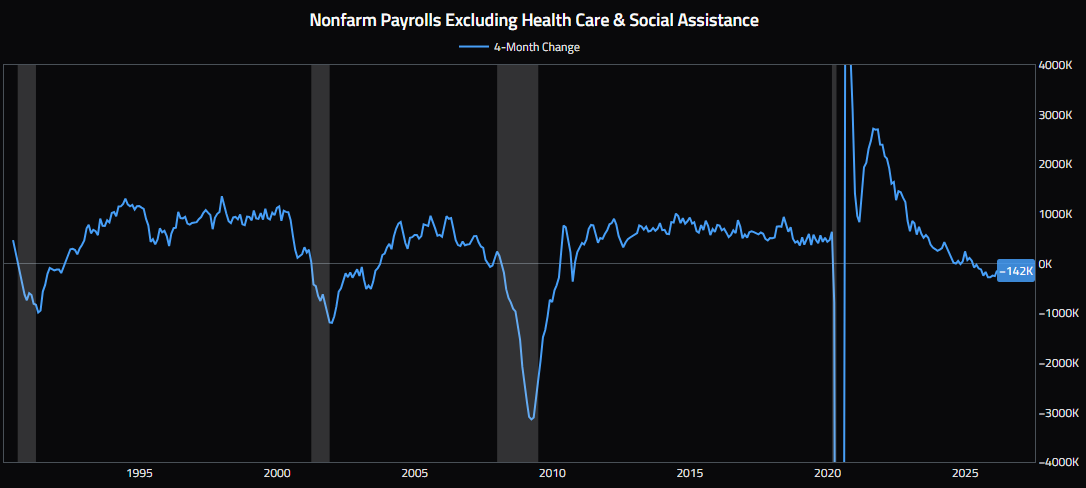

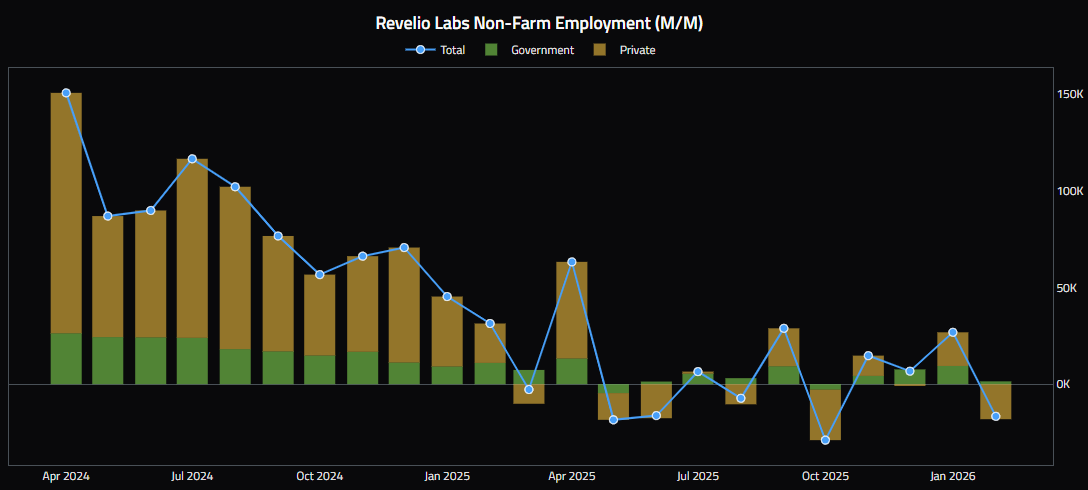

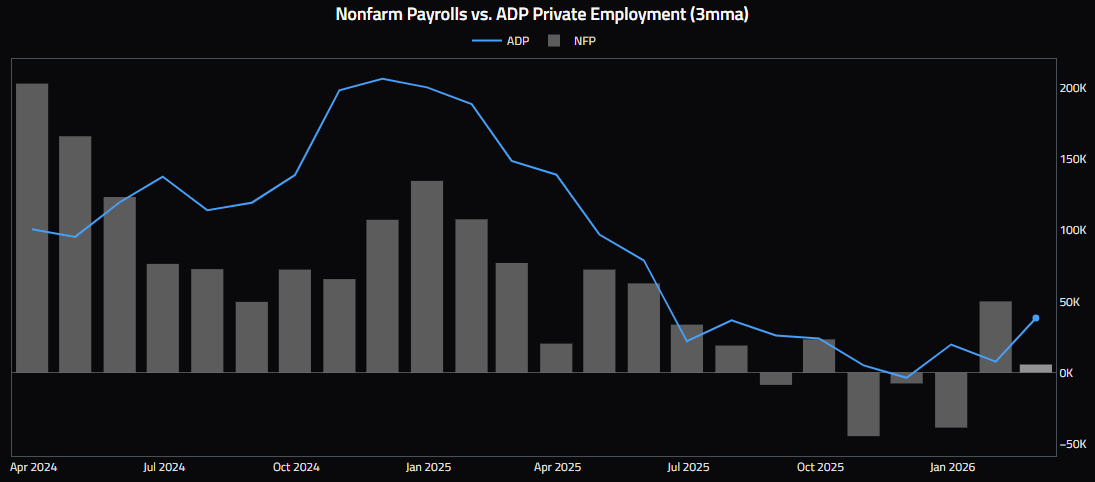

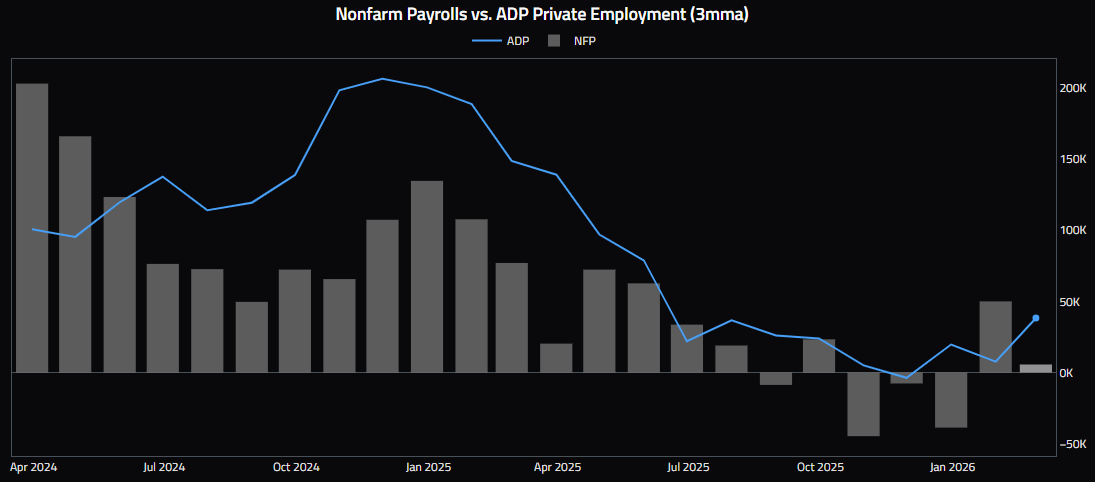

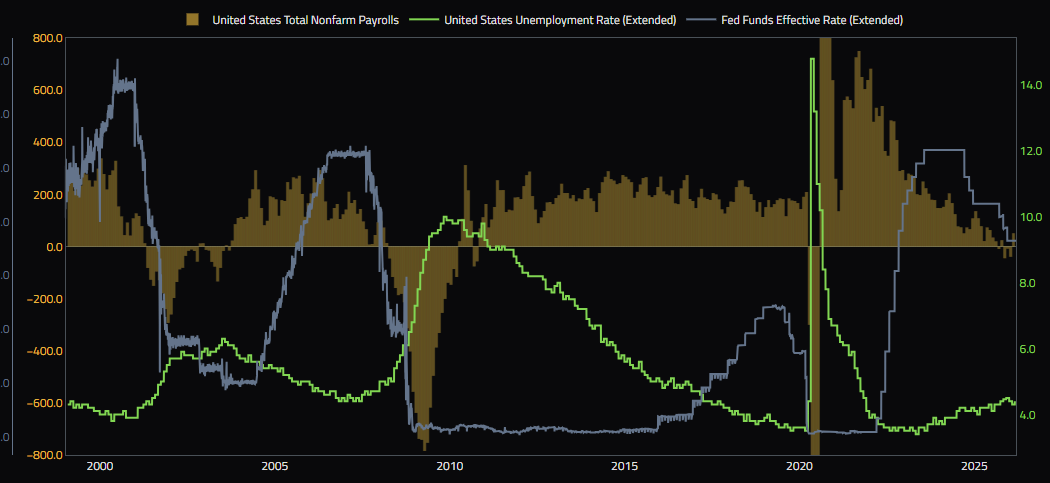

Outside of that, I believe the labor market is the next catalyst. The labor market has been very weak for over 2 years now. New job growth excluding healthcare has been flat or worse since early 2024 and negative since April 2025.

This weakness can also be seen in alternative data measures like Revelio and ADP.

If I were to guess what gets the Fed to cut, I don’t think one more negative print is enough, but two or three materially negative reports might get them to act. Meeting cadence here matters as well given there will only be one more NFP print before April’s meeting and then by June’s meeting we will have new Fed leadership and NFP reports for March, April and May. It’s possible that going into the June meeting that four of the last six months are showing negative job growth. It would be pretty clear at this point that the Fed would be late to supporting growth even if they did decide to cut in June which the market views as highly unlikely at this stage.

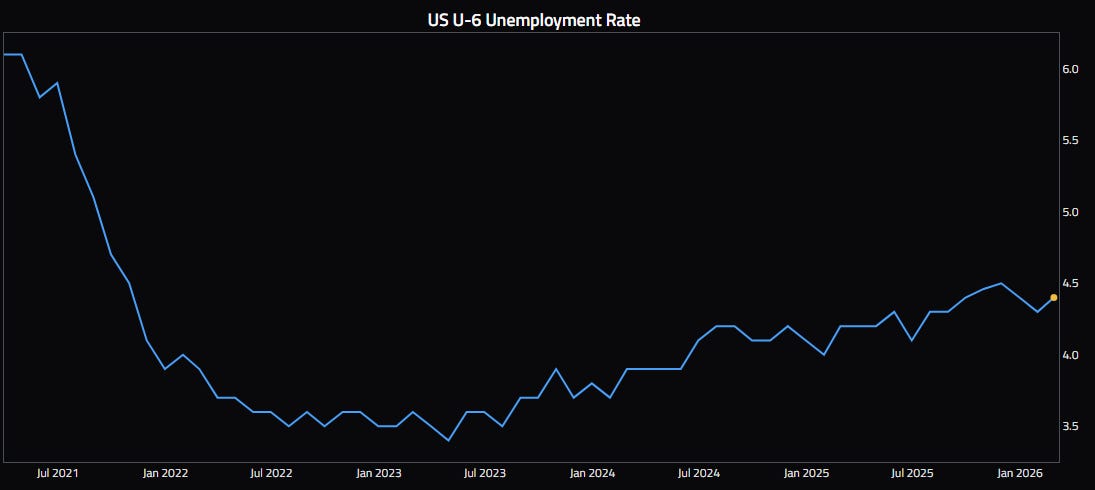

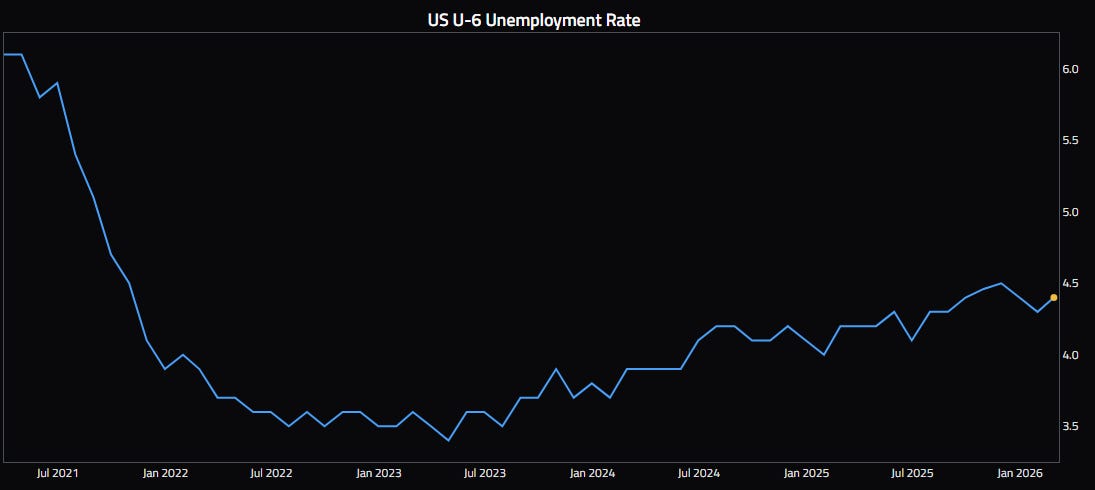

An uptick in unemployment rate towards 5% over the coming months would help the case. However recent increases there have been slow given the ‘no hire no fire’ stagnant environment.

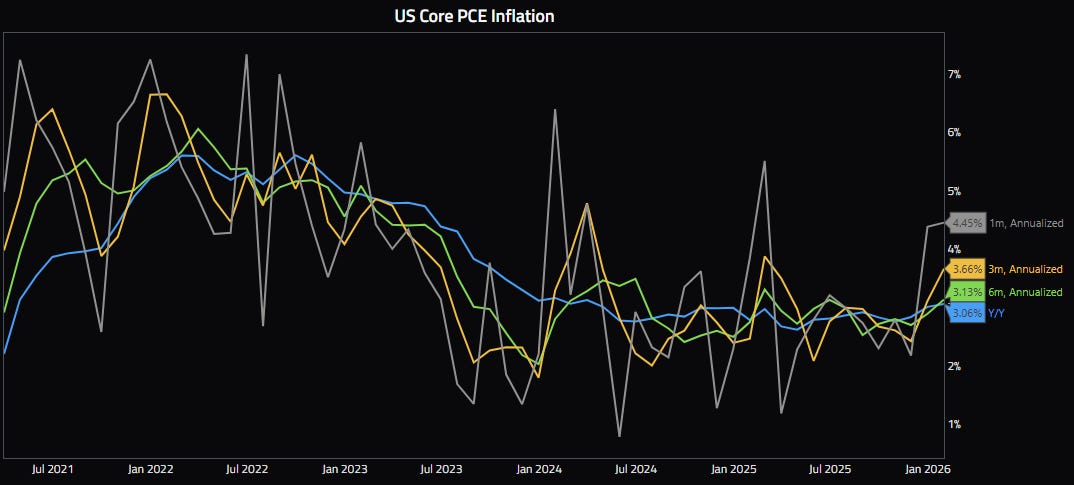

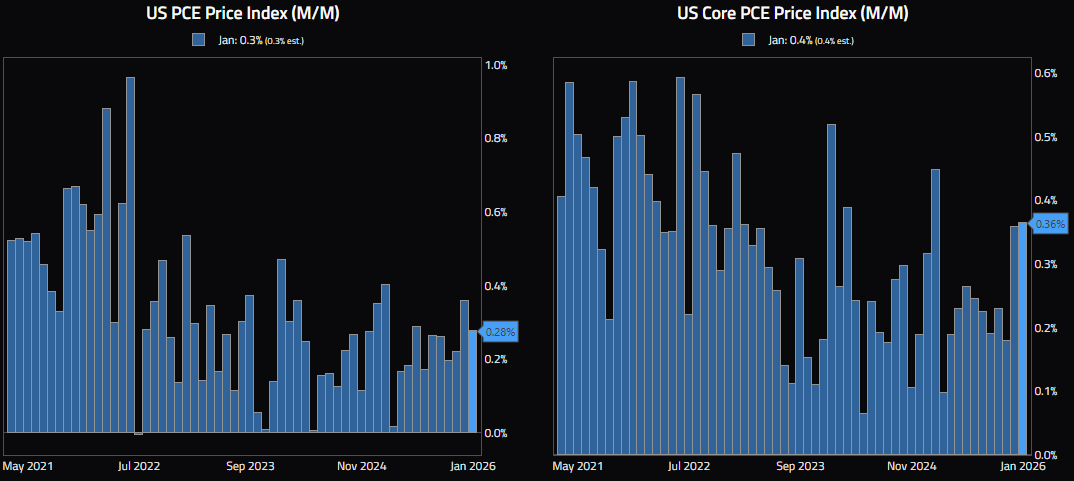

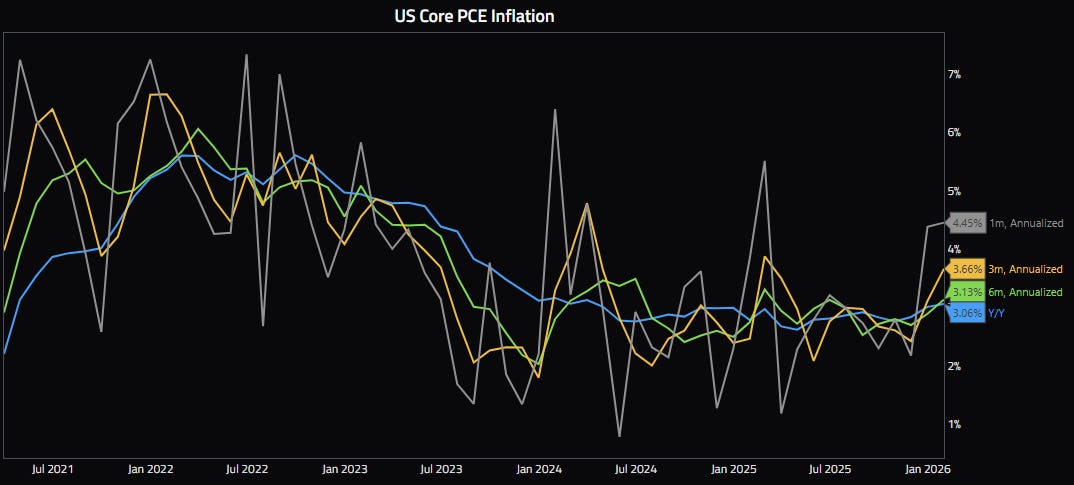

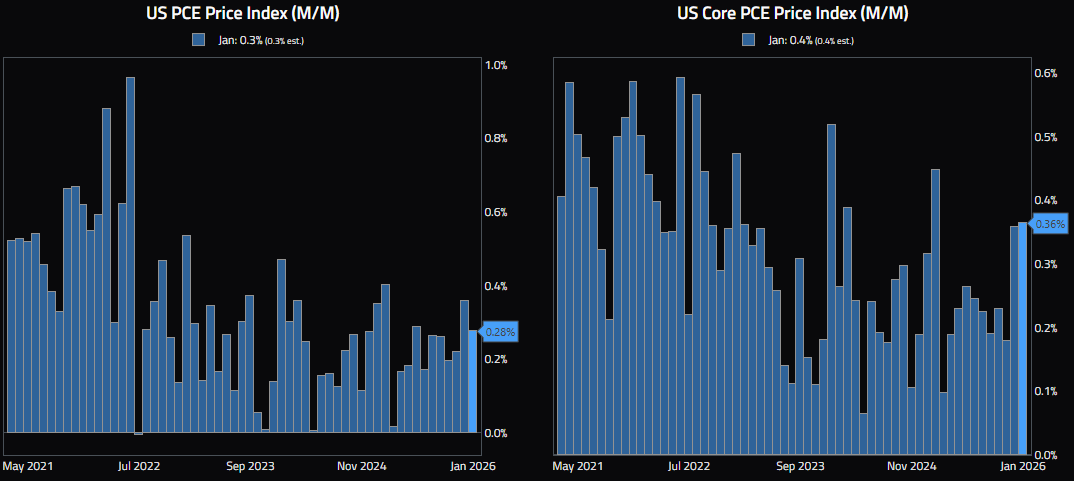

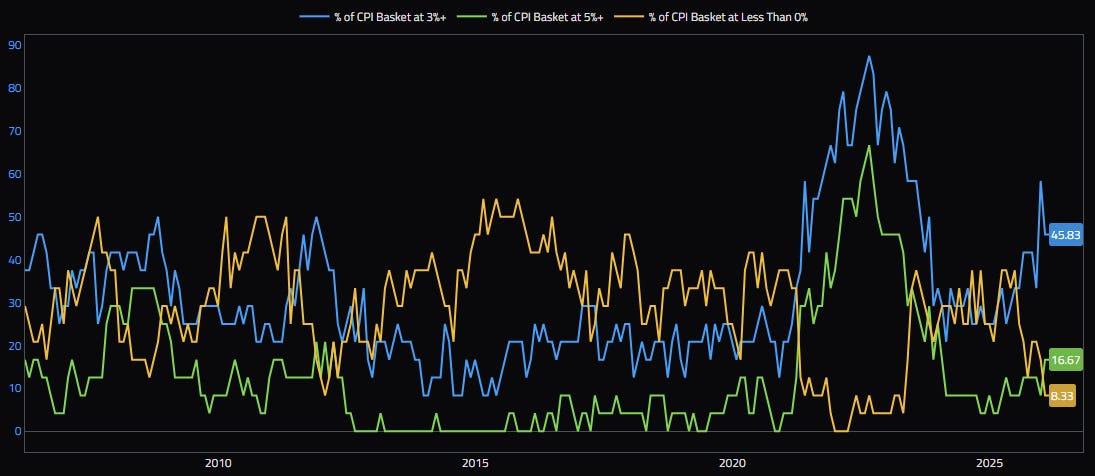

The inflation side of the mandate is the least likely to instigate cuts given it has largely flatlined and the ongoing oil supply shock will not help in the near-term.

If I were a Trump appointee who wanted to make a case for cuts, I would point to the seasonal distortions seen every Q1 since the pandemic and how they point to a declining trend.

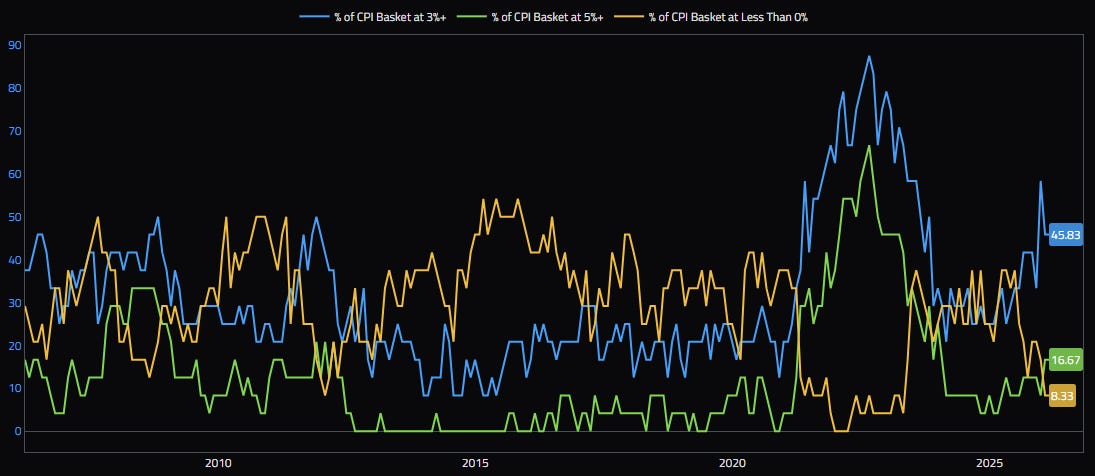

But given the Fed’s closer proximity to their perceived neutral rate after the 2024 and 2025 cuts, it is a higher bar to proceed from here. It is also not helpful to see inflation breadth rising as the number of components inflating >3% and >5% per year are rising while the components <0% are falling.

I am of the view that the disinflationary fruits have largely been squeezed. The most positive component is generally housing as its lagged effects are working through, however I question how much lower it can go given the labor force reduction from immigration increases replacement costs over time and financing costs remain elevated.

In summary, there isn’t a strong case to be made for the Fed to cut interest rates because of progress on inflation, particularly given the commodity supply shock is likely to cause problems for at least the next 3-6 months. This leaves their market stability and full employment mandates as likely to lead policy for the foreseeable future.

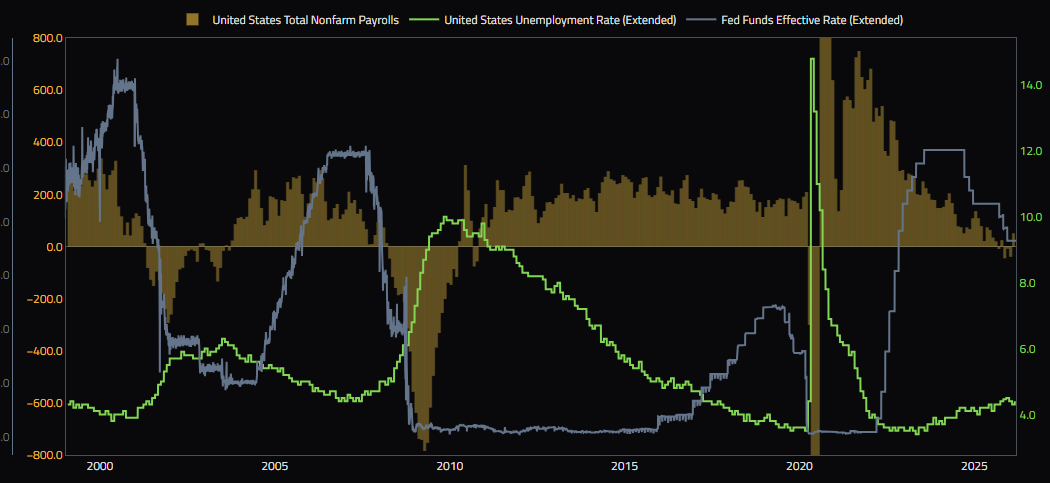

Looking at previous periods of Fed cutting, one could point to both early 2008 and late 2001 Fed cuts with the unemployment rate ~5%. In both cases, NFP prints were decidedly negative in the -50k to -100k+ range or lower. Both instances also saw >50% peak to trough S&P 500 drawdowns, but the Fed cuts began well before the drawdowns approached their extremes. The follow on round of cuts in September-December 2001 began with the S&P 500 -25% to -35% off its high while the January-March 2008 cuts came while the S&P 500 was -10% to -20% off its high. In neither instance was it Fed cuts that ultimately stopped the decline in equity prices.

In other words, the Fed put is probably lower than where many market participants currently perceive it to be and it is up for debate whether it even would fix anything.

I also interpret recent market price action to be saying “Houston, we have a growth problem”. It is approaching a near certainty at this point that the Fed will be late to supporting growth. We are beginning a slowly moving trainwreck.

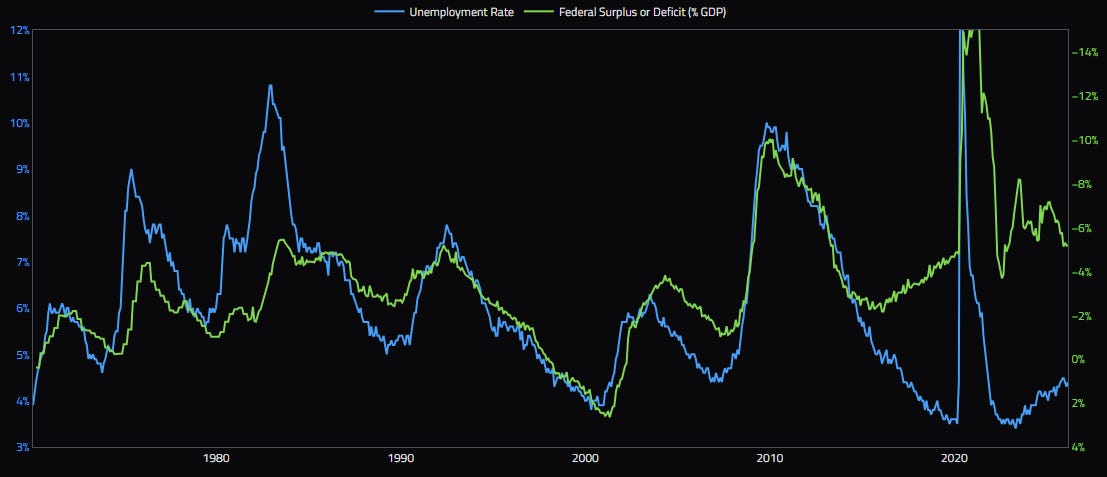

In the next 12-15 months, we are likely to approach a decision point for policymakers and bondholders.

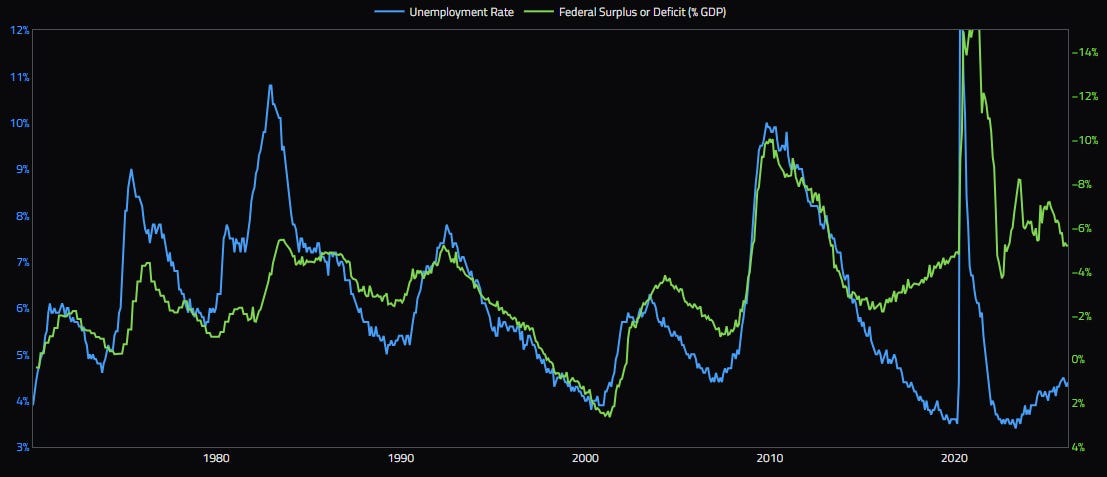

I hate to say it, but the historical relationship between unemployment rate and fiscal deficits as a percentage of GDP says we’re either headed for hyperinflation or a massive recession and big jump in unemployment.

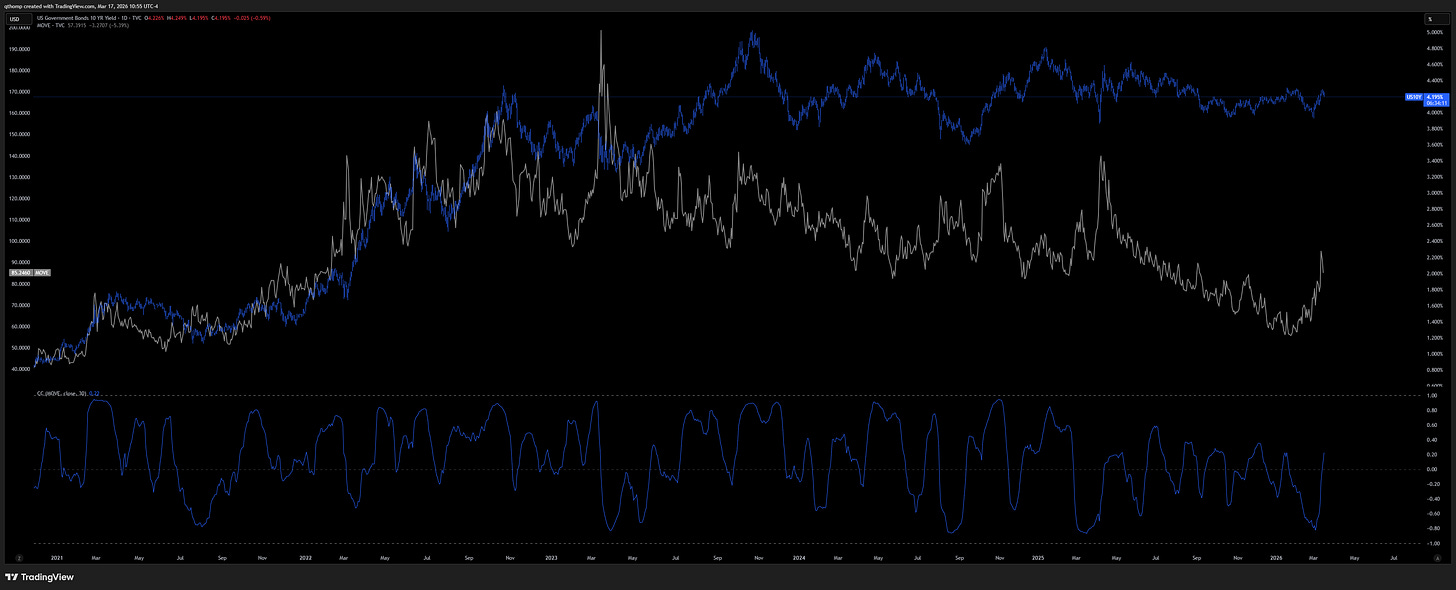

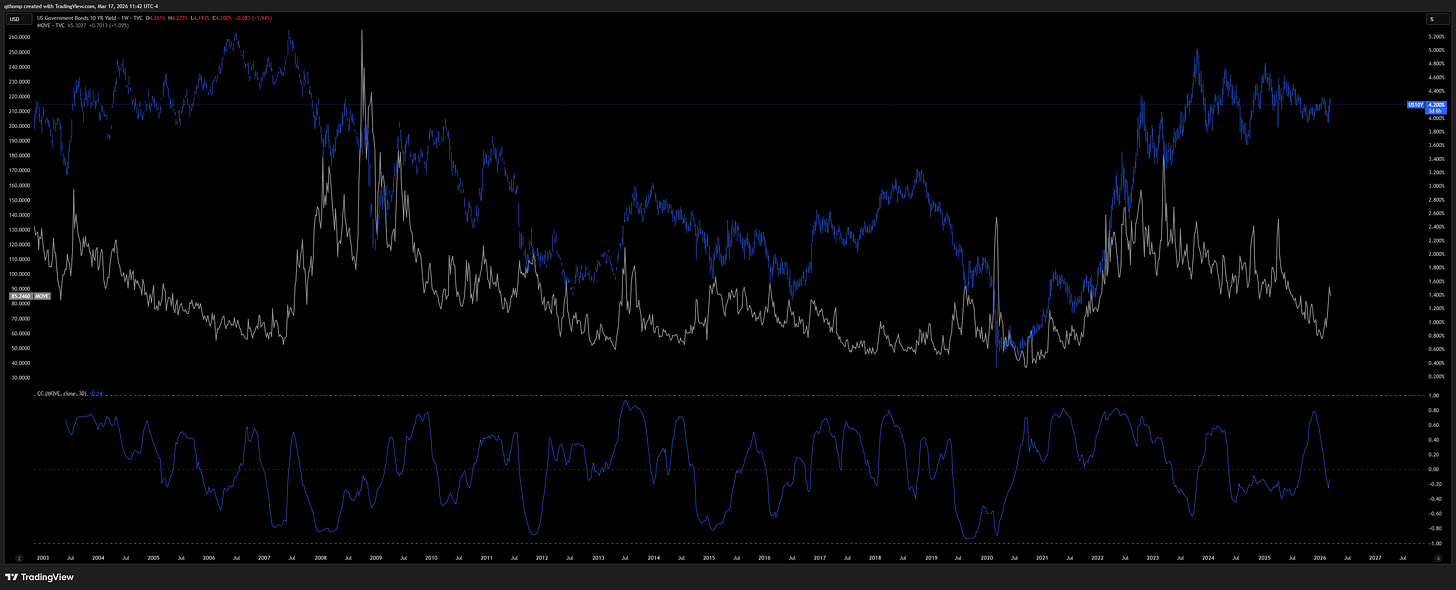

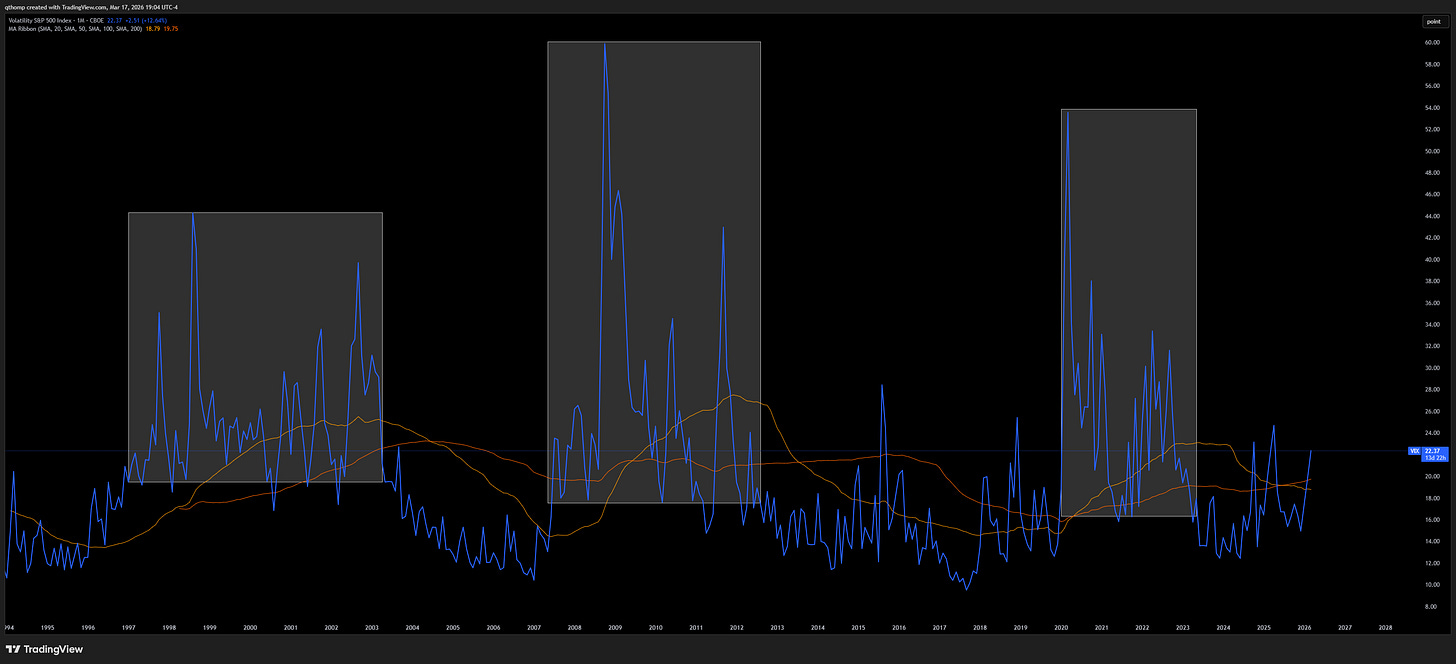

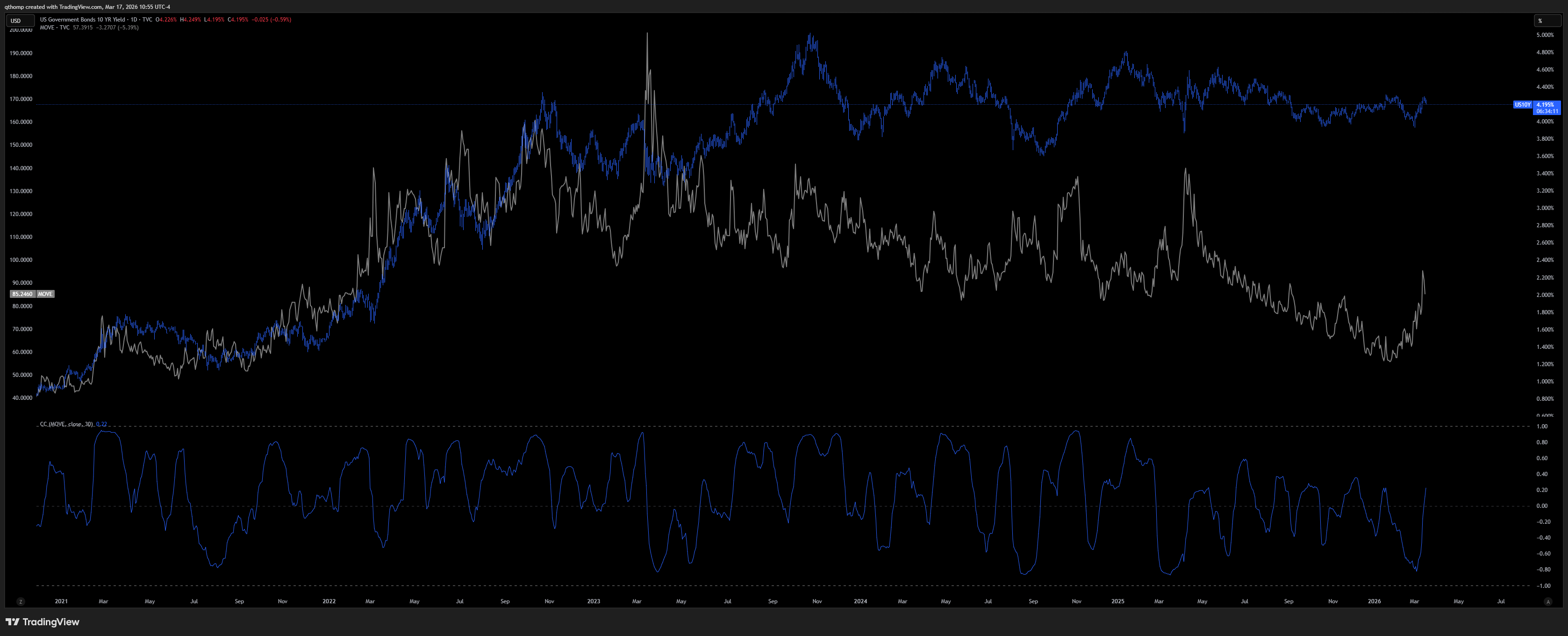

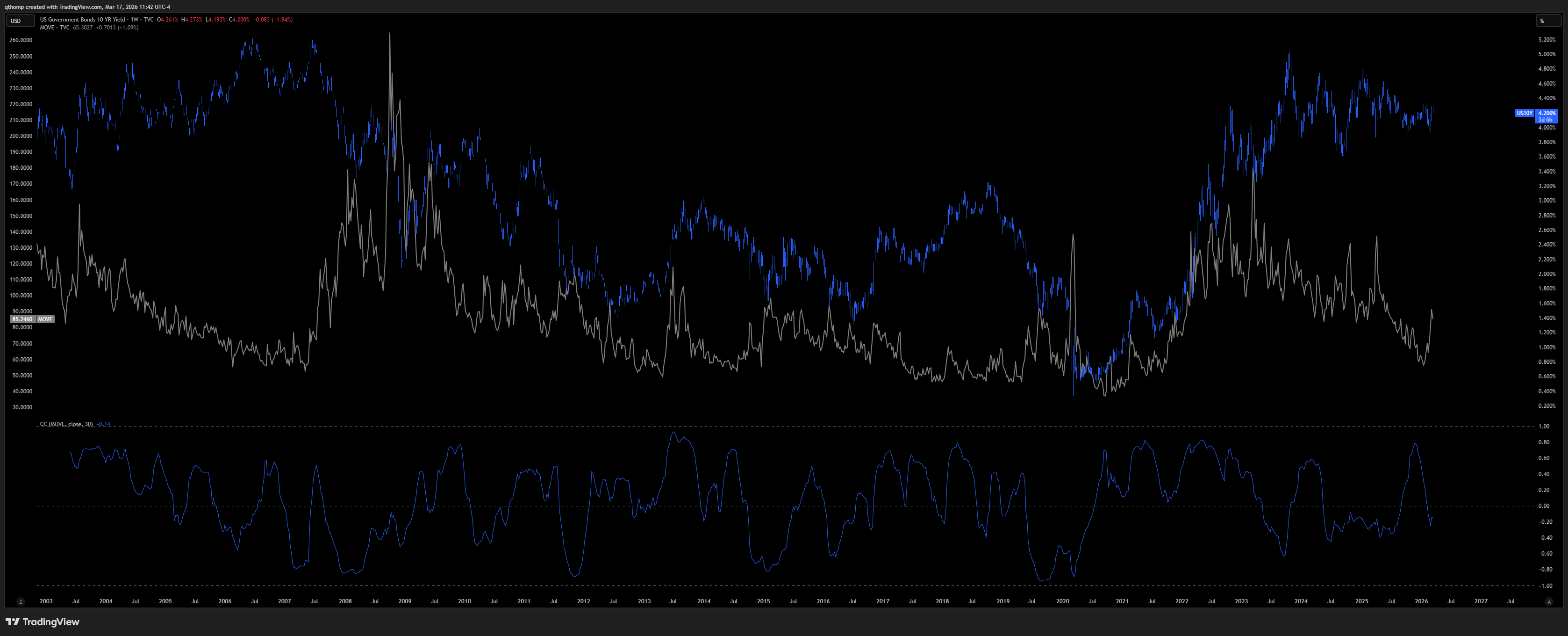

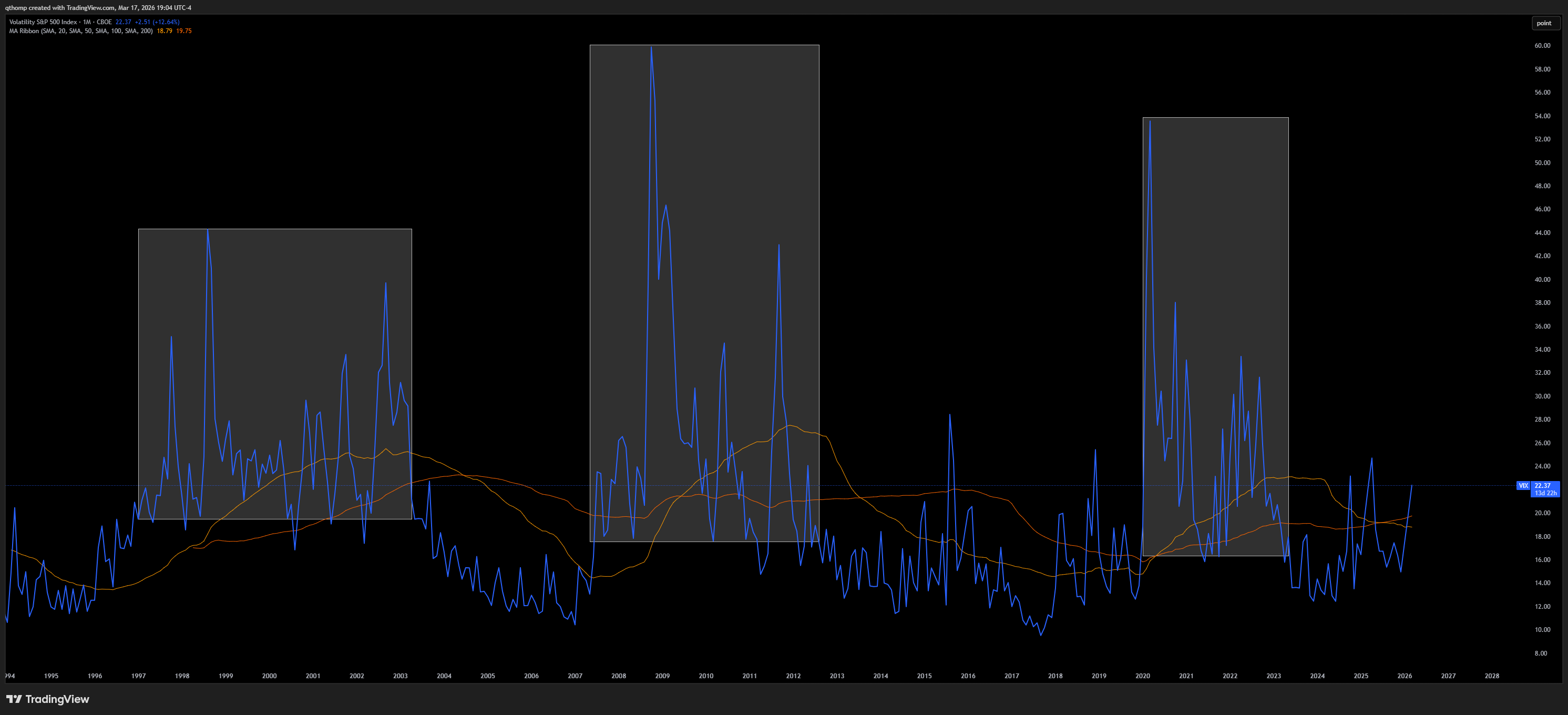

I’ve been wondering if bond volatility is cyclically bottomed. My gut says yes.

I think volatility across asset classes is entering a new structurally higher regime for that matter. Keep in mind that all else equal that lowers risk limits and gross exposures, particularly when paired with rising bond yields and volatility. This shouldn’t come as a surprise to anyone given we’re in a midterm election year and fighting a significant war. I suggest caution when anchoring too strongly to recency bias.

There are truly no safe havens out there.

I was talking markets with my friend Ram who has been calling things well and we view the world similarly. He mentioned even things like industrials ($XLI ETF) are stretched.

Ram Ahluwalia CFA, Lumida@ramahluwaliaIndustrials too $XLI7:11 PM · Mar 11, 2026 · 1.29K Views1 Reply · 6 Likes

Ram Ahluwalia CFA, Lumida@ramahluwaliaIndustrials too $XLI7:11 PM · Mar 11, 2026 · 1.29K Views1 Reply · 6 LikesI had been coming at the AI capex bubble top from a few different angles but this is another layer of confluence. Every possible you want to bet on this trade whether that be hyperscalers, raw inputs or semiconductors look topped.

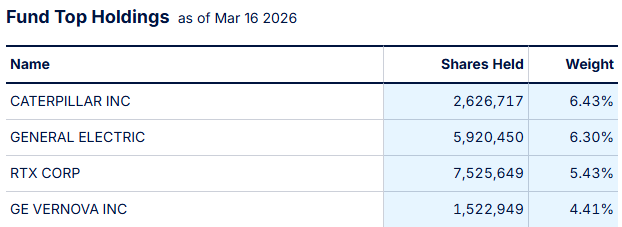

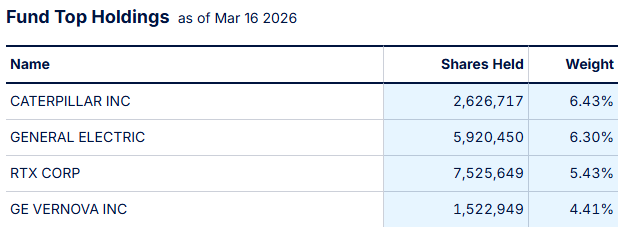

Oh you want to bet on the industrial builders who will benefit from the OBBB and AI capex boom? Good luck making money there as they all trade at massive all-time records that make the 2000 and 2008 stock bubbles look like childs play. Below are the top four holdings of XLI 0.00%↑ and other major industrial indices.

Defensives are another example of this extended valuation problem everywhere you look.

Quinn Thompson@qthompAnother illustration that displays just how few places there are to hide in this market. Short $COST big. Short $WMT smedium.

Quinn Thompson@qthompAnother illustration that displays just how few places there are to hide in this market. Short $COST big. Short $WMT smedium.

Quinn Thompson @qthompWalmart is now the 10th largest US public company by market cap at just over $1T, not far behind Berkshire in the 9th spot. Who has the best explanation for why $WMT and $COST trade at the valuation multiples they do?7:29 PM · Mar 10, 2026 · 6.11K Views1 Reply · 19 Likes

Quinn Thompson @qthompWalmart is now the 10th largest US public company by market cap at just over $1T, not far behind Berkshire in the 9th spot. Who has the best explanation for why $WMT and $COST trade at the valuation multiples they do?7:29 PM · Mar 10, 2026 · 6.11K Views1 Reply · 19 Likes

Crunch time is near and I continue to believe there is way too much complacency, regardless of the situation in the Middle East.

As we have been discussing in the chat, we favor agricultural commodities, natural gas producers, coal equities and other oil/energy equities from the long side. We have been seeking out shorts in the tech and semiconductor sectors in addition to Europe and certain Asian markets. Bonds remain for trading but we like a short bias there.

I hope everyone has a great weekend. Good luck out there.

Great Read as always

Nice writeup