Scouting the Tape - Apr 15, 2026

(Unique) macro idea generation and (insightful) market thoughts.

Today is April’s monthly Vixperation ahead of Friday’s equity and index options expiry. Today is also Strategy’s preferred stock STRC ex-dividend date. I have some travel the rest of the week so I figured I’d get this piece out earlier than normal. This week’s issue covers the coming IPO supply, DATs (MSTR, BMNR), crypto, the Trump policy agenda and the dollar.

Upcoming IPO supply.

Credit to @history_applied on X for the idea following the below tweet.

Applied History_65@history_appliedThought exercise on Anthropic/OpenAI/SpaceX IPOs & SaaS/IGV: > All 3 in QQQ by late ’26 at roughly $1.5T/$1.0T/$1.2T (~11% of NDX). > Flat‑index math implies IGV‑style software (~$7.1T today) could fall ~32% below 4/10 prices to fully “fund” their weight as offset to Jan 1

Applied History_65@history_appliedThought exercise on Anthropic/OpenAI/SpaceX IPOs & SaaS/IGV: > All 3 in QQQ by late ’26 at roughly $1.5T/$1.0T/$1.2T (~11% of NDX). > Flat‑index math implies IGV‑style software (~$7.1T today) could fall ~32% below 4/10 prices to fully “fund” their weight as offset to Jan 1 9:10 PM · Apr 11, 2026 · 54 Views2 Likes

9:10 PM · Apr 11, 2026 · 54 Views2 LikesPrivate capital markets have never been as large as they are today so there’s never been anything close to what we’re seeing in pre-IPO land. The fact that we may see 3 IPOs this year that are instantly top 10 largest market caps in the world is wild to wrap your head around. It’s an interesting thought exercise to try to quantify their impact on the rest of the market.

Napkin math says QQQ has a ~$30T market cap and ~$3-4T of IPO market cap coming down the pipe. That $3-4T of new IPO market cap equates to ~9-12% of total ~$33-34T pro forma QQQ market cap. In other words, for these three companies to join the index, every other company’s weight must decrease proportionally by ~9-12%. To be precise, 3 companies will also be removed from the index but the smallest companies have market caps in the $15-20B so the removal of their market caps are insignificant to our napkin math.

Taking it one step further, the negative impacts manifest in two ways - mechanical selling and thematic substitution.

Mechanical selling: The QQQ ETF currently has ~$400B in AUM, so to add a new ~9-12% position requires ~$36-48B of selling of its current holdings.

Thematic substitution: The companies most negatively impacted are legacy software firms (eg IGV ETF). Investors view these AI businesses as both software killers and ‘new software’. While everyone is understandably viewing the SaaS apocalypse through a fundamental lens, there’s a very real mechanical, index level element to it too.

So how do you express this trade?

First glance would be to short the most acutely affected software which is playing out in spades right now (see IGV).

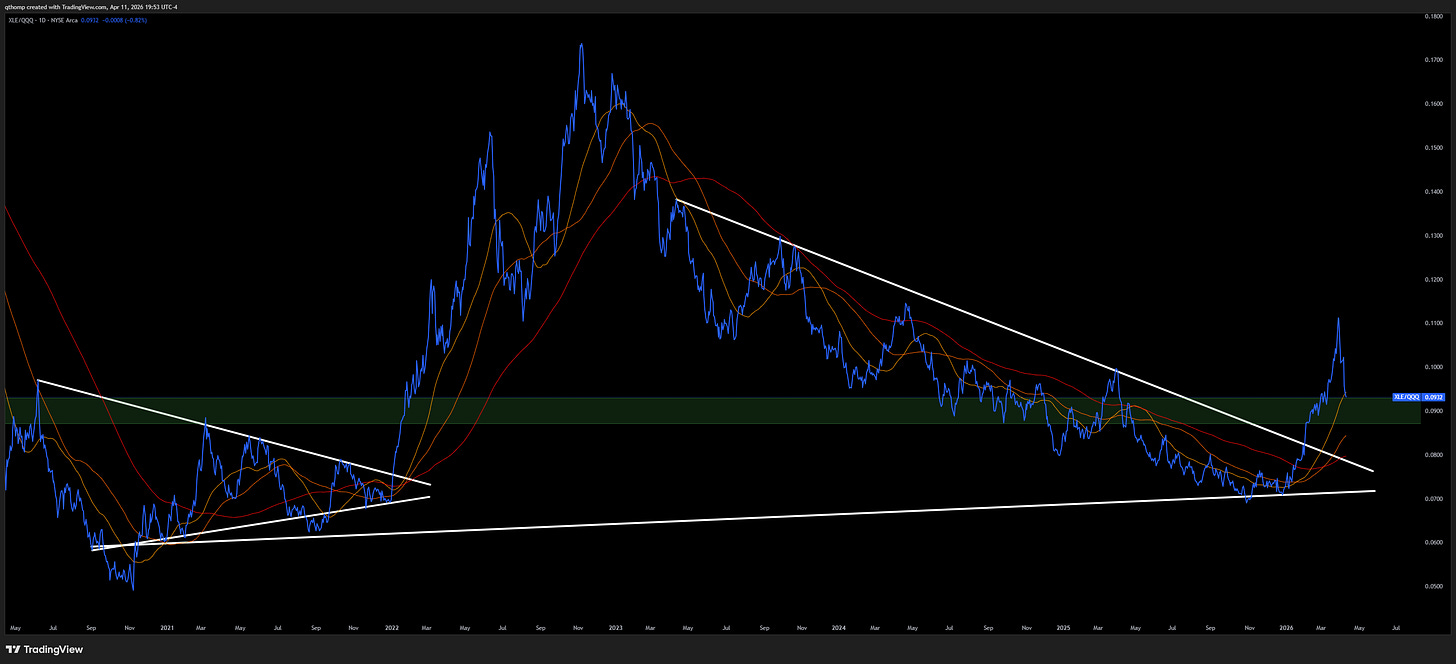

You could also use QQQ as a funding short versus your favorite longs in parts of the market that are neither affected on a sectoral basis nor an index rebalancing perspective. For example, long oil and gas via XLE against short QQQ. Not that it is recommended to rely on technical analysis for ETF pair trading, but I like the risk reward setup here. Feel free to apply this logic to your favorite sector, country or ETF that is far removed from mega cap tech concentration.

One might also think to short the largest market cap companies in the index who could be most affected by the largest negative flows on a nominal basis (eg Mag7). The other element to consider here is that the market may view these IPO events as liquidity/balance sheet boons for the businesses with large stakes in the newly public companies. Microsoft (~25-30% of OpenAI), Amazon (10-15% of Anthropic) and Google (strategic stake in Anthropic) stand to benefit the most. Nvidia owns a small stake in OpenAI and Tesla a small portion of SpaceX via xAI, however both are much smaller percentages of their market cap relative to the first three. Apple, Meta and Broadcom have no ownership in any of them.

This is a very unique scenario the market has never experienced before prior to the rise of private capital markets. The above logic can just as easily be applied to the S&P 500 index as a whole, or SPY instead of QQQ. The magnitude of impact on SPY is about half of QQQ given underlying SPY market cap is ~$60T compared to QQQ’s ~$30T. This means its up to a 4-6% in each company’s weight. Despite it being a smaller effect, the size of assets tied to the index is drastically larger. There is an estimated ~$15T in total assets tracking or benchmarked to the S&P 500, with ~$700B in SPY alone compared to QQQ’s $400B. This is a whole market moving event!

It’s never a good thing to overstretch ($STRC).

I’ve been writing about the Strategy capital structure over the last few weeks but want to expand on it.

Quinn Thompson@qthompYou'd think with $MSTR -80% from highs, bagholders would be more skeptical of every new "digital credit" innovation and its effect on the capital structure, but given the hype over $STRC, that appears to not be the case. While consensus on crypto twitter seems to be that $STRC

Quinn Thompson@qthompYou'd think with $MSTR -80% from highs, bagholders would be more skeptical of every new "digital credit" innovation and its effect on the capital structure, but given the hype over $STRC, that appears to not be the case. While consensus on crypto twitter seems to be that $STRC Quinn Thompson @qthompI don't think the lows in $MSTR nor its premium to NAV are in. True capitulation only arrives when the orange dots stop. https://t.co/Xo0lbzEvxE3:03 PM · Mar 31, 2026 · 51.8K Views43 Replies · 13 Reposts · 179 Likes

Quinn Thompson @qthompI don't think the lows in $MSTR nor its premium to NAV are in. True capitulation only arrives when the orange dots stop. https://t.co/Xo0lbzEvxE3:03 PM · Mar 31, 2026 · 51.8K Views43 Replies · 13 Reposts · 179 LikesThe "blow up risk" framing for MSTR misses the point. It's not an Enron overnight implosion - the capital structure doesn't work that way. The real risk is death by dilution. With the stock -75% from its highs, I’m surprised this is still controversial. They're already diluting common stock ~3% annually to service debt interest and pref dividends. If they issue another $10-15B of STRC that rises to 5-7%. Permanently instituting a 5-7% annual dilution rate to your common equity strikes me as a poor strategic decision and I imagine the company’s corporate finance team is well aware of these risks.

While most are focusing on the success of STRC and its growth, which can likely be attributed to the company’s tried and true strategy of dumping on retail (see -75% performance of MSTR from its peak). Most recently their CEO was on a Bitcoin podcast saying this is a great savings vehicle for people living paycheck to paycheck, comparing this preferred stock to a bank account. This is on top of the company’s frequent disingenuous ads. Even if the immediate term demand from unsophisticated investors is there, maxing it out increases dilution strain and adds risk to the capital structure.

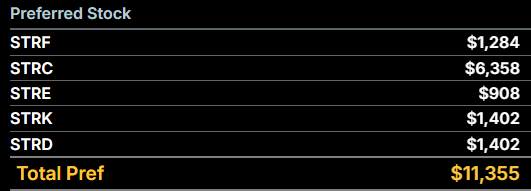

What do you notice about this picture? One of these instruments is sold to retail and the rest are sold to institutions. I’ll leave it to you to see which one has grown the largest and guess why.

The moral of the story is they’re reaching a point where STRC is tapped out and that is one less tool available to acquire more Bitcoin. MSTR common equity is already largely tapped and the unsecured credit markets are also unlikely available. From here, the remaining tool would be to encumber their Bitcoin holdings to issue secured debt against it and further lever the company up. The problem with this is that it adds even more pressure to their annual interest and dividend burden as that debt would come with a cost. It also removes a lot of future financing flexibility if they were ever to get into a bind. I would think they’d save this lever as a last resort rather than empty those bullets now.

Assuming they don’t go the secured debt route, the only real way to increase their financing capacity to buy more Bitcoin is if the price of Bitcoin itself materially rises. Obviously an expanding MSTR premium to NAV also would suffice but that is unlikely to happen without the former. You can see how reflexive this all is.

With Microstrategy soon to be out of the market, and a Bitcoin price increase the only real way for them to come back, they will need someone else to carry the burden of bidding the asset from here. Given the company is levered, all of its financial and balance sheet health metrics worsen if Bitcoin does not stay elevated. The situation to be weary of is one where BTC trades into the low 50s, and the annual interest and dividend dilution burden on MSTR rises to 4-8%. Let’s say the price of STRC then also falls and they have to further increase the dividend rate and the MSTR dilution along with it. This is where a prolonged period of BTC weakness starts to create a material drag and negative bleed spiral on MSTR. This will create a direct conflict between STRC and MSTR holders because the trade off will be to either let MSTR dilution run rampant or cut the STRC dividend rate and impair the pref holders. Again - neither are “blow up risk” in an immediate evaporation sense, but rather a long-term demise for MSTR holders, which shouldn’t be controversial given that’s exactly been what’s going on since late 2024.

Back in November 2024 when I happened to get lucky and call the intergalactic MSTR to almost the hour, someone asked me to explain how it works and I made this meme. It’s funny how well this simple picture describes every new ‘financial innovation’ that Saylor drums up.

Quinn Thompson@qthomp@JamesDa47116905 Here you go 4:46 PM · Nov 20, 2024 · 42.4K Views9 Replies · 5 Reposts · 95 Likes

4:46 PM · Nov 20, 2024 · 42.4K Views9 Replies · 5 Reposts · 95 LikesI find it a discouraging sign that BTC is flat to the S&P 500 over the last month. Given it has been trading with a lot more downside over the past bunch of months, I still don’t think it’s an interesting long. I believe we’re at or near peak short squeeze / animal spirits locally and when you combine that with Saylor jamming into BTC hard ahead of STRC’s ex-dividend date, I’m unimpressed that it’s only flat to S&P 500 in the last month.

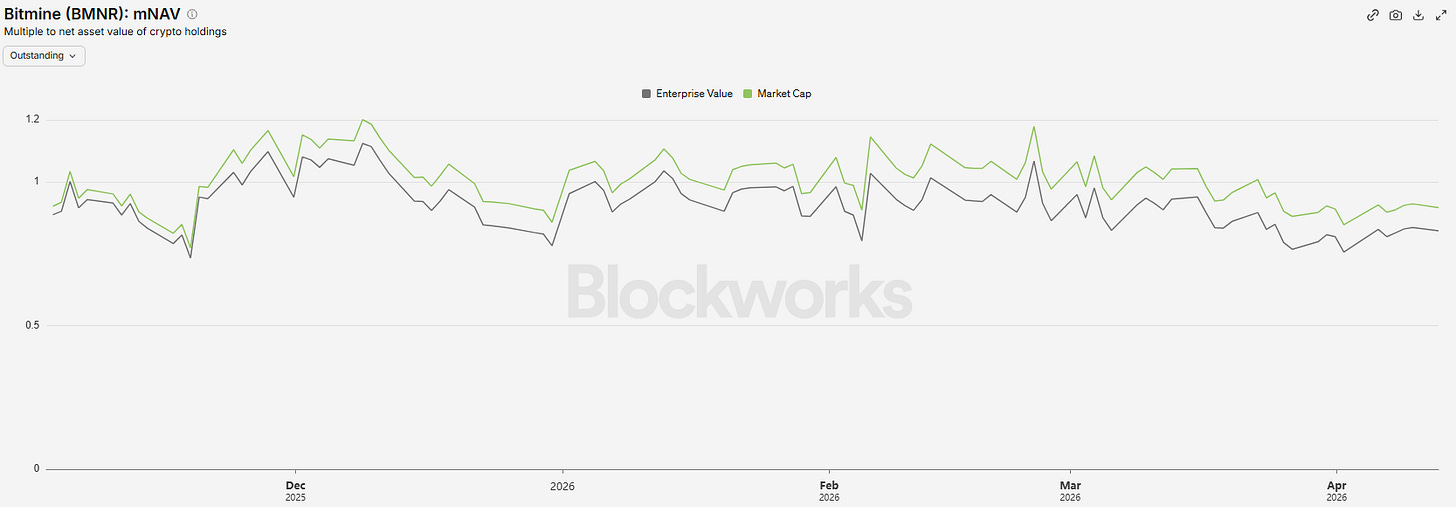

While I’m at it, might as well cover my quick thoughts on $BMNR, ETH, SOL and HYPE.

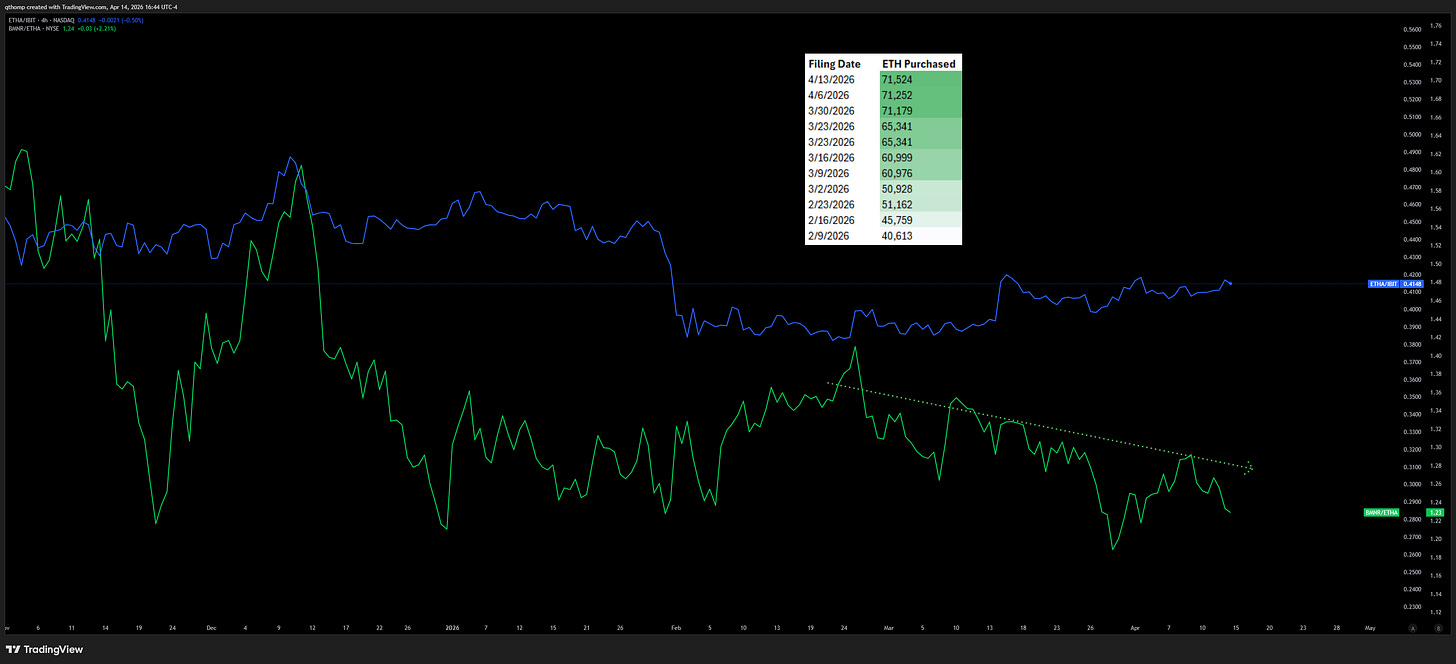

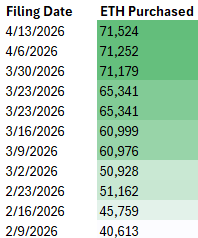

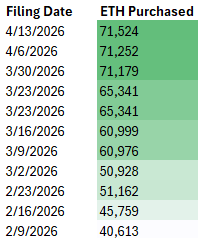

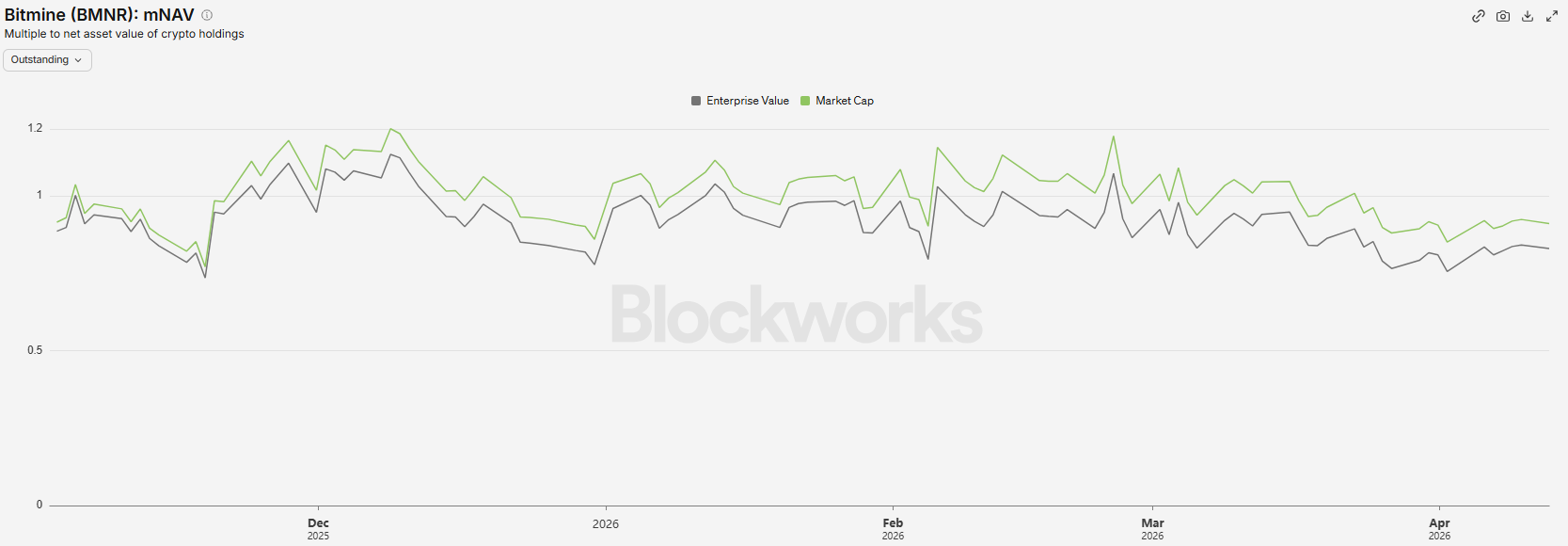

BMNR’s rate of ETH purchase (and equity sales) have nearly doubled since early February. This has weighed on the company’s premium to NAV (green line).

Some data provider dashboards show BMNR’s premium to NAV as closer to 0.9, others show it still above 1.0. My calculations have it just crossing below 1.0 this week.

Moral of the story here is that unless a second wind arrives, Tom Lee is also going to be sidelined for awhile or at least be forced to retreat from the recent level of buying.

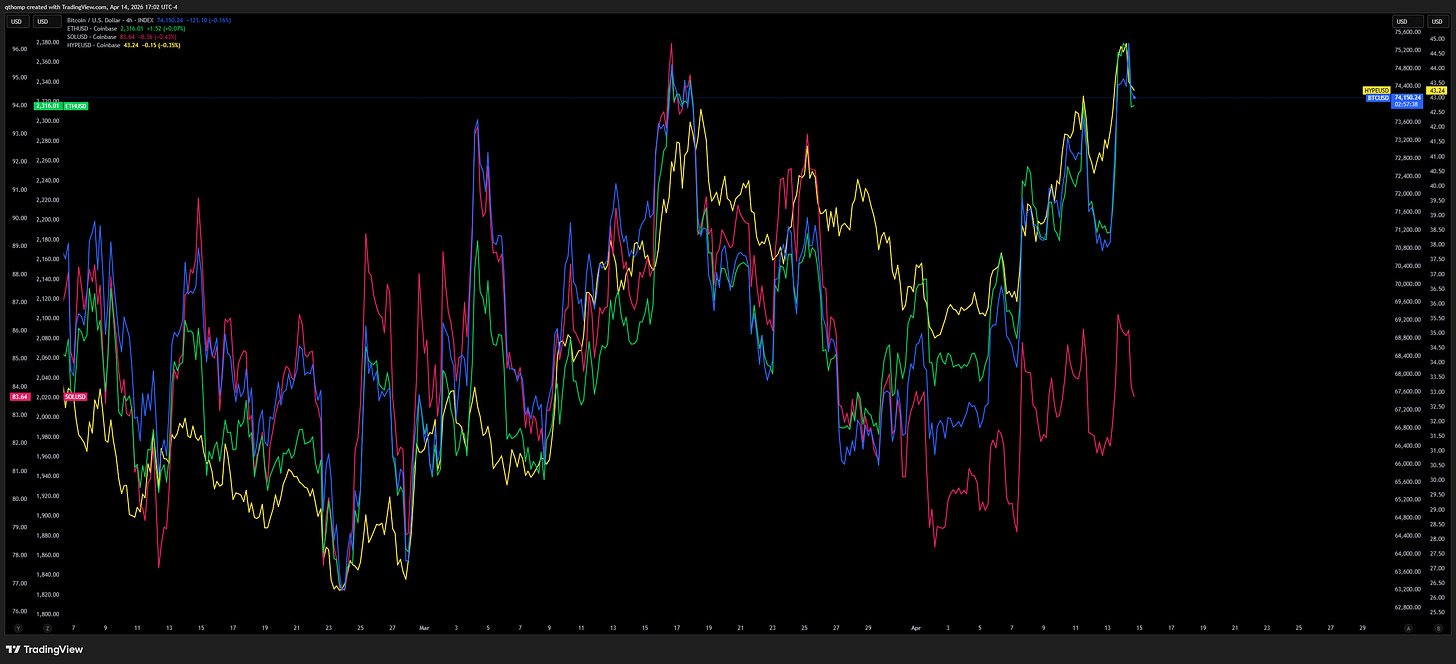

From the early Feb lows, the four majors have largely been trading in lockstep.

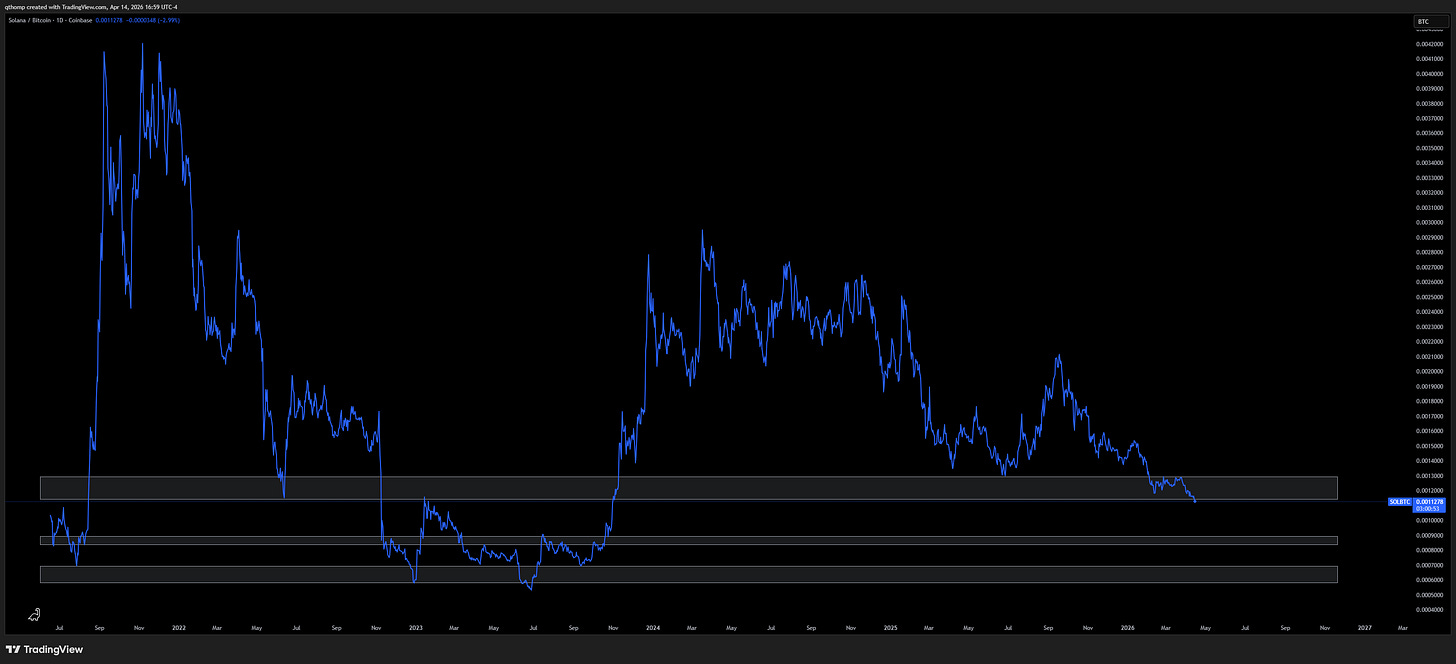

SOL has been the noticeable laggard. I’m not really sure what’s going on here. Maybe it has something to do with the large hack of one of its major exchanges but I don’t know.

HYPE has been the best performer and most interesting out of the 4 majors. Despite declining revenues and open interest since last summer, it’s garnered a lot of attention around its traditional asset trading, especially on volatile weekends with war headlines and oil moves. I will be interested in watching its revenue profile over time to see if it can diversify away from crypto because as of now it appears to be still heavily reliant on crypto prices doing well. Their CEO was recently featured on a magazine cover. It’s a great product and one of the few success stories in crypto from the last 18 months. I’m struggling to wrap my head around its valuation at $43B (or $11B circulating). It’s been difficult to get a straight answer around unlocks from people closer to the project than me. Robinhood trades ~$75B, Nasdaq trades ~$50B and Coinbase ~$40B.

Trump admin policy agenda.

When I objectively analyze the aggregate of Trump’s economic agenda, it is quite the mixed bag. On the one hand, there are countless pro-growth measures ranging from financial and energy deregulation, OBBB tax incentives and easing pressure on monetary policy and financial conditions.

On the other hand, there are also many blatantly anti-growth measures like ending immigration, tariffs and slowing global trade, reducing government spending and starting a war that leads to an oil price/supply shock.

The current tallying up of results is showing a 30 year bond yield at the same level as January 2025 inauguration (the 10 year is ~20-30 bps lower). I would rate the anti-growth measures as stronger and more immediate than the pro-growth measures which take longer to work through, but yet bond yields aren’t showing much progress nor a bid for safety. I attribute that to the fact that government spending is still at long-term problematic levels.

I don’t have many answers for you on this one but the point of the section is to more so amplify this idea that you don’t hear much about. Many of the administration’s largest policy changes thus far have weighed significantly on economic growth. These measures have worked to dampen growth and keep a lid on bond yields in the short-term. The cost has largely been borne by middle and low income workers and young new entrants to the workforce who are facing some of the worst labor market conditions in decades. The beneficiaries have been the mega cap tech and AI sectors and wealthy Americans who benefit from the uneven monetary policy and rising asset prices as a result of loose financial conditions. Over the long-term, this is unsustainable, but it remains to be seen when it reverses in the interim.

The dollar has structural problems.

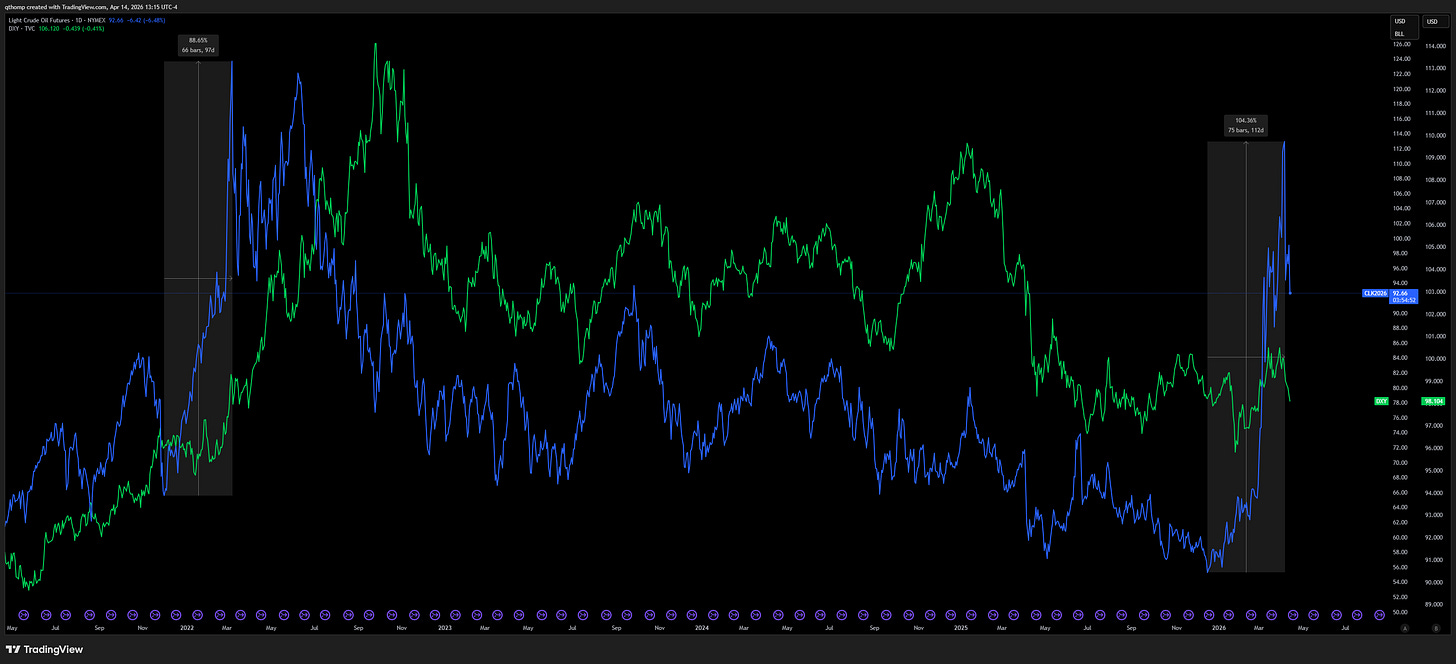

When you compare the 2022 oil price spike with 2026’s, the oil price increase has been greater while the rise in the dollar has been smaller. That said, a lot of the dollar’s rise in 2022 came after oil put in its highs. Locally I expect the dollar to bounce here, but I also don’t want to long-term fight the administration’s stated priorities of targeting a weaker dollar when other data points also align.

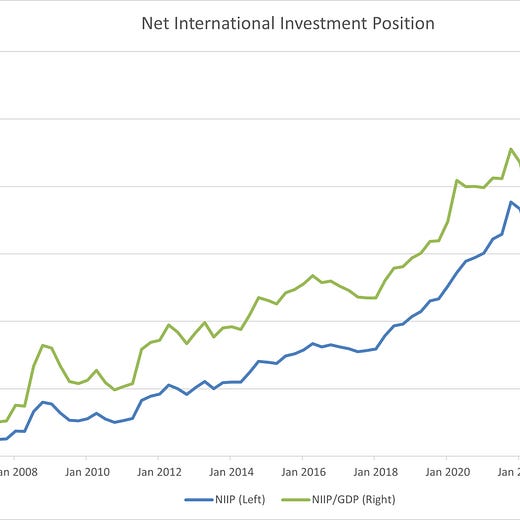

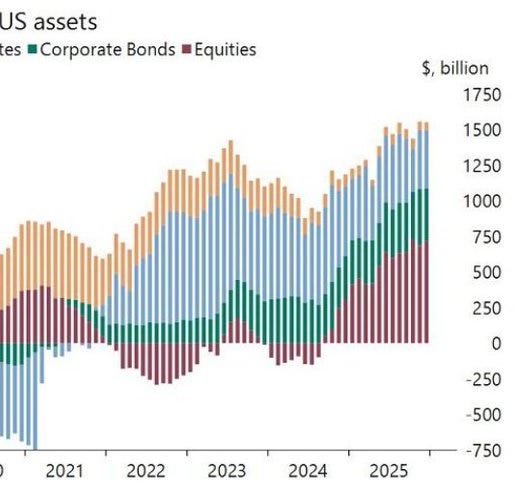

I believe this weight on the dollar has to do with the imbalance in the net international investment position as foreign capital is crowded into US assets.

Quinn Thompson@qthomp@fejau_inc I want to agree given the US is the world's most dominant energy power as the largest oil and gas producer globally. However, my argument for this time being different is that the Net International Investment Position in US assets has never been larger both outright and as a %

7:34 PM · Mar 8, 2026 · 13.8K Views5 Replies · 4 Reposts · 67 Likes

7:34 PM · Mar 8, 2026 · 13.8K Views5 Replies · 4 Reposts · 67 LikesIgnoring everything else and simply evaluating how global bond and currency markets are trading, the tape is telling me that policymakers and the powers that be are content choosing to sacrifice the currency to keep a floor under nominal equity prices and a lid on bond yields. This is nothing new.

Why my antennas are raised now though is because we have a +60% rise in front month oil (+30% in December contracts) since January 1st. The disinflation from 2025 has reversed back towards inflation. Suppressing bond yields and supporting stock prices loosens financial conditions and the economy and increases the chances that inflation is stickier for longer. I think this is going to be a very important concept for successful trading over the coming months.

This week I have reloaded on gold and metals longs as a result. With midterms now only 7 months away and campaigning to start picking up over the next month or two, I don’t really see how the inflation genie gets stuffed back in the bottle. At this point all I see is a ‘pretend and extend’ approach by the administration which will make matters worse down the road.

Have a great week!

One note on STRC - a 5-7% MSTR dilution rate to cover dividends today is not a 5-7% dilution rate forever. The dividends are fixed in dollar terms, so if the BTC price doubles and mNAV stays at similar levels, the dilution needed to service the dividends is cut in half. If you think BTC 3-10x's over the next 5-10 years, today's dividends are almost immaterial by then.

Ofc, they'll be issuing STRC all along the way, so the debt service need will rise as well, but that's a lever they control, and can cut if needed.

Great article - what’s your take on SOXX short? I’m in SOXS but feels early