Scouting the Tape - Apr 24, 2026

(Unique) macro idea generation and (insightful) market thoughts.

This week’s issue is focused on global FX and bond markets. It is often said that if you get the dollar right, you will get a lot of other things right. I think that will hold true over the coming months and this part of the market is not getting enough attention.

Our latest Forward Guidance podcast is out here.

The Yen has been top of mind for awhile now but I haven’t been able to identify exactly why.

Wrote this note on January 27 after the latest USDJPY intervention.

Discussed US-Japan policy decision making in the March 7 Scouting the Tape.

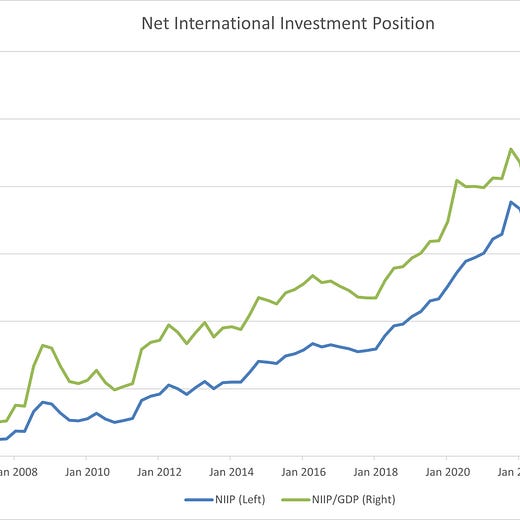

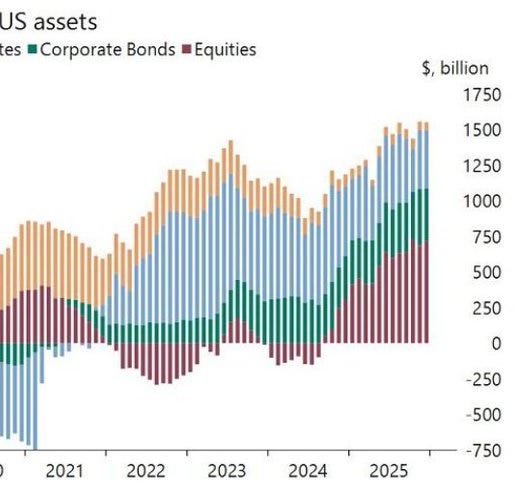

Posted about the headwind that the NIIP imbalance puts on the dollar.

Quinn Thompson@qthomp@fejau_inc I want to agree given the US is the world's most dominant energy power as the largest oil and gas producer globally. However, my argument for this time being different is that the Net International Investment Position in US assets has never been larger both outright and as a %

Quinn Thompson@qthomp@fejau_inc I want to agree given the US is the world's most dominant energy power as the largest oil and gas producer globally. However, my argument for this time being different is that the Net International Investment Position in US assets has never been larger both outright and as a %

7:34 PM · Mar 8, 2026 · 19.8K Views6 Replies · 5 Reposts · 82 Likes

7:34 PM · Mar 8, 2026 · 19.8K Views6 Replies · 5 Reposts · 82 Likes

Setting the stage.

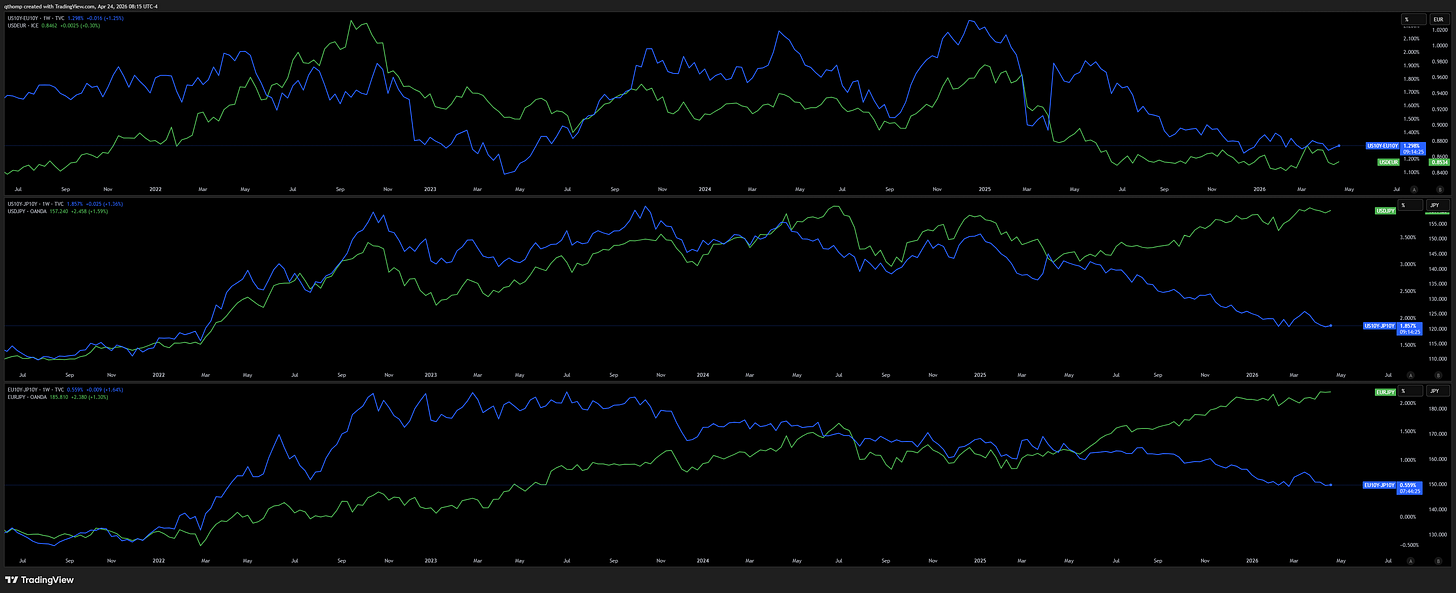

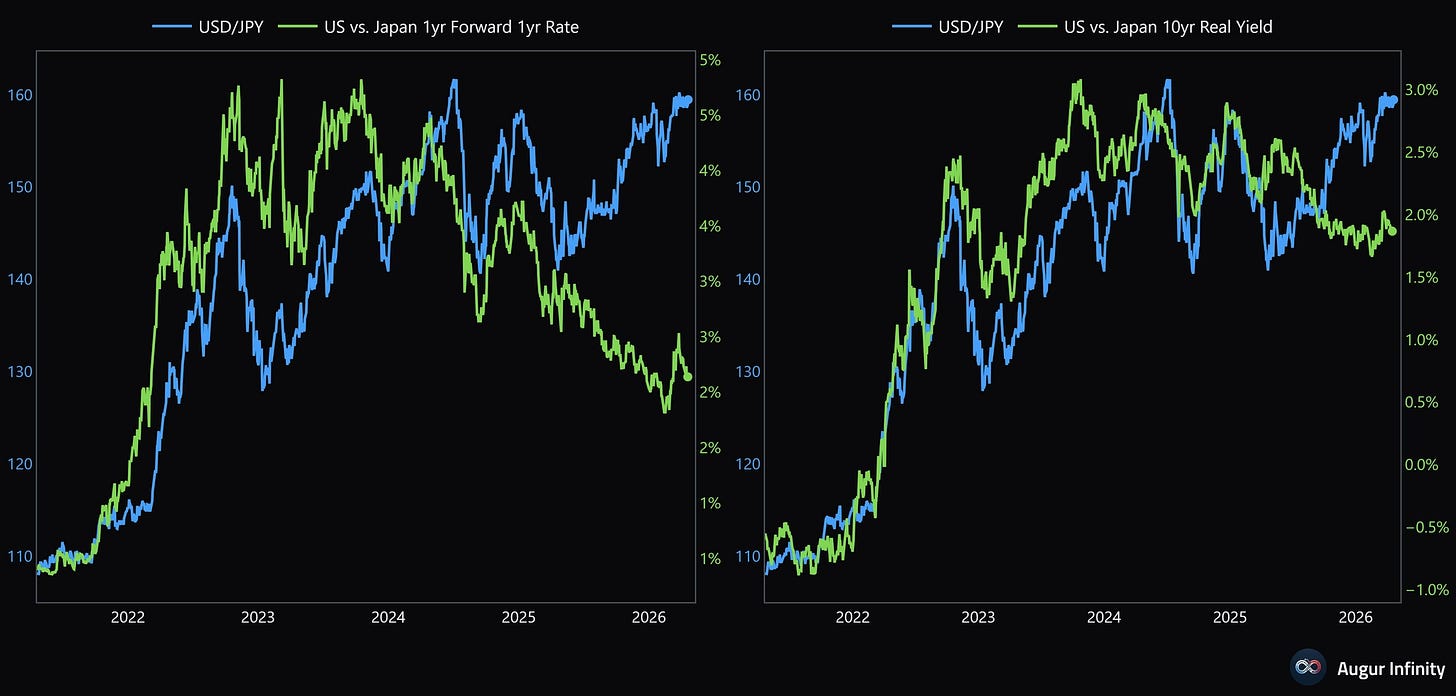

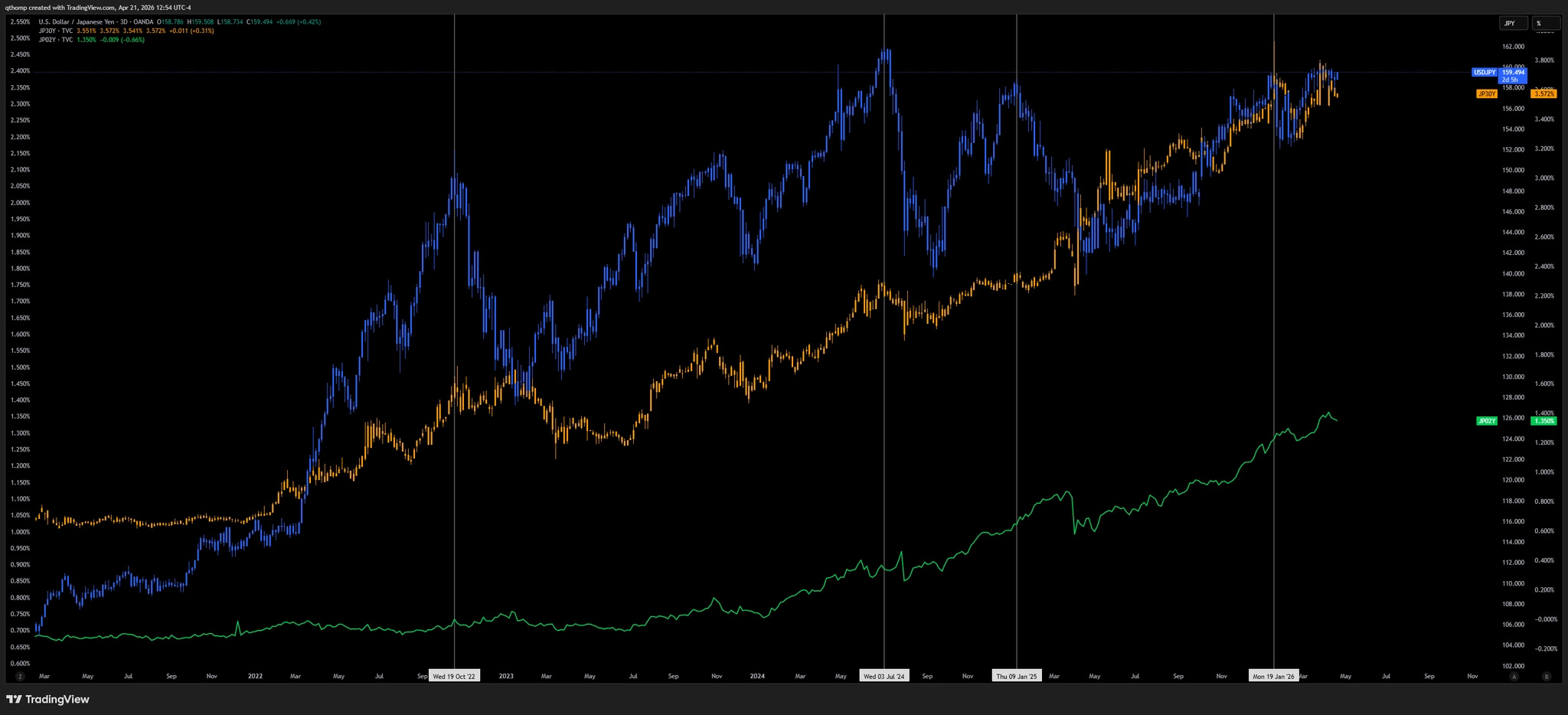

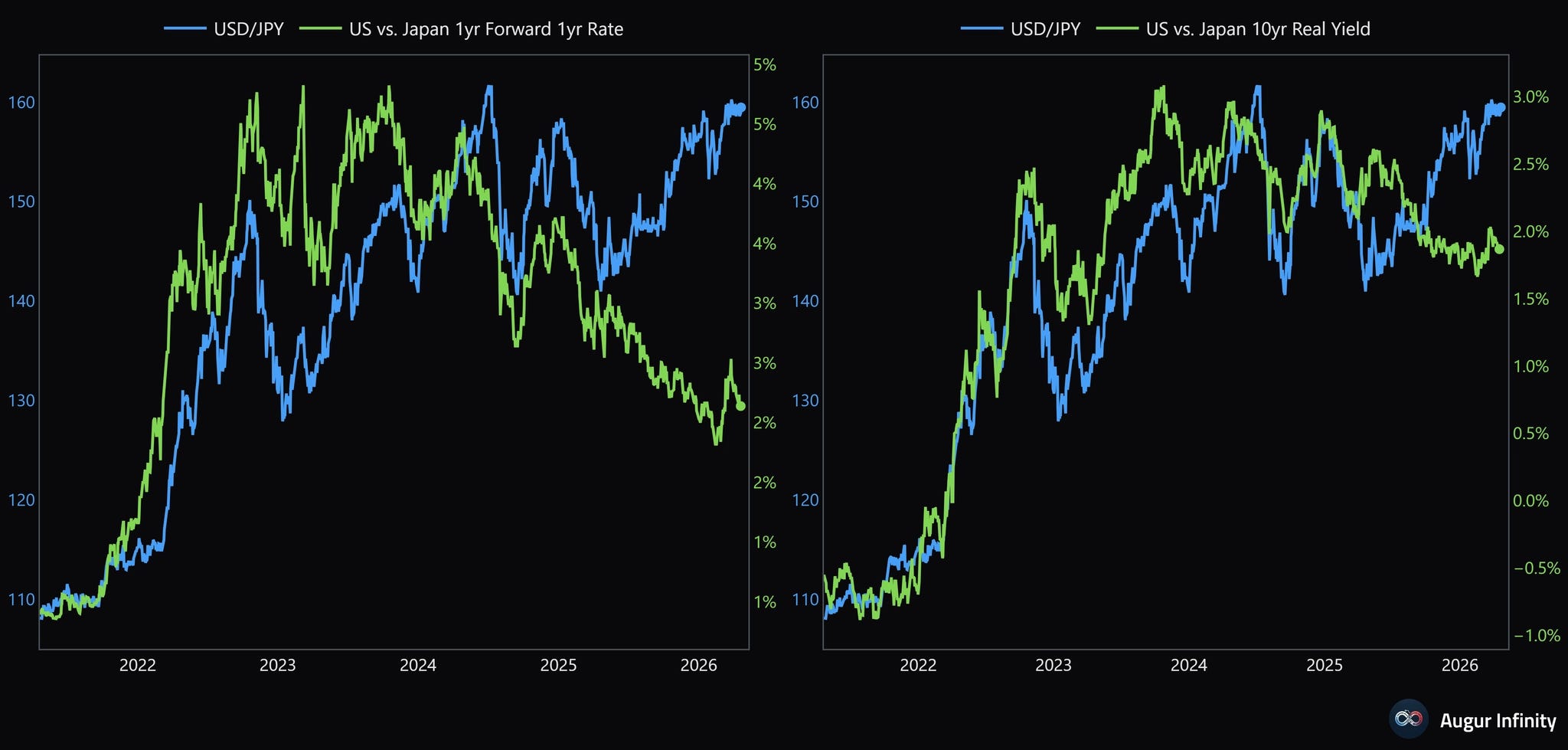

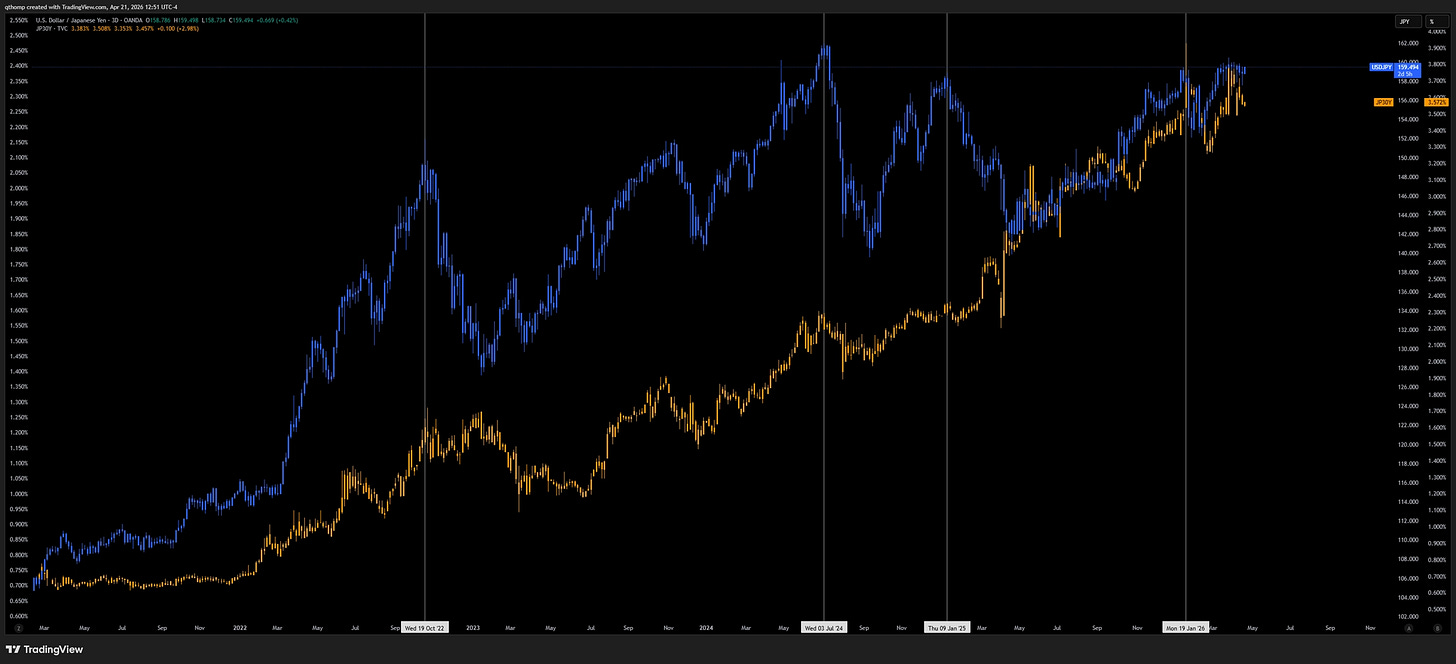

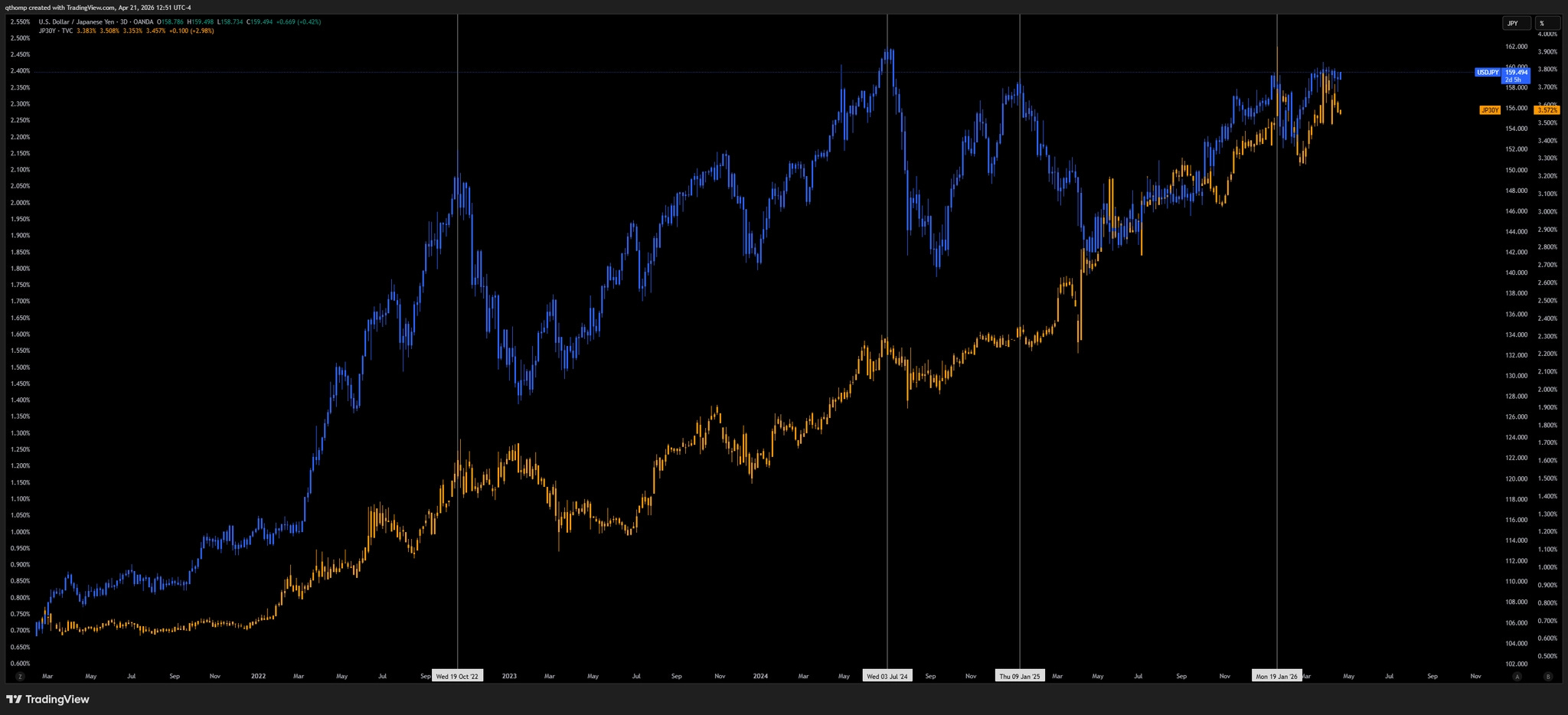

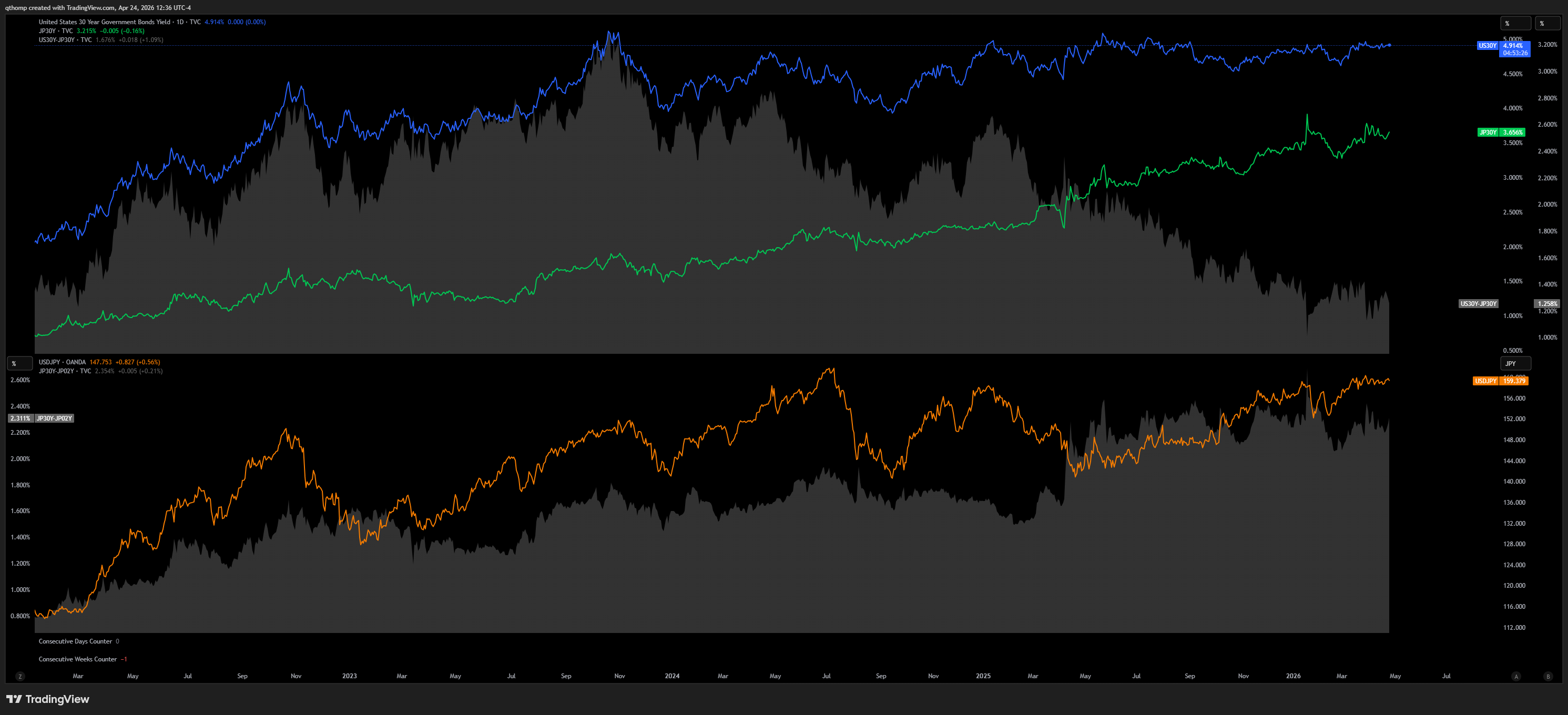

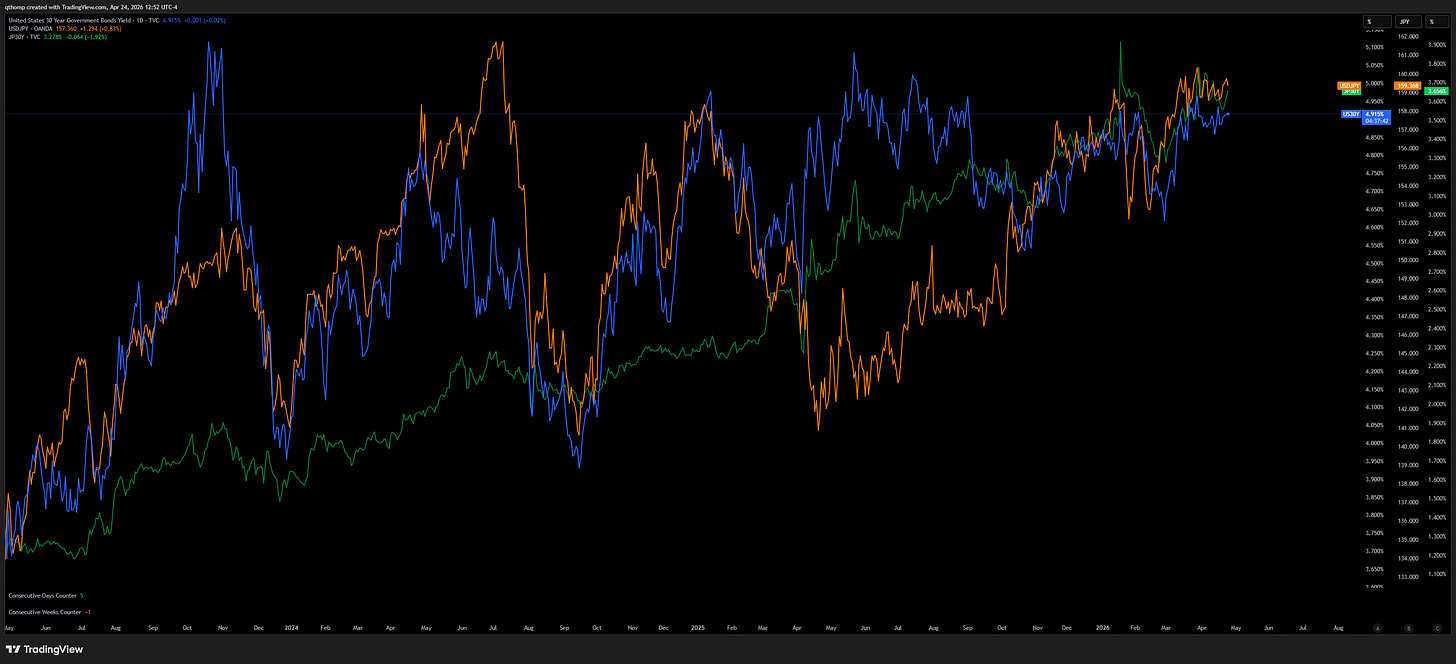

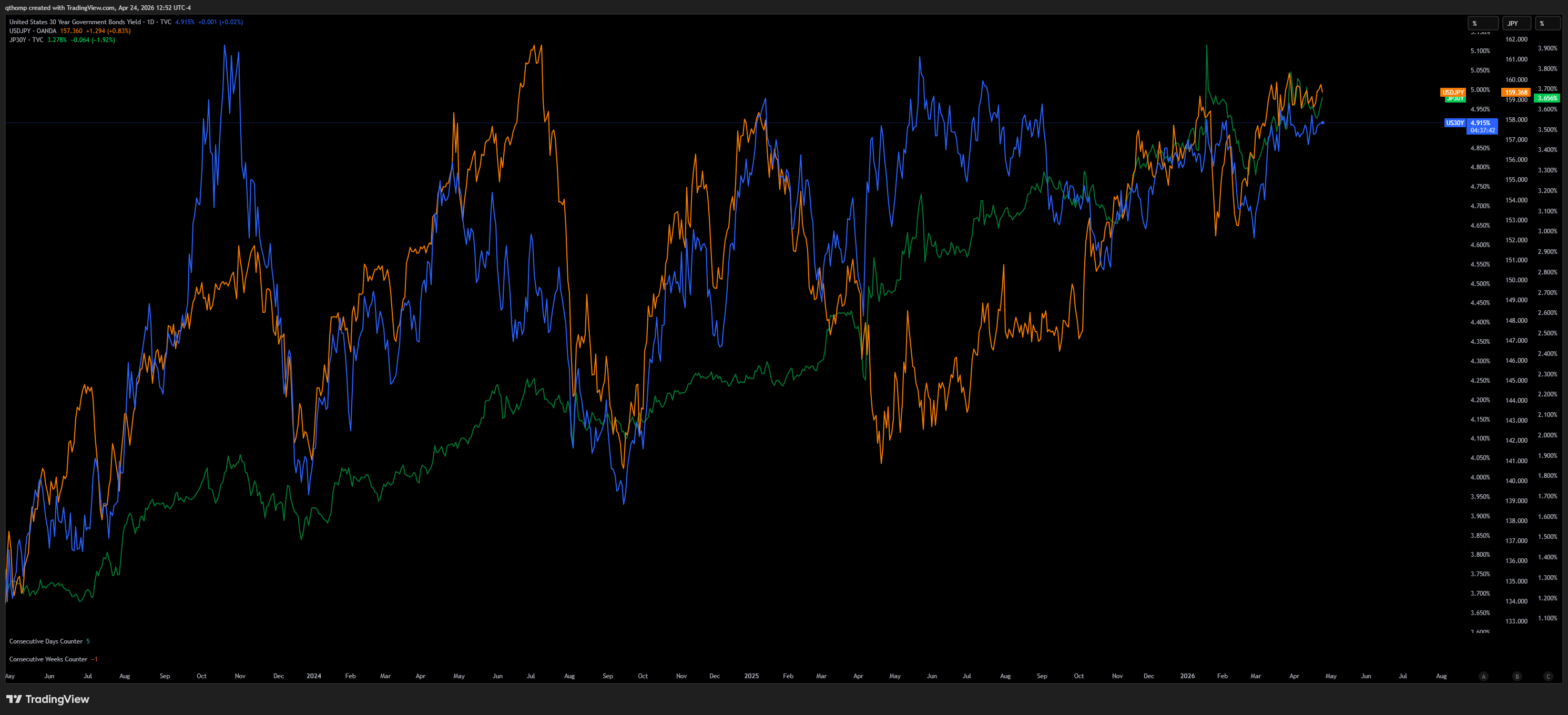

The Japanese Yen has been on a multi-year weakening trajectory that has also coincided with rising JGB bond yields. The read through is that monetary policy is too loose relative to growth and inflation and thus both their currency and bond market are losing value at the same time.

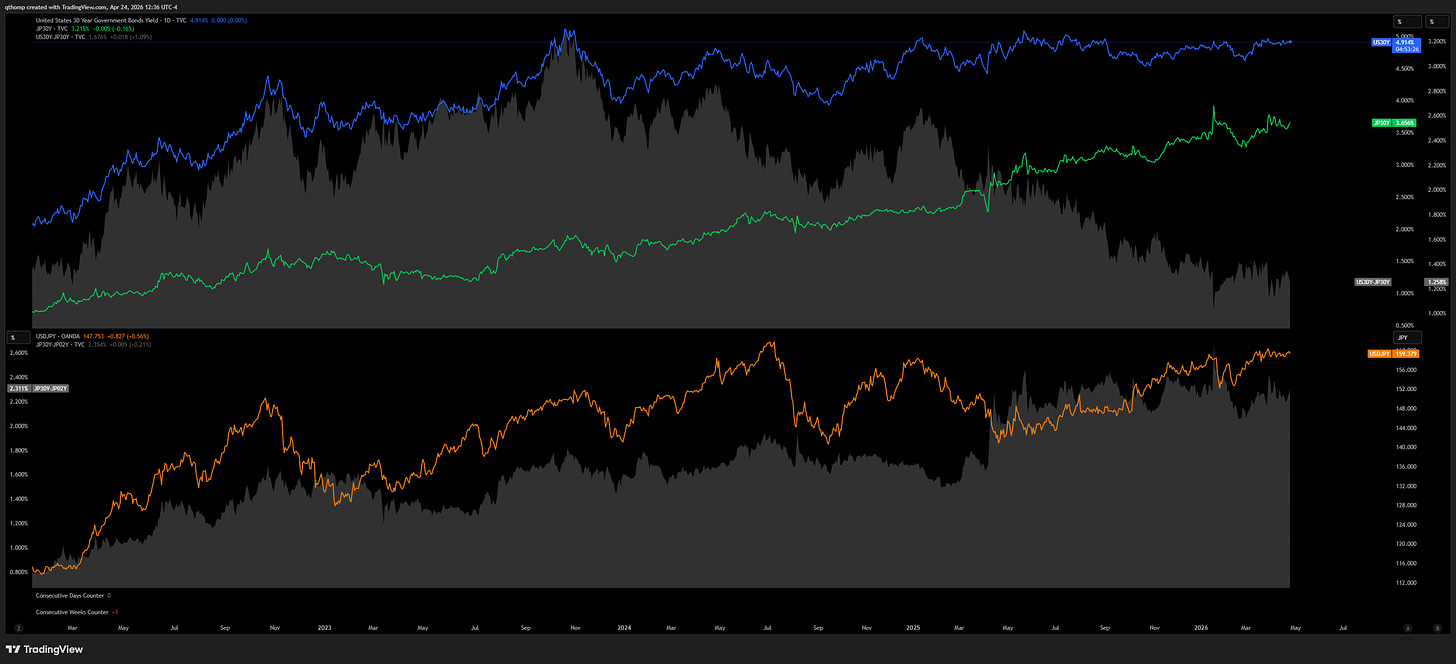

This idea can also be viewed through the lens of yield differentials. The relationship between Japan’s bond yield differentials with other developed markets and relative currency performance significantly shifted around Liberation Day in April 2025. Instead of seeing a strengthening Yen when yield differentials have moved in its favor (higher Japanese bond yields relative to other developed markets), the Yen has weakened relative to the Dollar and Euro. So either, US and Europe are both suppressing their bond yields relative to Japan while keeping their currencies strong (doesn’t make sense because if they were to be doing the former, the latter wouldn’t occur). Or, the Yen is saying that Japanese monetary policy is still too loose and their currency is depreciating against the US and Europe while their bond yields rise more relative to the US and Europe’s. Looking at the yield differentials historically, they do not often go much lower from here outside of a crisis.

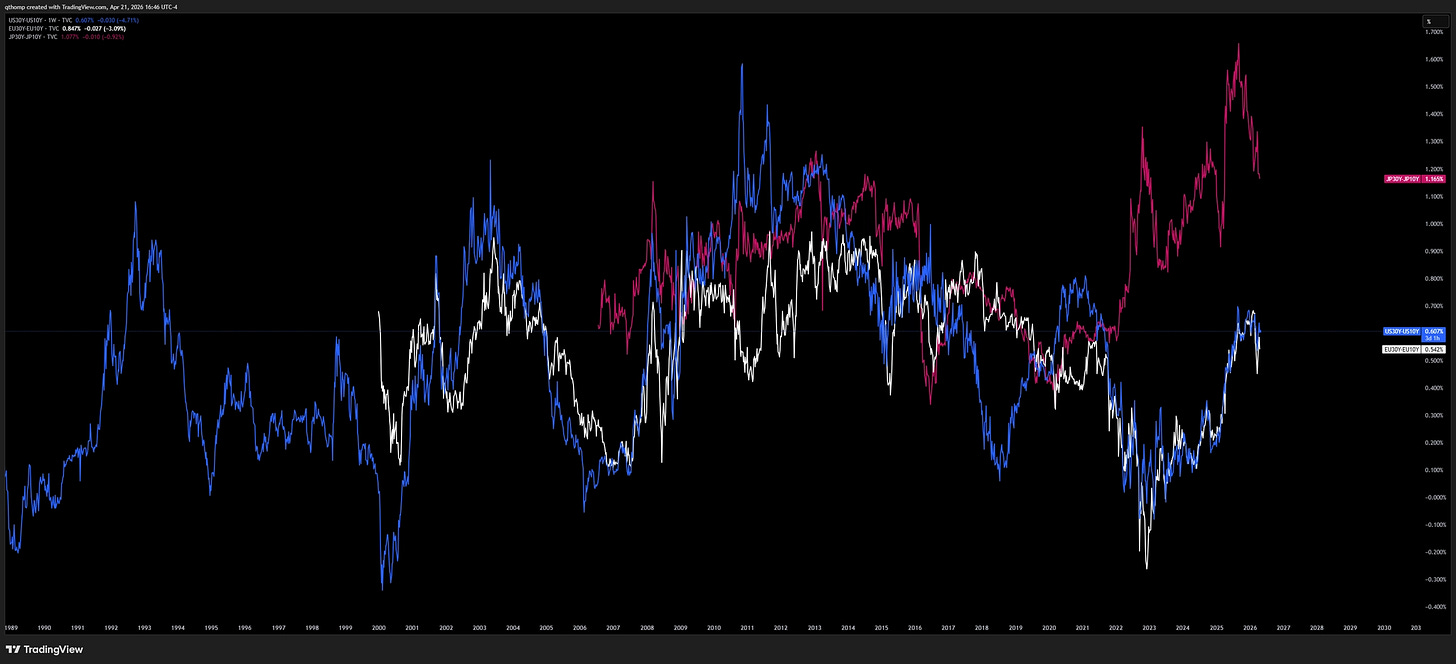

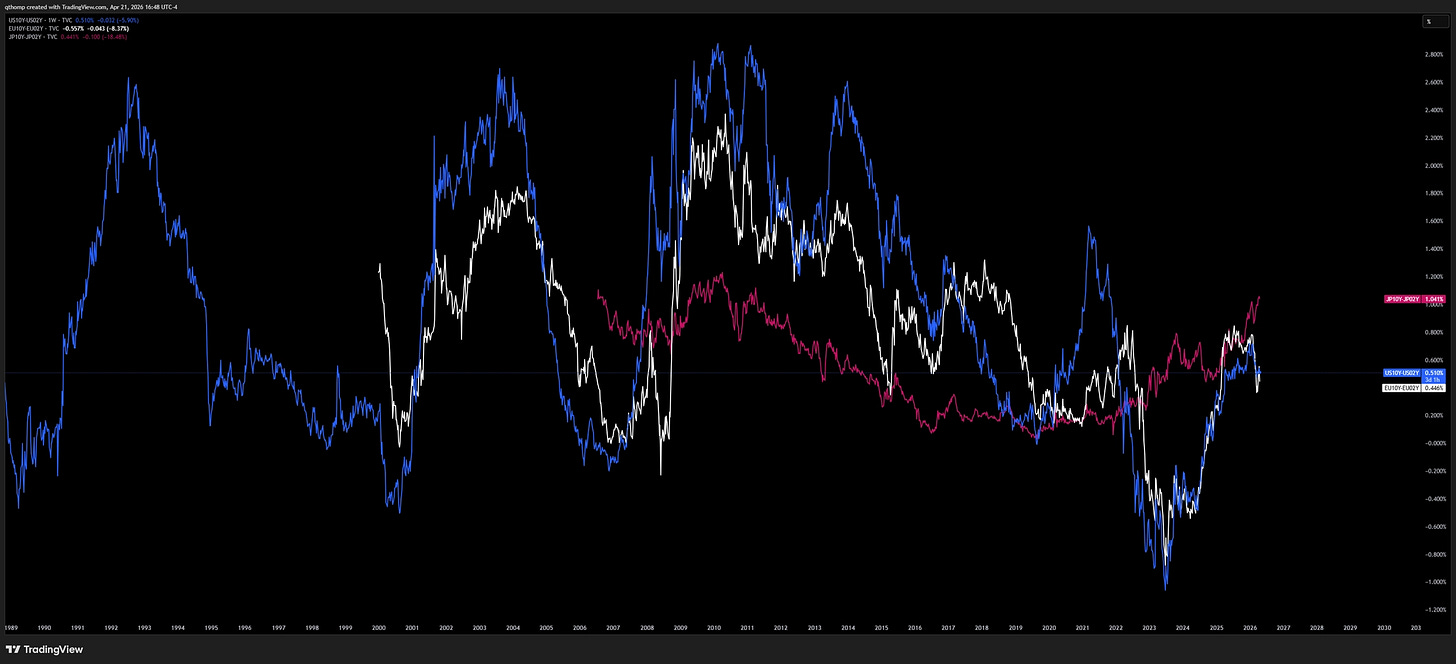

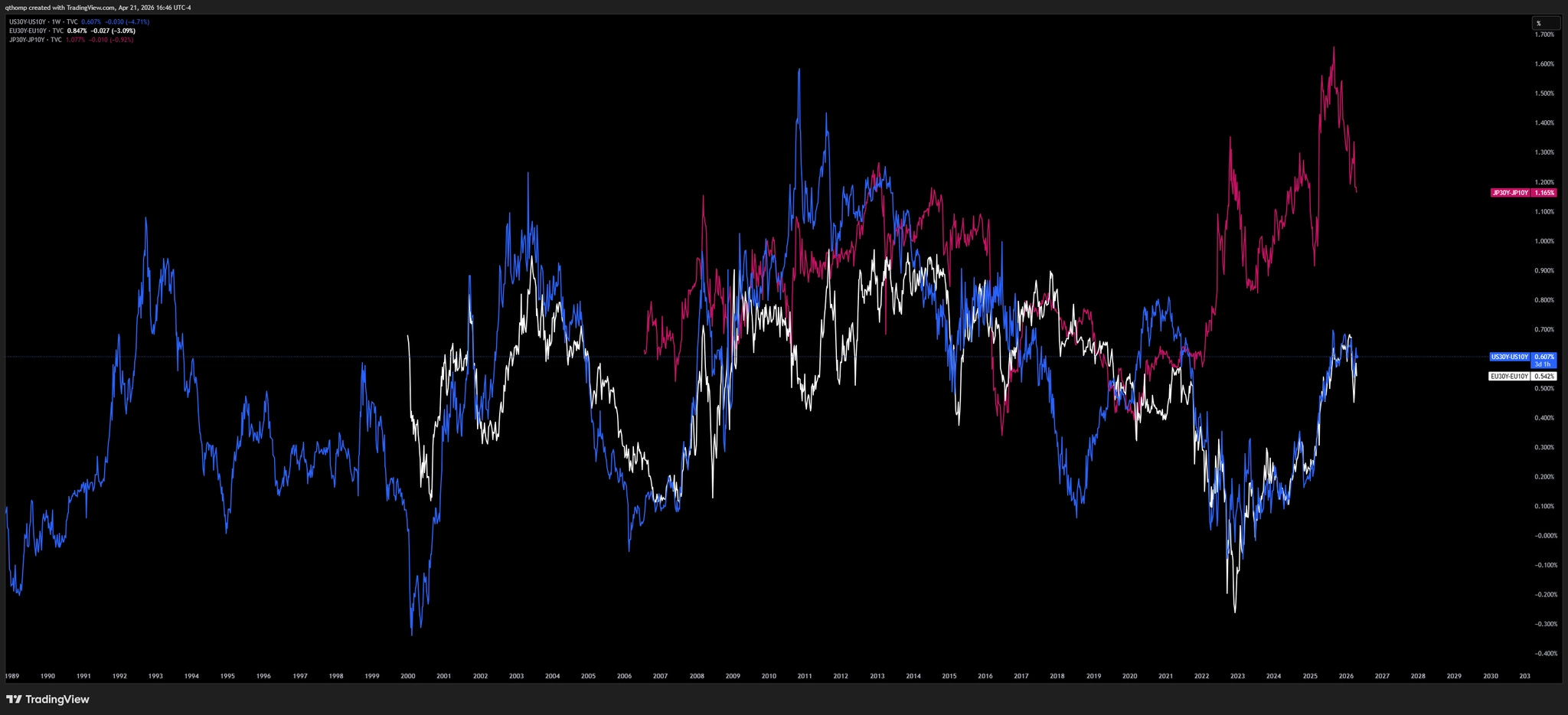

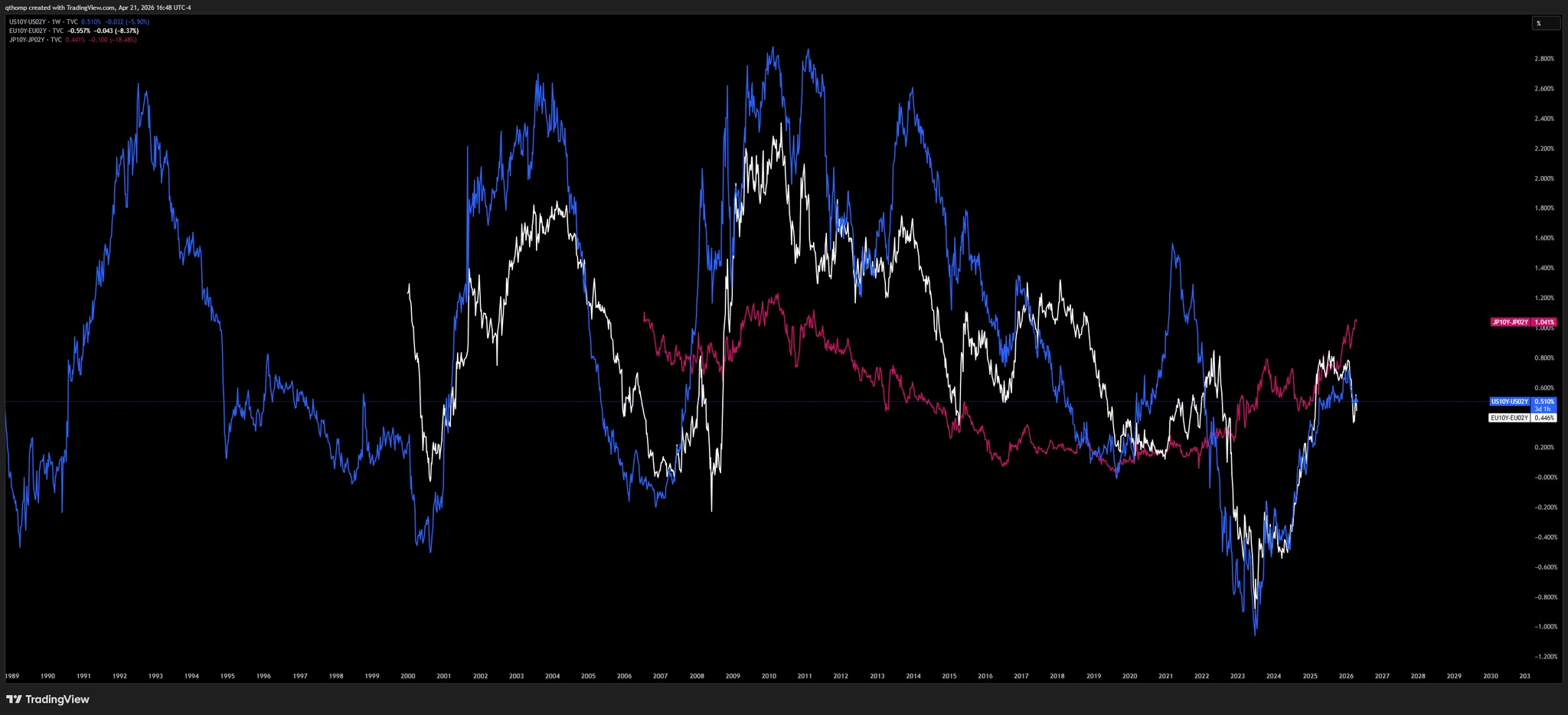

Looking at yield curves across the regions, both the 30s-10s and 10s-2s are much steeper in Japan than in the US and Europe. This further corroborates the idea that Japan’s monetary policy is too loose and investors are becoming increasingly uninterested in long-dated Japanese government debt.

Quantifying Japan’s problems.

Japan’s Debt to GDP ratio is ~230% which dwarfs the US’s at ~125% and the Eurozone average of ~90%. While the US and Europe have high debt levels by historical standards, Japan's debt is a systemic outlier that limits its ability to fight inflation with higher rates. For every 1% increase in interest rates, Japan’s annual interest burden increases by roughly 2.3% of its GDP. For the US, that same 1% hike only costs 1.2% of GDP. Japan is effectively twice as sensitive to interest rate shocks as the US, and even more than that relative to Europe.

The above metric is how much the fiscal side of Japan’s government is borrowing relative to the size of its economy. On the monetary side, Japan’s central bank’s balance sheet is ~100% of the country’s GDP. In Europe, the ECB’s balance sheet is ~40% of Eurozone GDP and in the US, the Fed’s balance sheet is ~20% of US GDP. In other words, the Fed’s footprint is 1/5th the size of the BOJ’s. The BOJ owns more than 50% of the entire JGB bond market which means there is no natural price discovery. When yields rise, the BOJ is effectively allowing it, but as that happens, the value of their own balance sheet is decreasing.

Lastly, Japan also has the most negative real interest rate policy (interest rates minus inflation). BOJ’s policy rate is currently set at ~0.75%, ECB’s at ~2.0% and the Fed’s at 3.6%.

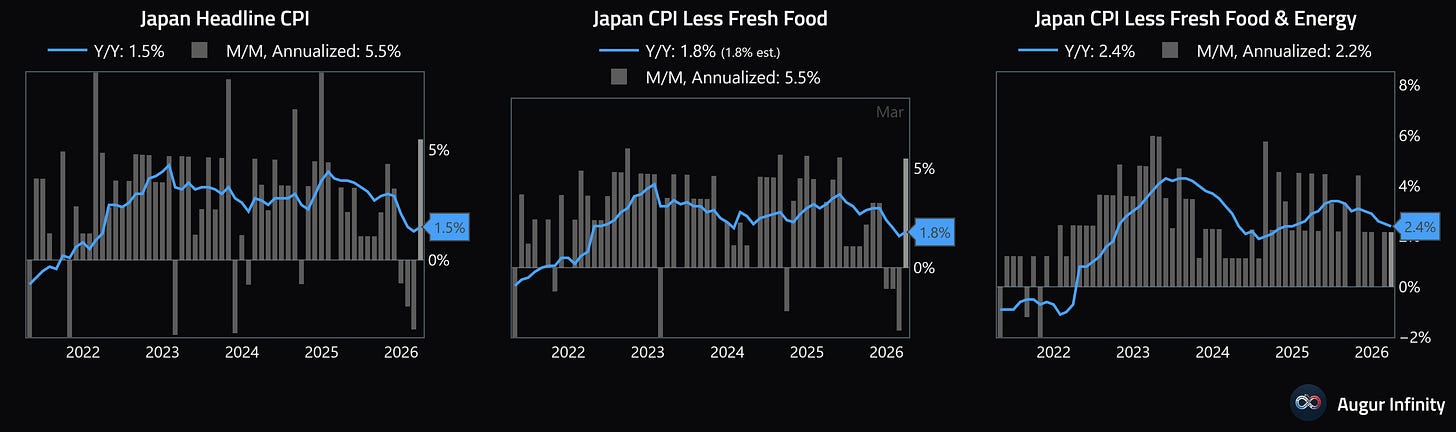

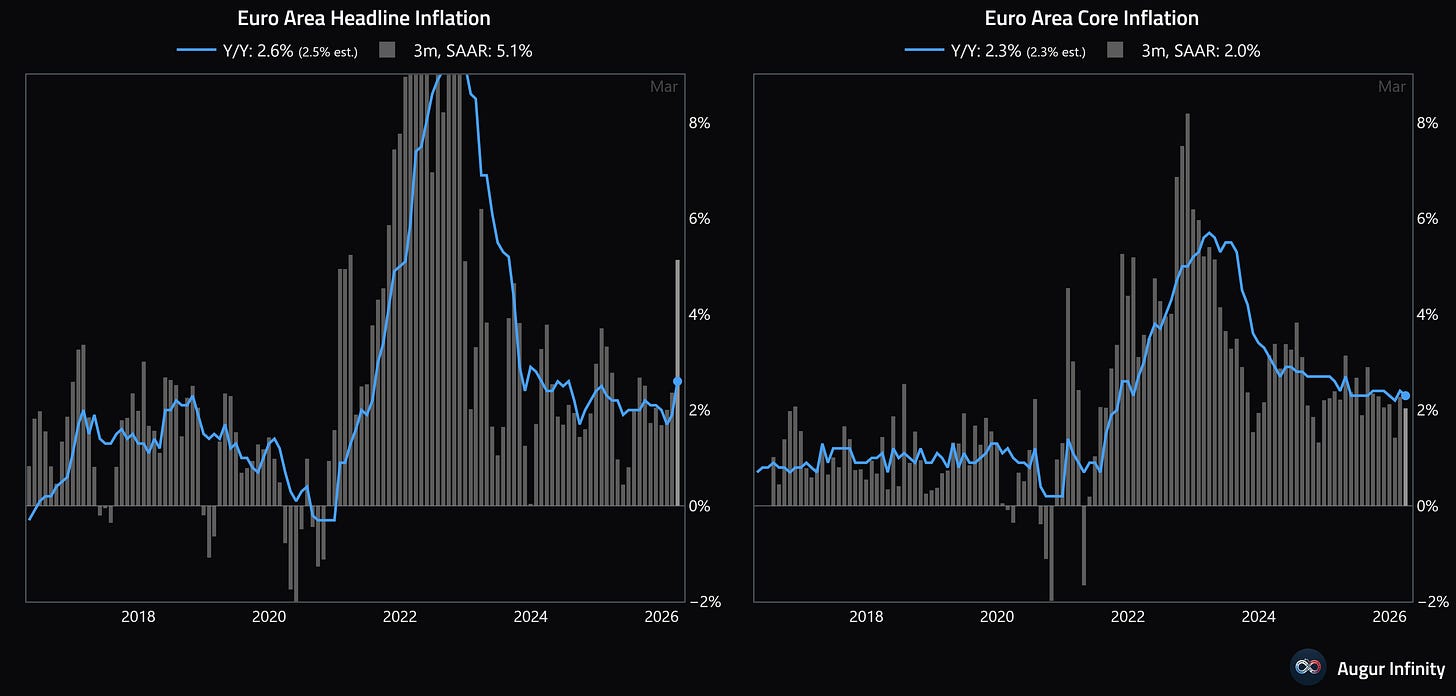

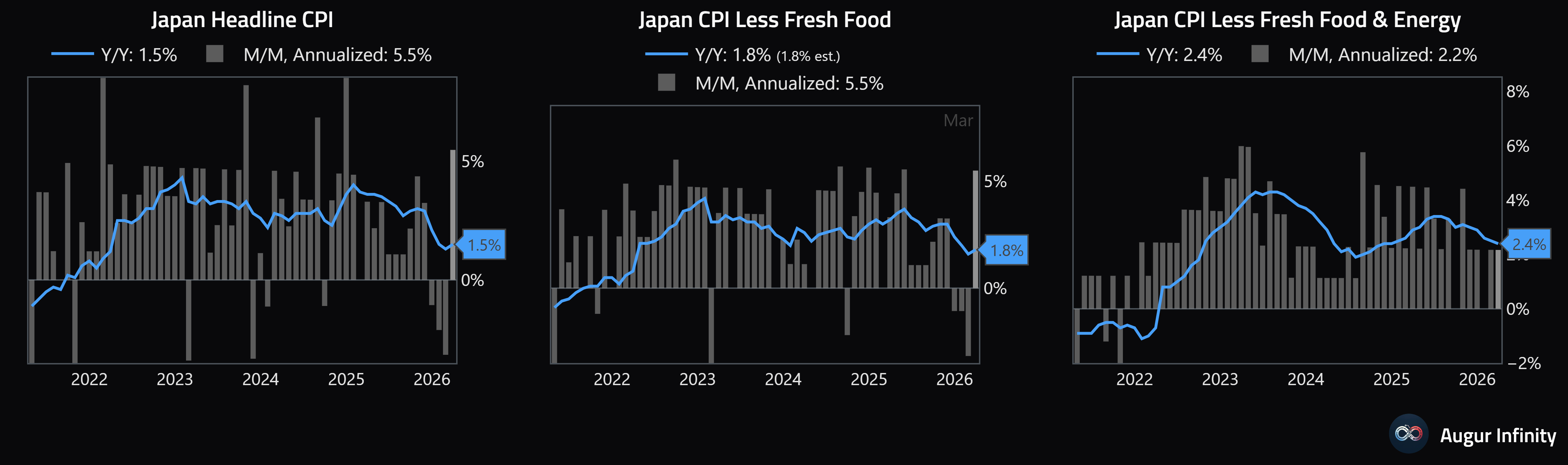

Looking at the inflation picture a bit closer (the second half of real interest rates). Prior to the Iran War, inflation in Japan and Europe actually appeared to be in a better position than in the US with core running in the 2-2.5% YoY area while core in the US has been stuck in the 2.75-3% YoY range. Despite better relative inflation, that still puts real rates in Japan at ~-1%, Europe ~0% and the US ~+0.75%. Given the Strait of Hormuz closure and ensuing commodity supply chain issues, we have gotten March’s inflation data that is showing a severe impact to headline inflation and a larger relative increase to Europe and Japan given their reliance on imported energy.

In summary, Japan is in a difficult and much more trapped situation than Europe and the US. The Japanese government is ~80% more leveraged than the US government and the BOJ has a 5x larger footprint than the Fed relative to its economy. The US and Europe have been able to maintain neutral to positive real rates while Japan has been forced to run deeply negative real rates. The Yen is devaluing despite rising yields because the market sees that Japan cannot afford to increase interest rates without triggering a fiscal crisis and their currency is the only release valve left.

Policymaker incentives and decision making.

There are a few elements at play here - there are the mechanics around the optically important USDJPY 160 level and then there are the fiscal and monetary policy considerations around the ongoing energy crisis.

The 160 level has been clearly defended by US and BOJ policymakers over the last few years.

Japan is highly susceptible to inflation due to its food and energy import dependence. Japan imports ~60% of its food on a caloric basis (>90% of soybeans, corn and wheat) and ~90% of its energy supply (oil, LNG and coal). The Eurozone is in a better position as they are a net food exporter and import only ~50% of their energy supply, but have less of a physical reliance on the Strait of Hormuz and larger renewable wind and solar buffer.

The commodity supply shock puts global central banks in a difficult position. They know their monetary policy tools cannot address the root of the crisis and their natural inclination is to do nothing as a result. They see the inflation pressures but fear a tightening monetary response risks adding insult to the injury that is already being caused to consumer demand destruction and the negative effects that would have on the economy and growth. On the other hand, allowing policy to run too loose introduces risks that their monetary stance adds fuel to the inflation fire, can lead to a weaker currency and potentially exacerbate the energy price shock.

It is my observation that global central banks like to move in unison and operate with a high degree of groupthink. After all, the rising sovereign debt problems are a global phenomenon and have been shown to require tight coordination amongst policymakers in order to suppress volatility and cooperatively manage the global FX and bond markets.

It’s not a great situation either way. For Japan, if they allow USDJPY > 160, bond yields may start moving more aggressively higher and the risks of an inflation problem increase. Given Japan owns ~50% of their sovereign bond market, that seems like an easier market to manipulate than the flows of the global FX market.

For the US, USDJPY > 160 means the carry trade lives on. There would be risk of bond market spillover into the US from JGB yield contagion, but Bessent and his predecessor Yellen have shown their appetite to use all available tools to suppress bond yields via ATI and YCC. The downside to USDJPY >160 is a strong dollar and the negative effects that could have on risk assets. The alternative where USDJPY 160 is heavily defended and swatted down has historically not bode well for US tech equities, which we know is a priority of this administration, particularly during an election year.

All in all, policymakers number one goal is to reduce volatility. Given USDJPY is a systemically important funding pair, low volatility is key as carry trades don’t do well with volatility. They also must have an eye on inflation because over time it tends to increase bond and currency market volatility.

What I am gathering thus far, is that Bessent and co are throwing the kitchen sink at the dollar to keep it down. It has been trading in a structurally damaged way since Q1 2025 and is key to keeping financial conditions loose when the Fed is trapped and cannot loosen policy due to too high inflation. In addition to YCC and ATI, this is yet another way the Treasury market has coopted policy away from the Fed. This works in the short-term as you can see via stock prices. The flip side to this, however, is the bottling up and accumulation of inflation risks due to too loose financial conditions. By suppressing the dollar and bond yields, you bolster financial markets and economic activity at the risk of reigniting another inflation problem. Notice inflation bottomed post Liberation Day last year and is once again reaccelerating.

The lid on US bond yields is becoming increasingly difficult to hold. Yield differentials are falling, meaning global sovereign bond markets are becoming more attractive on a relative basis, inflation pressures are mounting and the economy is reheating. This is the big picture and the chart I think is not getting enough attention.

I believe oil and commodity problems are here to stay which puts continued pressure on USDJPY. The BOJ and ECB are unlikely to hike into energy crises at risk of exacerbating the demand destruction. Bessent does not want to kill the Nasdaq and prefers the carry trade to continue as he likely feels he is better suited to address the US bond market versus the global currency market. For Bessent, it’s not just a USDJPY issue, its a USD vs everything issue and the flows there are just too big to stop. The same likely holds for BOJ as they own ~50% of their bond market and can control that much easier than they can control global currency flows. Since the US dollar became a petrocurrency in the late teens, its relationship to energy crises has flipped as seen in 2022 (stronger dollar). In addition to Bessent not wanting to swat USDJPY to avoid a Nasdaq problem, he also doesn’t want too weak of a dollar that risks a domestic inflation problem during a midterm election year that is already shaping up to be an uphill battle for Republicans.

I think policymakers can defend the 160 level (would be ignorant for one to believe they can’t, at least in the short-term). However, their will and incentive to do so must be evaluated.

Japan’s bond market is largely government owned - the BOJ owns 50% of their government’s outstanding bonds. It’s not the same ubiquitous safe haven / SoV holding that USTs are.

Hiking rates or turning hawkish certainly doesn’t fix the root of the problem (energy supply crisis) and it might make matters worse domestically (cause a stock market decline that hurts people’s savings and creates negative wealth effect).

The problems are widespread and not just confined to Japan. Indonesia, India and many others in Asia (and to lesser extent in Europe) are seeing their currencies start to depreciate more meaningfully against the dollar. How much Bessent and US a) want to help when the problem is out of their hands due to oil, b) can help when the problem is so widespread across all currencies and c) are incentivized to help when if they do via unilateral dollar weakening will stir domestic inflation problems that we know are politically unfathomable long-term.

If I were a betting man, they continue to suppress volatility and let USDJPY slowly drift up while working to avoid large moves in either direction, both via suppressing bond markets and letting the hidden inflation tax do its work. Eventually though, the markets will catch on, the inflation pressures will become large enough, and the levee will break. Trying to control things you ultimately can’t can succeed in the short-term but it often makes the wildfire worse on the other end, whenever that is.

Letting markets speak.

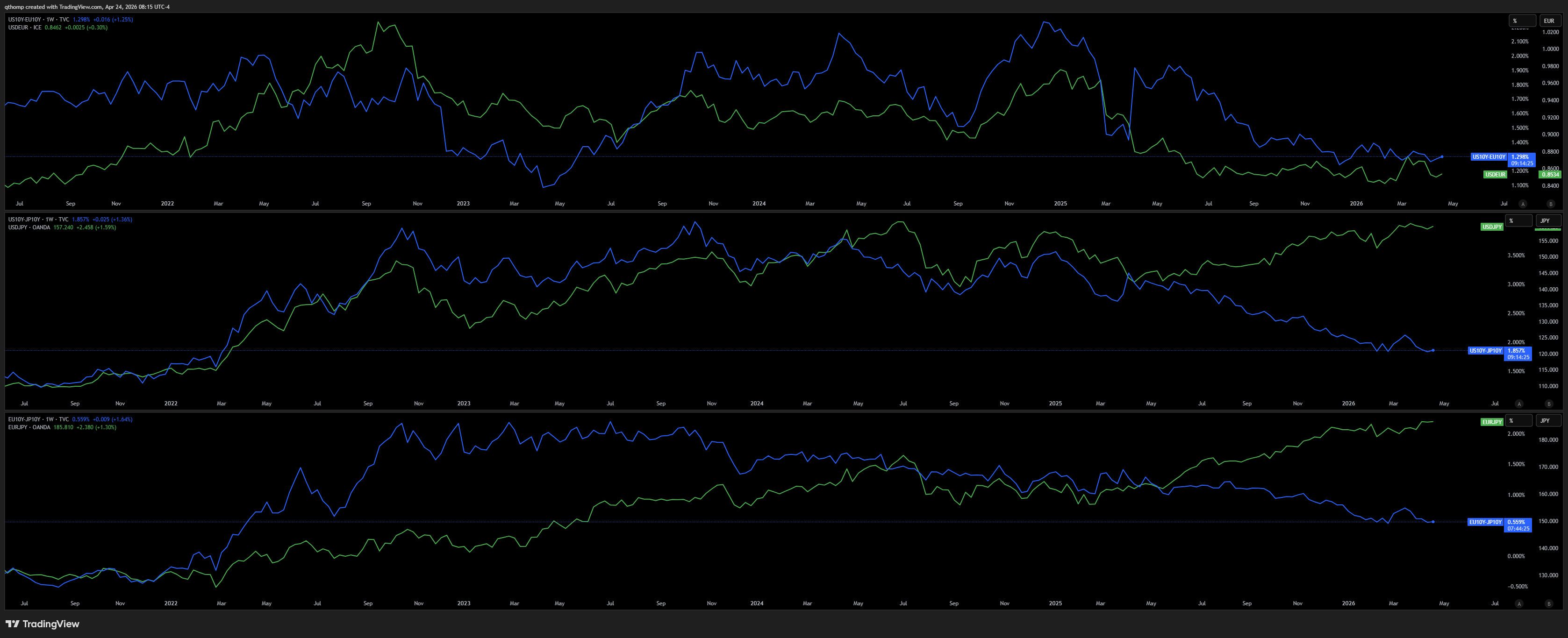

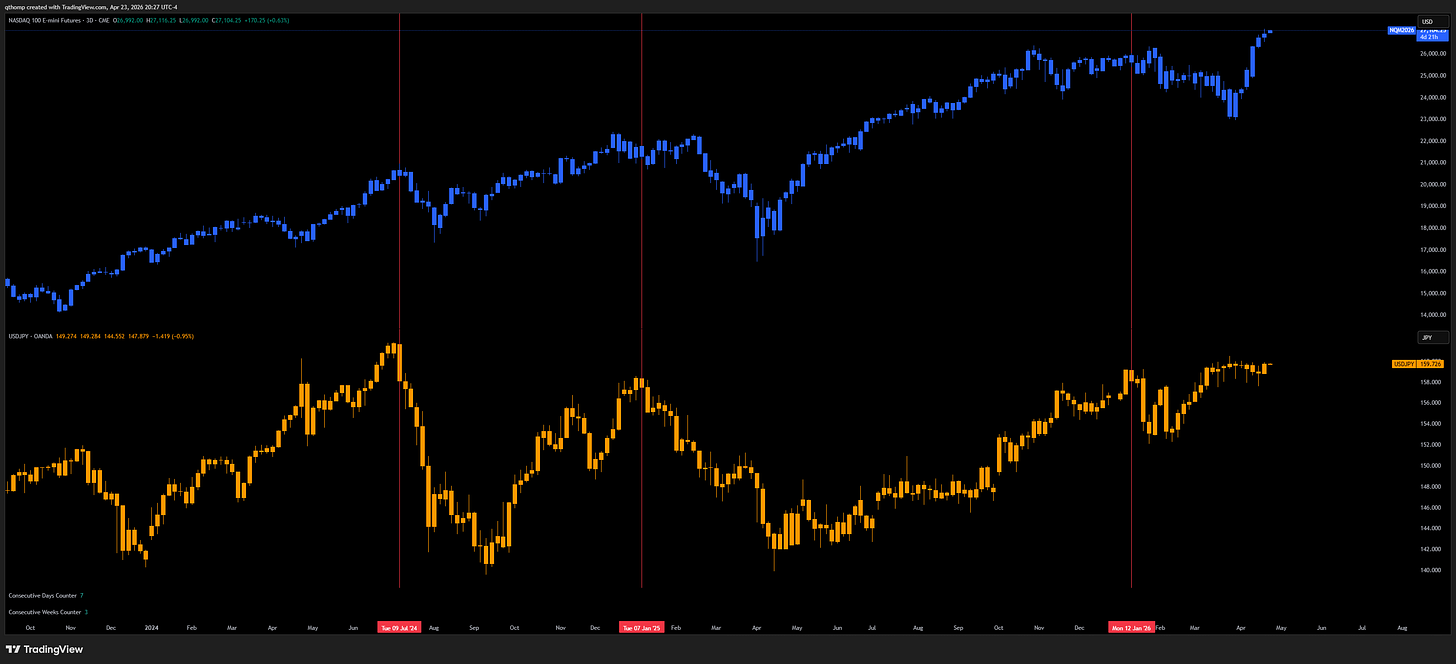

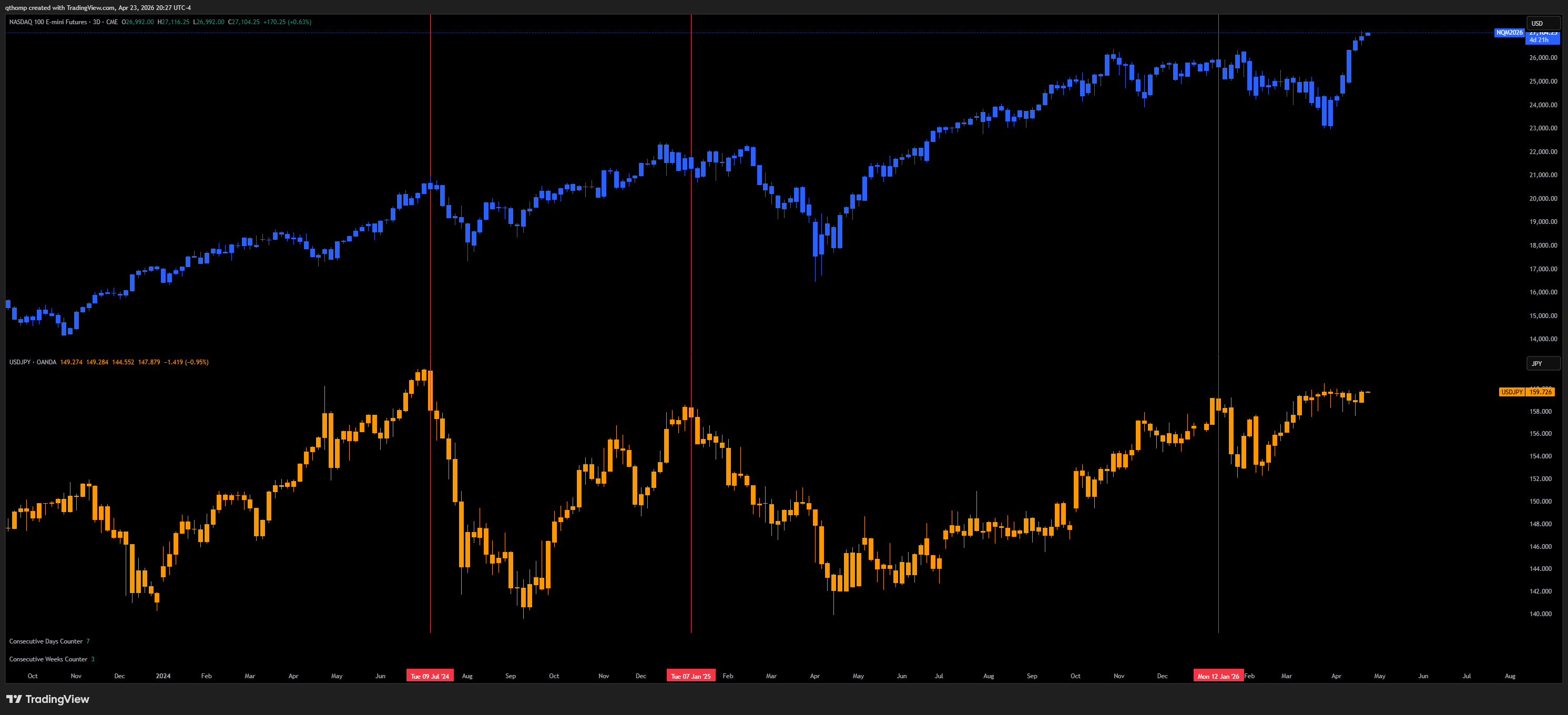

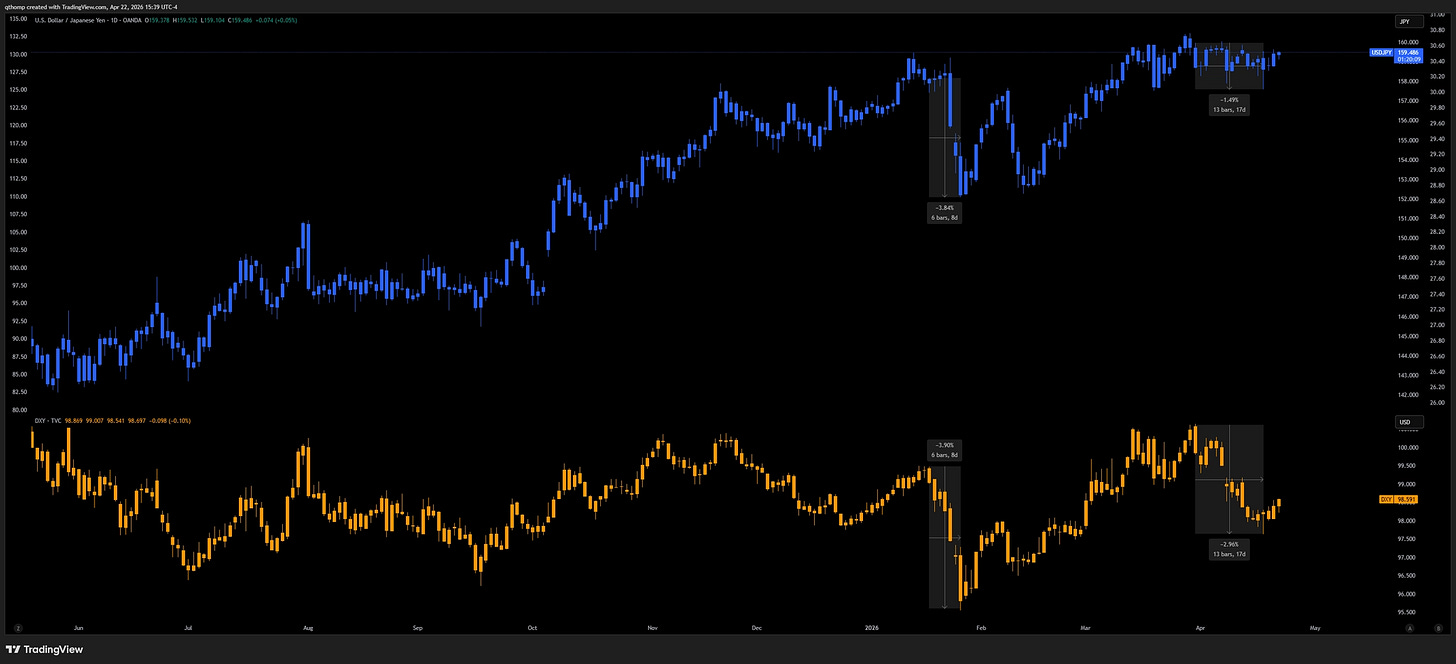

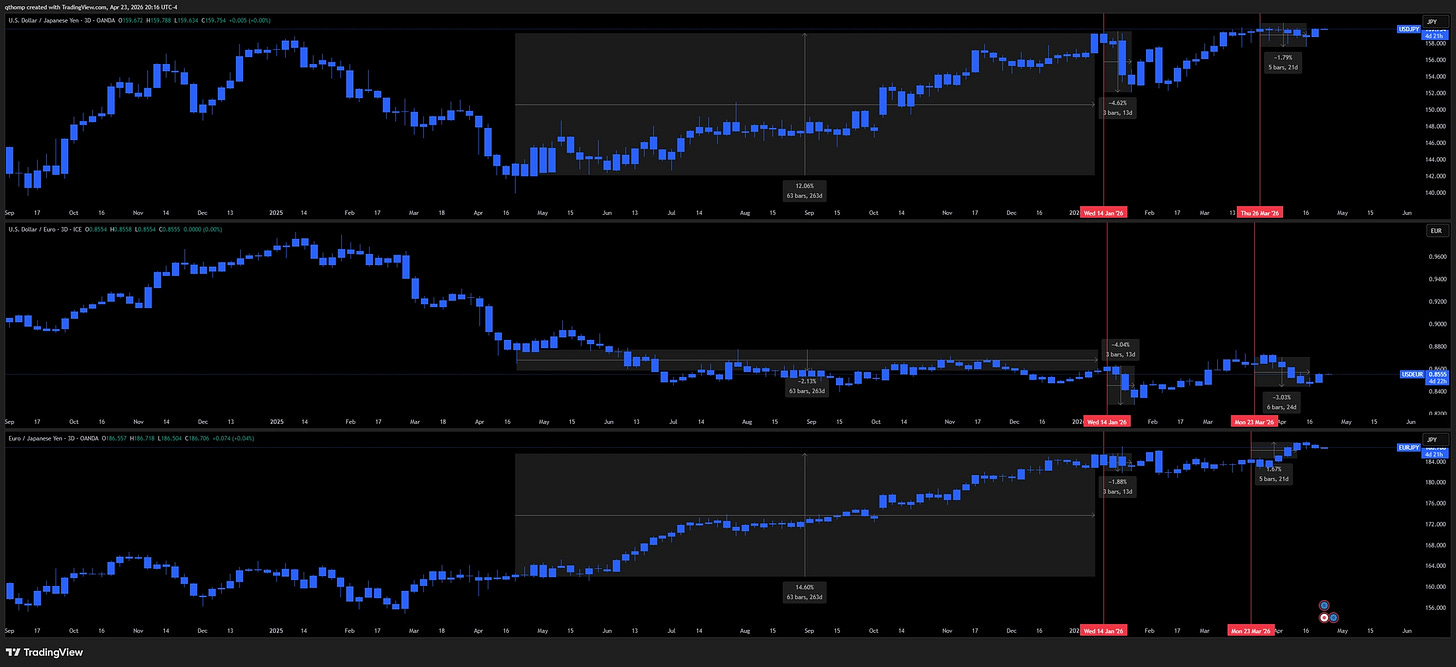

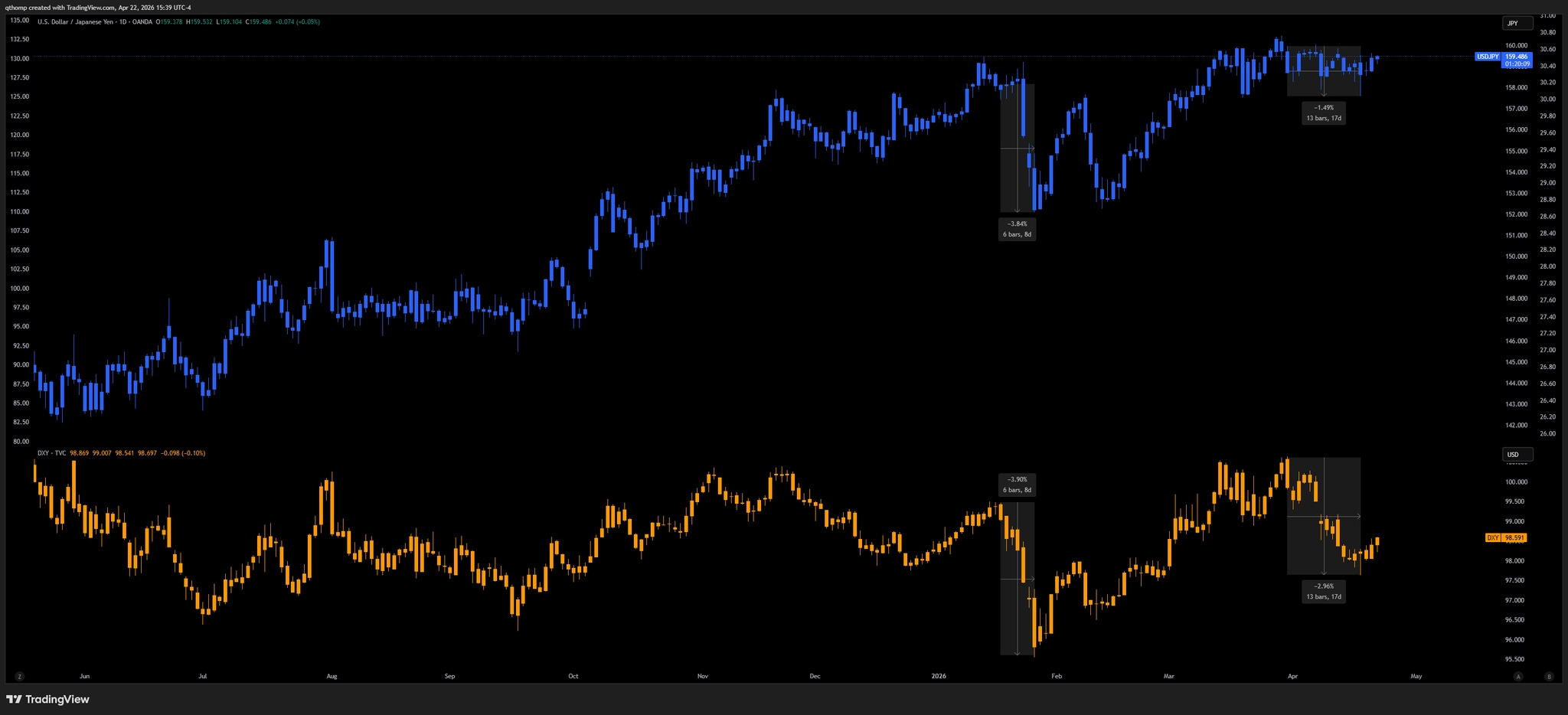

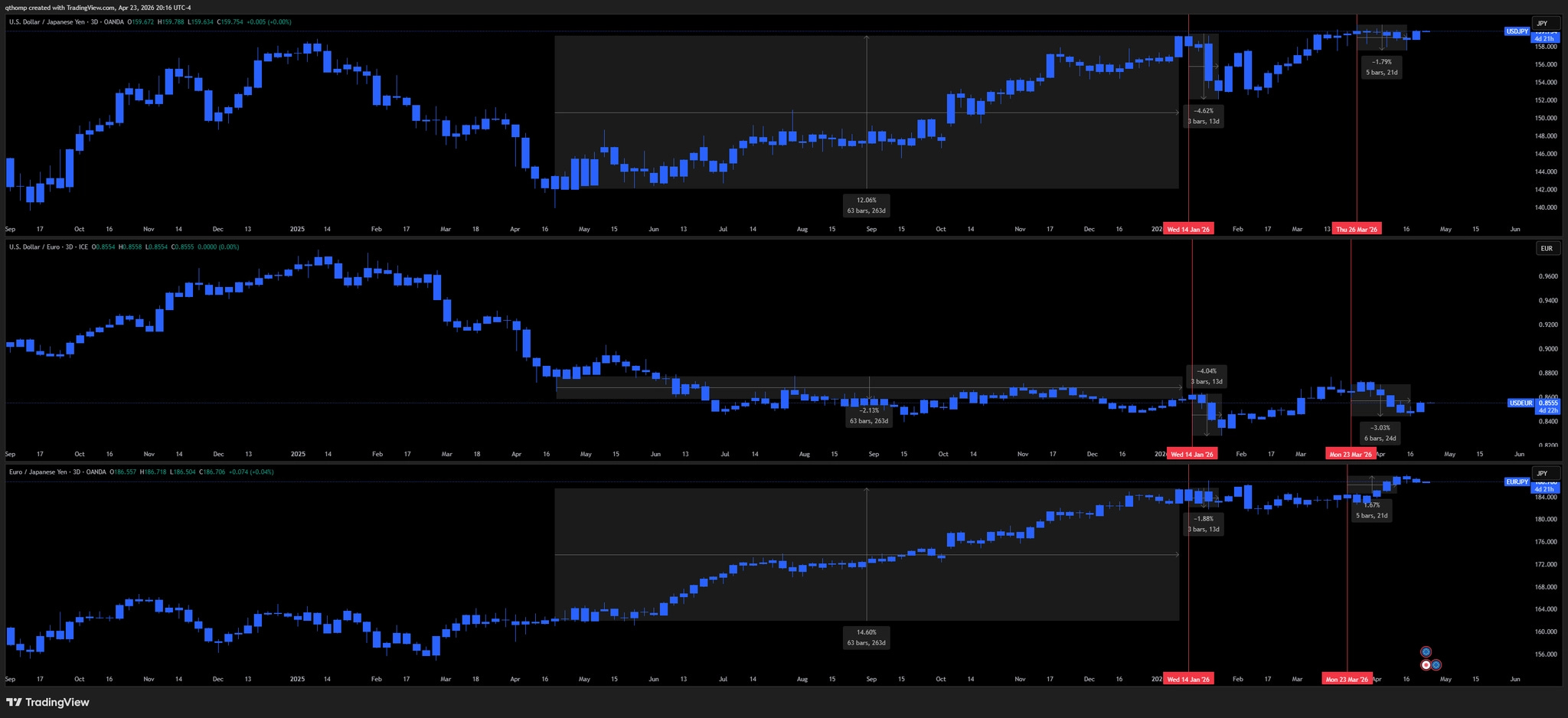

Of late, USDJPY has not moved with DXY as much as before.

Given a large part of the DXY is the EURUSD cross, this shows that the Yen has been trading even weaker to the Euro.

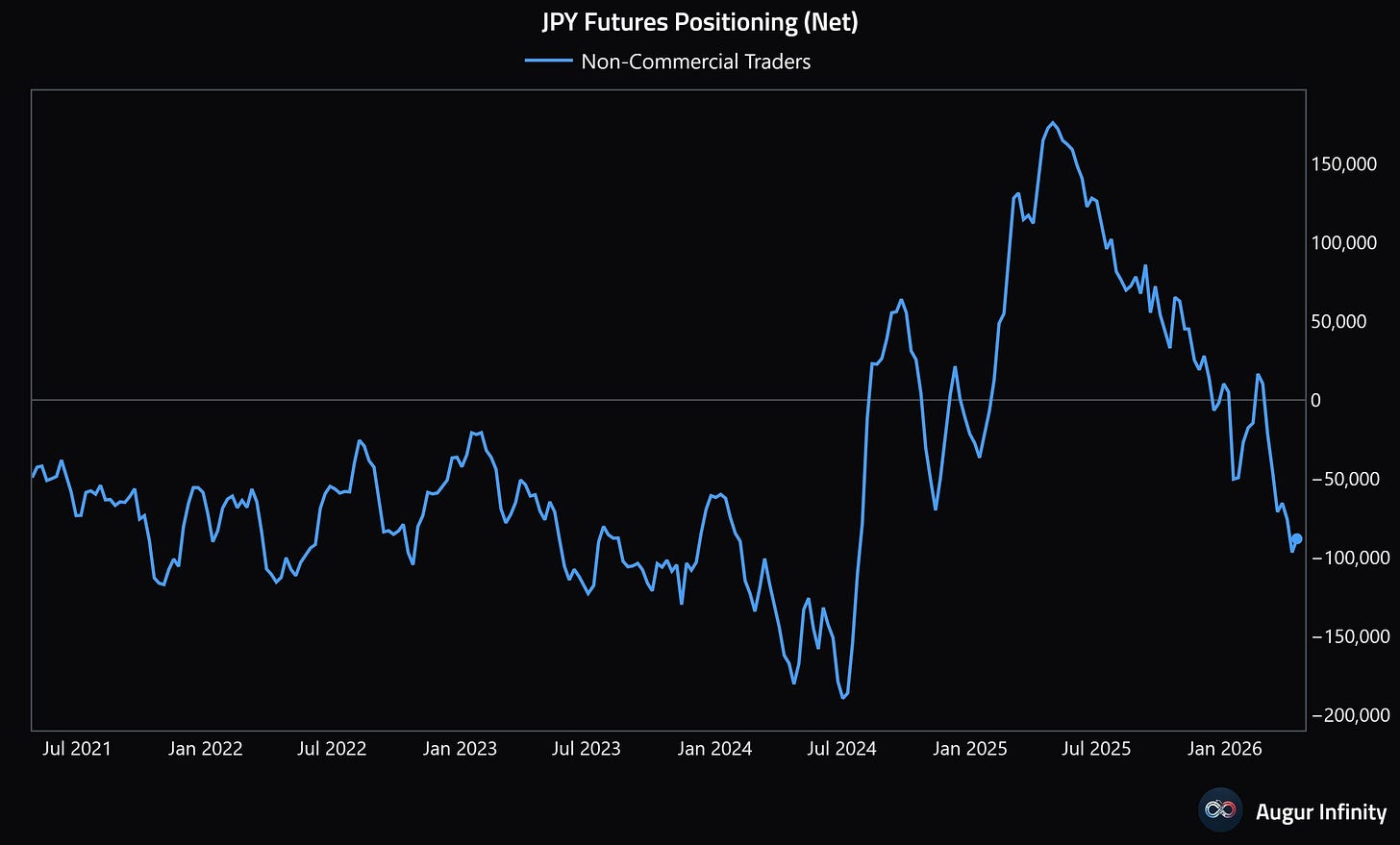

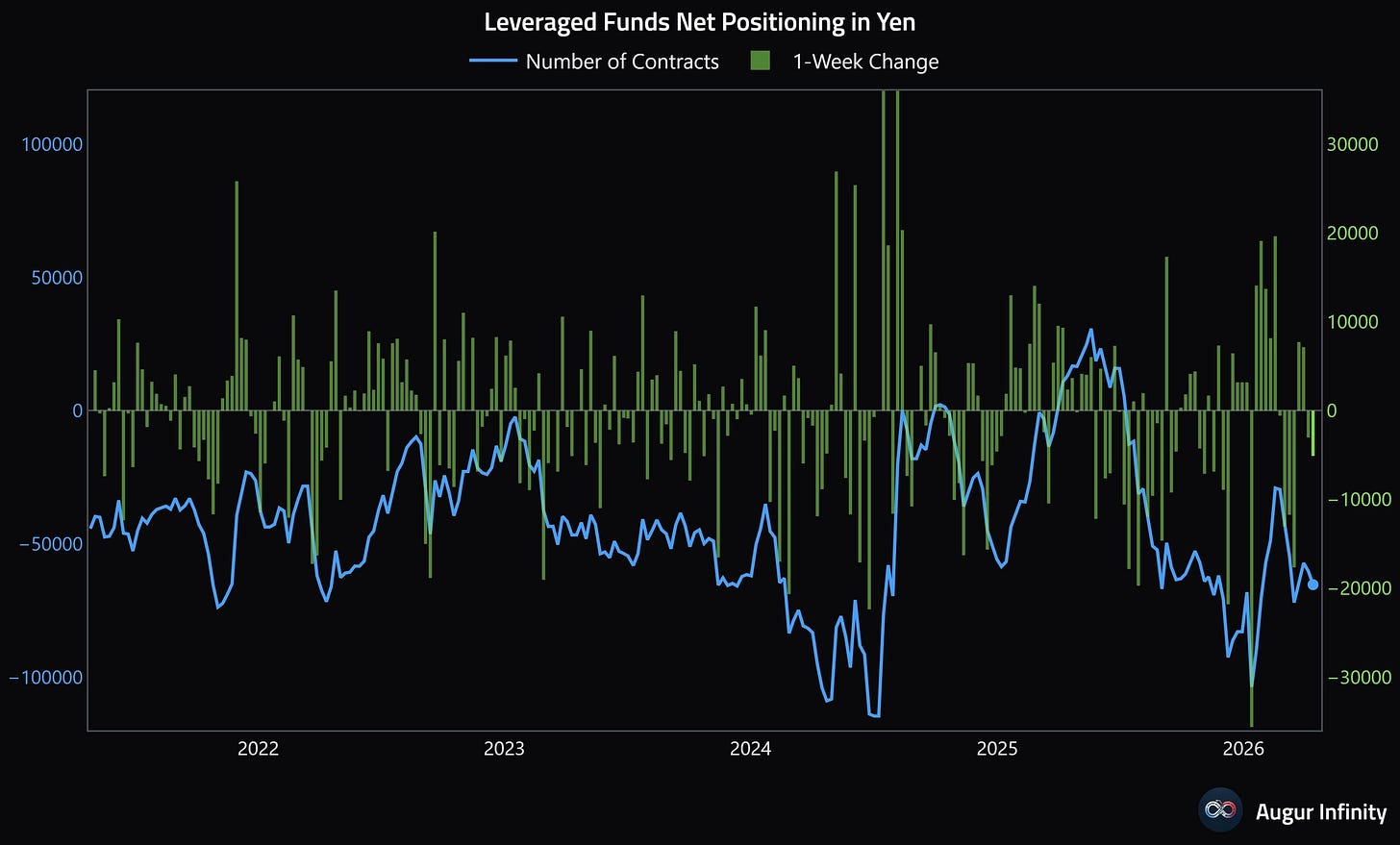

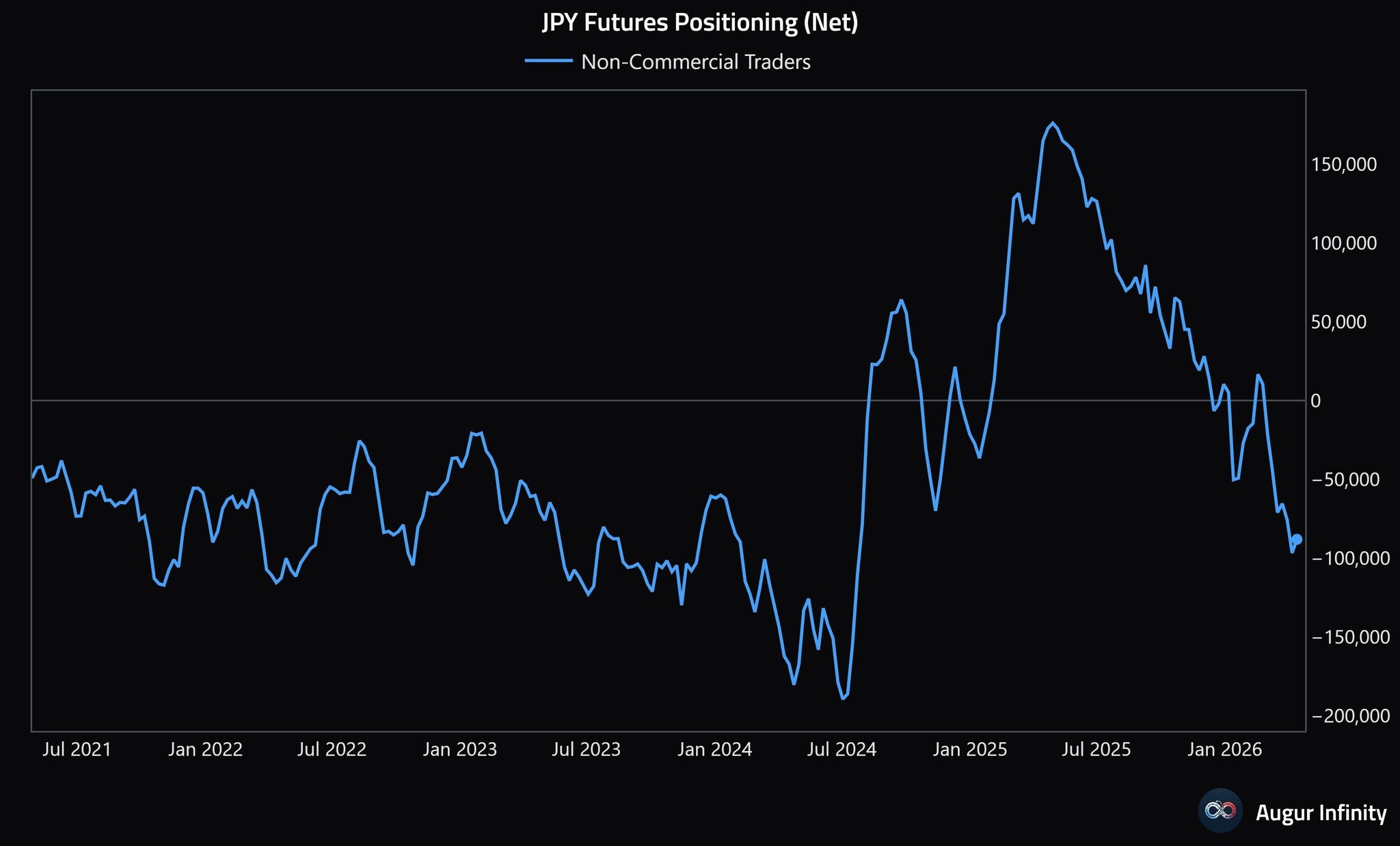

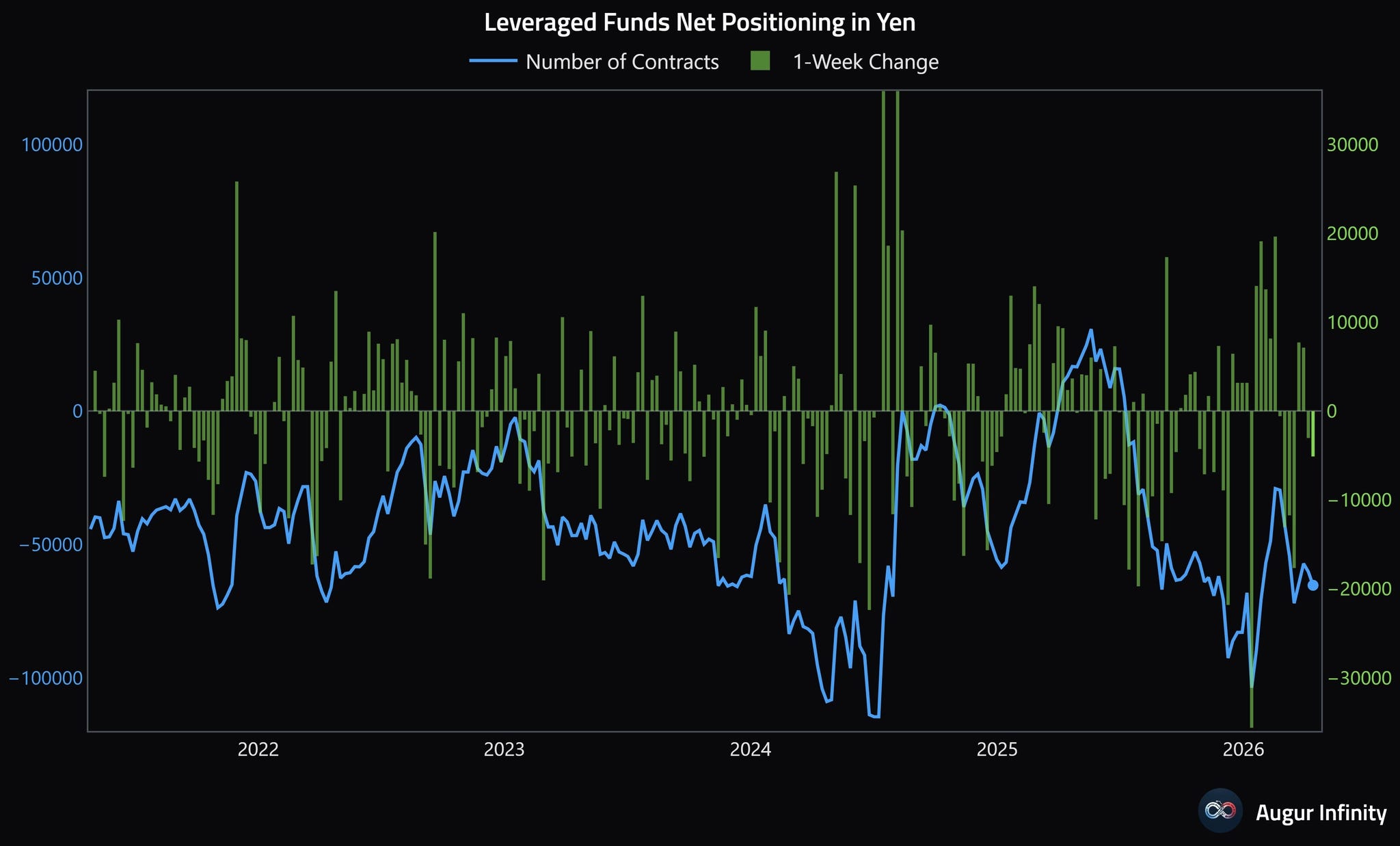

Yen positioning is short, but not particularly extreme in one way or another relative to the last 5 years.

Watching the bond markets will be critical as this is all very intertwined. Will we see an awakening of bond vigilantes?

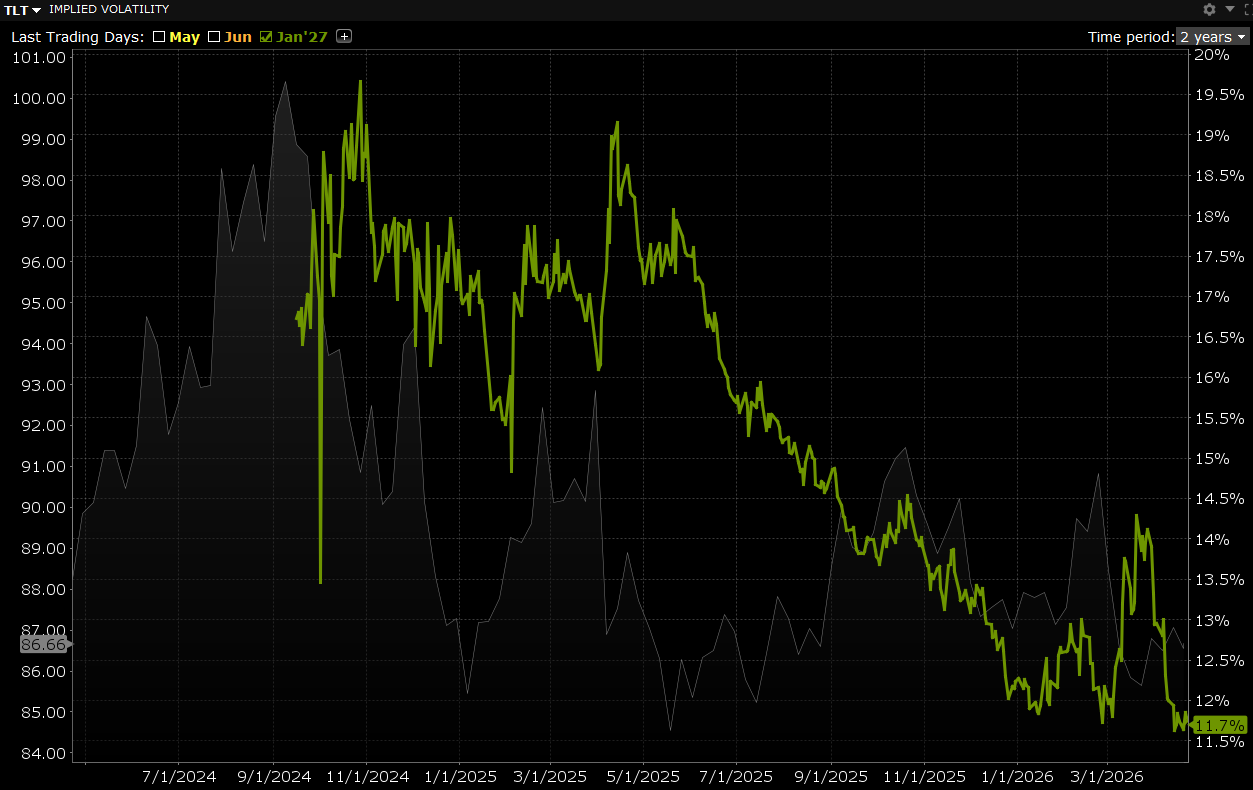

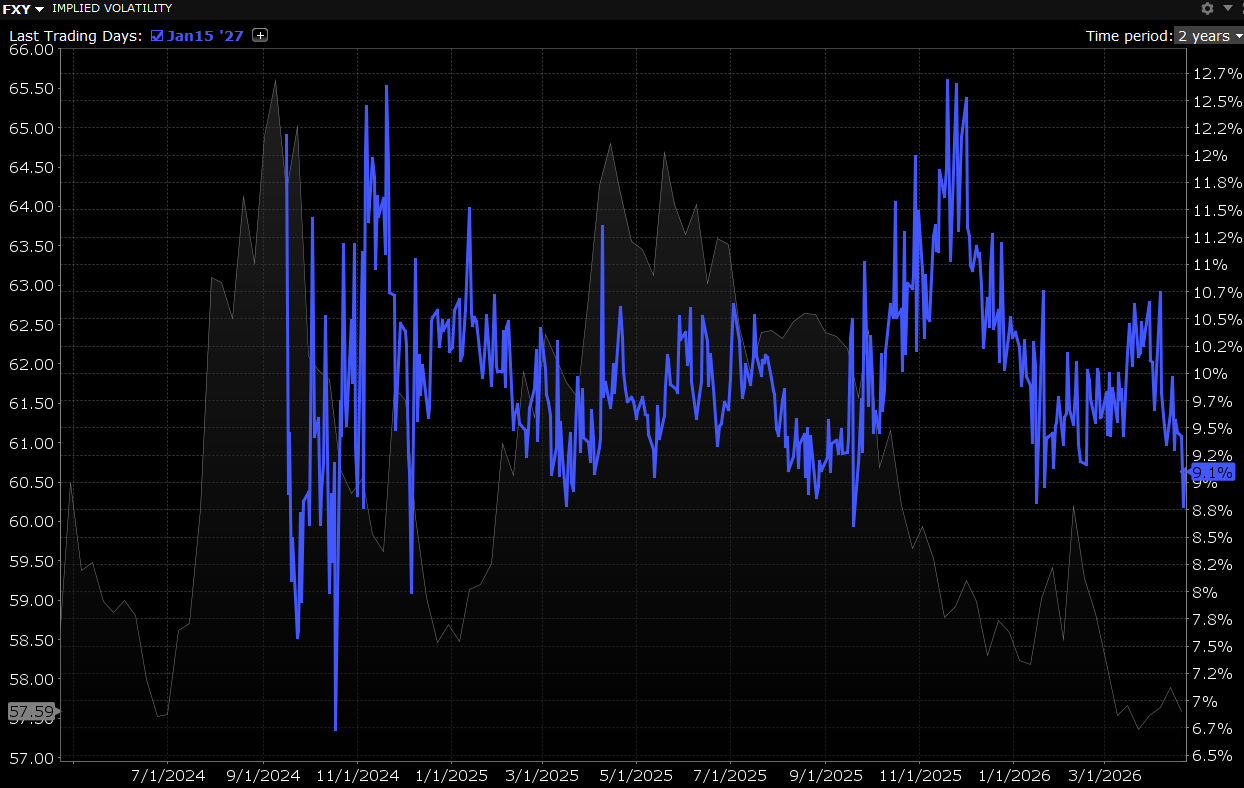

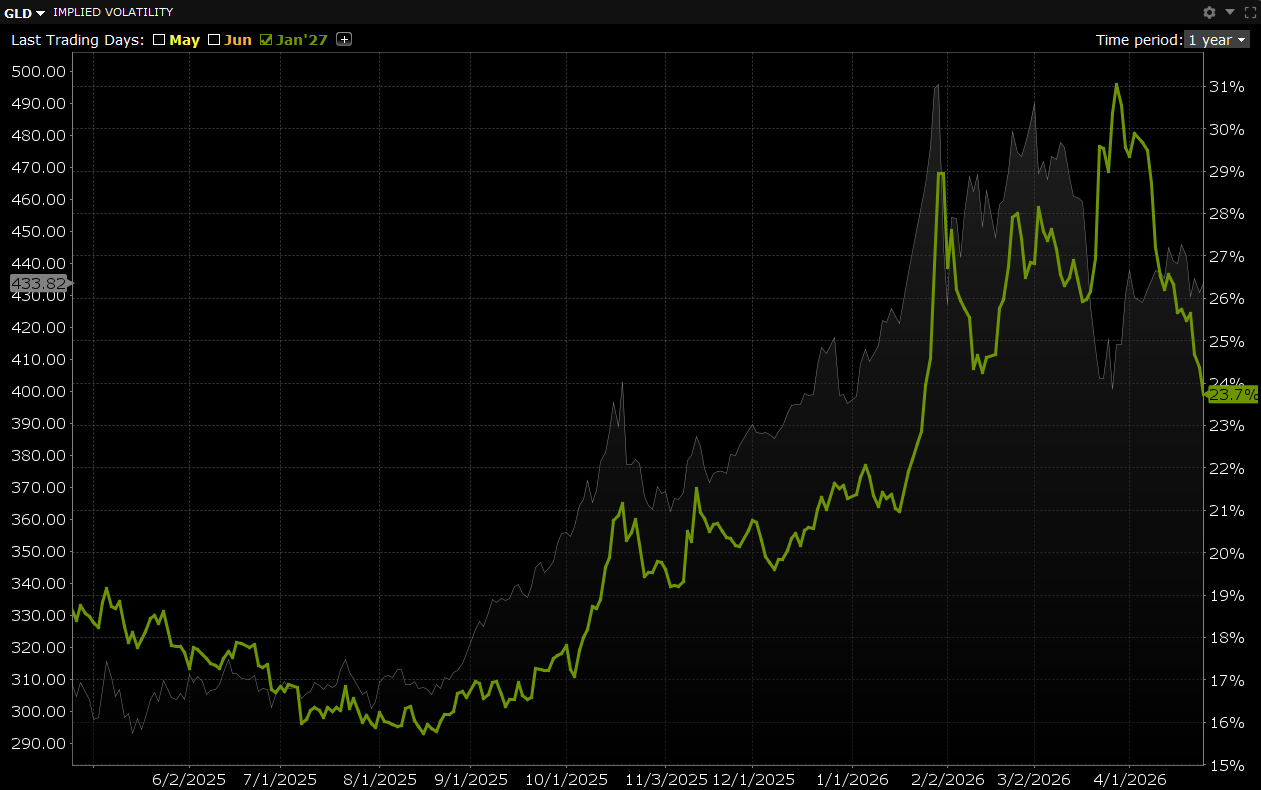

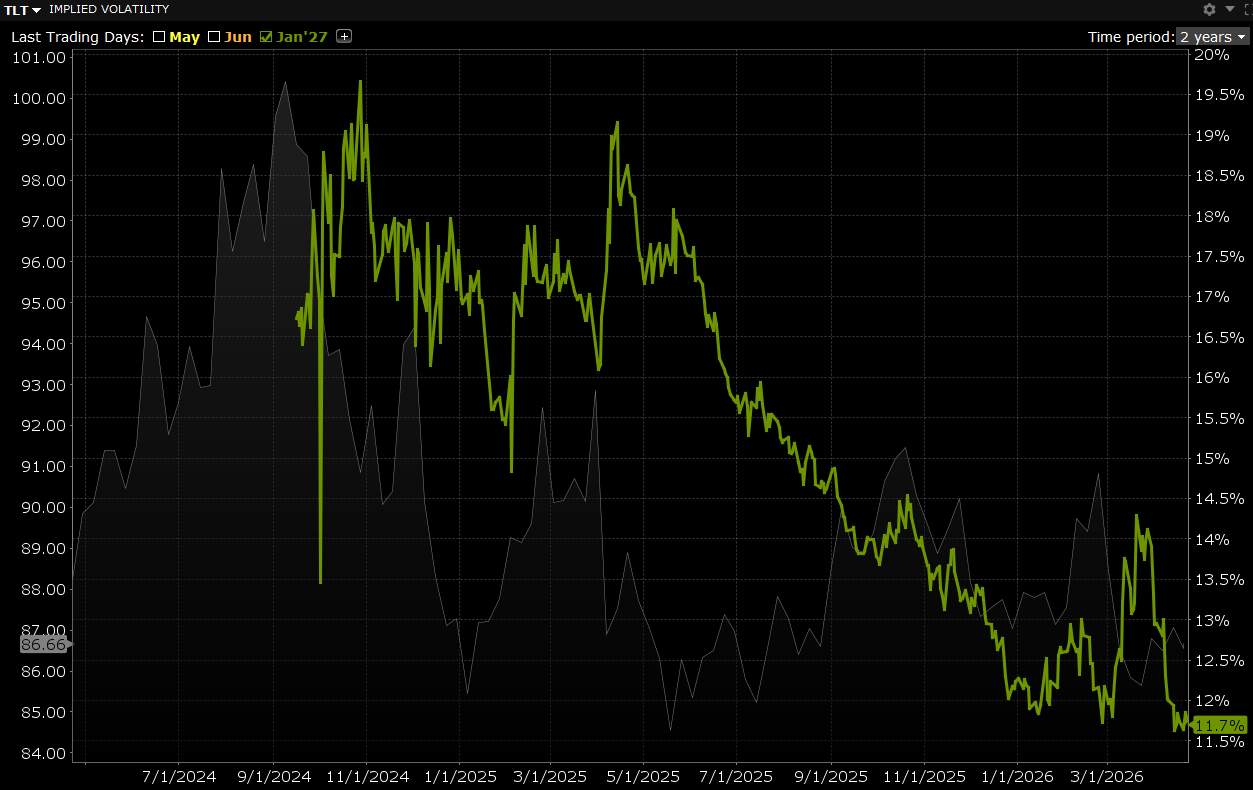

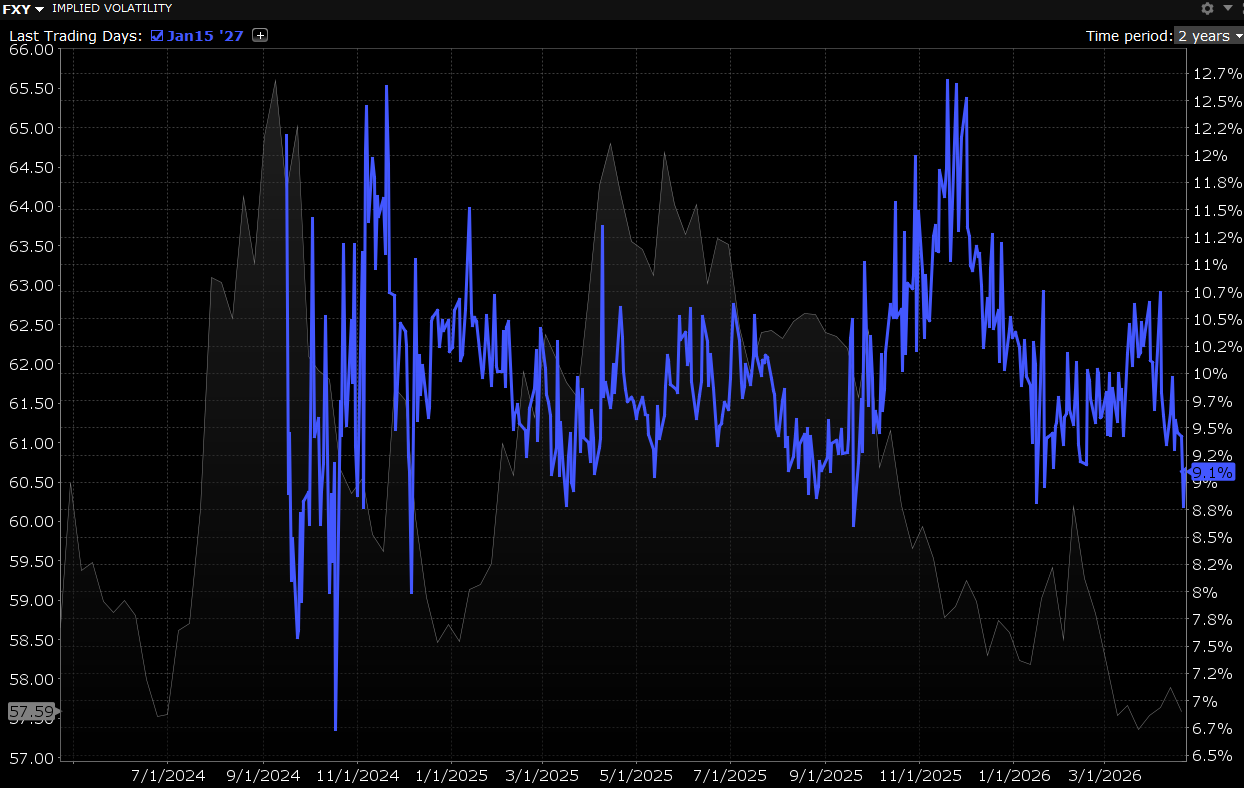

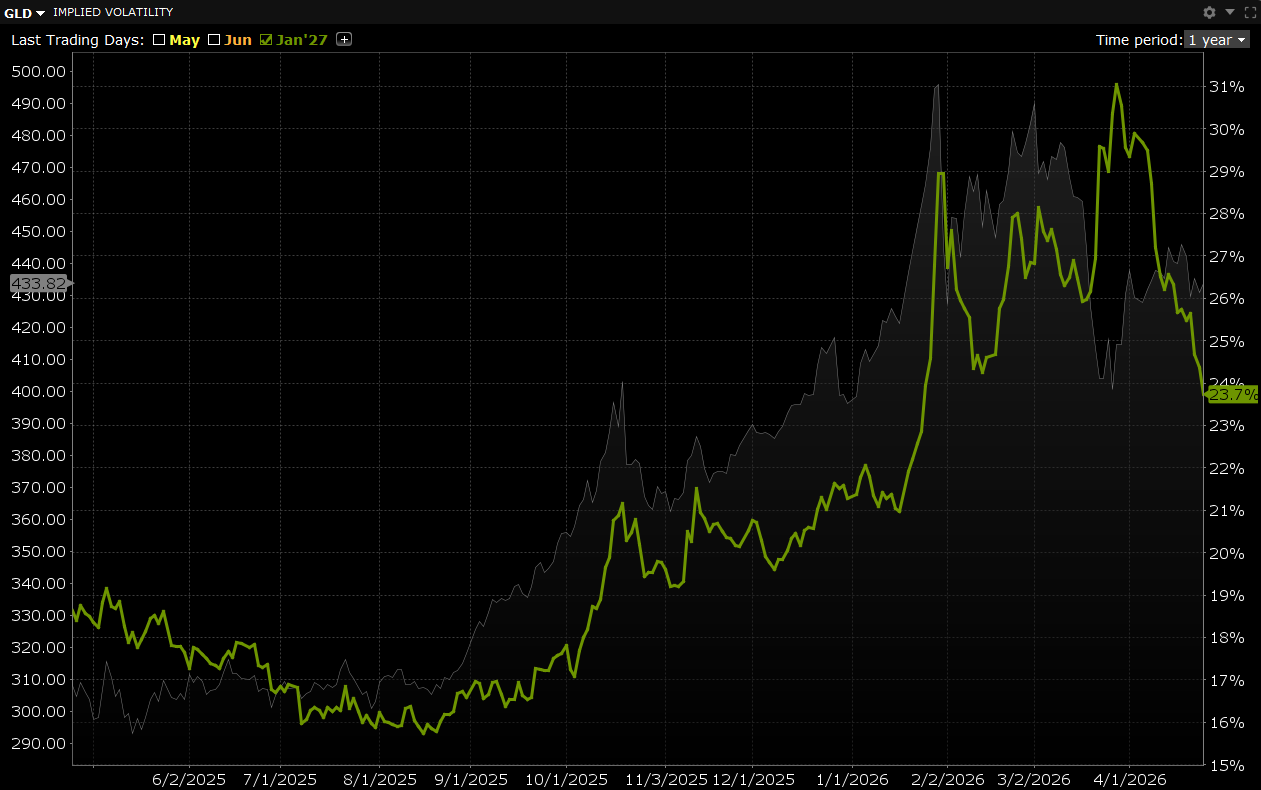

I’m not sure of the answer to that question, but I like the risk/reward, particularly given how cheap implied volatility is around the idea. Both US bond and USDJPY currency volatility are trading at multi-year lows. I have been placing bets on rising bond yields, weakening Yen and rising volatility.

We’ve seen over the past few years that gold is the release valve for all of this policy manipulation and volatility suppression. Despite what I believe to be conditions that indicate things are coming to a head, gold volatility is also meaningfully off its highs.

Looking elsewhere in Asia.

Given my views on Japan, I’ve also been digging into other Asian countries that might be in the same or worse position, but have less currency intervention risk. I did a quick screen of other possible candidates. Each country is unique and deserves its own research and discussion as their fiscal and monetary policy positions vary greatly. There are other elements as well, for example, despite the difficult positions Korea and Taiwan are in relative to the commodity supply chain problems, they benefit from the AI craze and are more difficult markets to short.

Risk of US oil export controls?

There is a historical correlation between gas prices and election outcomes, primarily as a gauge of voter sentiment and economic dissatisfaction, rather than a direct, consistent predictor of victory. Rising gas prices often correlate with lower presidential approval ratings and reduced electoral success for incumbents due to the “pocketbook effect,” where voters notice fuel costs more than other economic factors.

Impact on Approval Ratings: Studies have shown a strong inverse correlation, with a 10-cent increase in gas prices previously linked to a roughly 0.60% drop in presidential approval.

Incumbent Weakness: High prices generally harm the incumbent party, whereas lower prices, often caused by natural seasonal dips after Labor Day, can temporarily boost an administration’s standing.

Therefore it is not good for the administration when gasoline prices are still going vertical, despite their best efforts to manipulate the paper oil market.

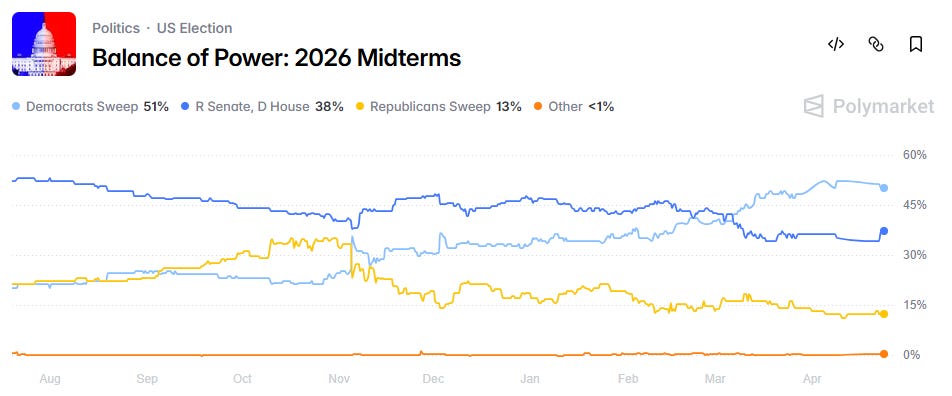

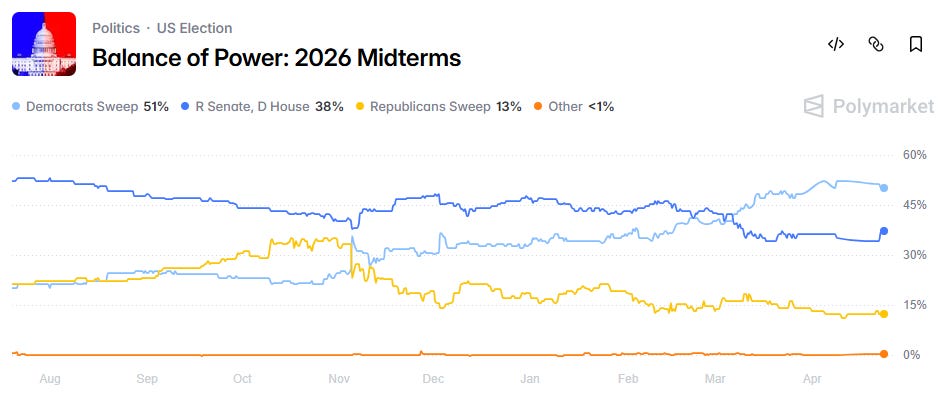

Combining the price shock with the Iran War being an extremely unpopular undertaking, it’s no surprise the midterm odds have been falling for Republicans.

We’ve been discussing all year how important this election is for Trump, first in our 2026 outlook and in recent Scouting the Tapes.

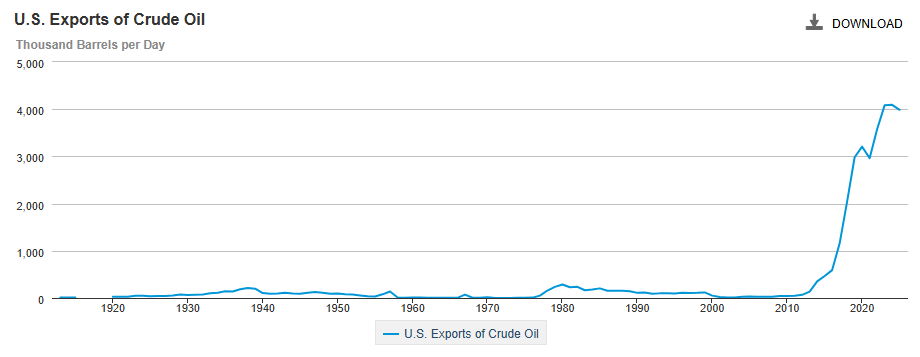

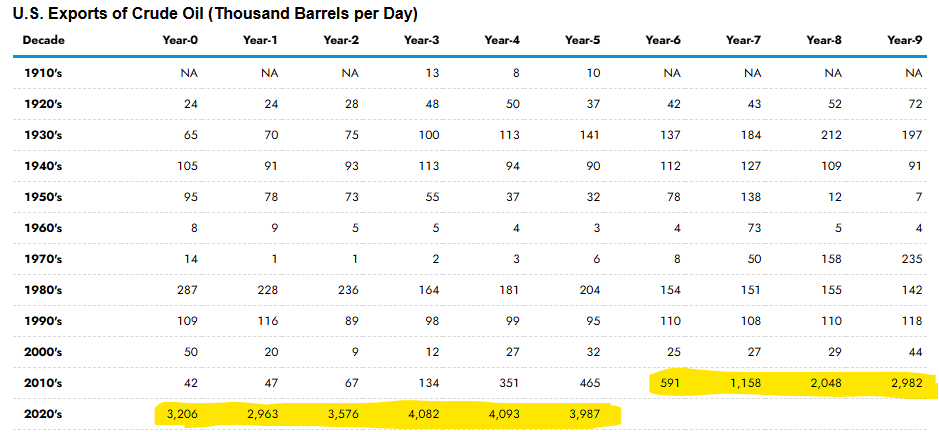

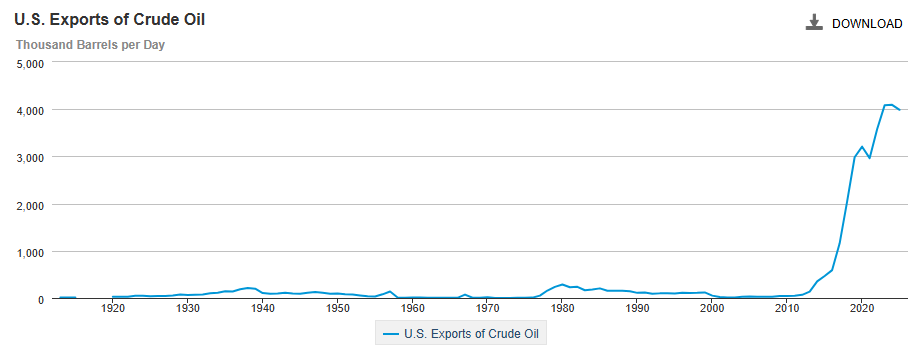

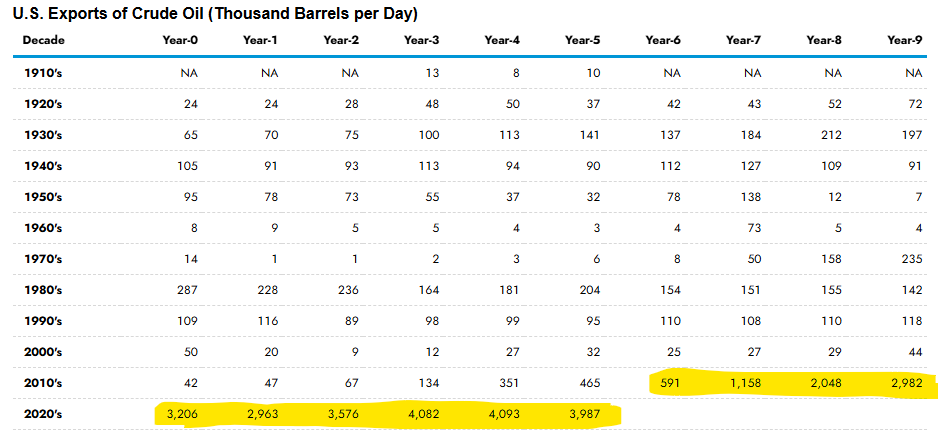

The crude oil export ban was only lifted in 2015 as a result of the massive rise in domestic production.

The surest fire way to reduce gas prices at the pump going into midterms would be to reinstate some for of export controls. This would lower domestic US oil and gas prices and provide a stimulus to consumers and businesses nationwide. While it would reduce US domiciled prices, it would be a large tailwind to non-US oil and gas prices and increase pressure on other countries. This isn’t that crazy of an idea given Trump has already shown us countless times he is not afraid to throw allies under the bus.

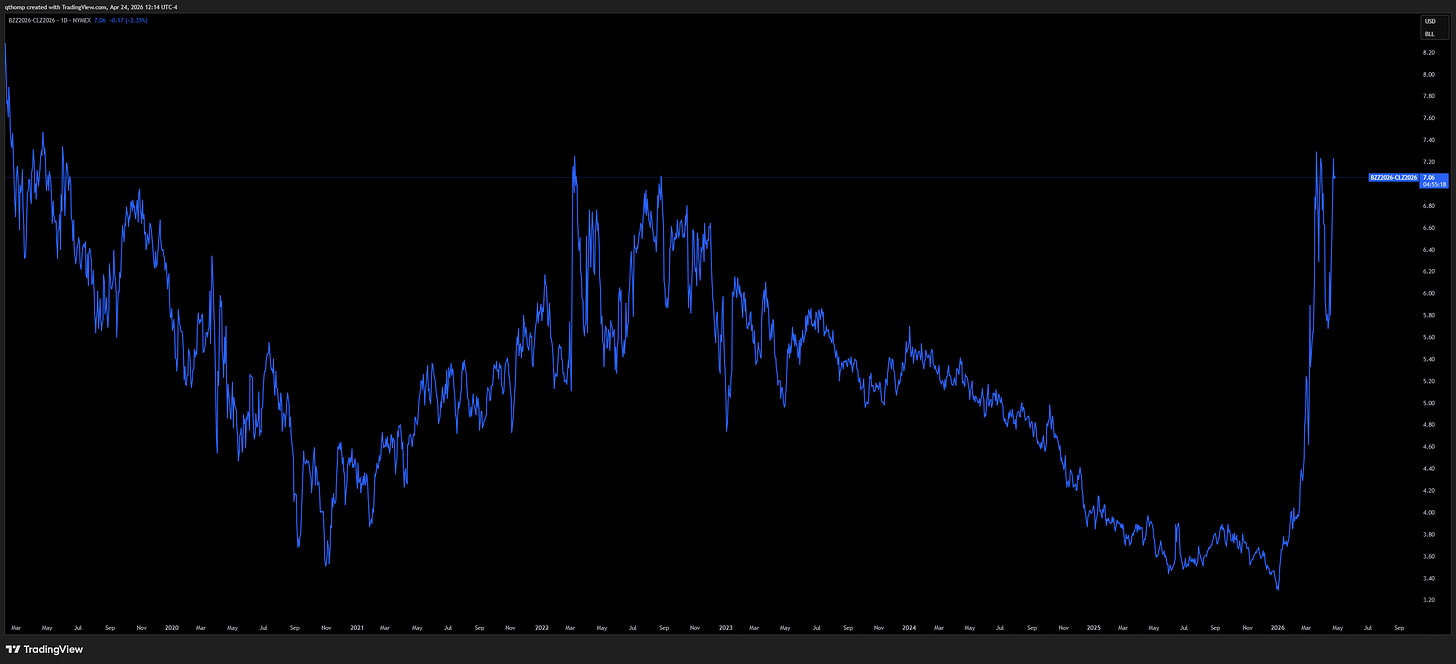

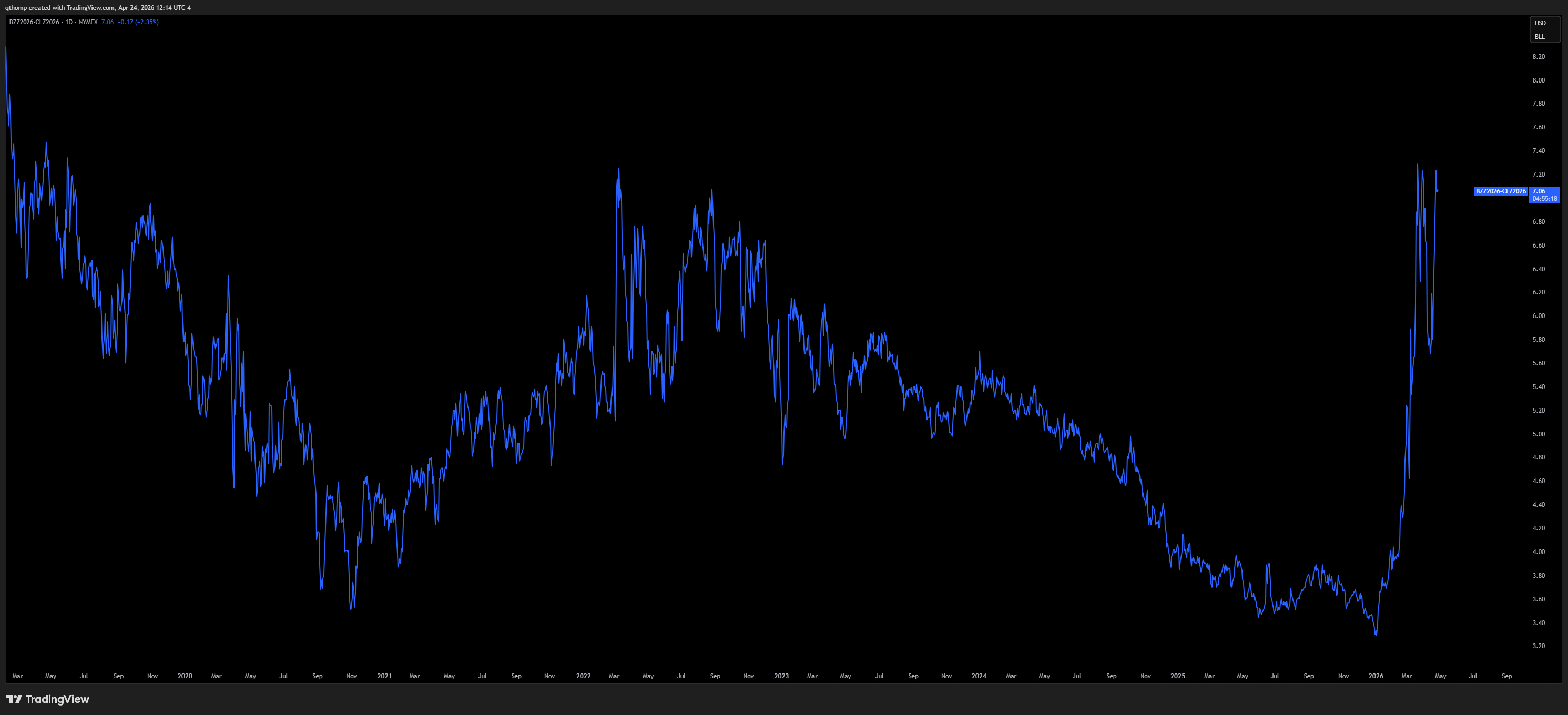

The market is not oblivious to this risk as the spread between Brent and WTI is sitting at its recent highs, despite front month oil prices being a fair bit off the highs.

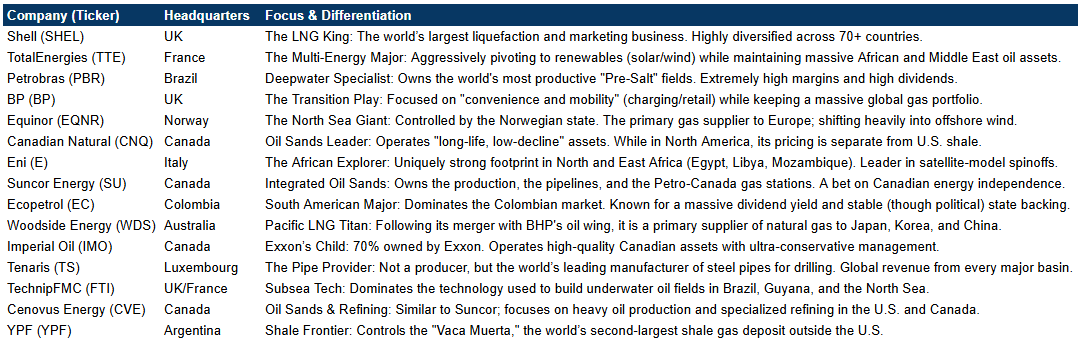

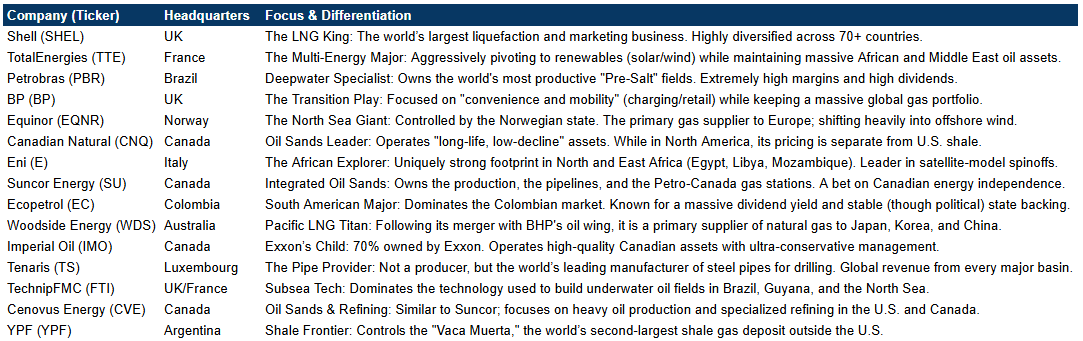

Given this risk, I prefer non-US exposure. Here is a list of the largest oil and gas stocks worth looking into that may provide more insulation than their domestic counterparts if the US were to re-instate some sort of export ban.

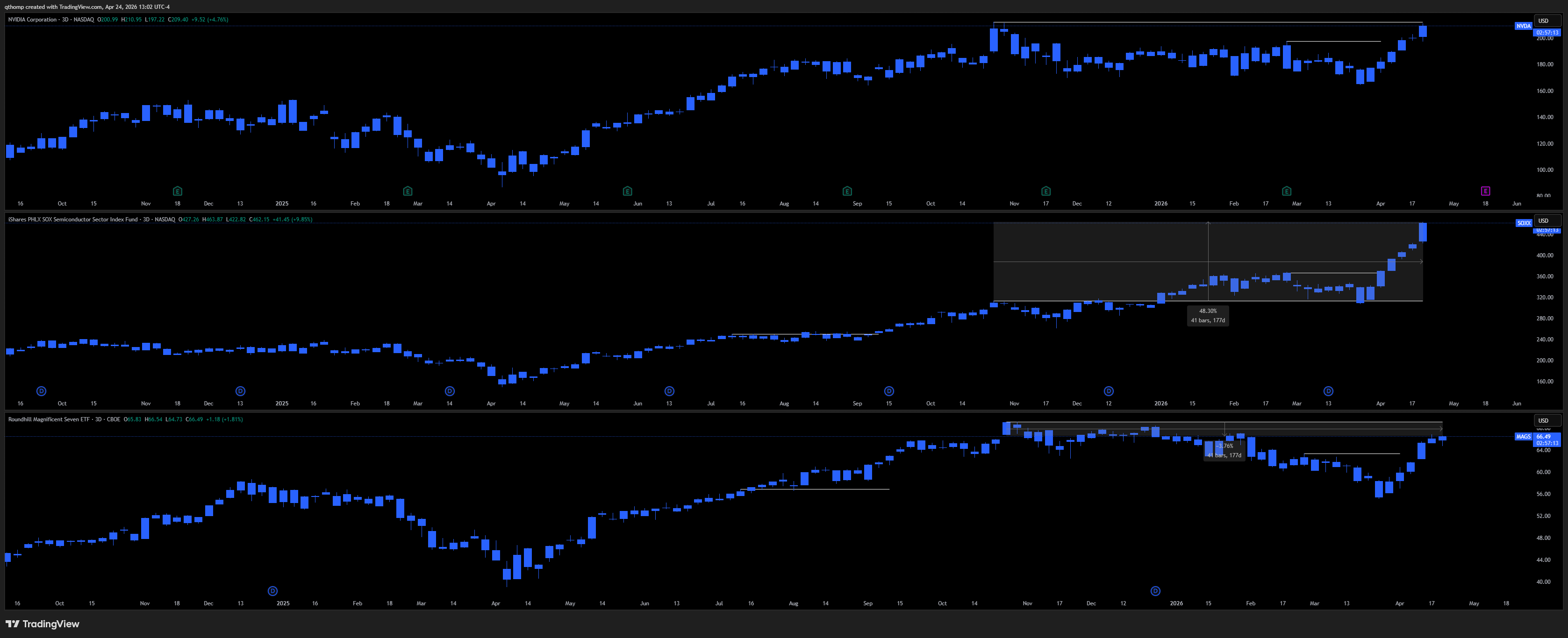

Semiconductors vs. NVDA

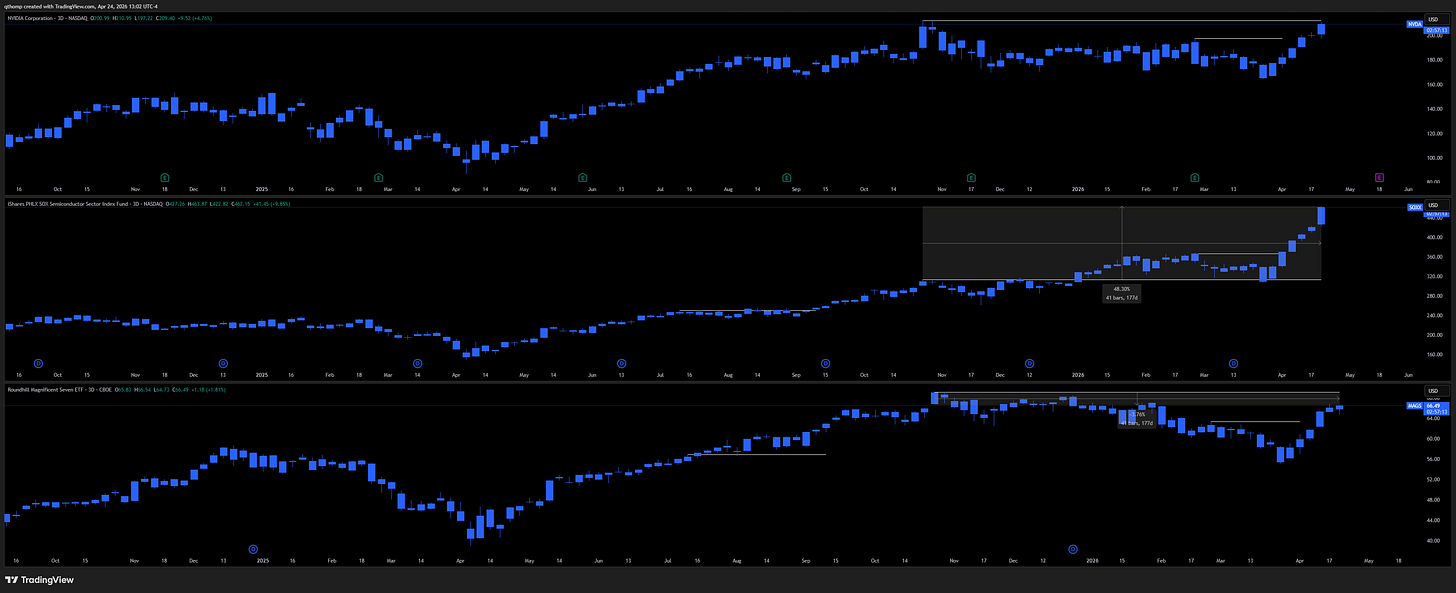

As a parting thought, I found something that caught my eye. Since NVDA and MAGS all-time highs in late October 2025, SOXX is +48%, NVDA is flat and MAGS is -4%.

Looking back in time, I’ve found that it’s extremely rare for NVDA to ‘play catch up’ to SOXX. So if you expect NVDA to break out to new highs here, you’re sorta betting on SOXX continuing its run but via the slower horse. I’ve started building long dated NVDA ATM puts. I think volatility is too cheap.

MAGS trades a bit differently and can continue higher even when SOXX stalls out from time to time, but MAGS is yet to see its highs retested. It’s interesting to see MAGS trading back up to its yearly open while we no longer hear anything about the capex burdens, FCF concerns and lack of share buybacks.

I hope this has been a thought provoking read. Please comment or reach out with any ideas that come to mind. Have a great weekend everybody.