Scouting the Tape - May 17, 2026

(Unique) macro idea generation and (insightful) market thoughts.

First off, a massive thank you to everyone who has contributed to this full on display of love and kindness. I am grateful for our community that is filled with such generous people who are front-footed in giving back and supporting others. You all donated and raised over $10,000 in less than a week for children and families going through some of the most difficult obstacles imaginable. Thank you very much.

As for the markets, I have a lot of different thoughts this week so some will be quick hitter ideas more so than usual. Maybe over the coming weeks a few of them will really tug at my attention and I will go deeper. As a reader, I would suggest that is something to be on the look out for - when I write about sectors or trades consistently week over week, odds are my conviction and interest in them are growing.

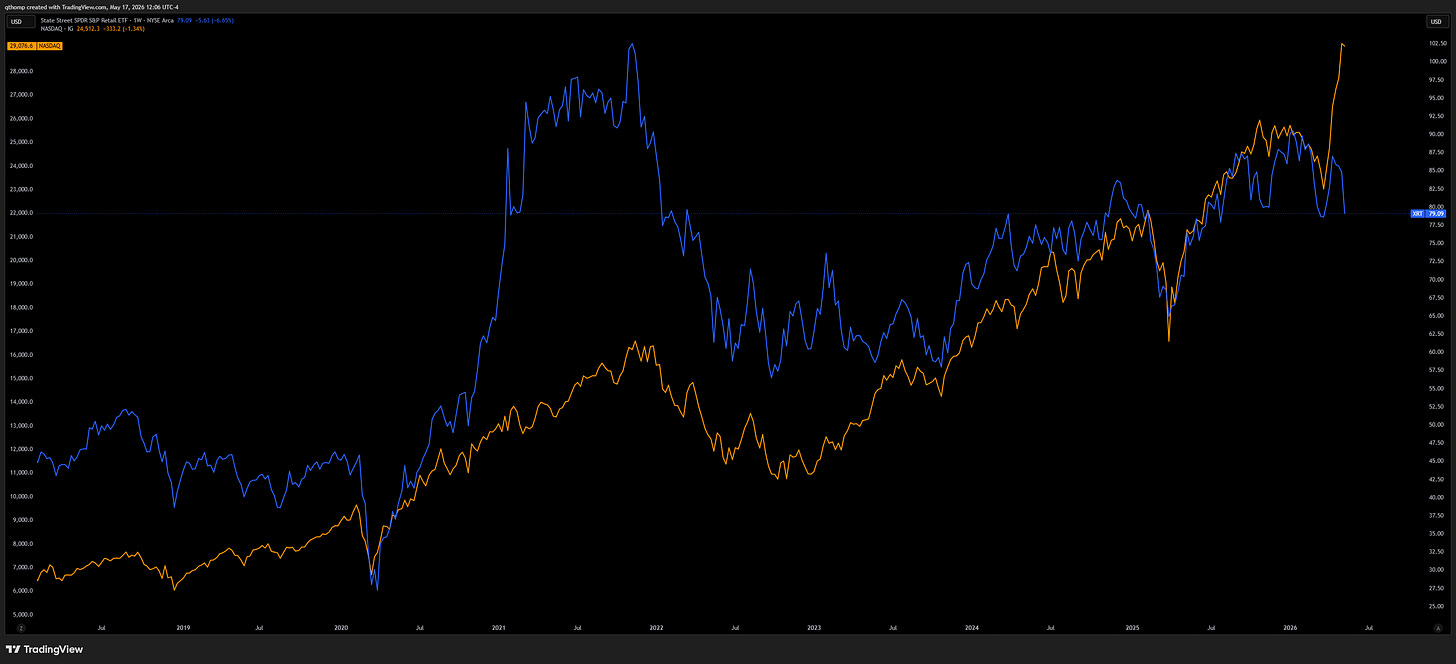

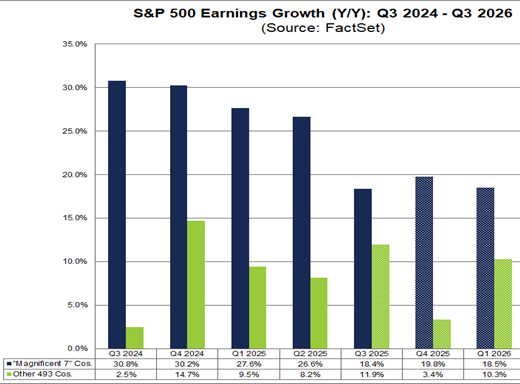

S&P 500 Retail index is saying something much different than Nasdaq.

This chart is bat shit crazy to me and is the K-shaped economy in a nutshell.

Continued fascination with the oil market dynamics.

The magnitude of the SPR release is not getting enough attention in my opinion. Once again we have another example of Trump and Bessent doing the exact same thing they criticized Biden and Yellen for doing. Exact same thing.

Quinn Thompson@qthompBiden drained ~300mm barrels of oil from the SPR over ~2.5 years. Trump is going to drain ~170mm over ~7 months. From 640mm to 240mm in 5 years, all to protect boomers' asset prices. Together the political elite are paving the way for $250 oil prices in a few years.

Quinn Thompson@qthompBiden drained ~300mm barrels of oil from the SPR over ~2.5 years. Trump is going to drain ~170mm over ~7 months. From 640mm to 240mm in 5 years, all to protect boomers' asset prices. Together the political elite are paving the way for $250 oil prices in a few years.

Quinn Thompson @qthomphttps://t.co/kYCvBXIOwA3:10 PM · May 16, 2026 · 6.76K Views8 Replies · 6 Reposts · 70 Likes

Quinn Thompson @qthomphttps://t.co/kYCvBXIOwA3:10 PM · May 16, 2026 · 6.76K Views8 Replies · 6 Reposts · 70 LikesThis may be one of those instances I mentioned in the introduction where your antennas should perk up because I keep writing about something. The oil complex has been in just about every Scouting the Tape for weeks on end now. Last week I noted the XLE/XLK divergence. In April I discussed the risks of a US export ban and the bull case for long dated Brent oil futures.

A quote of my recent tweet put it very succinctly.

4lex@_4lex_4The GS commodity basket is +50% YTD, and that’s with global oil reserves drawing down by 100m barrels (7%) per month. Severe inflation is coming. US voters will be in a very foul mood come Nov.Quinn Thompson @qthompBiden drained ~300mm barrels of oil from the SPR over ~2.5 years. Trump is going to drain ~170mm over ~7 months. From 640mm to 240mm in 5 years, all to protect boomers' asset prices. Together the political elite are paving the way for $250 oil prices in a few years. https://t.co/nPBXEI8U1n1:40 AM · May 17, 2026 · 316 Views1 Like

4lex@_4lex_4The GS commodity basket is +50% YTD, and that’s with global oil reserves drawing down by 100m barrels (7%) per month. Severe inflation is coming. US voters will be in a very foul mood come Nov.Quinn Thompson @qthompBiden drained ~300mm barrels of oil from the SPR over ~2.5 years. Trump is going to drain ~170mm over ~7 months. From 640mm to 240mm in 5 years, all to protect boomers' asset prices. Together the political elite are paving the way for $250 oil prices in a few years. https://t.co/nPBXEI8U1n1:40 AM · May 17, 2026 · 316 Views1 LikeInflation is here to stay and your portfolio best be positioned for it. You can entertain yourself with the table game of the day at the semiconductor casino but getting really long critical commodity infrastructure and national energy security plays will probably net out the same if not better returns over time with a lot less stress.

FX and the dollar.

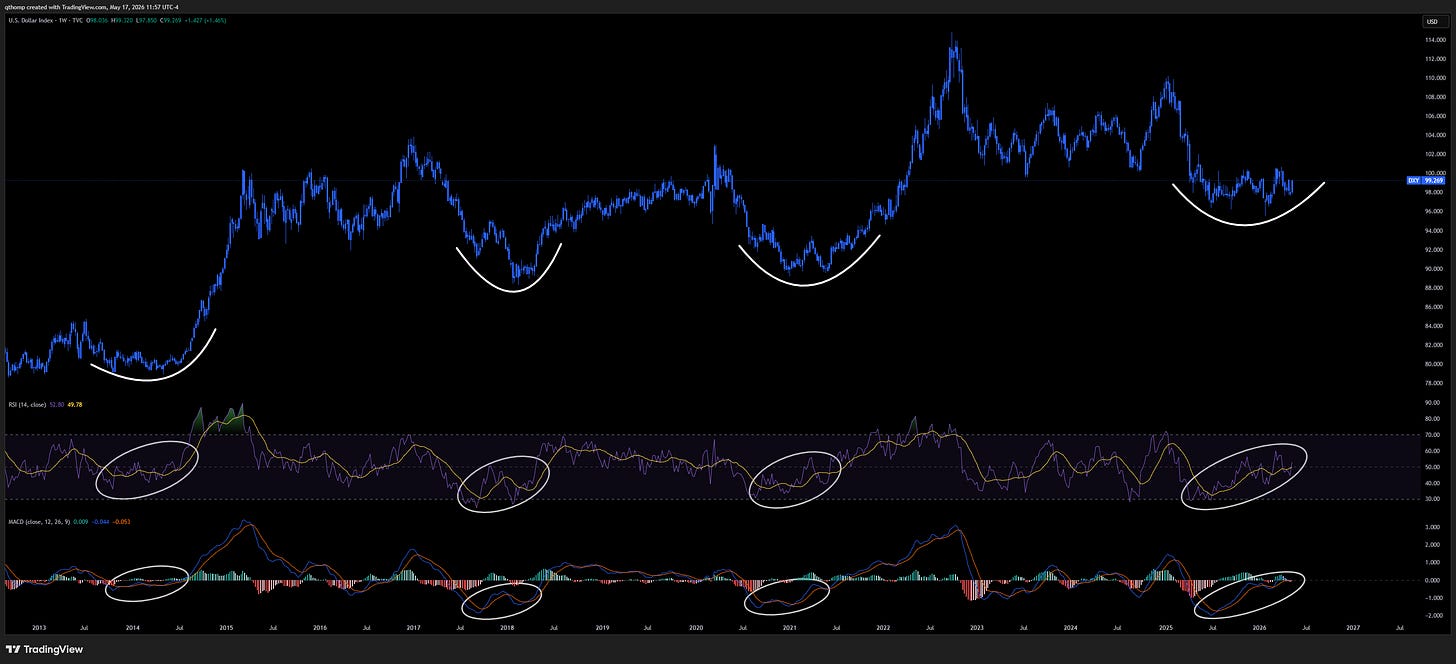

On Monday I tweeted the following arguing for a rise in the dollar. I got lucky on the timing.

Quinn Thompson@qthompI think dollar shorts are vulnerable here and I'm not sure DXY's next go at 100 is going to hold again. Economic data continues to show stabilization and improvement while inflation will worsen in the near-term. Hawkish is the path of least resistance for the FOMC.7:14 PM · May 11, 2026 · 10.7K Views5 Replies · 3 Reposts · 56 LikesI will leave you with just one chart which is the weekly DXY with RSI and MACD indicators. The technical setup here looks unbelievably bullish to me.

In recent weeks I’ve been writing about the setup in USDJPY and what policymakers can do about it. This is all related to the dollar. I continue to believe FX and the dollar are integral to understanding the direction of global macro right now.

Taiwan.

Watch this recent Trump interview. It is the most soberly I’ve heard him speak on the Taiwan issue and he seems a bit shook about it.

Quinn Thompson@qthompWatching this interview pretty much validates everything @jam_croissant has been warning about Taiwan over the last few years. Rapid Response 47 @RapidResponse47WATCH IN FULL: President Donald J. Trump's interview with @BretBaier in Beijing3:13 PM · May 16, 2026 · 8.53K Views3 Replies · 1 Repost · 28 Likes

Rapid Response 47 @RapidResponse47WATCH IN FULL: President Donald J. Trump's interview with @BretBaier in Beijing3:13 PM · May 16, 2026 · 8.53K Views3 Replies · 1 Repost · 28 LikesIt got me thinking about this tweet I wrote last December where I called NVDA a national security threat.

Quinn Thompson@qthompA few weeks ago on @ForwardGuidance I called $NVDA a national security threat. The US stock market has a Mag7 problem. Concentration risks are mounting as the top 10% of US stocks now represent ~80% of total US equity market cap. It begs the question - does the US have a

Forward Guidance @ForwardGuidance$PLTR at ~250x earnings, $NVDA at $5T, and the top 10 stocks now making up 40% of the S&P The problem with bubbles is that they’re reflexive in both directions, and when the entire market floats on Fed-driven liquidity, the distortions get extreme Meanwhile, the core of12:51 PM · Dec 8, 2025 · 64.5K Views14 Replies · 18 Reposts · 186 Likes

Forward Guidance @ForwardGuidance$PLTR at ~250x earnings, $NVDA at $5T, and the top 10 stocks now making up 40% of the S&P The problem with bubbles is that they’re reflexive in both directions, and when the entire market floats on Fed-driven liquidity, the distortions get extreme Meanwhile, the core of12:51 PM · Dec 8, 2025 · 64.5K Views14 Replies · 18 Reposts · 186 LikesIt has me thinking, has the Trump administration been blowing the bubble in the AI sector (purposefully, they aren’t stupid) because they need these companies to have cheap and large access to financing to re-shore the semiconductor and chip industry to the US as quickly as possible before Taiwan loses its independence? Outside of national security or strategic imperative, there aren’t many great reasons why you’d want both your stock market and economy so levered to one extremely cyclical sector while negatively impacting the majority of the population.

I’ve been noodling over this line of thinking for a few days and it won’t go away. Then I see this Chamath clip of him talking about Taiwan’s declining relevance which has me thinking he got this narrative from his buddy and podcast mate David Sacks who happens to be Trump’s AI czar.

The All-In Podcast@theallinpodChamath: Taiwan Loses Its Strategic Importance in 18 Months @chamath: “ We're 18 months from Taiwan not being an important moment of conversation the way it is today. Why 18 months? Because we are at a point where we're probably 1-2 nanometers away from being able to do what1:30 AM · May 17, 2026 · 591K Views313 Replies · 180 Reposts · 1.33K Likes

The All-In Podcast@theallinpodChamath: Taiwan Loses Its Strategic Importance in 18 Months @chamath: “ We're 18 months from Taiwan not being an important moment of conversation the way it is today. Why 18 months? Because we are at a point where we're probably 1-2 nanometers away from being able to do what1:30 AM · May 17, 2026 · 591K Views313 Replies · 180 Reposts · 1.33K Likes

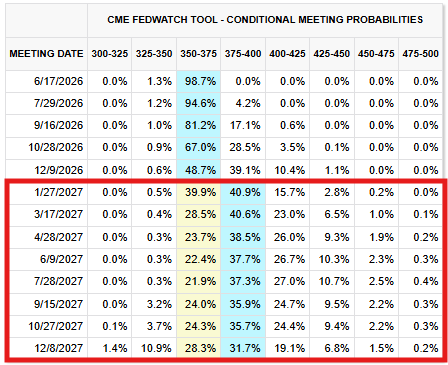

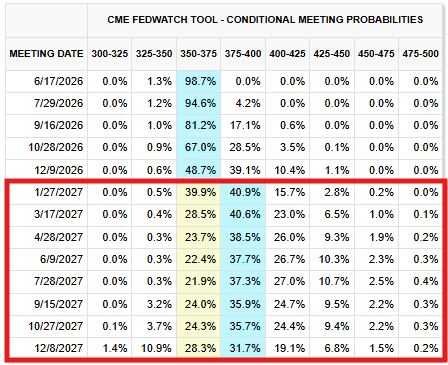

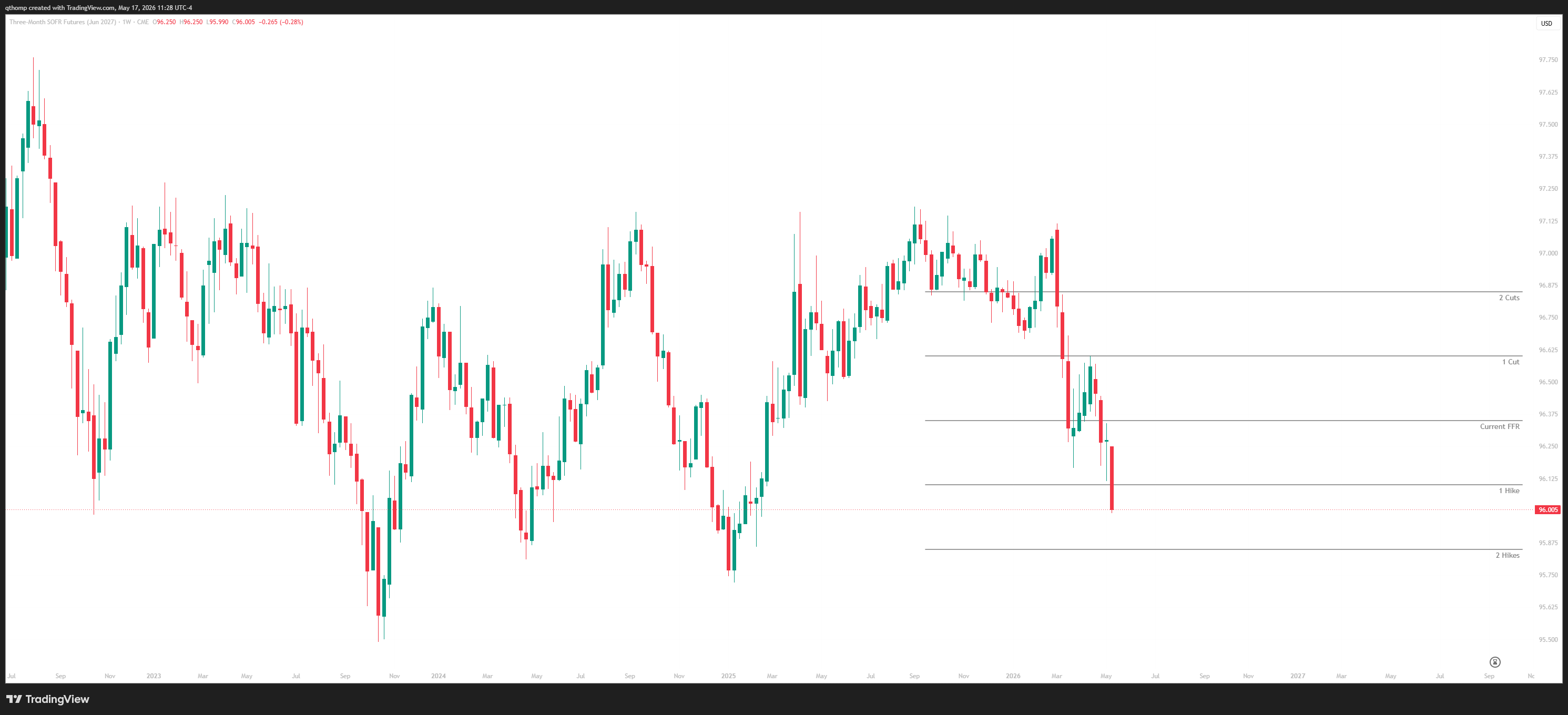

When do SOFR futures become interesting?

The recent change in the Fed Funds rate market has been dramatic. We’ve been playing the rates market well this year having made money from both the long and short side.

Since early April we have been bearish on SOFR futures under the expectation that inflation was going to keep surprising to the upside. In late April we continued to expand on this idea, detailing the worsening inflation picture and the negative outlook for SOFR futures.

Here we are weeks later and you have almost 2 rate hikes priced into 2027 and I' find myself asking what is an attractive entry, if any, to get back into the trade from the long side. I’ve been focusing a lot on the June 2027 contract.

In that April 10th post I wrote “the optimal entries should come when equities are still trading well but inflation is surprising to the upside”. I think that could come over the coming 1-2 months. I think we still have a few more worsening inflation prints to get through but there will be a time to get long SOFR again as cheap insurance. I want to fade the rate hikes happening but do so from a great price.

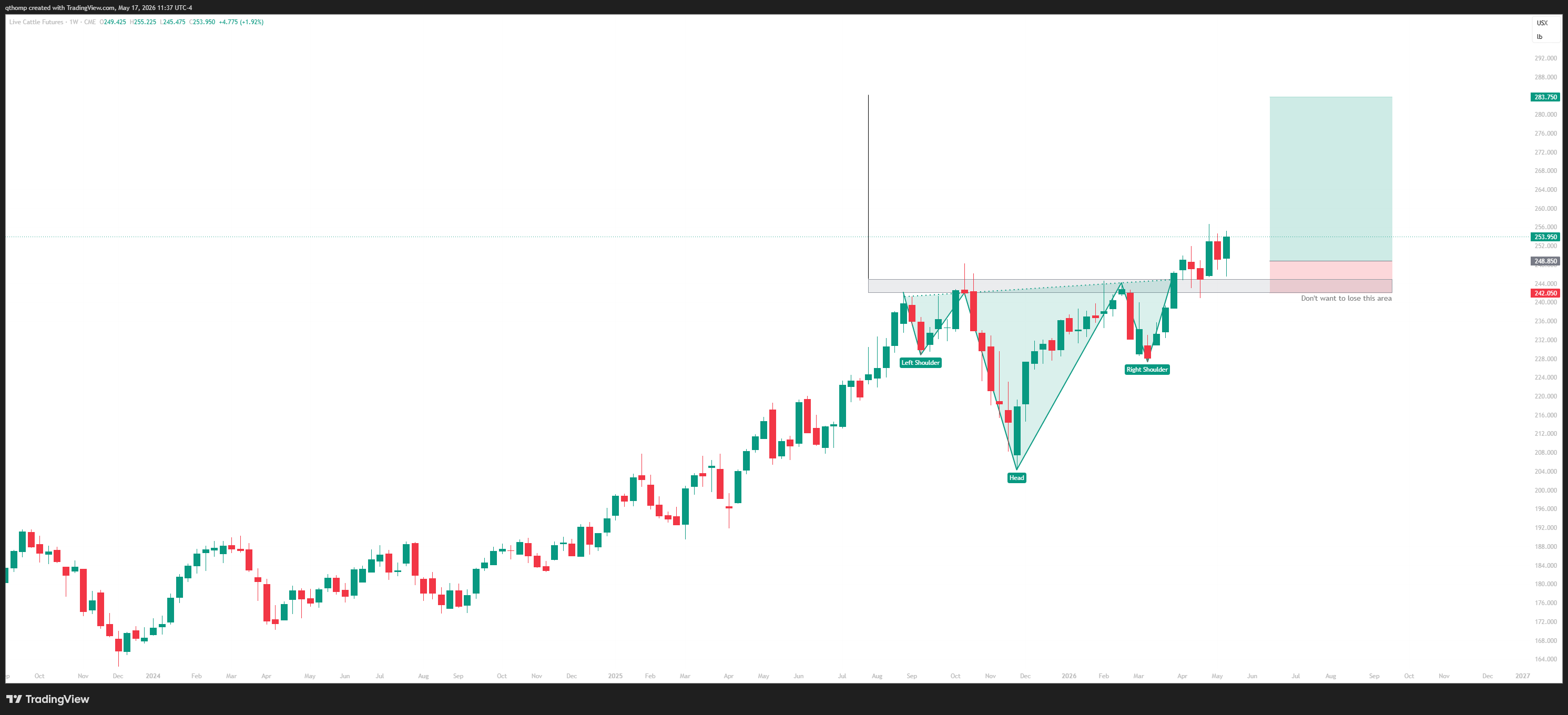

Agricultural commodity futures are ripe for speculation.

I started writing about ags in a few March editions of Scouting the Tape. Initially laying out the high level trade and then simplifying it further. I believe this is an area to be seeking attractive risk/reward setups and trading around the complex.

One of the trades I am currently long are live cattle futures (LE). What if I told you that since the March 2020 COVID bottom, the asset has matched the S&P 500 return with a smaller max drawdown (-17%) and lower volatility. Suffice to say live cattle prices are in a secular bull market which is why you’re reading about the cost of beef hitting new highs every 3 months. I like the 5:1 risk/reward setup out of this head and shoulders on the daily chart. I’ve been long for a few weeks now so have a better entry than the current level but still really like it.

Live cattle are cows that have reached their finished weight (1,200-1,500 pounds) and are ready for slaughter. This is the primary point of price discovery for the beef industry, meatpackers and grocery chains, creating for a large and liquid market. There are also feeder cattle futures (GF) which constitute younger calves (700-900 pounds) that are sold to be fattened up for eventual slaughter. There is a concept that simplifies the supply chain known as “cost of gain” where essentially feeder cattle + corn + time = live cattle. The cattle crush spread is a profitability or margin calculation that = live cattle - (feeder cattle + corn).

From here you can understand that when the cost of corn and other agricultural commodities rise, it has a serious impact on the supply chain. It can cause the cost of feeder cattle to drop as they can only charge the market rate for the finished beef and thus their cost inputs must rebalance. Live cattle on the other hand are more resilient to broader ag inflation because their price includes all of the costs throughout the supply chain. I am drastically simplifying things here but maybe I will try to elaborate each week on a new aspect of the agricultural commodity complex as I assume most of my readers did not grow up in Wisconsin and have no familiarity with this stuff.

Capital vs. labor.

Shout out to Deer Point Macro for the updated capital vs. labor chart. I wrote about what I think is a bubble in corporate profits last week and used their chart to illustrate the divergence between the two camps of the economy.

Thank you all for reading and I hope everyone has a great week. On the next Forward Guidance episode I will have a shaved head courtesy of our wonderful fundraiser donors.

Great thoughts, Quinn. Excited for a series on ag complex. Catch you on the round up!

Really interesting Quinn, thanks! I've been watching that continuation H&S on Cattle too.