Scouting the Tape - May 30, 2026

(Unique) macro idea generation and (insightful) market thoughts.

Volatility is nowhere to be found in this market and it could be months later this summer before that changes - the administration has a huge incentive to keep things copacetic into midterms. That said, I am excited about what I think are some very actionable opportunities setting up over the coming weeks in my neck of the woods, aka not semiconductors and AI bottlenecks. I believe the next few weeks will bring about a trend change. It’s always difficult to predict the exact timing of these things because you never know the catalyst that will really land with the market to set things off, but I believe it is coming.

In addition to the usual Forward Guidance recording this week, I also joined Maggie Lake for an episode of The Market House .

Stagflation.

As someone who is quite interested in geopolitics and strategy, I wouldn’t say I’m surprised the US is in the situation it is in given Trump’s hubris and the structural problems outside of his control. But I would say there are moments where I find myself in disbelief that this is the chosen path. Back in February I wrote on X: “What if Trump views this conflict as his 2026 Liberation Day equivalent? His confidence must be at all-time highs given the Maduro raid and his belief he can control the US dollar like a yo-yo and pump the stock market whenever he chooses.”

Quinn Thompson@qthompI'm a bit surprised at the lack of discussion on Iran and what's going on in the Middle East. The US is on the brink of war that by extension would be against China and Russia as well given the support they are providing. I am also surprised that oil is not trading at highs given

Quinn Thompson@qthompI'm a bit surprised at the lack of discussion on Iran and what's going on in the Middle East. The US is on the brink of war that by extension would be against China and Russia as well given the support they are providing. I am also surprised that oil is not trading at highs given

Quinn Thompson @qthompThis is the last weekend before Ramadan (2/17 - 3/26) and it happens to be a 3 day US holiday. Not that someone with Trump's risk appetite couldn't strike Iran during the holiest month of the Islamic calendar, it certainly would come with risk of alienation and disapproval from5:46 PM · Feb 17, 2026 · 113K Views21 Replies · 3 Reposts · 146 Likes

Quinn Thompson @qthompThis is the last weekend before Ramadan (2/17 - 3/26) and it happens to be a 3 day US holiday. Not that someone with Trump's risk appetite couldn't strike Iran during the holiest month of the Islamic calendar, it certainly would come with risk of alienation and disapproval from5:46 PM · Feb 17, 2026 · 113K Views21 Replies · 3 Reposts · 146 LikesDemocrat, republican or independent, the Iran War is unanimously unpopular. Real wage growth is firmly negative as inflation pushes higher into the 4-5% range and the average American household continues in a state of distress. And now Iran has control of a key commodity supply chain channel that it never did before. While there have been a number of very positive policy changes throughout the first two years of this Trump administration, there have also been so many self-owns and policy rollout botches that the campaign scripts for Democrats are writing themselves. Since I became an active investor/speculator, I have a strong track record in political outcomes having correctly called the last 3 presidential races. I will be doing more writing on the topic of midterms as we approach them but at this juncture I do not think it will be pretty for Trump.

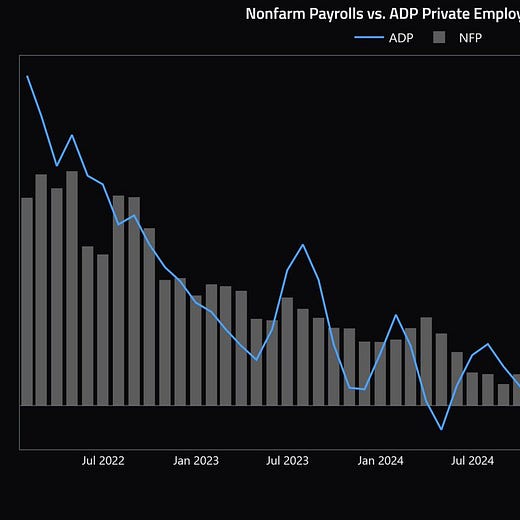

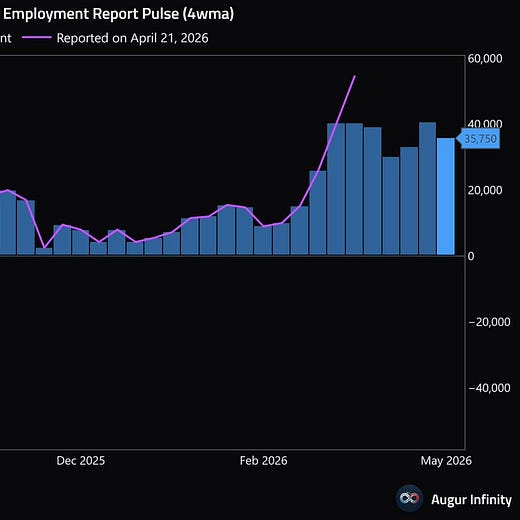

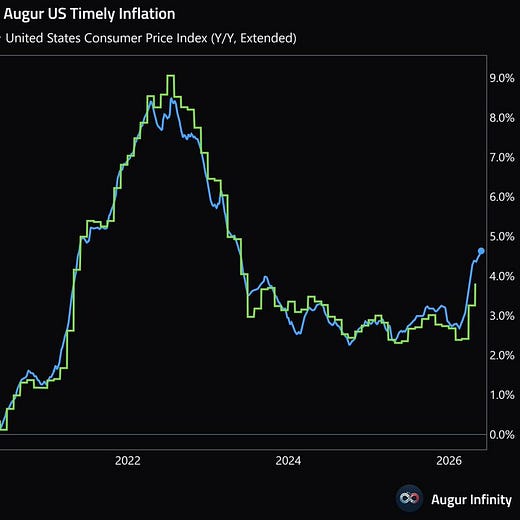

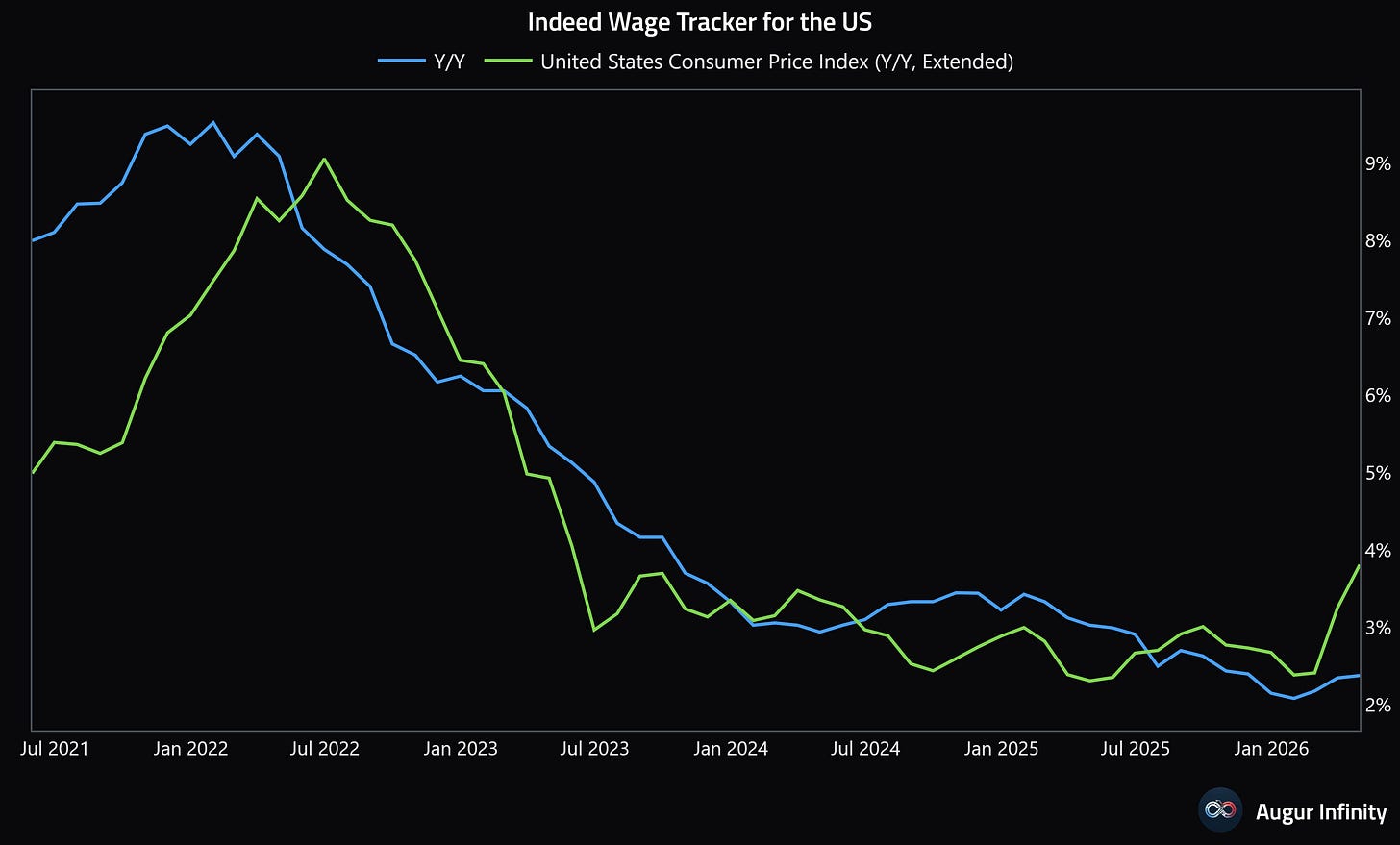

Stagflation is one of the worst setups for risk assets and economic health but that is where we are headed. >4% inflation for the foreseeable future and stagnant economic growth.

Quinn Thompson@qthompGet ready to hear the word STAGFLATION again. The labor market is likely to make another deadcat bounce similar to recent years while inflation will continue to print higher for the next few months.

12:23 PM · May 28, 2026 · 1.22K Views1 Repost · 18 Likes

12:23 PM · May 28, 2026 · 1.22K Views1 Repost · 18 Likes

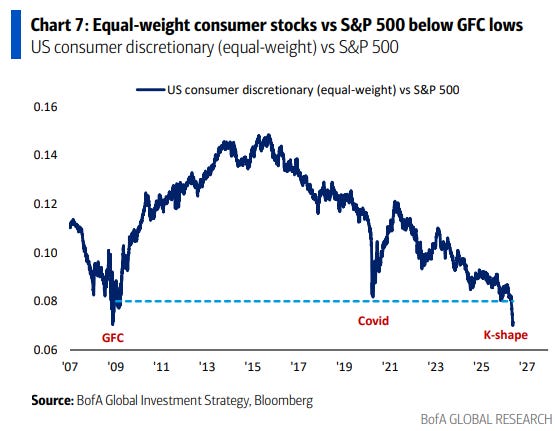

The K-shaped economy is taking step function changes in the wrong direction.

Similar to the above idea, it sure strikes me as a major problem facing policymakers but given their appetite to ignore and worsen the K-shaped economy over the past few years, it is nearly impossible to predict when it will start to matter more acutely.

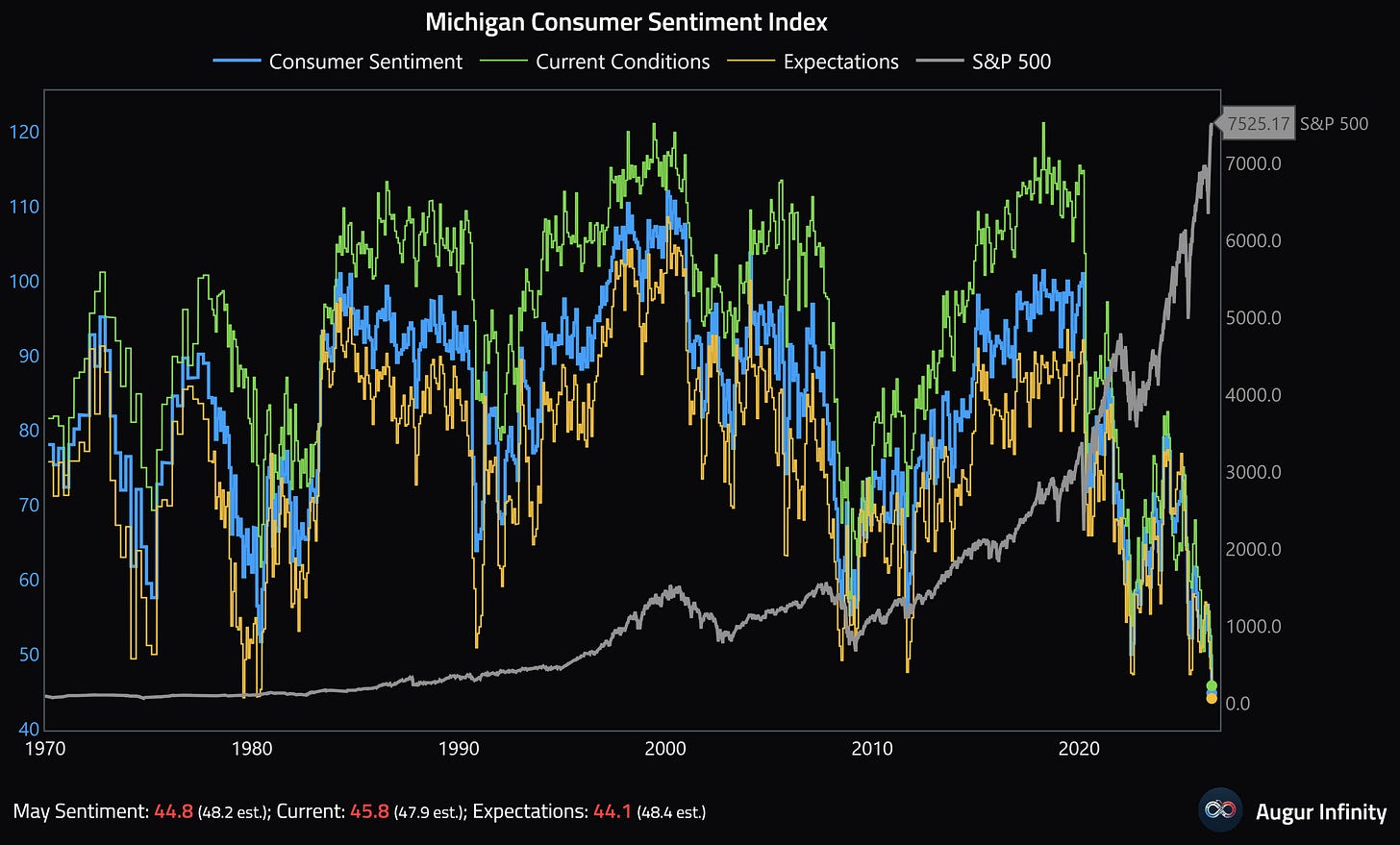

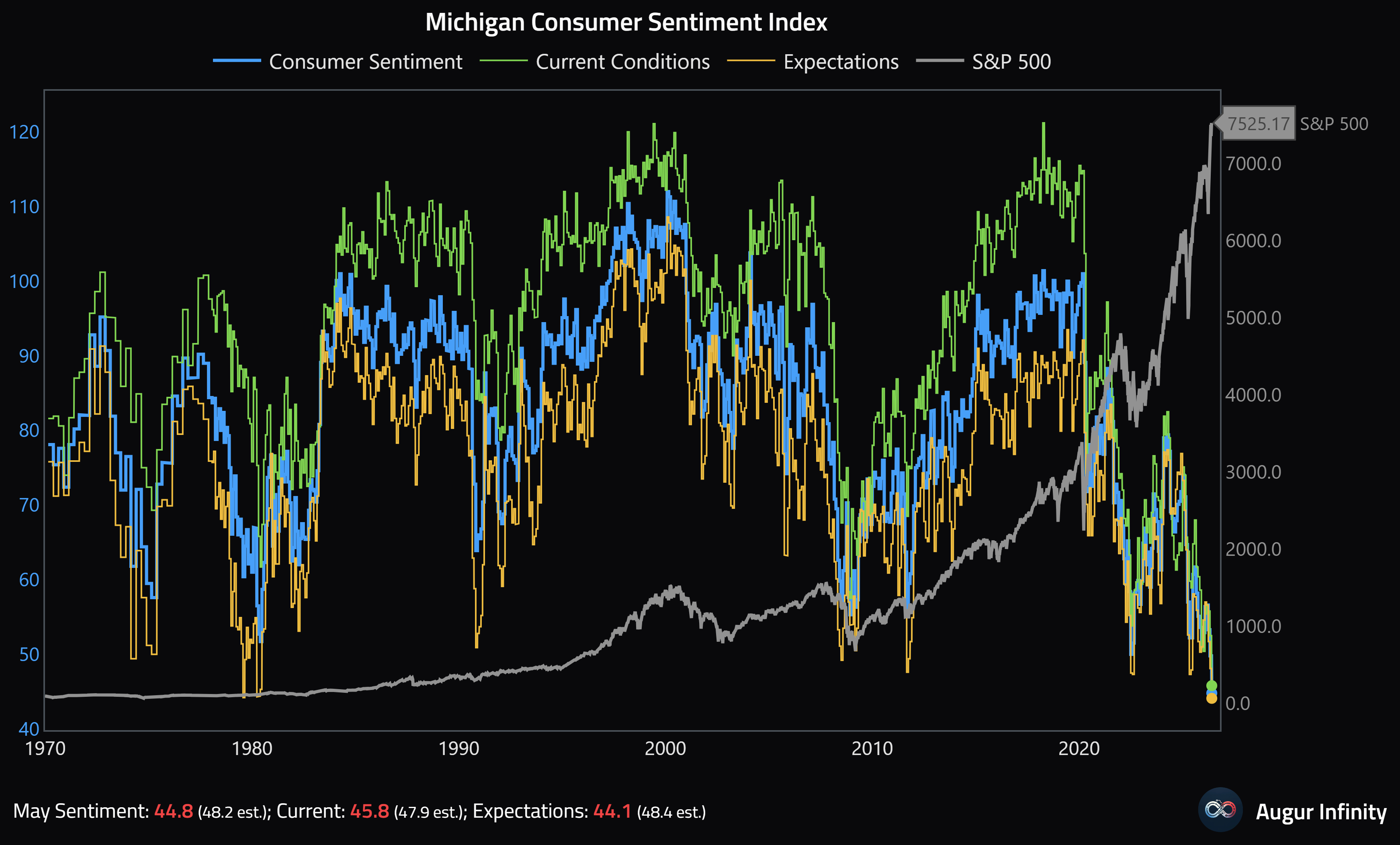

Everyone knows about the new record lows in consumer confidence and small business optimism. The numbers are so mind boggling that people now just dismiss them as being faulty surveys.

Walmart earnings takeaways were bleak for the average consumer.

“Increasingly, [consumer strength] depends upon which consumer you’re talking about. We see with our customers that the high income customer is spending with confidence into many categories, while the lower income consumer is more budget conscious and perhaps navigating financial distress.”

“In the most recent period, the number of gallons that customers fill up with when they come to our fuel stations fell below 10 for the first time since 2022. That’s an indication of stress.”

Fuel weighed on Walmart’s profit margin in the quarter, as

the company absorbed “virtually the entirety” of the increases

during the period.

Real wage growth in the US has been negative for almost a year now.

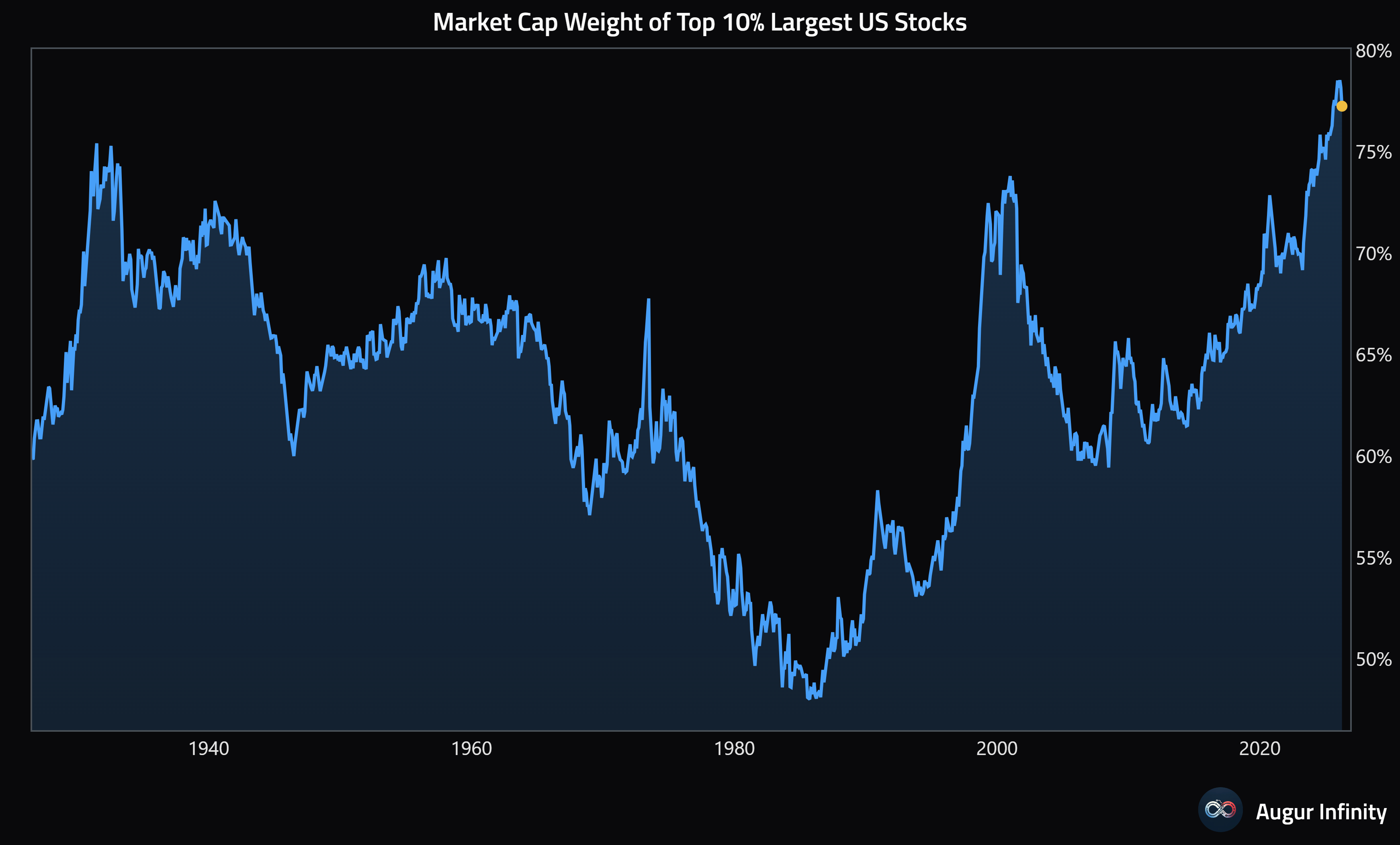

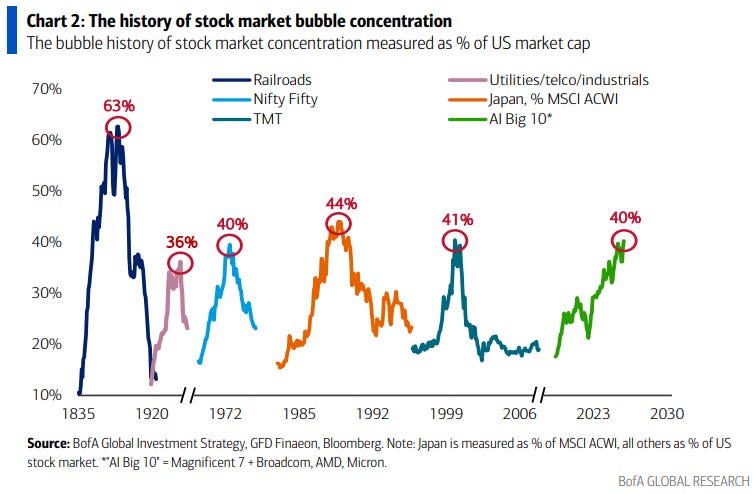

Market concentration continues to make new record highs.

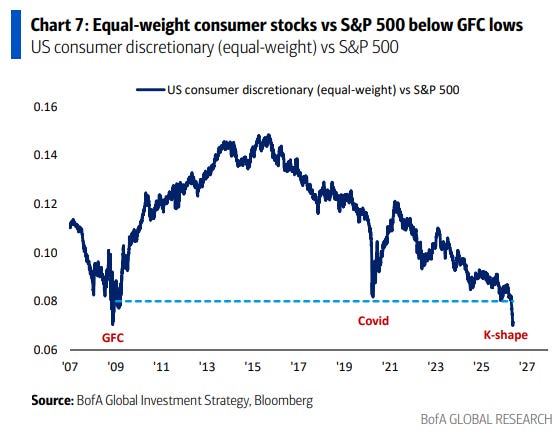

Consumer stocks vs the S&P 500 are below GFC levels.

But here’s the kicker. Boomers don’t give up their voting majority until at least 2028 and more definitively 2032, so it actually could be quite some time before this resolves itself.

By the 2028 presidential election, the combined power of millennials and gen Z is expected to make up over half of the entire voting-eligible population. However, voter turnout rates are highest among boomers at ~75% and decline from there with millennials at ~60% and gen Z at ~45%. So despite the larger voter eligible younger cohorts, this election will still very much be influenced if not controlled by boomers. Add on top of that the fact that boomers still dominate leadership positions in congress and state governments which we know favors incumbents.

This means that it may not be until 2032 presidential elections that we start to see real change where the younger generations’ raw numbers will be strong enough to significantly outweigh the boomers’ consistently high turnout rate. In other words, you may have to hear about the K-shaped economy from me and many others for another 6 years before any real progress is made in rebalancing it.

Late cycle behavior in Japan.

I continue to be fascinated by Japan because it may be the place that has defied more gravity than any other country’s equity market. What do I mean by that?

They also have some of the worst demographics globally. They are the oldest developed nation at a median age of 50 years (compared to 39 in the US). For every 2 workers there is 1 retiree (that ratio is 4:1 in the US) and their population is declining -0.25-0.5% per year, effectively losing a city the size of San Francisco every 12 months.

That said, it is ‘better’ at handling these demographic problems. Japan’s social security, medicare and medicaid equivalent spending is ~55% which is identical to that of the US, despite that being spent on Japan’s ~30% elderly population compared to the ~18% elderly population in the US. On the other hand, Japan spends ~25% of its total budget on debt service, whereas that figure is ~14% in the US.

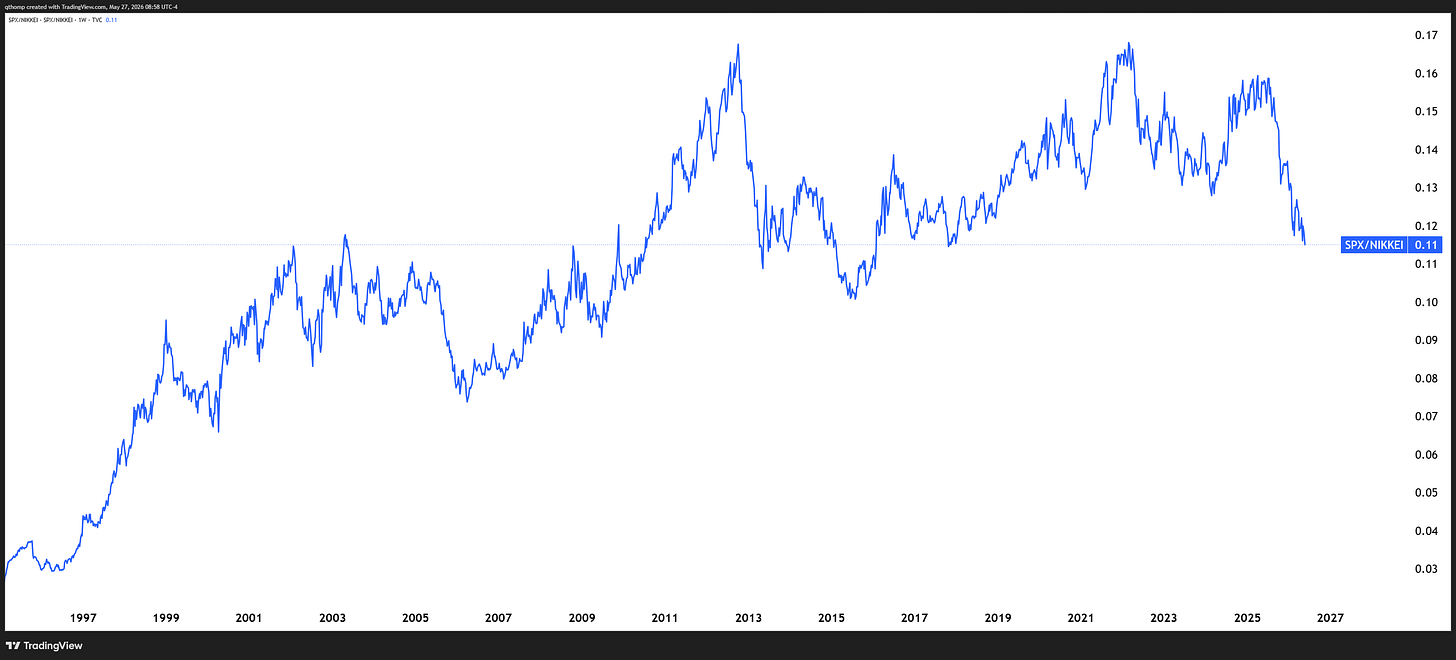

Despite all of those problems, the Nikkei has outperformed the S&P 500 by nearly +30% since Liberation Day, and this is without all of the leading AI and semiconductor companies comprising the Japanese index.

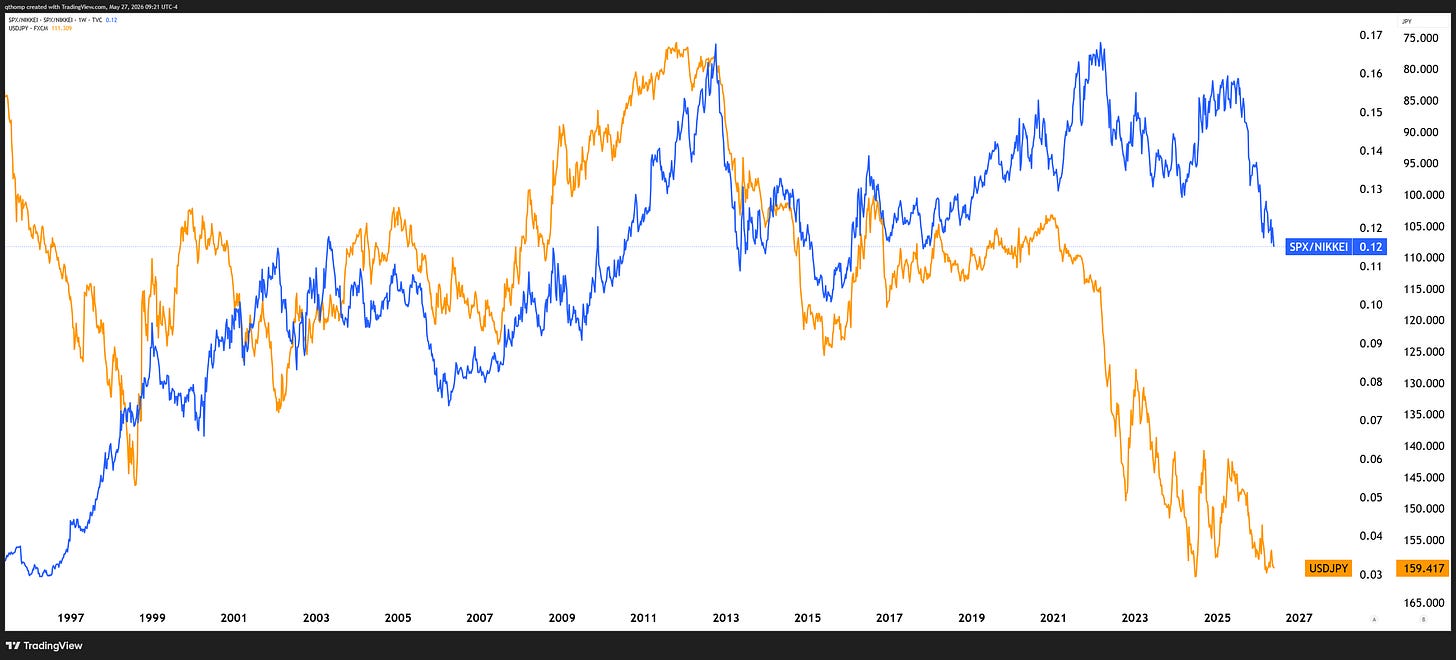

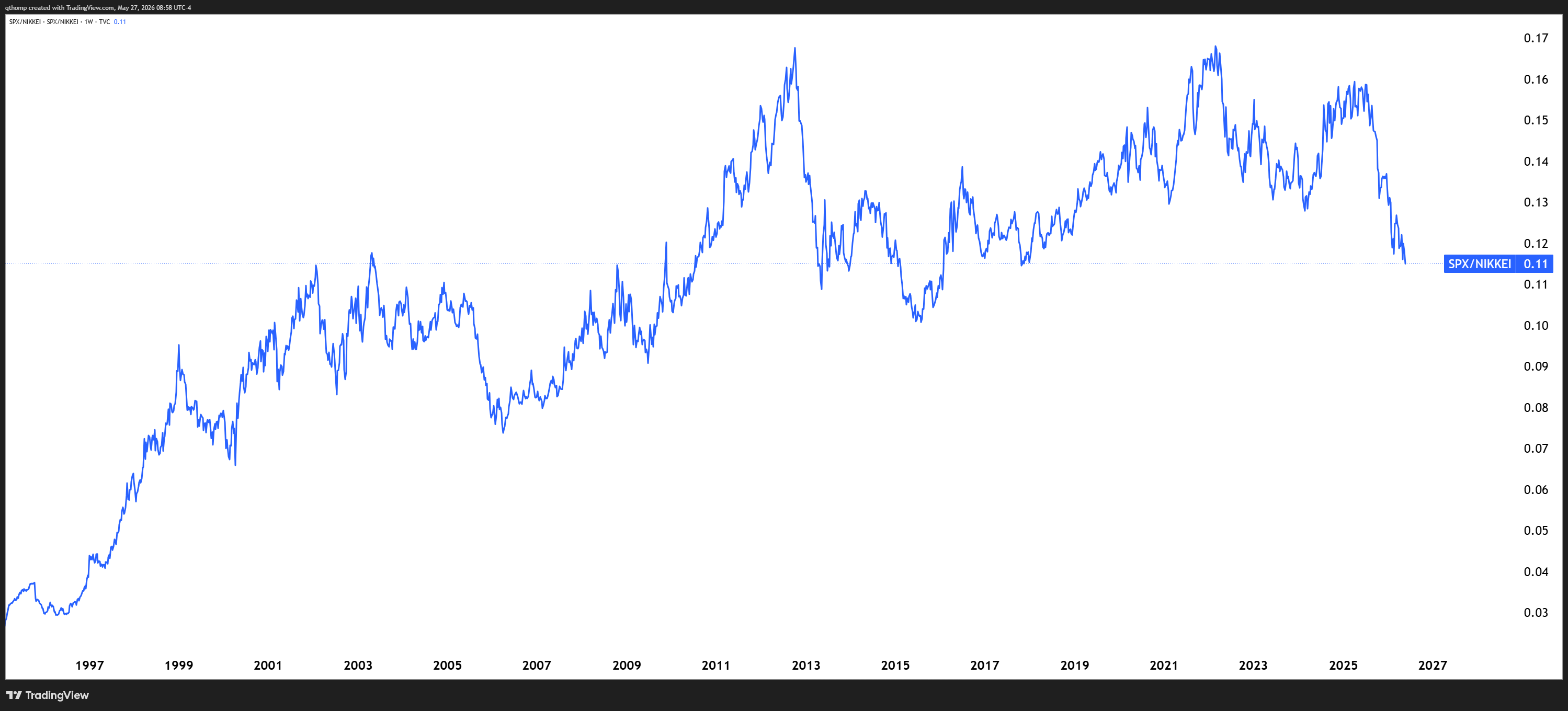

S&P 500 / Nikkei ratio in constant currency basis. Equity valuations in Japan are not quite what they are in the US, but on a relative historical basis they are becoming more elevated.

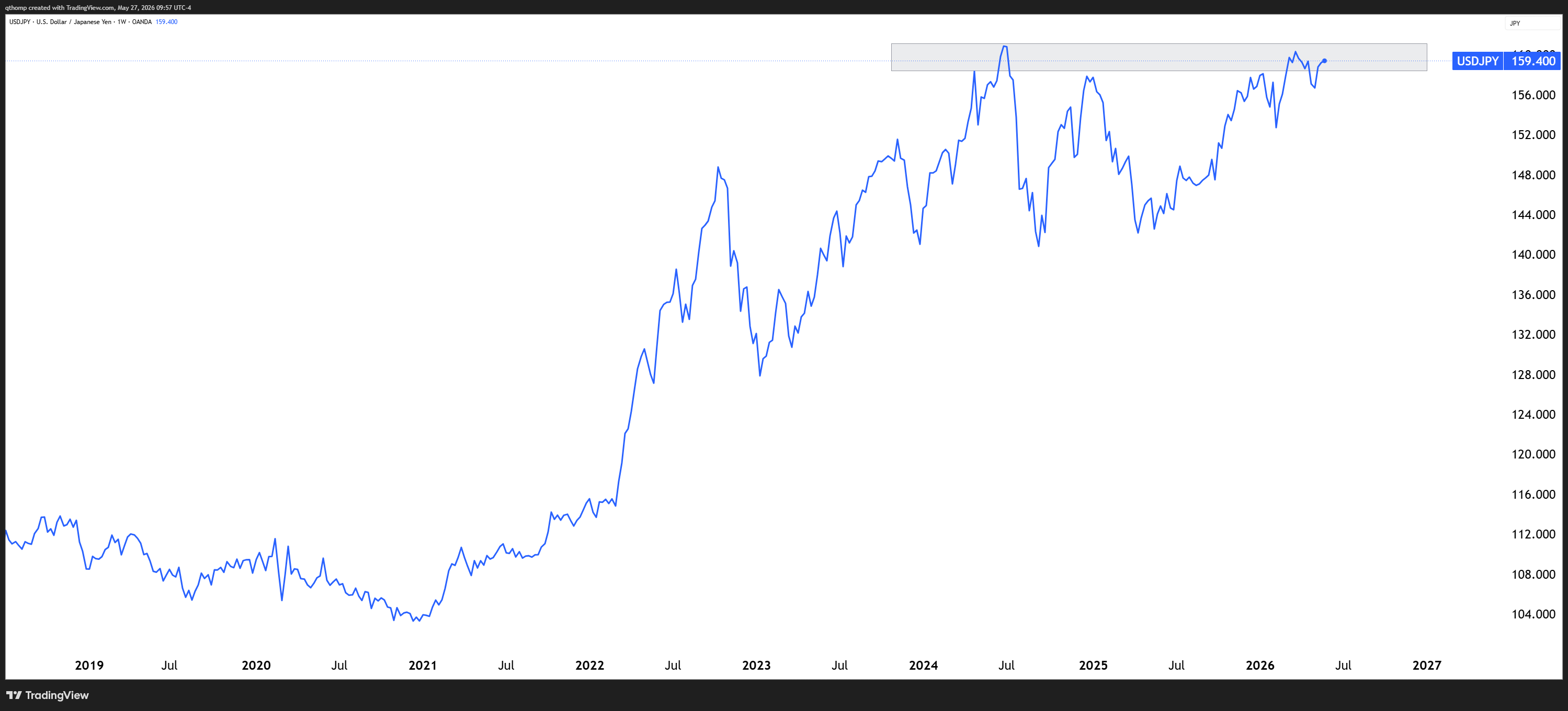

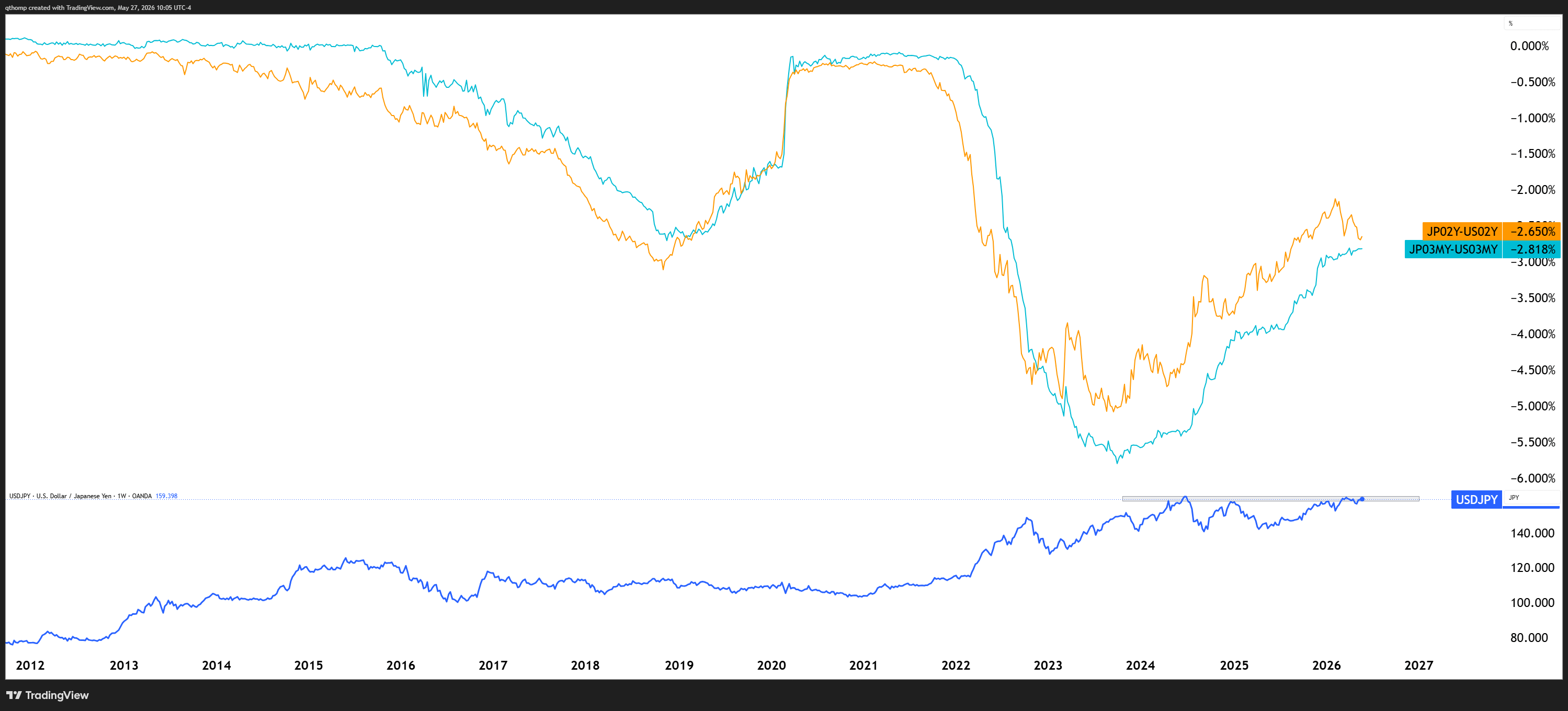

Here’s that same SPX/Nikkei chart from above with USDJPY (inverted) added in orange. For the last 20 years, the relationship has been fairly steady whereby weaker yen leads to Nikkei outperformance and stronger yen leads to S&P 500 outperformance. This wasn’t always the case though as you can see that relationship reversing in the late 90s as well as throughout most of 2021. Interestingly, that late 90s period where the Yen weakened while the S&P 500 outperformed the Nikkei in the infamous dot com bubble occurred under Fed chair Greenspan who is often cited by Bessent and Warsh as their model policymaker for today. You can also see that the Yen has been extremely weak since 2022 which makes me wonder how much longer the USDJPY ceiling holds.

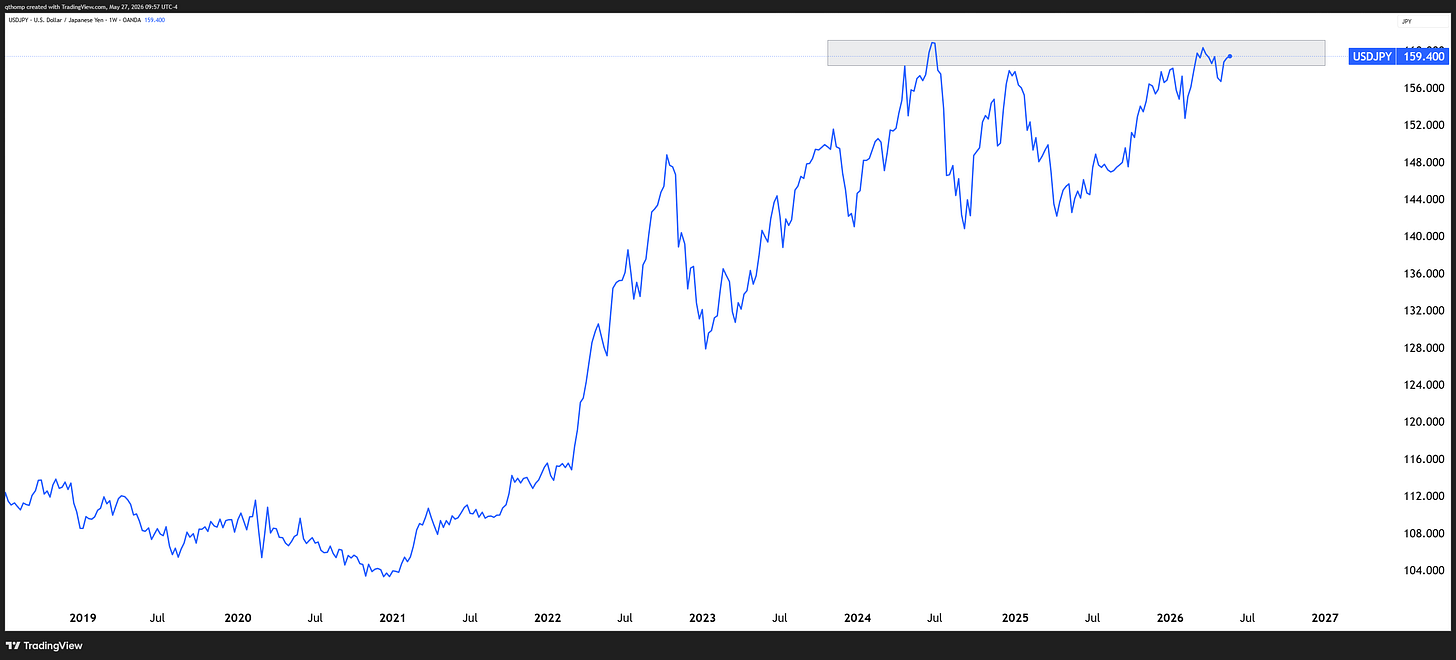

With USDJPY trading back into its heavily defended 160 area, it really boils down to a policy decision as to what happens from here. This is one of the reasons why Trump has come to the table with Iran to reopen the Strait of Hormuz despite no success in the war. If he continues to disrupt commodity flows and keeps prices elevated, it would force the BOJ to turn hawkish and do more to strengthen the Yen to fight inflation. This would not be good for risk assets and would go against Trump and Bessent’s goals of keeping markets propped up into midterms.

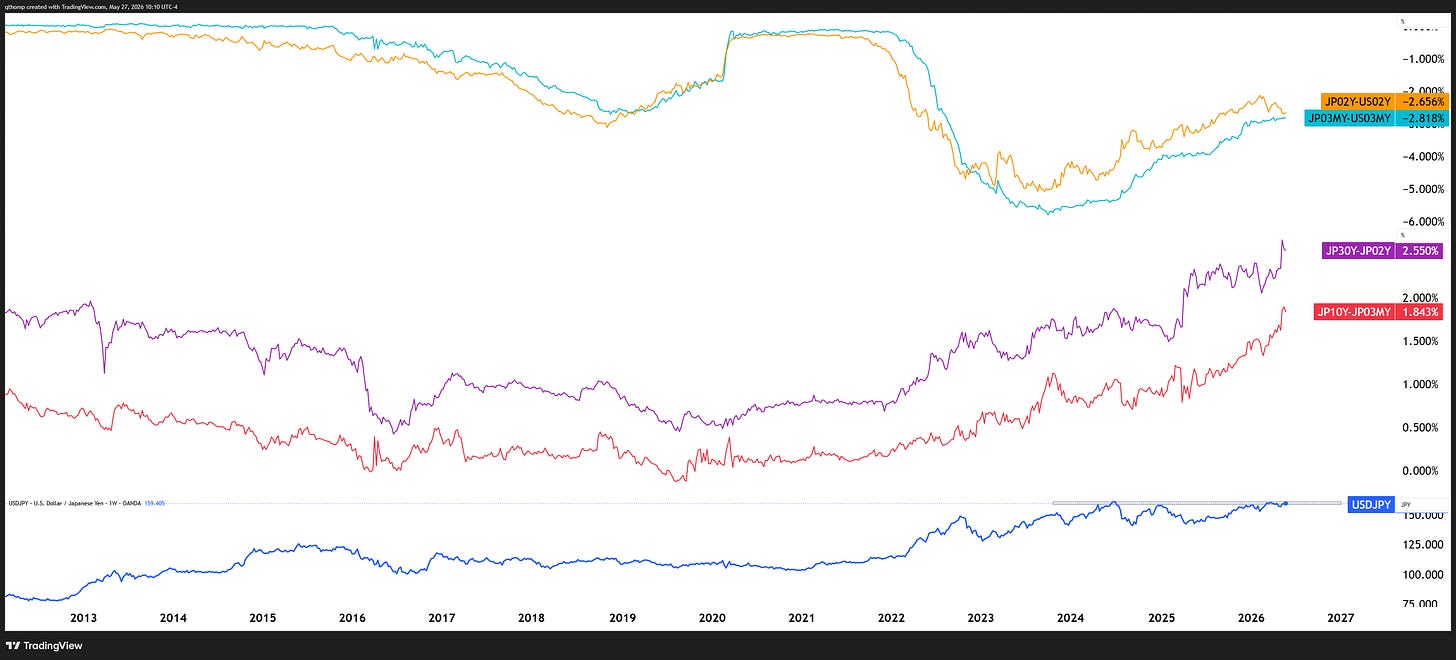

The only way to durably defend the 160 USDJPY level outside of temporary currency interventions is for the BOJ to adopt a more restrictive policy stance. Short-term rates in Japan are 250-300 bps lower than in the US and have been since 2022.

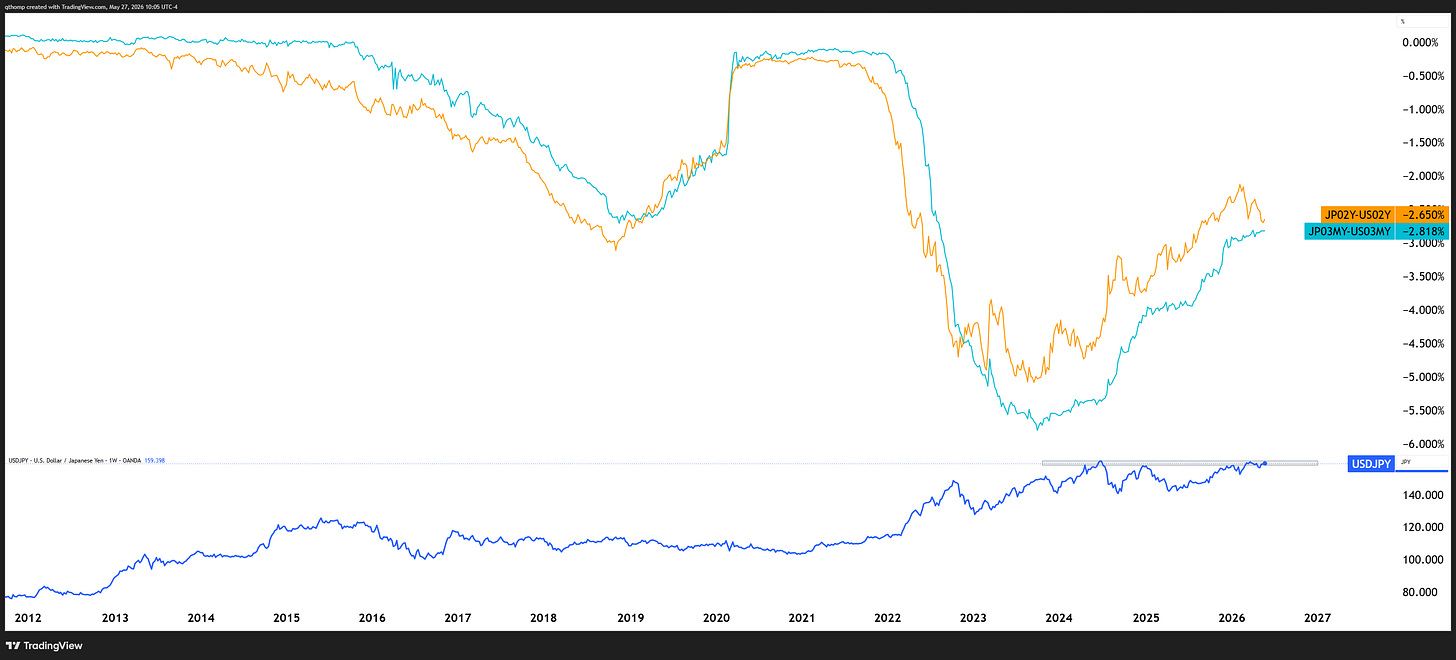

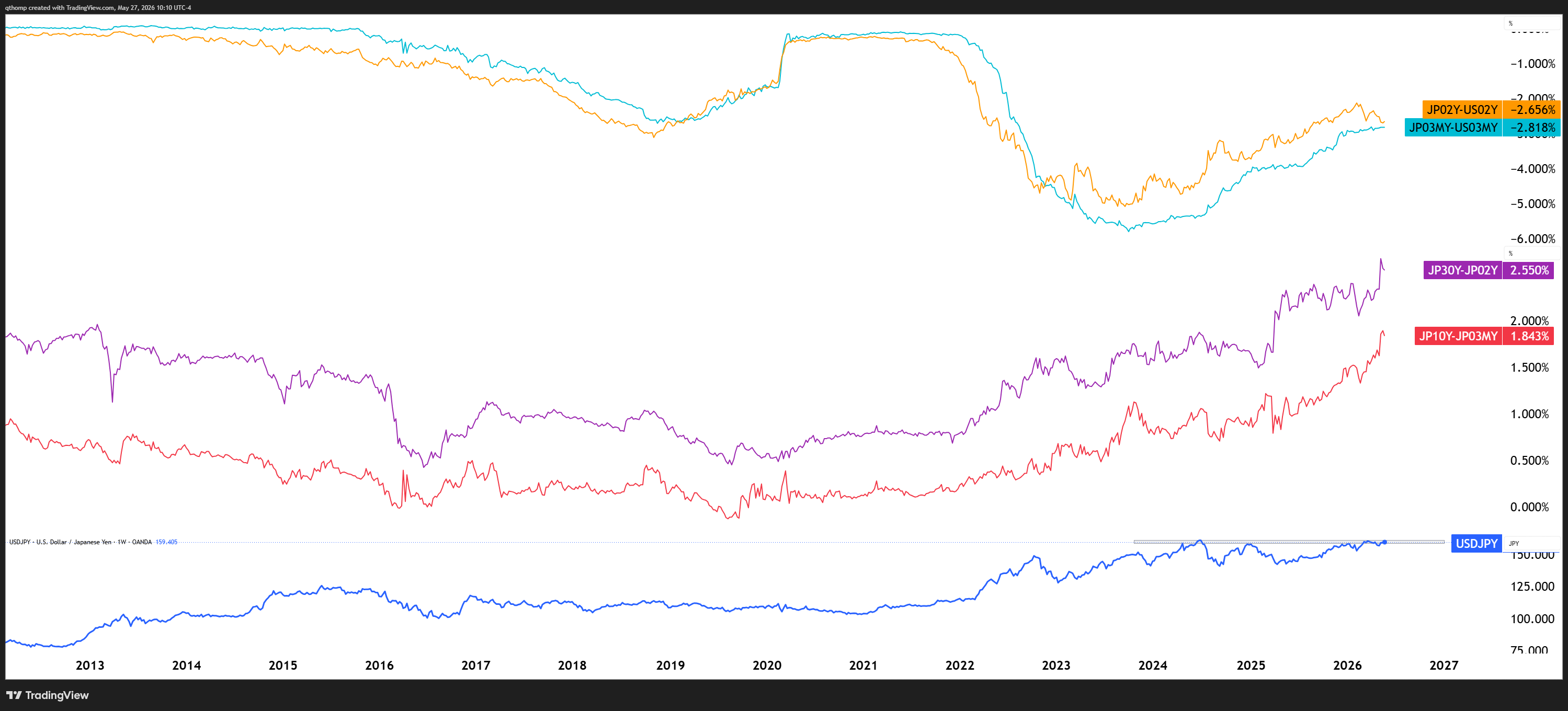

This loose monetary policy is causing a record yield curve steepening in the JGB market. Presumably this starts to matter at some point, but given the lack of reaction thus far when they’ve been breaking out to record levels for the past year, it is difficult to say when.

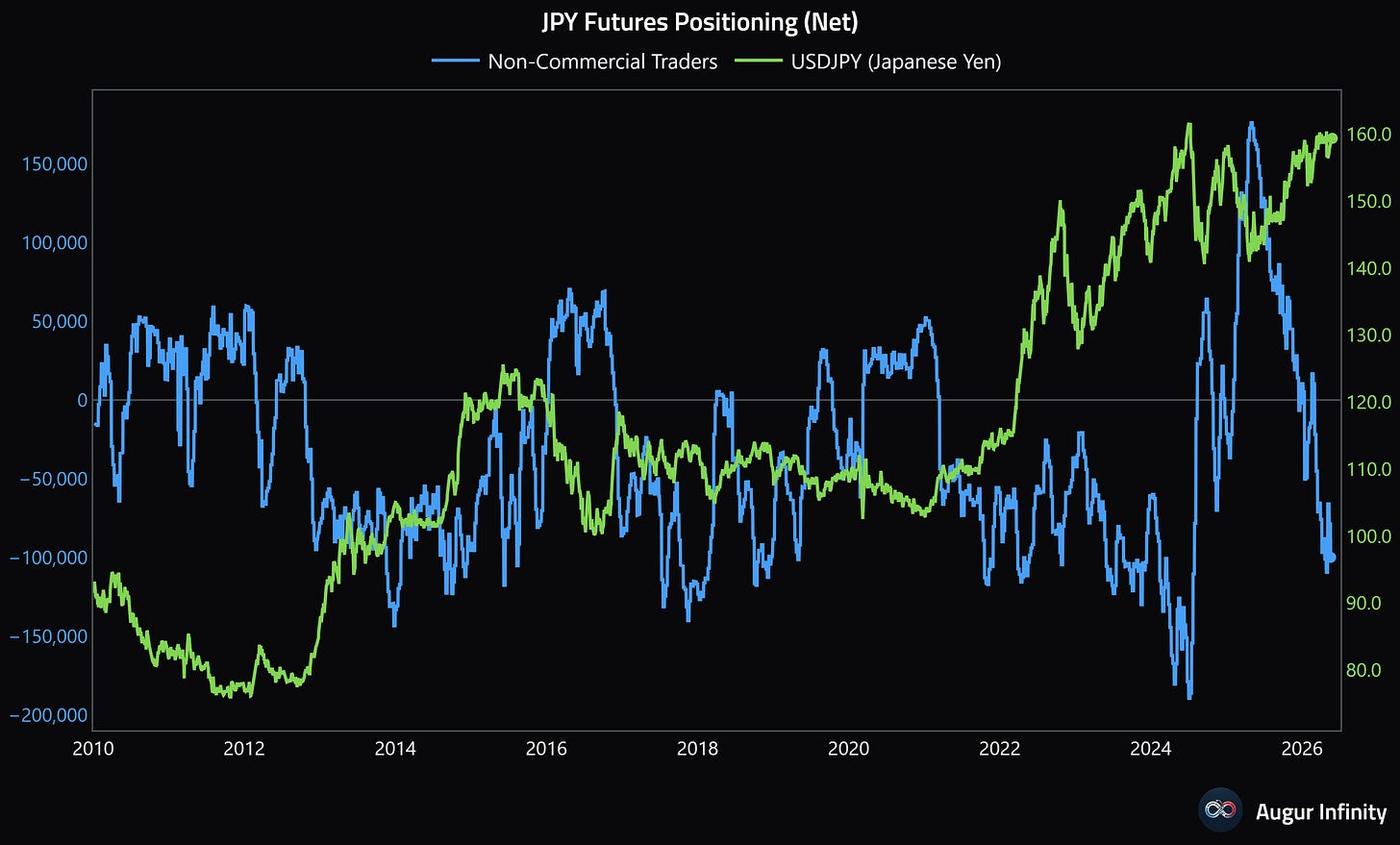

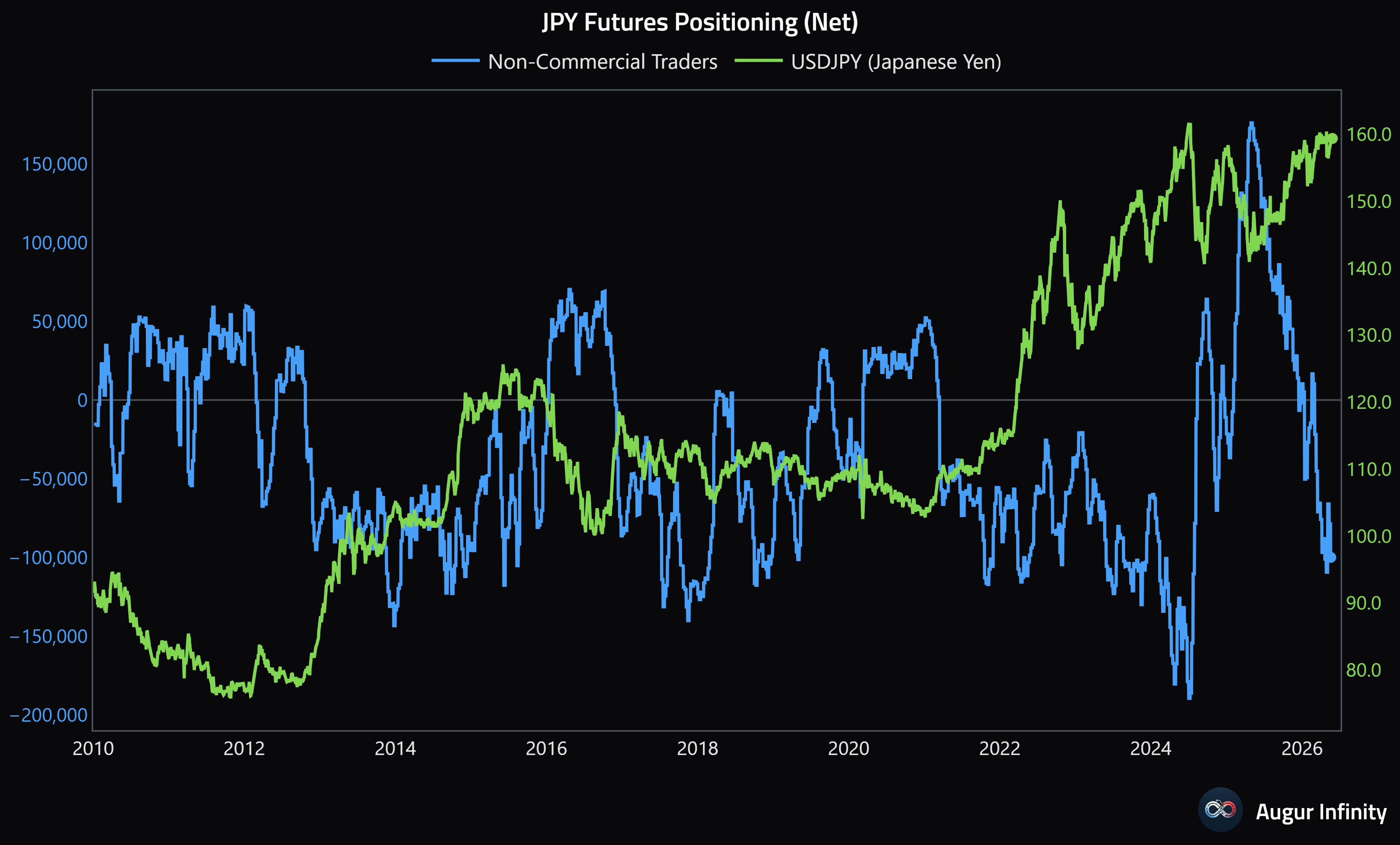

Yen speculative short positioning is present but its just over half of what it was in the summer 2024 peak.

Unfortunately I don’t have many answers for you at this juncture, but I do believe this area of the market will become increasingly relevant over the coming months so it remains top of mind. The yen was a good short 3 weeks ago when one of the largest BOJ currency interventions in recent years yielded one of the smallest magnitude movements, but now that USDJPY is back to the 160 area and Japanese yield curves are screaming for the central bank to tighten policy, I am inclined to look for Yen strength / dollar bearish bets here. The invalidation becomes more attractive the closer it gets to 160-161 because if they want to defend it again they’re going to have to send a stronger signal and really bat it down with more than just talk. On the flip side, if they continue to stand pat and USDJPY closes above the 161-162 area, it is unlikely to stop there.

Quinn Thompson@qthompFrom our latest @ForwardGuidance…”throwing good money after bad”… BOJ intervention >2x the size of recent Yen purchases with minimal impact.

zerohedge @zerohedgeA quick history of pass yenterventions: (1) Thu 22Sep22: ¥2,838.2bn / ~$19.8bn (@ USDJPY ~143.50) (2) Mon 21Oct22: ¥5,620.2bn / ~$37.7bn (@ USDJPY ~149.00) (3) Thu 24Oct22: ¥729.6bn / ~$4.9bn (@ USDJPY ~147.50) (4) Mon 29Apr24: ¥5,918.5bn / ~$37.7bn (@ USDJPY ~157.00) (5) Wed11:53 AM · May 1, 2026 · 9.92K Views2 Replies · 1 Repost · 32 Likes

zerohedge @zerohedgeA quick history of pass yenterventions: (1) Thu 22Sep22: ¥2,838.2bn / ~$19.8bn (@ USDJPY ~143.50) (2) Mon 21Oct22: ¥5,620.2bn / ~$37.7bn (@ USDJPY ~149.00) (3) Thu 24Oct22: ¥729.6bn / ~$4.9bn (@ USDJPY ~147.50) (4) Mon 29Apr24: ¥5,918.5bn / ~$37.7bn (@ USDJPY ~157.00) (5) Wed11:53 AM · May 1, 2026 · 9.92K Views2 Replies · 1 Repost · 32 Likes

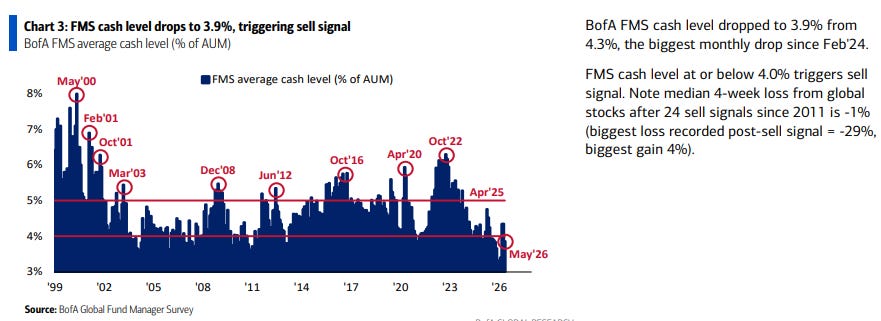

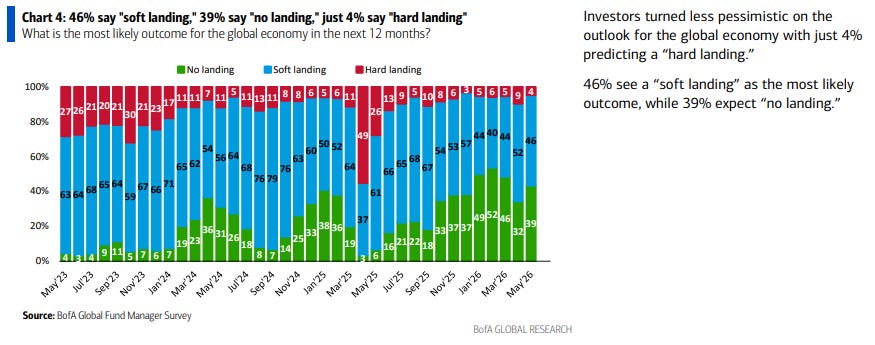

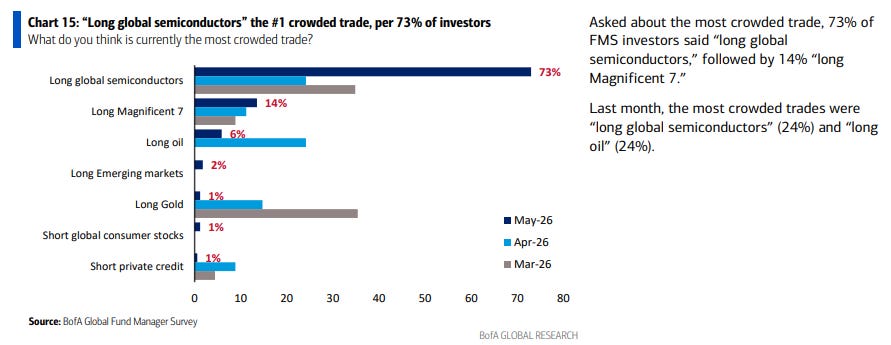

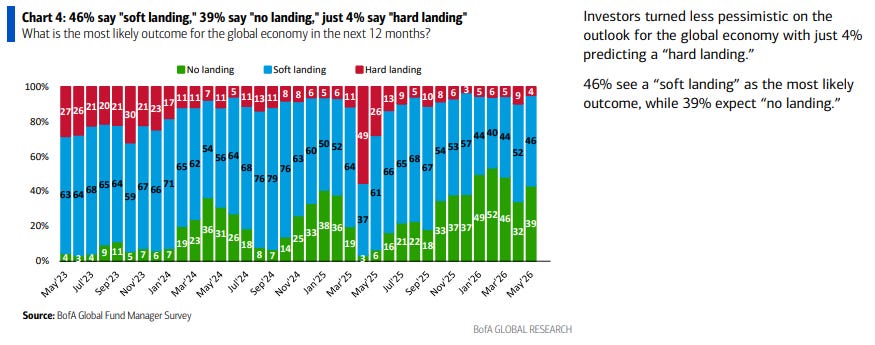

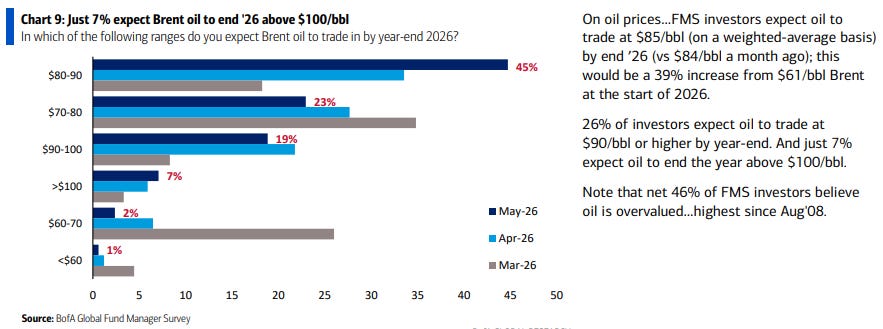

BofA fund manager survey highlights.

There weren’t many surprises in the recent Bank of America fund manager survey but I thought I’d share a few charts. Investors are pretty bought into the economic reacceleration and overheating risks given the looseness of financial conditions, and rightfully so. This has helped to influence both the hawkish shift in rate policy expectations as well as the upside chase in equities.

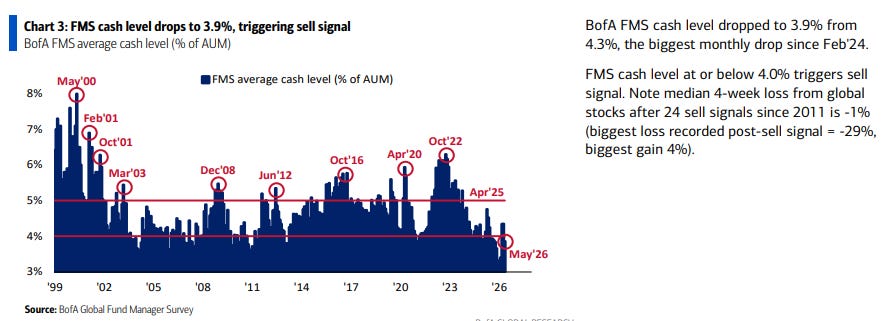

Investors cash allergies are flaring up again as the administration's loose financial conditions have people avoiding the sidelines at all costs.

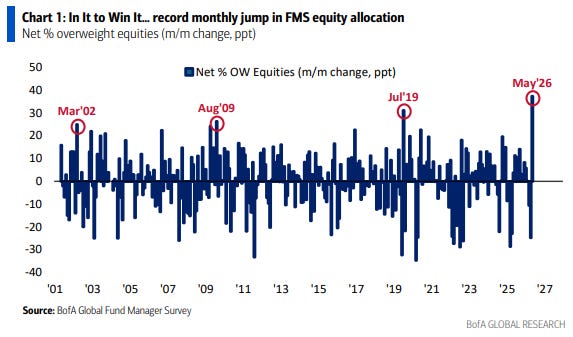

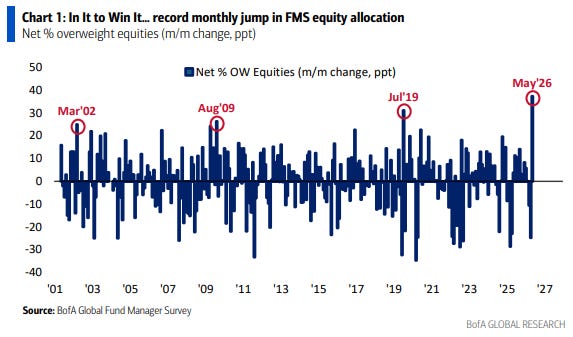

Equity buying has started to become more intense in recent weeks.

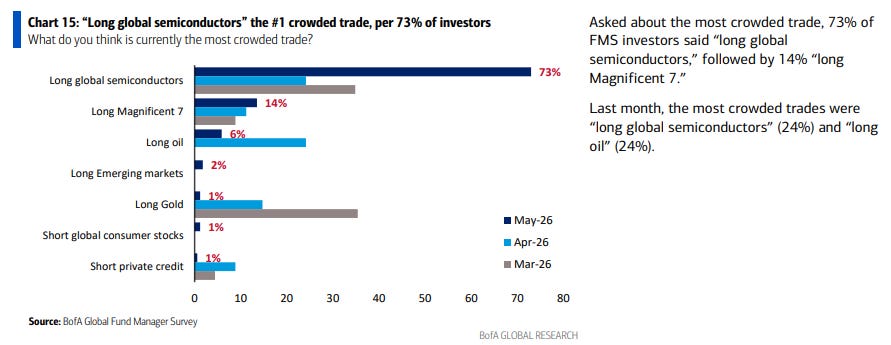

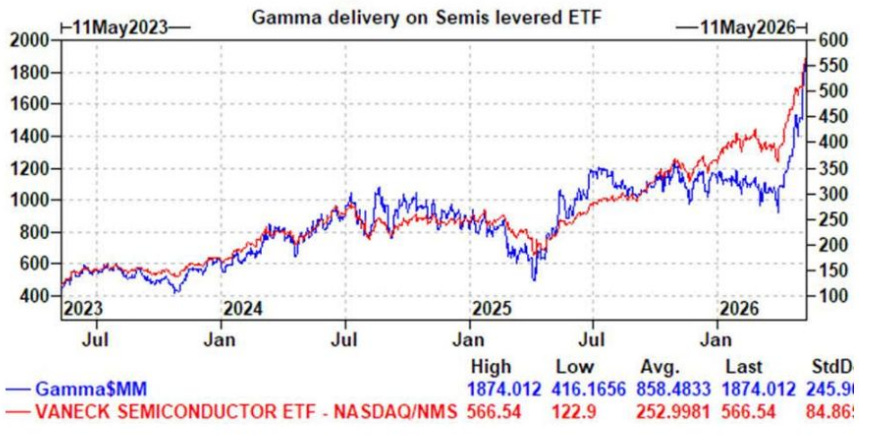

Unless you live under a rock you could guess that semiconductors is the most crowded trade.

Expectations for the economy are back to where they were before the Iran war - understandable given how intertwined the equity market wealth effect is with AI capex driving earnings driving higher stock prices driving consumer spending.

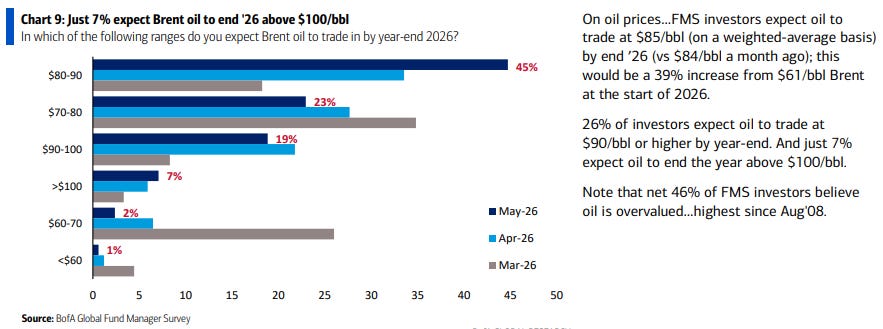

I was a bit surprised by this one but given how backwardated the oil curves are it makes sense. The Trump administration also has given themselves 170 million barrels of SPR drainage to work with which should be more than enough for them to manipulate prices lower ahead of midterms. Whether that is prudent longer-term policy is a different question.

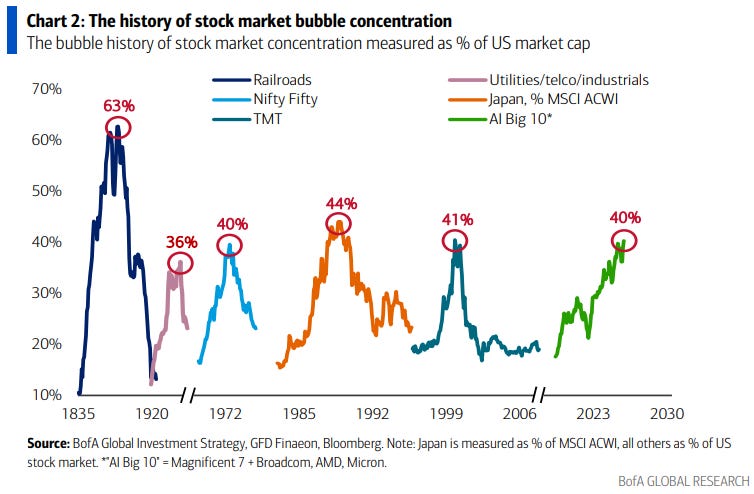

Let’s call it “late cycle” so as to not scare away any tech bulls.

The term bubble has become so divisive. It’s never a good thing when emotions are triggered on any side of investing. At the end of the day we’re just clicking buttons on a computer and trying to make money. These market conditions will cause even the most experienced market participants to lose their marbles. Try to stay sane and open minded.

I spent a lot of my earlier years in finance working in various energy and commodity sectors so this tweet from Milton resonated and is something I’ve been talking about on numerous occasions. At the end of the day semiconductors are extremely cyclical and while historically the Mag7 names haven’t been, their transition into capex heavy business models will very likely make them or at least their cash flows much more so. This has important ramifications.

Milton W Berg CFA@BergMiltonCyclical Stocks 101: Final highs don’t come at high P/Es. They come when earnings are peaking and P/Es look deceptively “cheap.” Semis—especially MU—are classic: they screen undervalued right before the cycle turns.

Milton W Berg CFA@BergMiltonCyclical Stocks 101: Final highs don’t come at high P/Es. They come when earnings are peaking and P/Es look deceptively “cheap.” Semis—especially MU—are classic: they screen undervalued right before the cycle turns. Gunjan Banerji @GunjanJSMicron now trades with a ~10x multiple S&P 500 has a P/E ratio of ~21x12:00 AM · May 27, 2026 · 153K Views70 Replies · 79 Reposts · 885 Likes

Gunjan Banerji @GunjanJSMicron now trades with a ~10x multiple S&P 500 has a P/E ratio of ~21x12:00 AM · May 27, 2026 · 153K Views70 Replies · 79 Reposts · 885 LikesThis chart is sure to ignite emotions on both sides of the aisle.

October 2025 was the most recent local peak in the broader tech sector relative to the rest of the market. Something to be mindful of when thinking about where to position the long side of your portfolio over the coming months.

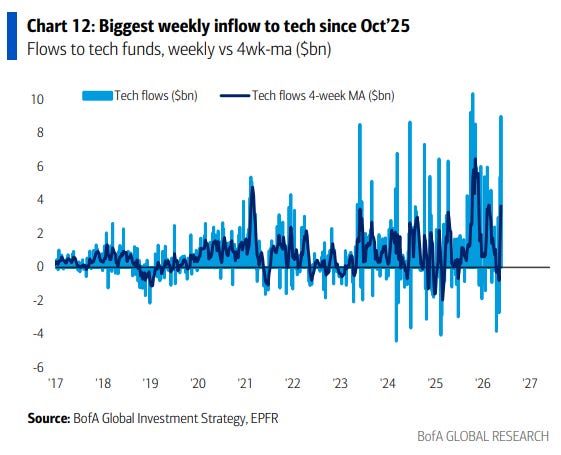

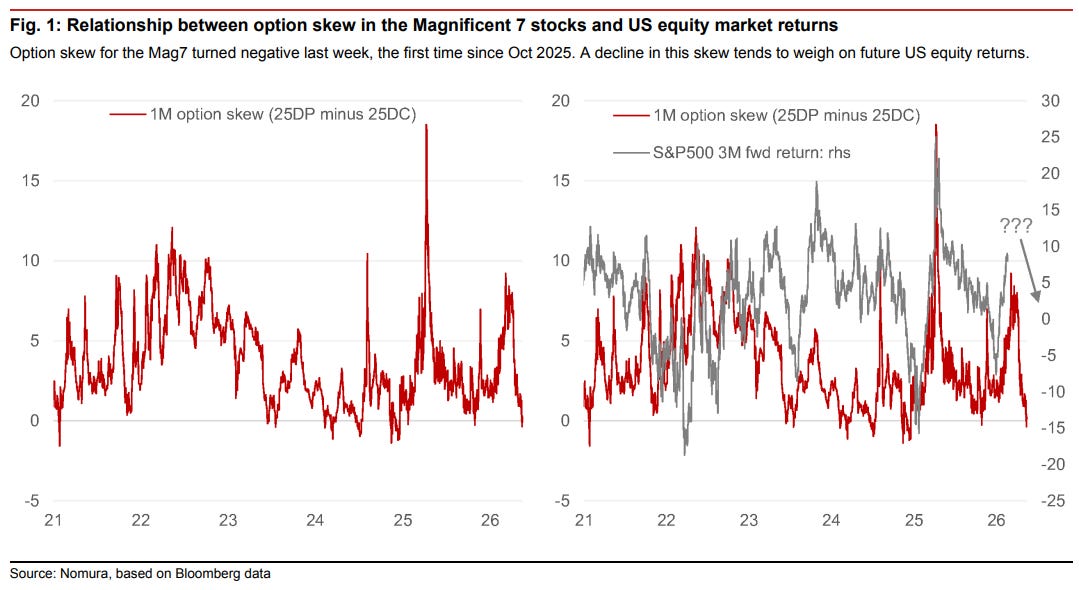

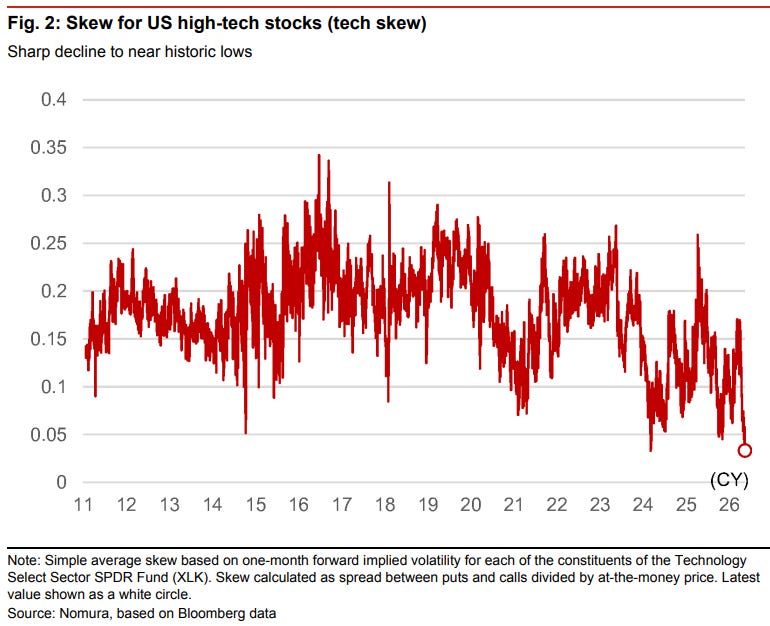

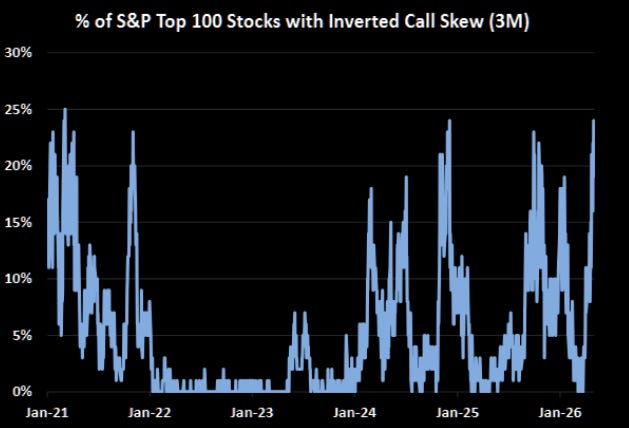

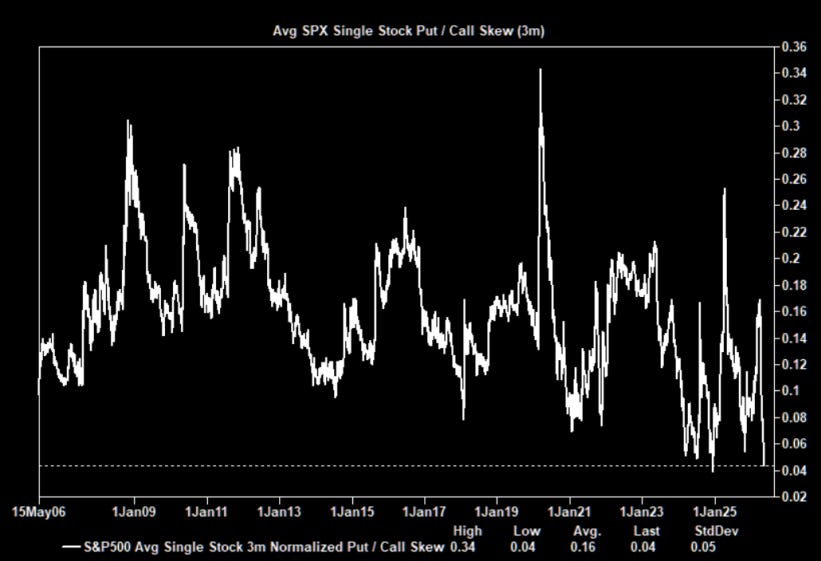

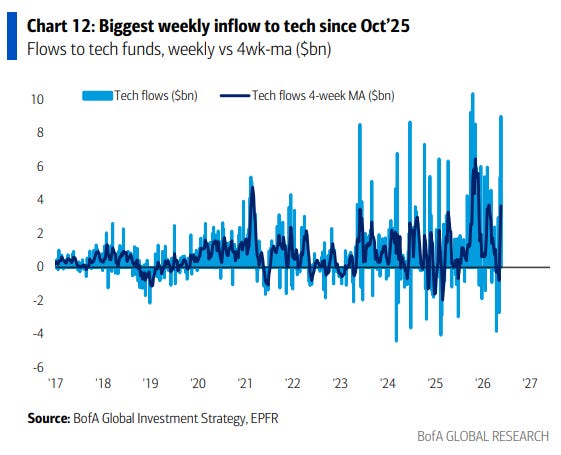

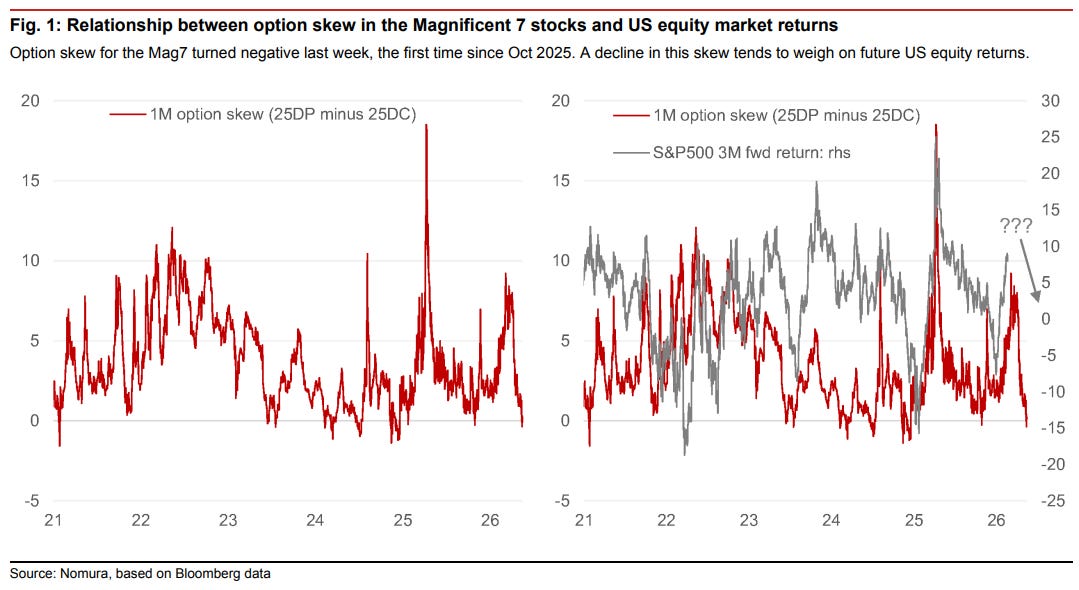

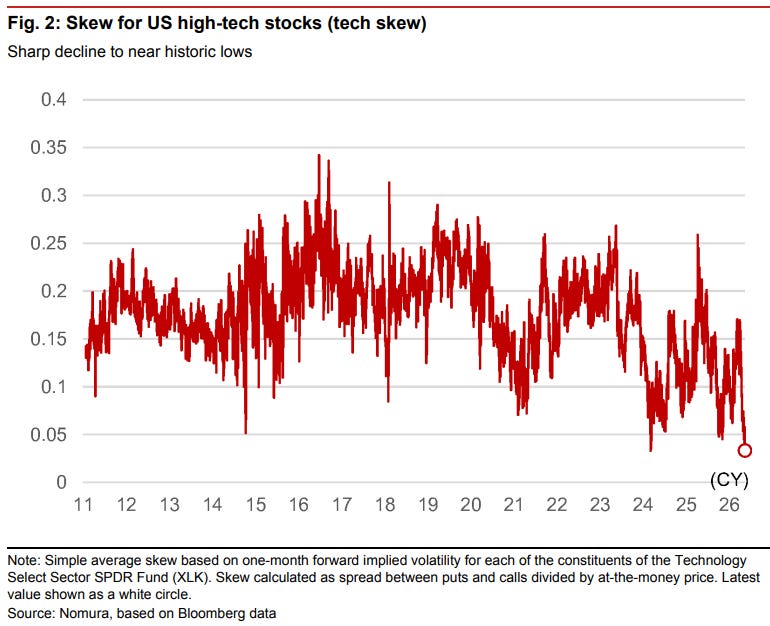

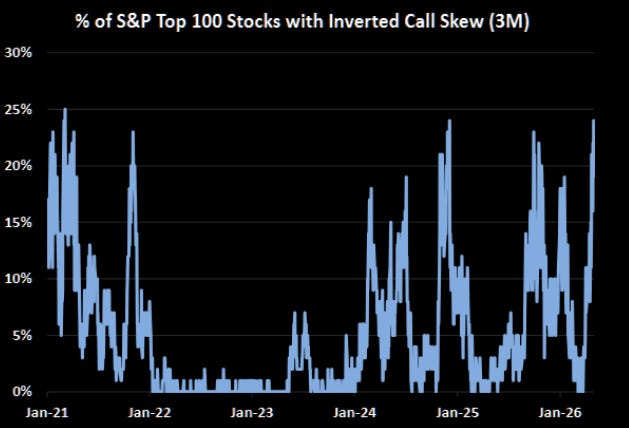

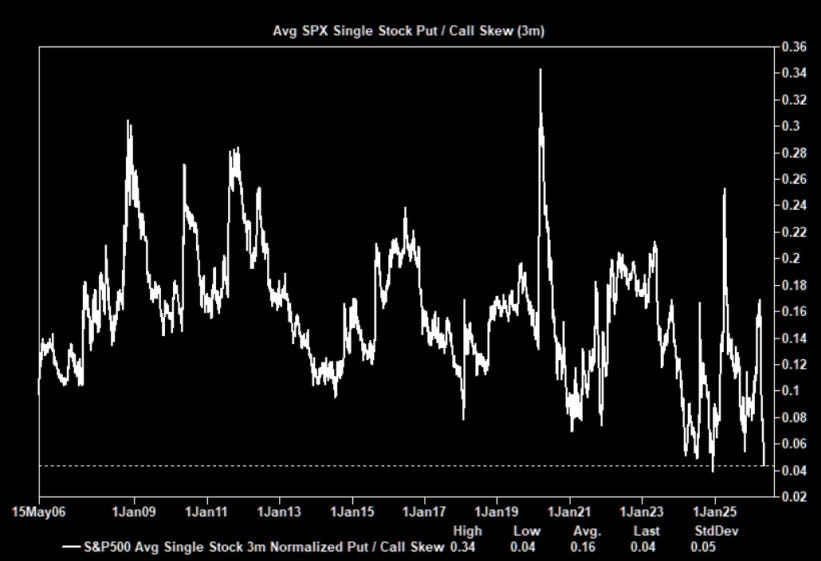

Mega-cap tech and AI is where all the vol is. Said another way, the benign volatility at the index level is masking the upside chase into tech and AI, where it has been spot up, vol up. Some great charts from Nomura on this below.

In one report they wrote “US tech skew suggests 100% probability of reversal”. Timing remains highly uncertain because these moves often end with unrelated macro catalysts rather than a fundamental lights out to the narrative. Moral of the story is that it’s time to have your head on a swivel. Bubble or no bubble who really cares - reading the data for what it is just says to be careful, not when or what is going to happen next.

Upside panic is back, reminiscent of 2021, which we’ve been pointing to as a corollary for a few weeks now.

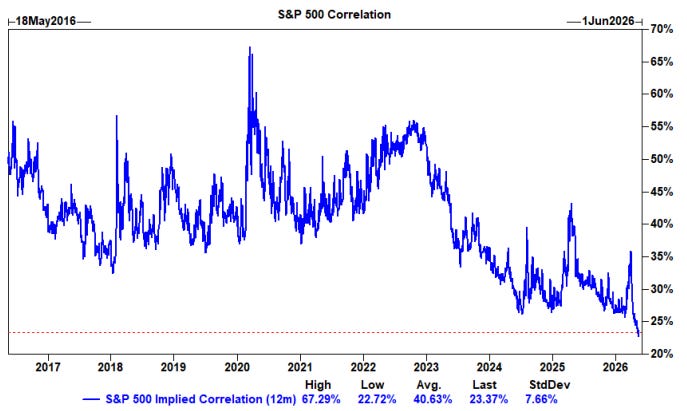

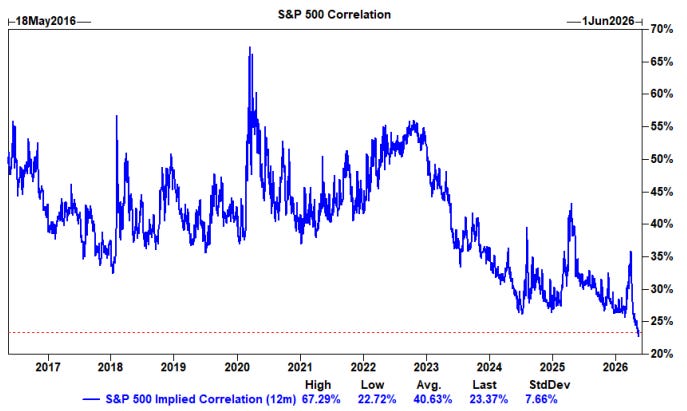

Record levels of dispersion (lows in correlation) is something to watch given earnings season is now behind us which is a big driver of idiosyncratic moves. If you can find longs in unloved and uncrowded sectors that are performing well, that is the ideal setup.

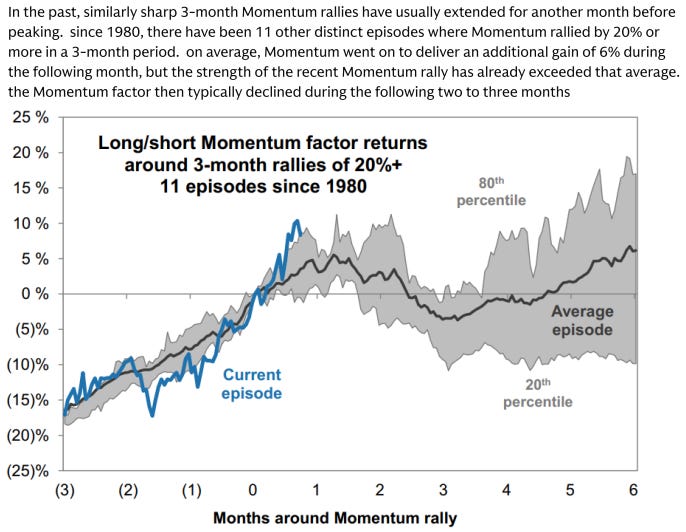

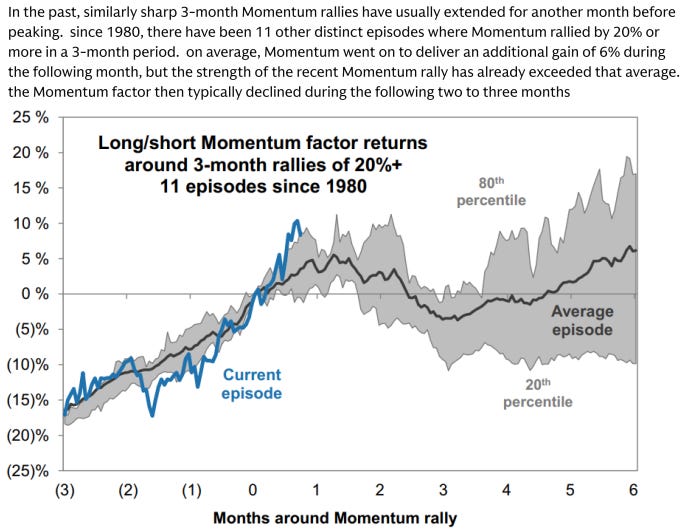

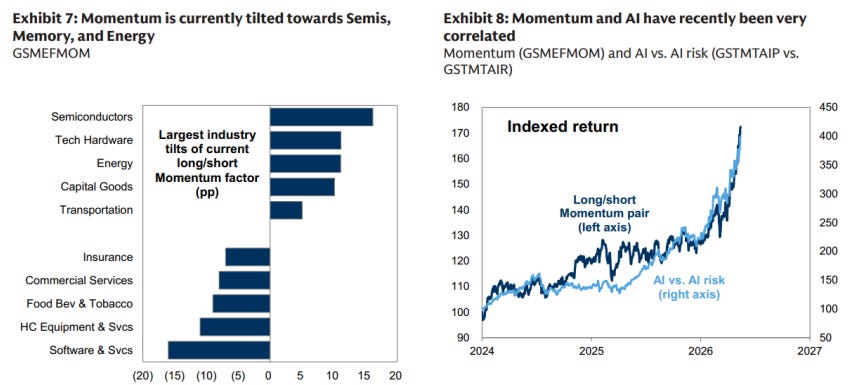

Momentum has been the engine of this market.

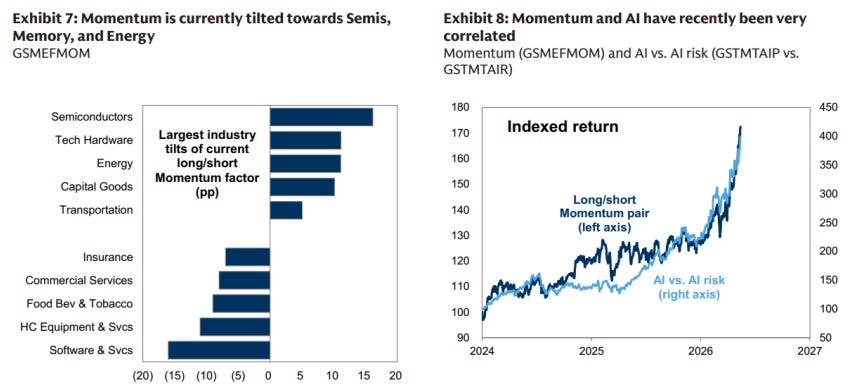

“Momentum” is basically just tech and semis.

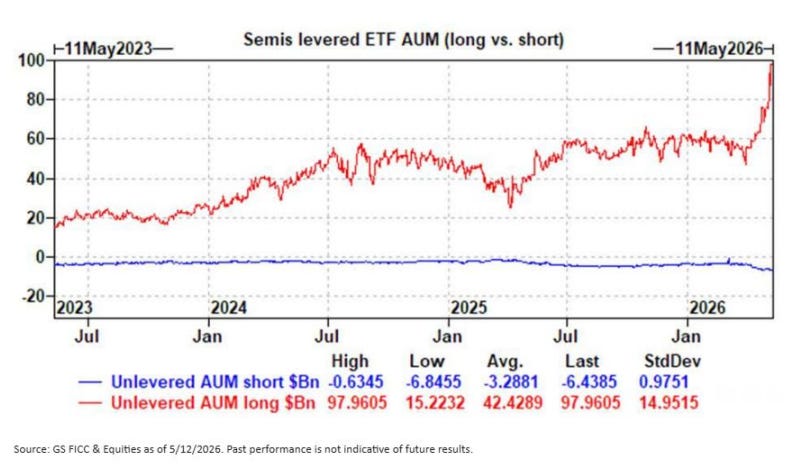

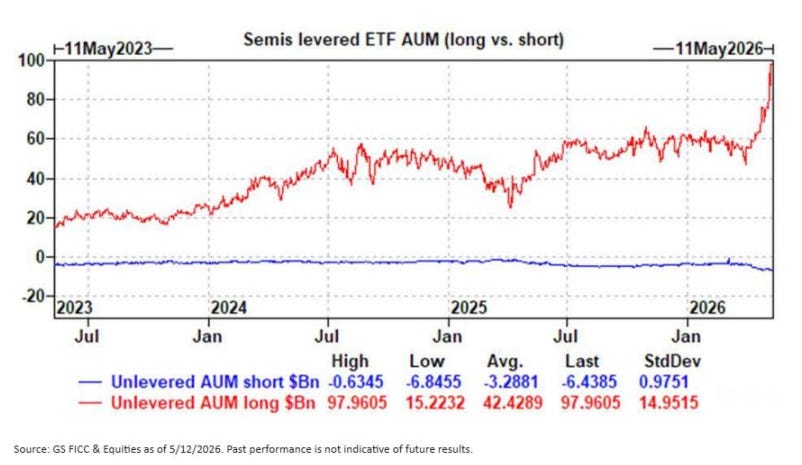

And one of my favorites which is a few weeks old that we covered on the podcast but figured it was a relevant place to share it again. Semiconductor leveraged long ETF AUM has grown from <$50B to >$100B in <2 months. Truly remarkable stuff. The other day someone asked me if I think everything is priced into semis. I chuckled because when the main drivers of stock movement start coming from leveraged ETFs and retail gambling, I would say the answer is a resounding yes that everything is priced in. But on the other hand, when was the point everything was priced into 2021? The answer to that is many months before the peak.

Record Bitcoin ETF sale.

Last week I wrote about the problems plaguing the crypto market. BTC and ETH are in the process of putting in their 3rd straight losing week and I don’t expect a drastic improvement in the outlook anytime soon.

This week there was a $1.26 billion, single block sale of IBIT, the largest Bitcoin ETF. It gives me similar vibes as last year when the whales were unloading into the late summer price pumps. This seller took a 2.3% discount on their coins, costing them ~$30 million to cleanly transact in one go.

A trade like this makes everyone ask the age old question, “does someone know something?” It’s not a surprising data point to me given I am seeing more and more people starting to understand the dilemma facing MSTR and BMNR, the two DATs who have been the largest buyers of crypto this year.

Strategy in particular is in a precarious spot given their more complex capital structure that includes convertible debt and high dividend rate preferred equity securities that dilutes the MSTR common stock. The moral of the story is Saylor has some balance sheet fortification to do before leaning into BTC buys again.

Quinn Thompson@qthompTBD whether or not $STRC holders will get a dividend rate increase announced in a few days.

Michael Saylor @saylorAll-time high volume. $1.53B of liquidity. Two cents of volatility. Closed at par. $STRC12:25 AM · May 29, 2026 · 6.64K Views26 Likes

Michael Saylor @saylorAll-time high volume. $1.53B of liquidity. Two cents of volatility. Closed at par. $STRC12:25 AM · May 29, 2026 · 6.64K Views26 LikesNYDIG had a good write up examining the trade closer that I encourage you to read if interested.

Over the coming weeks, I expect I’ll have more trade ideas and actionable thoughts for you than the last few weeks. It’s been difficult for me to achieve the same level of conviction that I was playing with in Q1, but that’s normal. Market environments ebb and flow and it’s important to know your style so you can recharge and preserve capital to maximize returns when your systems work best.

I hope everyone has a great weekend!

Excellent as always

Thanks, another great one!

"If you can find longs in unloved and uncrowded sectors that are performing well, that is the ideal setup."

Why, if correlations are at the lows now, wouldn't higher correlations during a sell off mean everything down, instead of previously shorted names up?