Scouting the Tape - Apr 29, 2026

(Unique) macro idea generation and (insightful) market thoughts.

Now that Powell’s last meeting as FOMC chair will be behind us, the market must start looking forward to Warsh’s leadership. This Scouting the Tape is focused on what I am seeing as a major problem boiling to the surface. Bonds-R-F’d. This is my favorite new meme for sovereign debt markets, the US in particular.

If you haven’t yet, I suggest giving last week’s Scouting the Tape a read. It is separate but related to what I go into below and will help paint the full picture of everything I am thinking about.

Scouting the Tape - Apr 24, 2026

This week’s issue is focused on global FX and bond markets. It is often said that if you get the dollar right, you will get a lot of other things right. I think that will hold true over the coming months and this part of the market is not getting enough attention.

The most consistent message from Warsh, Miran and Bessent is their interest in shrinking the Fed’s footprint in financial markets.

This looks like at a minimum reducing the duration of the Fed’s balance sheet (currently ongoing slowly) and at a maximum reducing the size of the Fed’s balance sheet (currently not happening - balance sheet is growing thanks to RMPs).

This approach allows the Treasury market to serve as a natural governor on congressional spending and fiscal profligacy.

This in turn raises long end bond yields, all else equal, thus creating a headwind for asset prices and creates a steeper yield curve which helps to even out the playing field for main street and Wall Street by removing the suppressed yield curve that has inflicted pain on front end borrowers (small businesses and low and middle income wealth cohorts) and disproportionately benefited long end borrowers (large corporations and wealthy individuals).

Given the stock market effectively is the economy today, dampening equity indices slows the economy. This is what could allow the Fed to cut interest rates further, assuming inflation is under control (which it isn’t). The problem is the White House and Treasury do not allow stock market corrections and utilize their fiscal and currency tools to manipulate equities higher, thus continuing the inflation persistence.

The facts as they stand, however, don’t necessarily paint a clean picture and suggest that Warsh, Miran and Bessent’s actions might not follow their words.

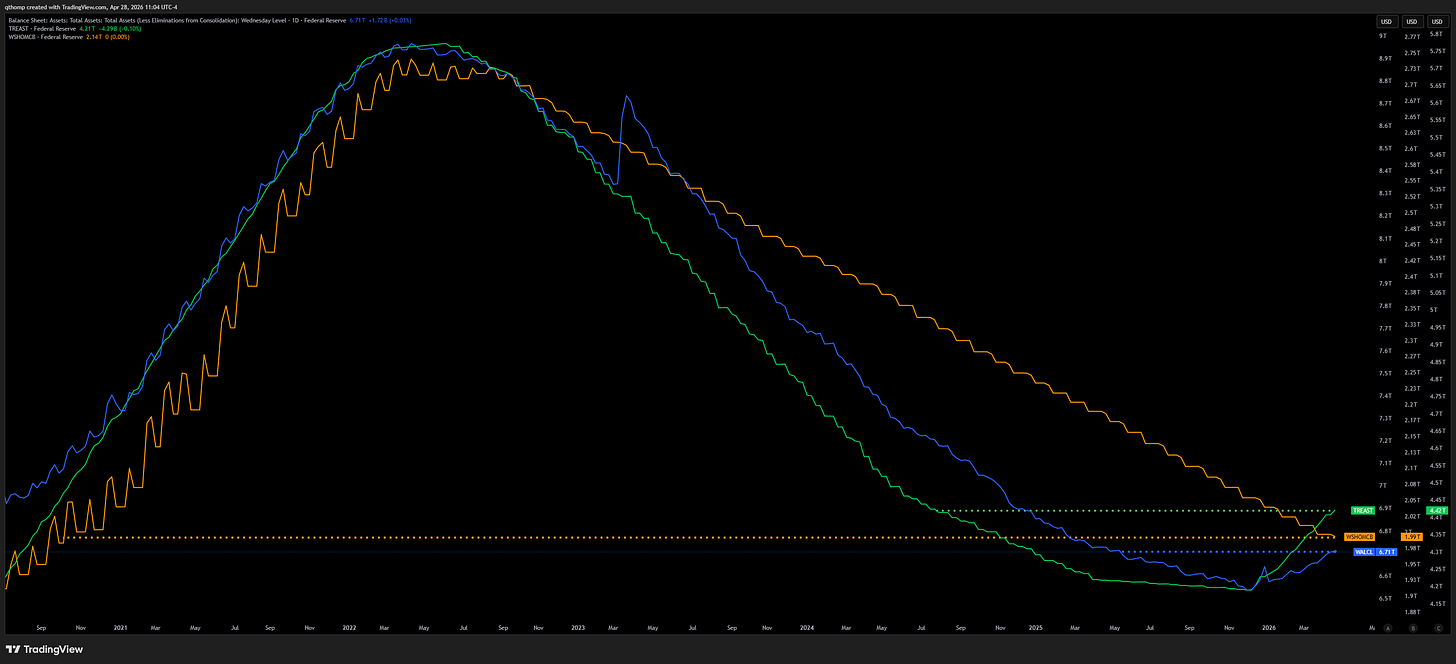

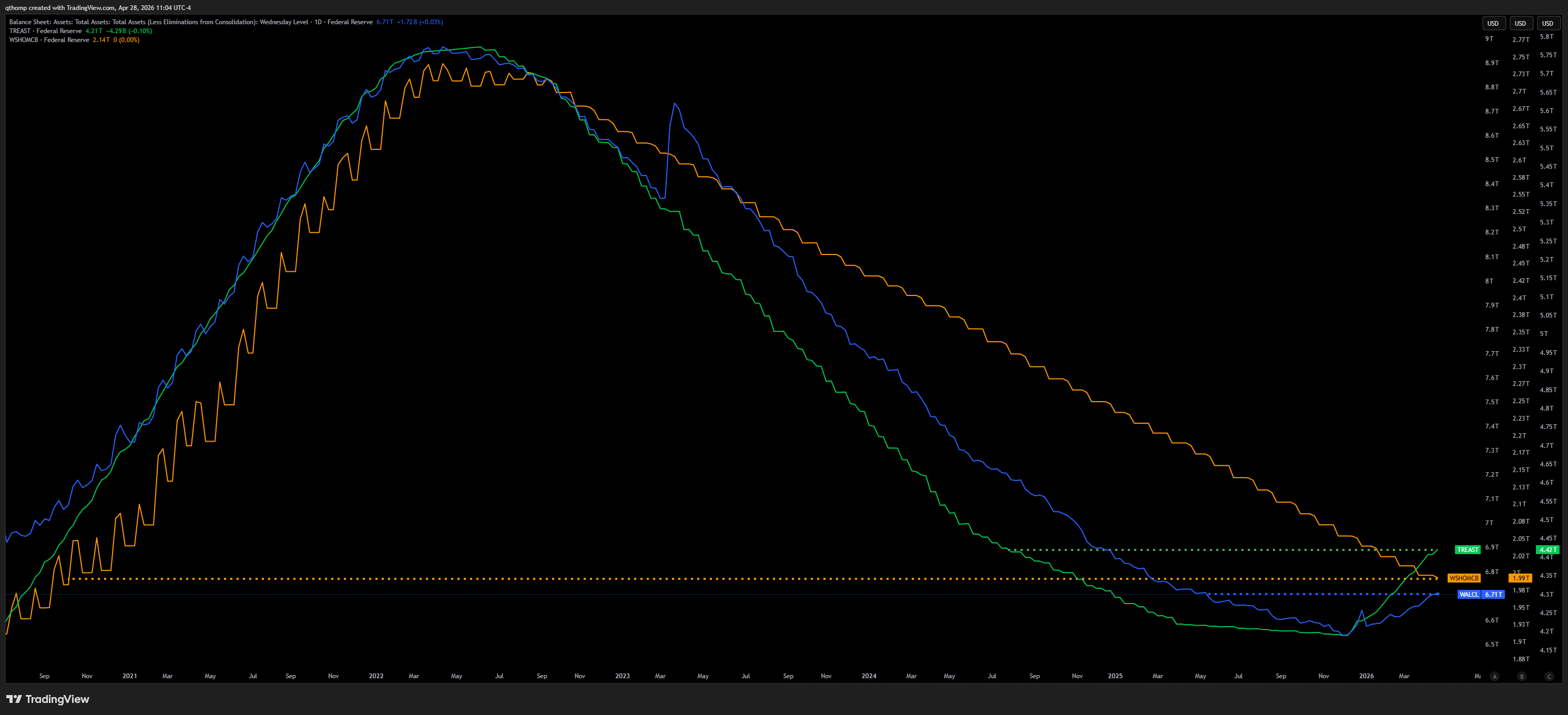

For starters, the Fed’s balance sheet began growing again in December 2025. This has been led by ‘Reserve Management Purchases’ of $40B/month. They are supposed to taper down after April, but it remains to be seen what Warsh will do here. If rate cuts are off the table because of an inflation problem (as appears likely), I could easily see him increasing these to support the front end in a different way - it is de facto QE. The chart below shows while the Fed’s MBS holdings have continued to fall, now back to October 2020 levels, the rise in Treasury holdings back to July 2024 levels has brought the total balance sheet increase back to May 2025 levels.

While Bessent, Miran and Warsh have voiced their discontent with the previous administration’s use of Active Treasury Issuance (ATI) as a covert form of yield curve control, they appear to be hypocritical given their usage of the same exact tools. We will find out more in next week’s QRA but the seeds were sown in February’s QRA. I wrote about it here:

And now most recently in his confirmation hearing, Warsh spoke numerous times about data overhauls and revamping at the Fed. While on the surface they will say this is to improve accuracy, the reality, just like Trump’s replacement of BLS staff and canceling of key data releases, is to fudge the numbers to paint the picture they want it to paint - the opposite of accuracy.

There’s an overarching takeaway here which is that ‘financial policy’ as a whole (fiscal + monetary) has been almost completely taken over by the Treasury and White House. While I don’t think Warsh does himself any favors by refusing to disavow Epstein or acknowledge the 2020 election results, the truth is the Fed has not been independent for a long time now, especially since 2020. Yellen and Powell worked extremely closely through the various fiscal stimulus and bond market liquidity measures, just with less of a loud public focus on the issue. The trajectory is for this independence to continue to weaken - both out of desire by current leaders and frankly necessity given the problems have gotten so bad that closer coordination is required to avoid disaster or crisis (which may not be unavoidable in the end).

Another bout of inflation is largely baked in the cake.

2025 saw one of the largest efforts in recent history to curtail profligate government spending, yet all that could be mustered was a small reduction in the budget deficit.

The DOGE and shrinking the fiscal deficit Trump admin rhetoric was not all just talk. The federal workforce shrunk by ~10% in 2025 alone. The fiscal deficit as a percentage of GDP fell from ~6.3% in 2024 to ~5.8% in 2025. But that’s the problem - it’s still at 5.8% despite the major push.

Because the budget cuts targeted non-defense discretionary spending (which is only about 15% of the total budget) while increasing defense spending, the impact on the total federal deficit has been marginal. It was more of a reorganization than it was meaningful cuts.

Without budget cuts and a deficit to GDP greater than 5%, the government’s interest burden continues to grow at an exponential rate and forces the Treasury to pay the interest on its debt with the issuance of more debt. This is the type of behavior you see from troubled and distressed companies.

“It’s not possible for us to take care of day care, Medicaid, Medicare, all these individual things,” Trump said. “They can do it on a state basis. You can’t do it on a federal. We have to take care of one thing: military protection. We have to guard the country.” Wars are inflationary and we are in a wartime economy with no end in sight.

The closure of the Strait of Hormuz has created long-lasting physical shortages that will result in higher oil prices for longer - implying an inflation problem for at least the next year until the base effects fall out after Q1 2027, however the feed through of these price increases into and around the rest of the economy tend to take longer to work through. Eric Nuttall of Ninepoint and HFI Research have both been highlighting the significant decrease in US crude reserves. This reduces future resilience to supply shocks and will keep oil prices elevated into the future.

Immigration impacts are likely starting to feed through to wages. After the initial mass reduction in immigration was paired with tariffs and cuts to the government workforce to suppress economic growth in 2025, it appears the effects are now working through the economy. With green shoots appearing across the industrial and manufacturing base thanks to the capex boom and OBBB tax incentives, the labor market is now also showing signs of an uptick. With economic expansion in some of these industries now happening for the first time in years, hiring should follow. But with a lower supply of workers, particularly foreign born, that is likely to at a minimum keep wage growth steady, while at a maximum cause it to pick up from here.

Considering all of the above, paired with policymakers attempting to exert control over maintaining loose monetary policy, it’s very difficult to see how the US and rest of world avoid another serious bout of inflation over the next 12-24 months.

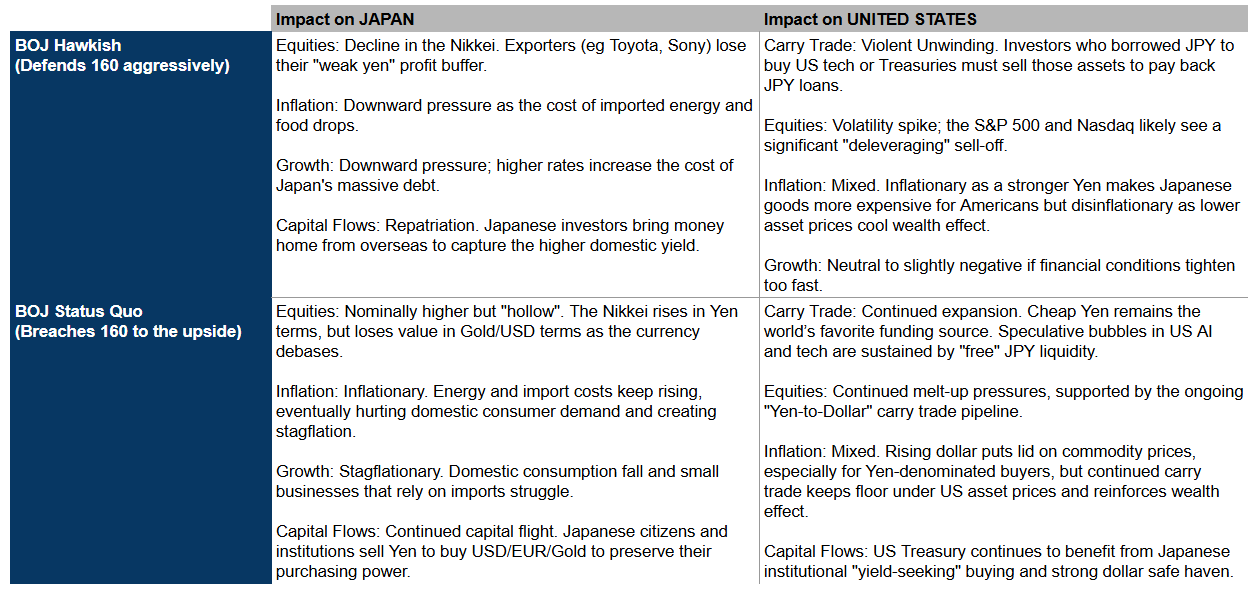

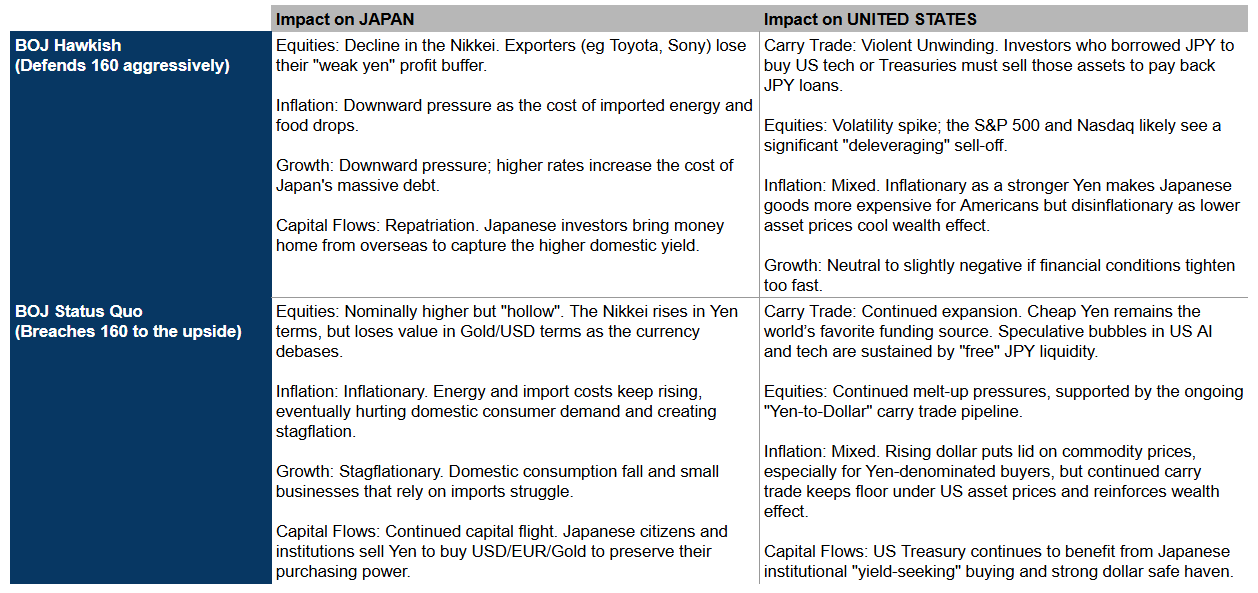

Gaming out US-Japan decision making.

Here is a scenario analysis of the two simplest paths (obviously there is a lot more nuance and levers to pull in reality).

What isn’t yet obvious to people is that it is now a lose-lose for Treasuries.

If the BOJ truly turns hawkish to defend 160 USDJPY, US Treasuries suffer from i) Japanese capital flight to repatriate back home, ii) a weaker dollar creating inflationary pressures domestically in the US and globally for commodity prices and iii) negative wealth effect of falling US asset prices that hurts tax revenues and worsens fiscal deficit.

If the BOJ maintains the status quo and allows USDJPY 160 to break higher, US Treasuries suffer from i) contagion from rising Japanese bond yields and ii) carry trade reinforcing positive wealth effect making inflation more persistent, while (iii) the stronger dollar helps to offset some of the commodity inflation.

I view the tensions here as Japan wanting to prevent a social crisis resulting from falling real wages and runaway inflation while the US wants to maintain the US asset bubble for as long as possible. From this perspective, Bessent and team are likely pushing for the BOJ to remain dovish to bolster global liquidity while using reserves to try to maintain the 160 level on USDJPY. In return the US is likely offering access to commodities and national security. Japanese policymakers are rightfully nervous about runaway inflation and may use threats of selling US assets and/or unwinding the carry trade in their negotiations, however given the unsustainability of their overleveraged fiscal position amidst a commodity supply shock likely know that defending the 160 USDJPY level is throwing good money after bad.

The BOJ, ECB and Fed will continue to work in close coordination as they always do. So if the ECB and Fed are both going to ignore inflation and stand pat in order to maintain economic growth, or even attempt to maintain an easing bias in the case of the US, there isn’t much incentive for Japan to turn hawkish.

There’s an argument to be made even one BOJ hike this year would not change the upward trajectory of USDJPY given their inflation and economic problems are much more dire than the US’s.

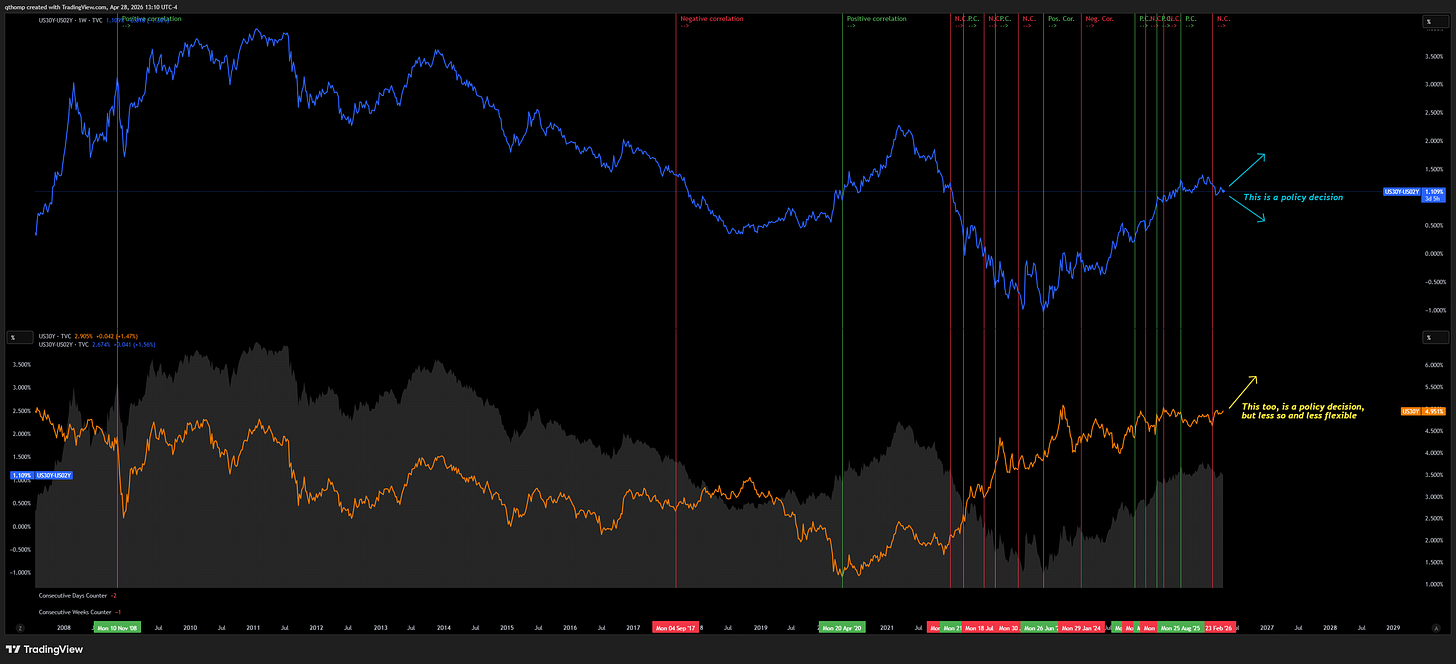

What is the market saying?

Here is the 30y - 3m yield curve. This is one of the most bullish charts on my entire watchlist.

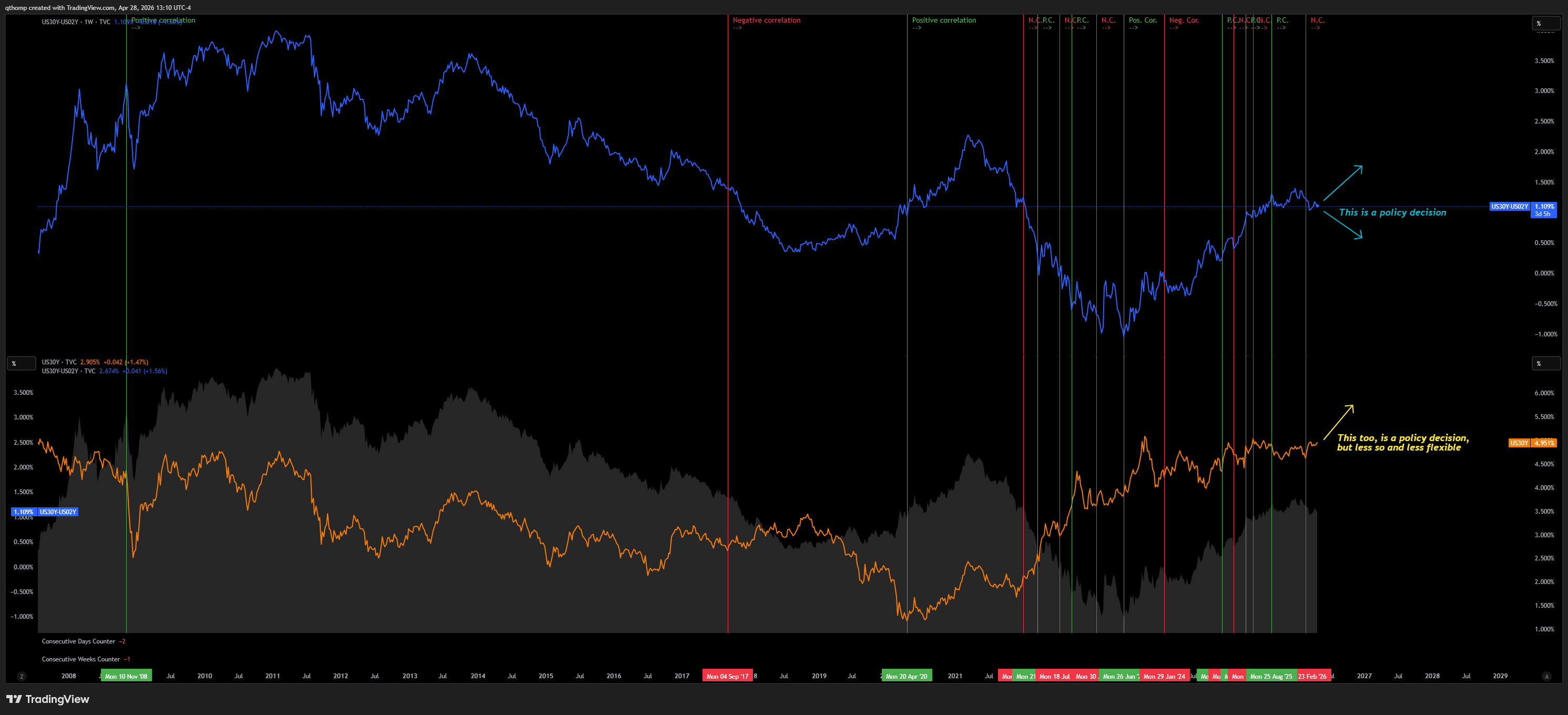

Below is a chart showing the US 30y-2y yield curve on top (blue) vs. the 30y yield on the bottom in orange. What you will notice is that for nearly 10 years following November 2008, the two moved together with a positive correlation. Then from January 2022 onward, the correlation has frequently alternated between positive and negative. Why did this start happening? The short answer is policy intervention to try to manage markets.

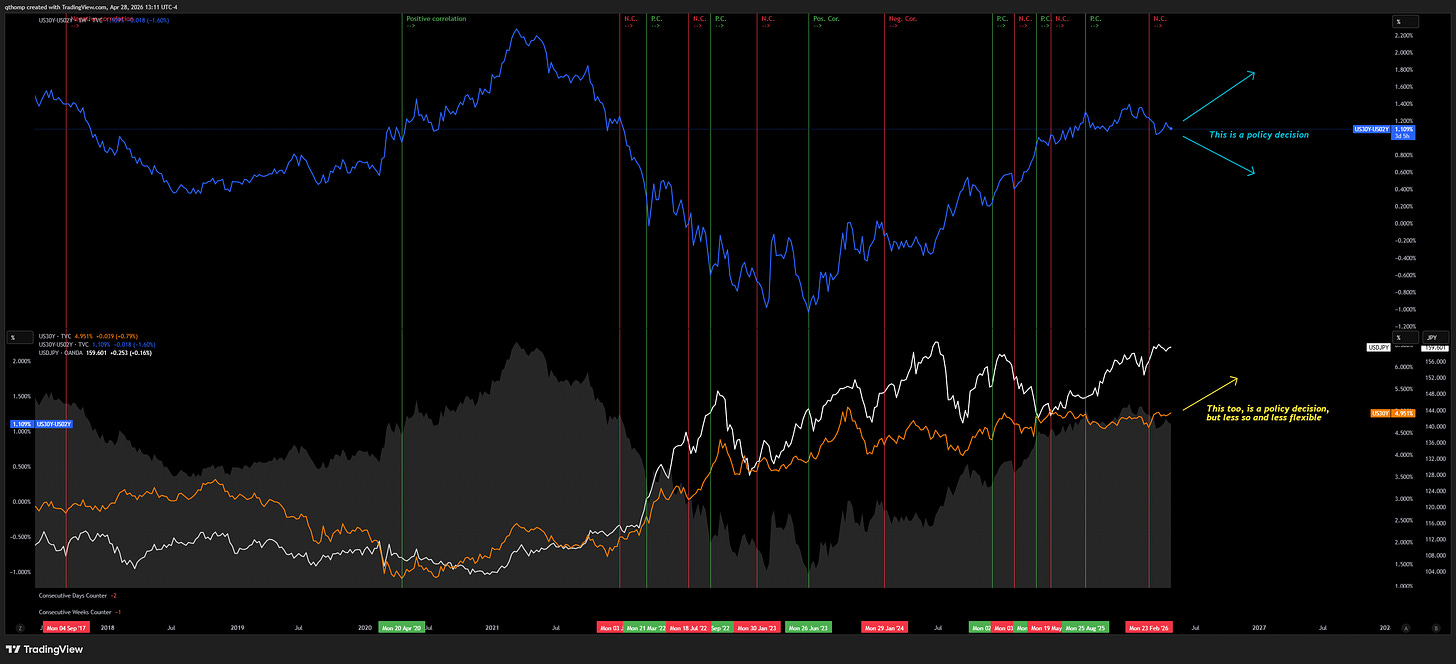

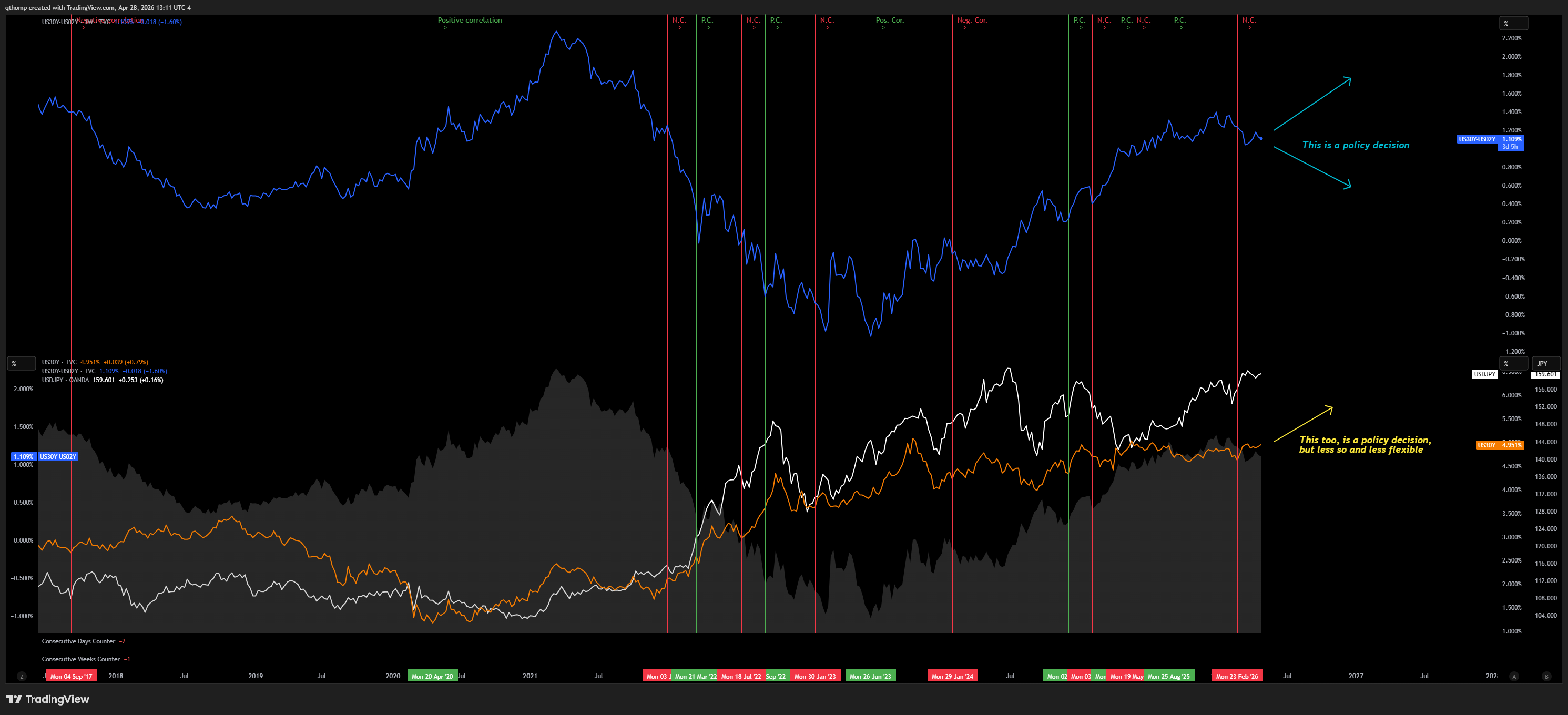

Why does this matter more now than in the last few years? In the below chart I’ve zoomed in further and added the USDJPY chart (in white on the bottom). You can see USDJPY is up against 160 and the 30y yield is up against 5% - both critical levels with competing priorities.

The free market approach would be to allow natural price discovery with both yields and the dollar strengthening, however we don’t live in a world of free markets anymore so we will await policymaker action to determine which way things move. There is a QRA meeting next week which very well could see the US Treasury further manipulate issuance to reduce pressure on bond yields. The problem is that with all of these volatility and market suppression tactics, they continue to make inflation pressures worse and risk a bigger problem down the road.

Channeling my inner Peter Brandt, the ascending triangle on the US 30y bond yield chart implies a 6.6% target (the widest height of the wedge). I understand Bessent and team’s desire to keep a lid on bond yields to support economic growth, but I believe it would be a mistake to continue manipulating this market lower as it would create a larger inflation problem down the road. The economy is already showing signs of reheating in the labor market, across wages and green shoots in housing - further suppression of rates to bolster liquidity will all but guarantee a meaningful overheating. However the presence of this risk of continued Fed and Treasury intervention is why it is imperative to own commodities and hard assets.

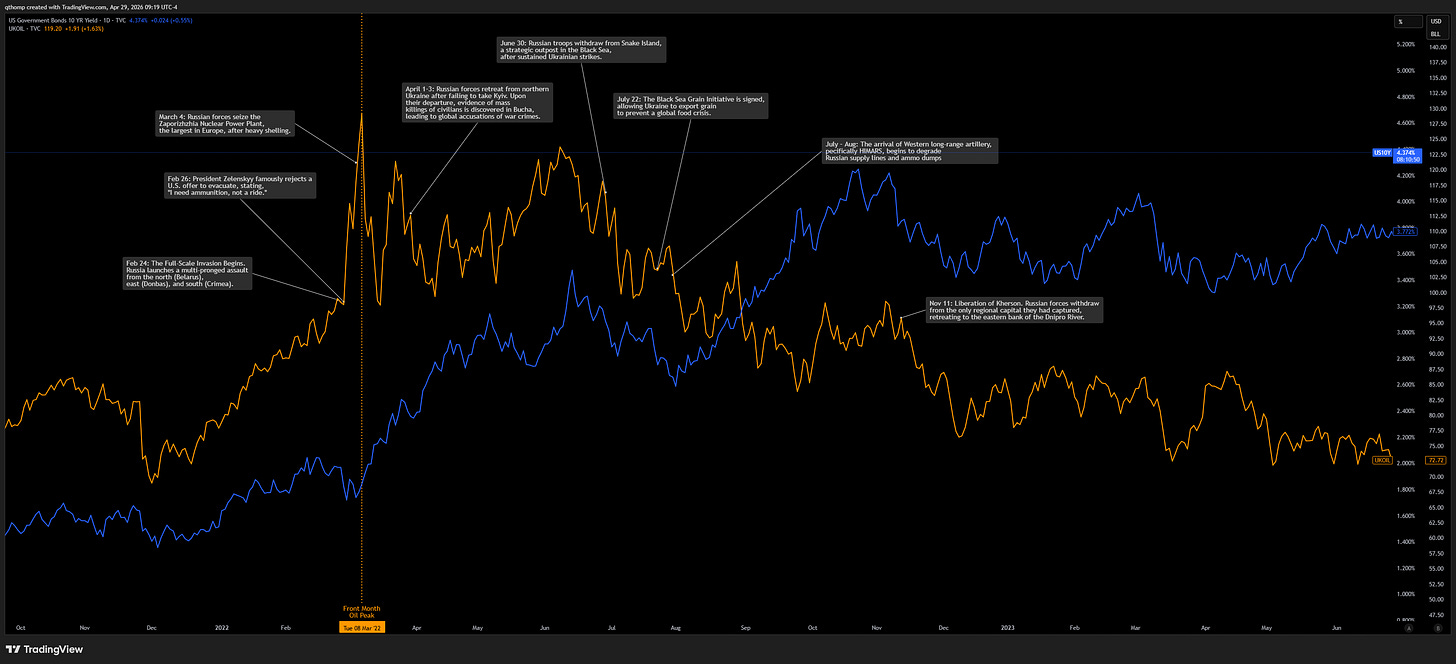

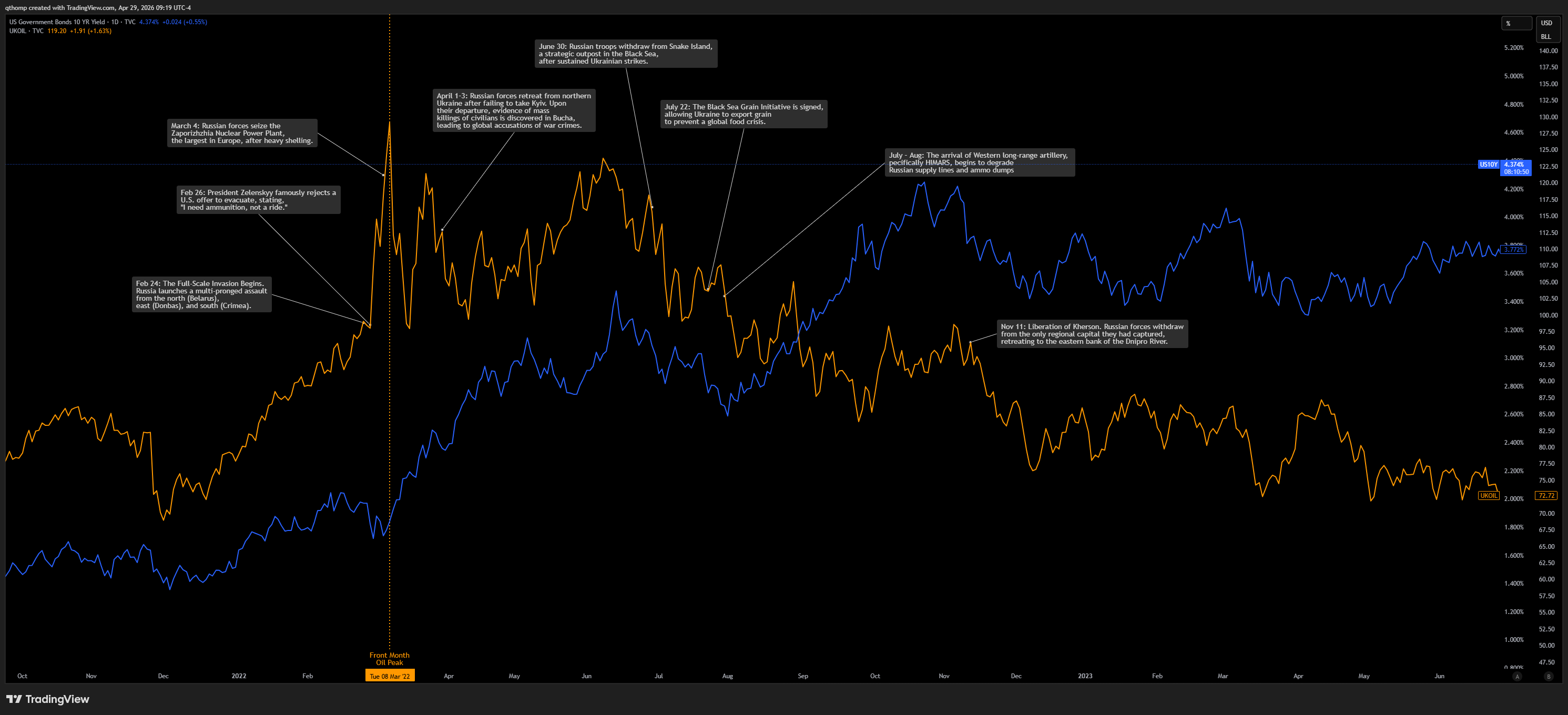

Let it be known that in 2022, yields actually didn’t break out until after the peak in war hysteria and front month oil. I actually believe there’s an argument to be made that Trump escalates or prolongs the Iran War in order to ensure physical commodity shortages don’t just increase price, but actually cause demand destruction which would slow the global economy and put downward pressure on bond yields. If it sounds like a cut off one arm to spare the other, trust your instincts. But the 2022 analog gives some level of credence to that idea if the correct read through is that once the war hysteria and economic uncertainty subsided, yields took off because global recession was taken off the table.

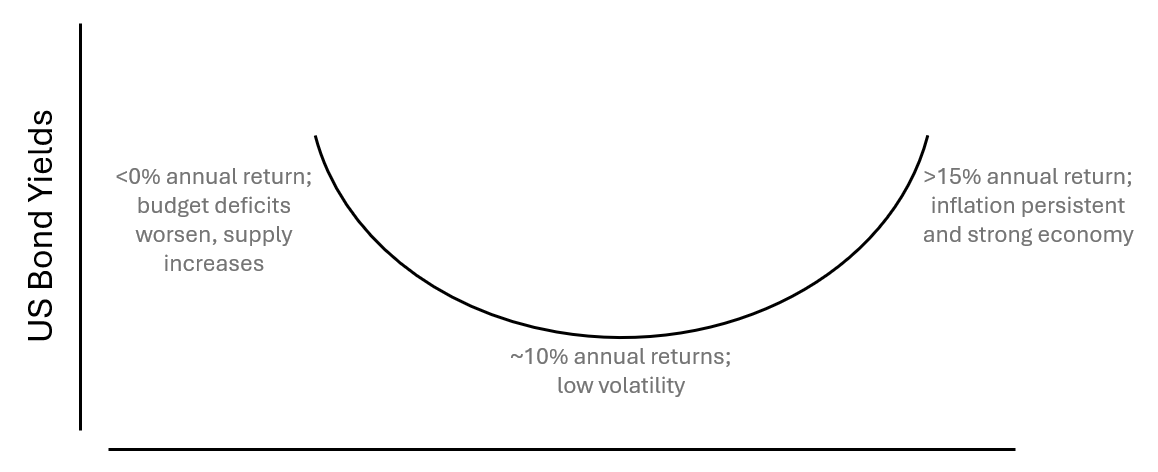

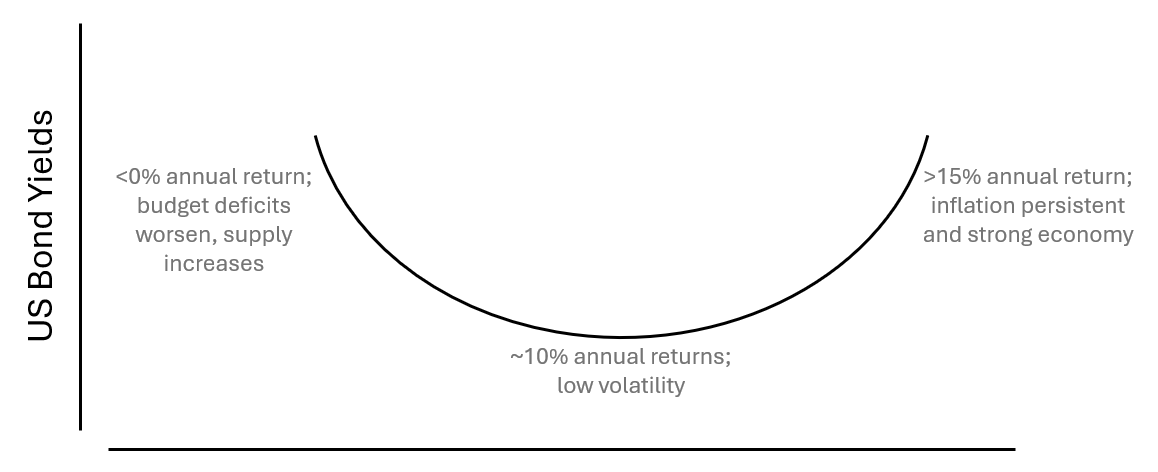

The yield smile.

There is a theory known as the dollar smile which describes a phenomenon where the US dollar strengthens during extreme scenarios (extreme fear or exceptional US growth) and weakens during moderate global growth, forming a smile-shaped curve. The dollar acts as a safe haven during crises and a high-performing asset during US economic superiority.

I have been thinking about this a bit differently with a focus on bond yields that might be better suited for the evolving fiscal dominant landscape we find ourselves in - the Yield Smile™.

Basically this is what I view Bessent and policymakers trying to manage markets towards. Low volatility, stable systematic buying pressure and passive flows behind US equities that just grind up slowly by a little each year. Move to far in either direction and risk a problem in the bond market. The difficulty right now though is that 3 straight years of the juicing the market via various interventionist policies has created the tinder for another inflation problem. Bond yields are pushing up against their upper limit and any further tactics to suppress them only makes matters worse. That’s not to say it can’t work in the very short-term, but it seems irresponsible to continue these policies and does not jive with the principles they have stood behind.

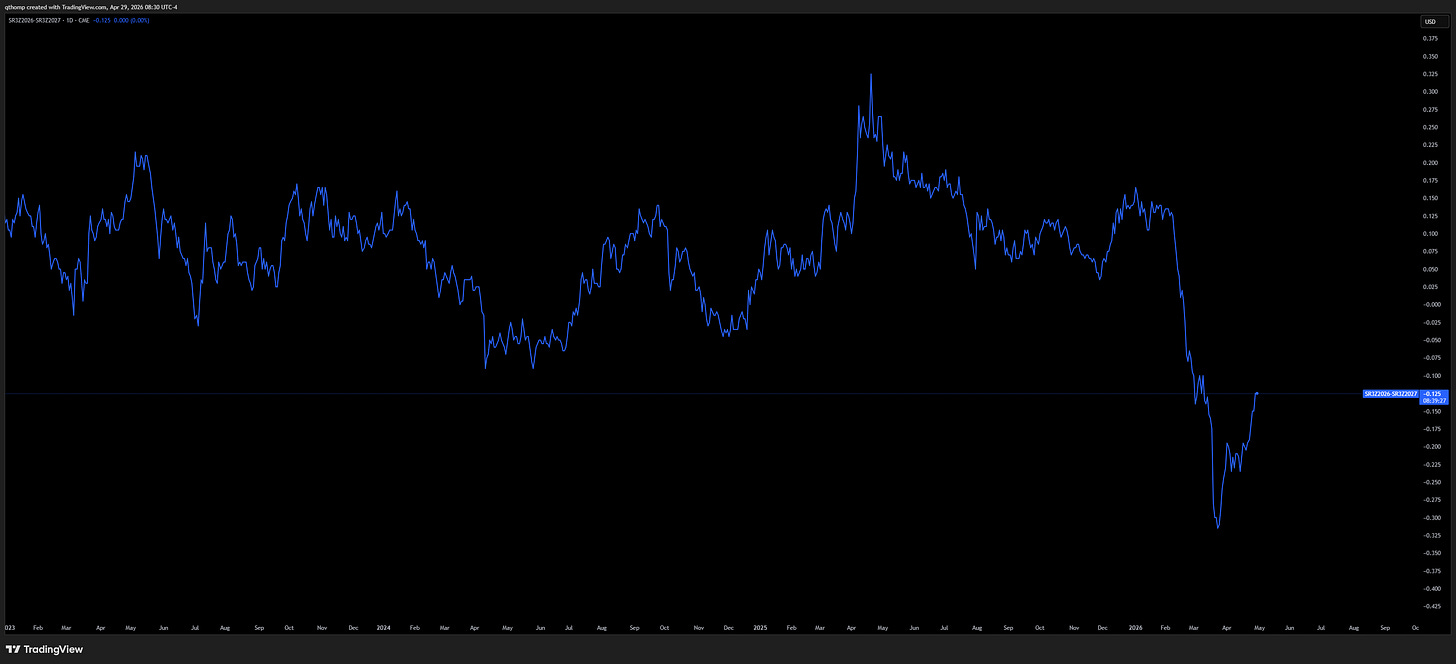

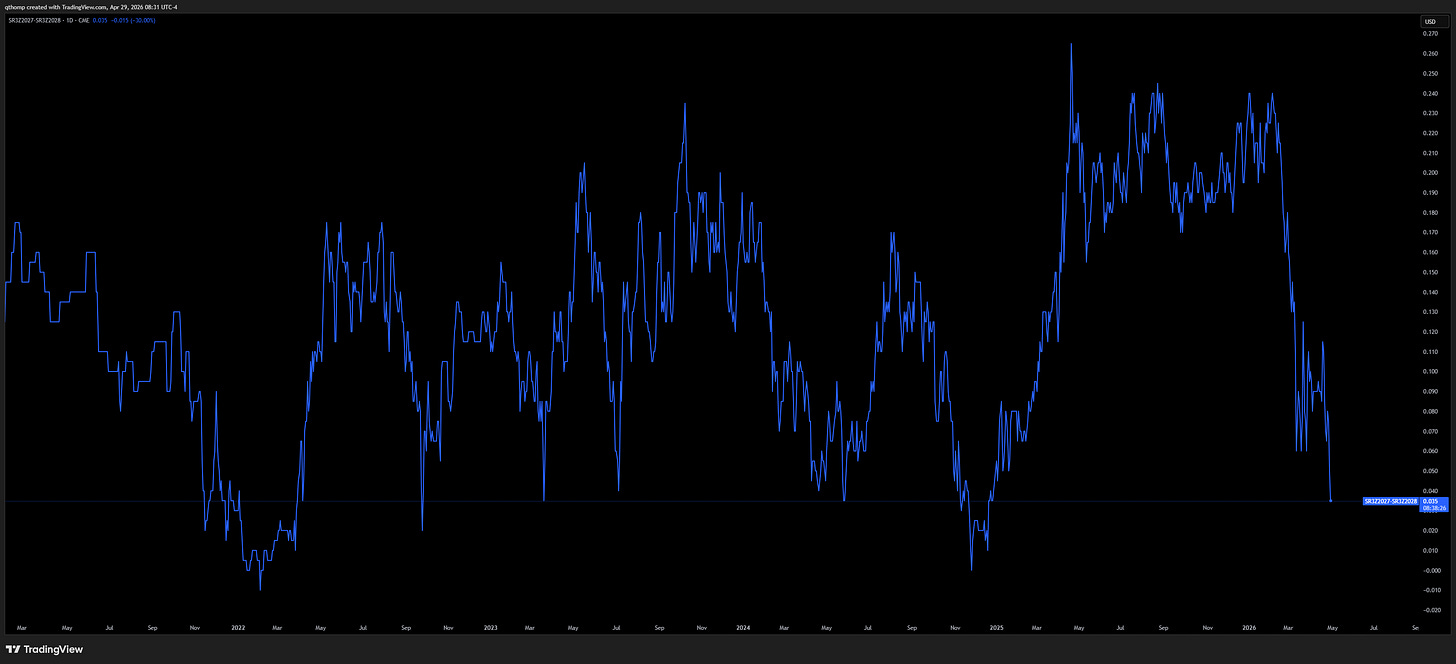

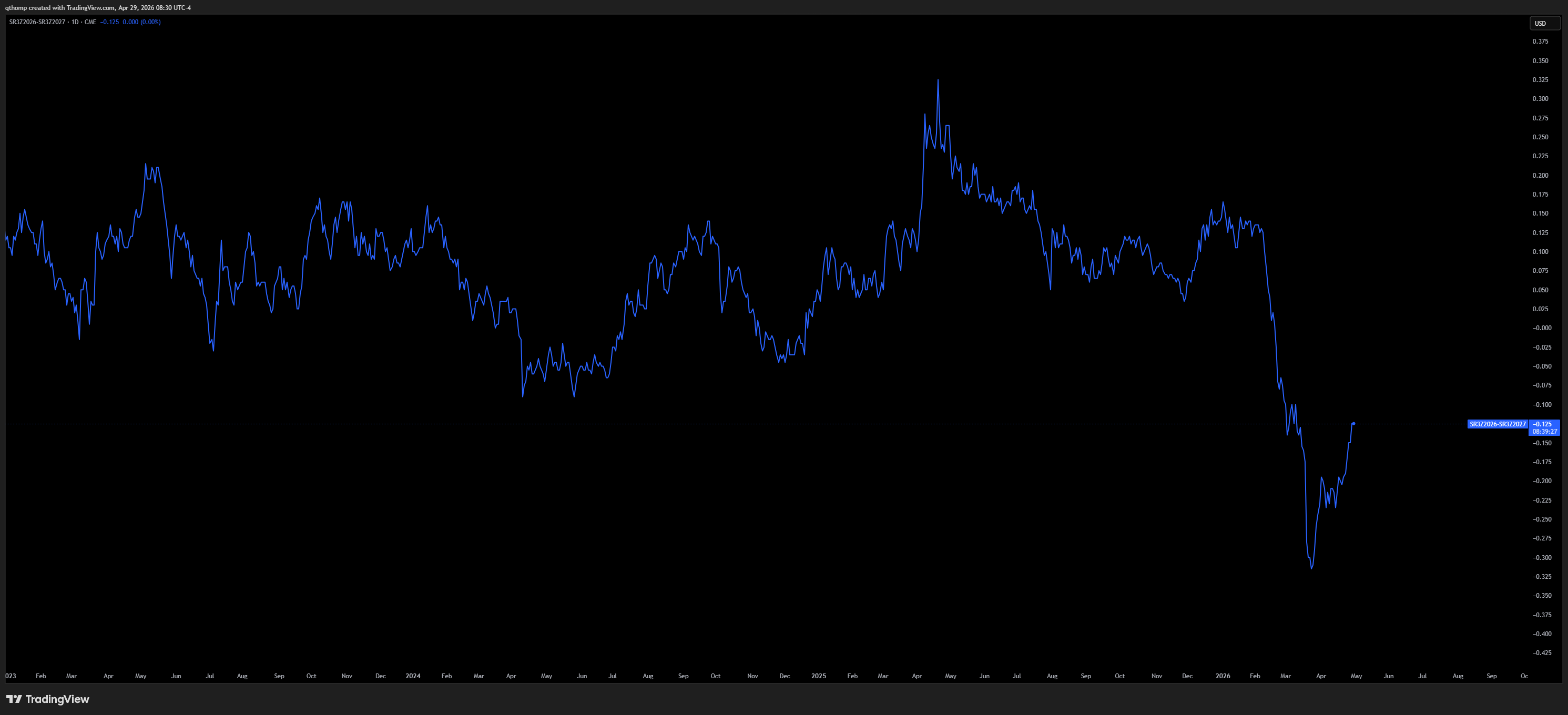

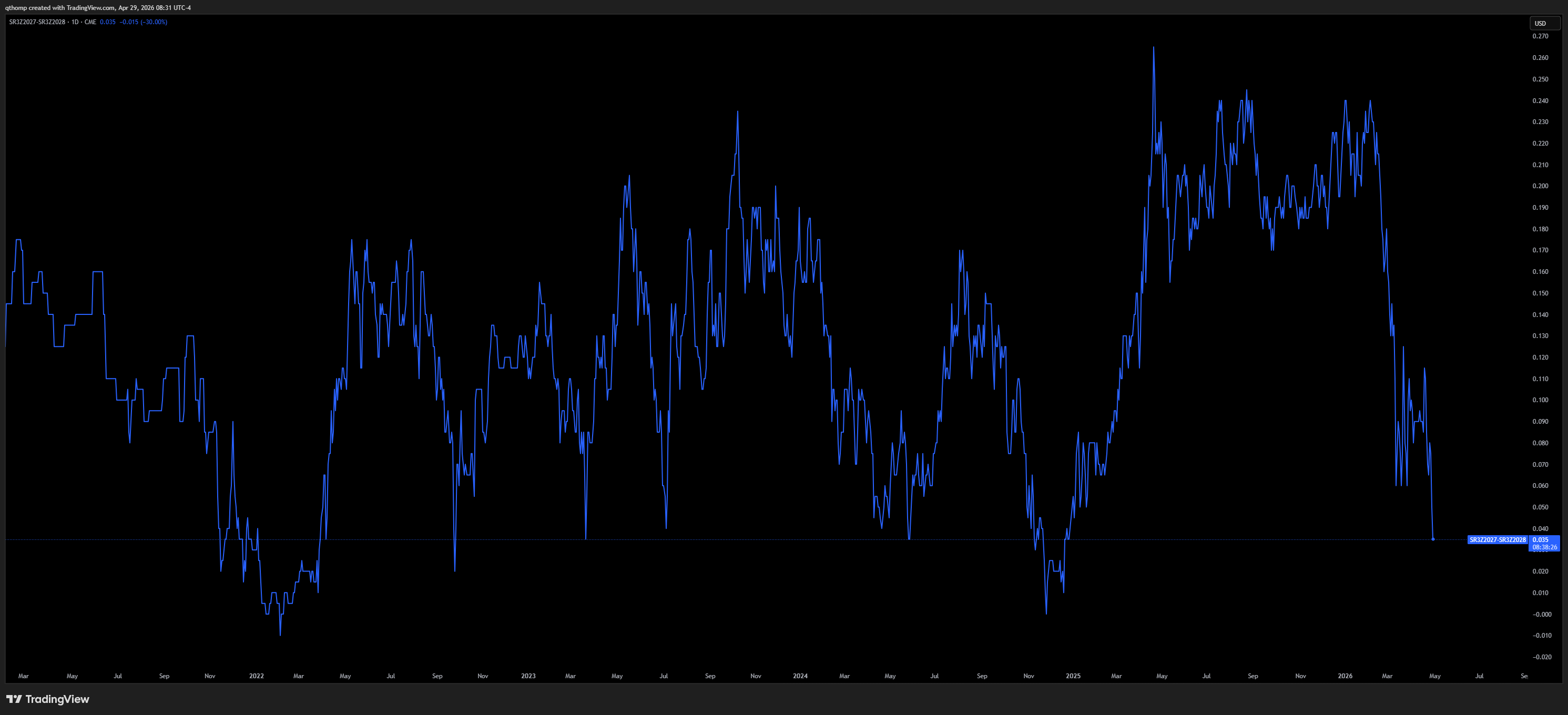

SOFR curve moves.

At the turn of the year the market was pricing in a ~15bps lower FFR in Dec 26 than Dec 27, this moved hard until late March where Dec 26 FFR was priced ~30bps higher than Dec 27. The move has since mean reverted back to pre-Iran war levels of ~13bps higher in Dec 26 than Dec 27.

Meanwhile, Dec 27 was pricing in a ~25bps lower FFR than Dec 28 and that has come all the way back near flat.

Dec 28 is interesting because it goes out to the end of Trump’s term. This part of the curve has seen less volatility than 26 and 27 but has still priced in marginally less rate cut expectations than at the start of the year.

The question I keep coming back to is whether or not any cuts can or should happen without a crisis given where inflation is expected to rise to over the next 12 months. I’m currently in the camp that neither the growth nor inflation pictures justify any rate cuts over the next 12 months. History has shown that a co-opted Fed and/or manipulated data can help the White House and Treasury takeover Fed policy to force cuts, but it isn’t really something I want to bet on outside of cheap entries for insurance policies. The other thing to consider is that if you have my view that long end yields become a problem before anything else, then you’d expect yield curve control oriented policy actions to come at some point. If and when this happens, it means the government is stepping in to support markets before they become a problem for the broader economy. These actions would reinforce stubborn inflation and persistent nominal growth, and thus further reduce the need for rate cuts.

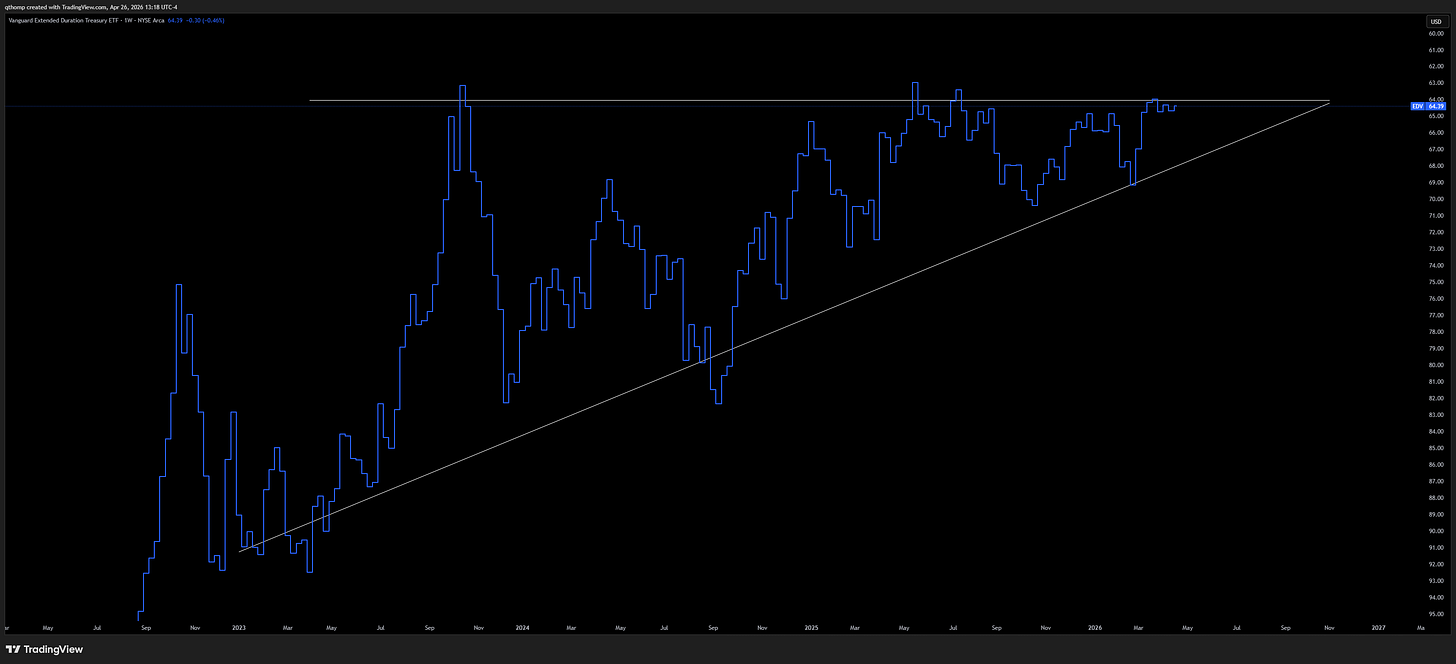

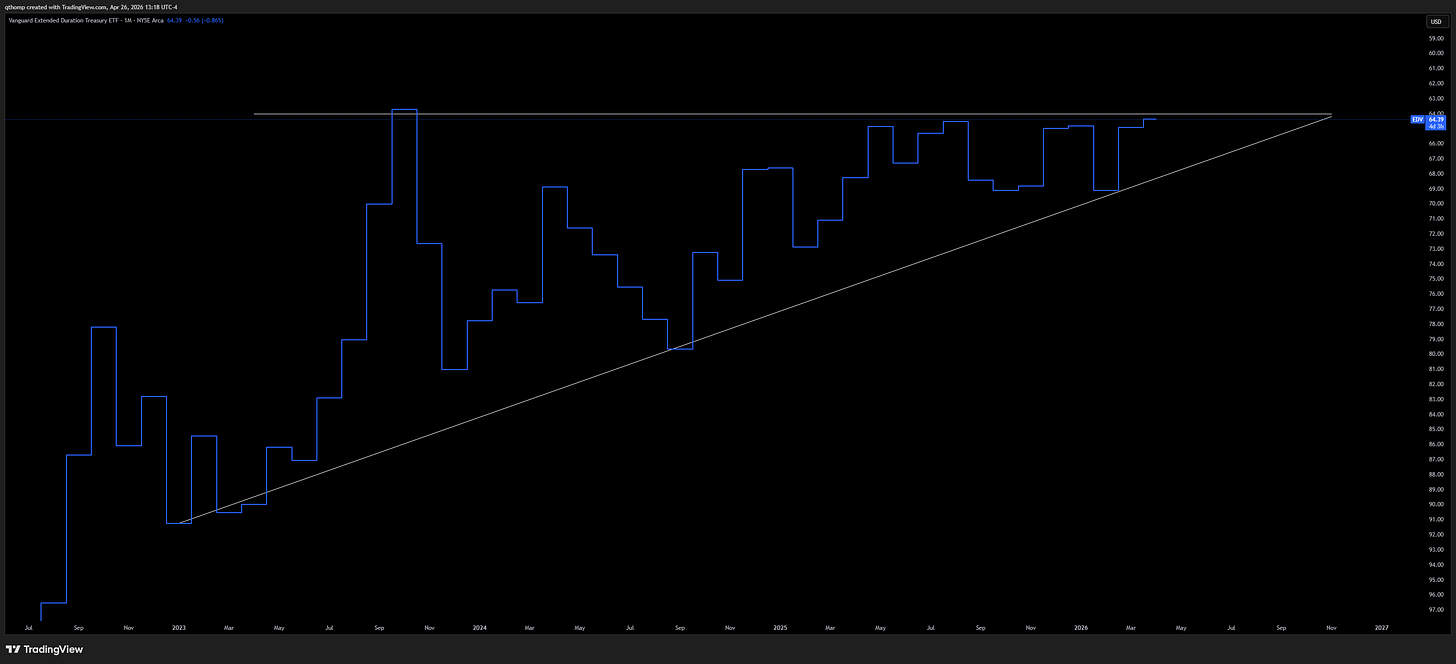

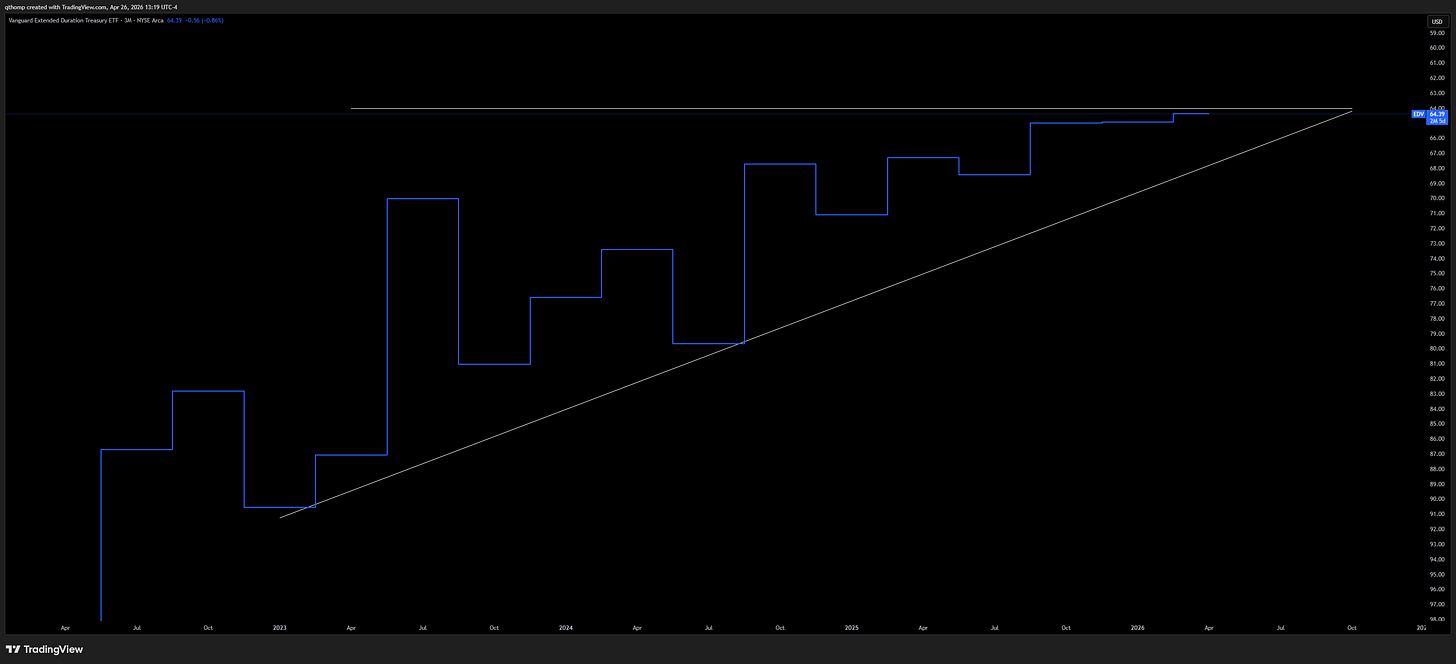

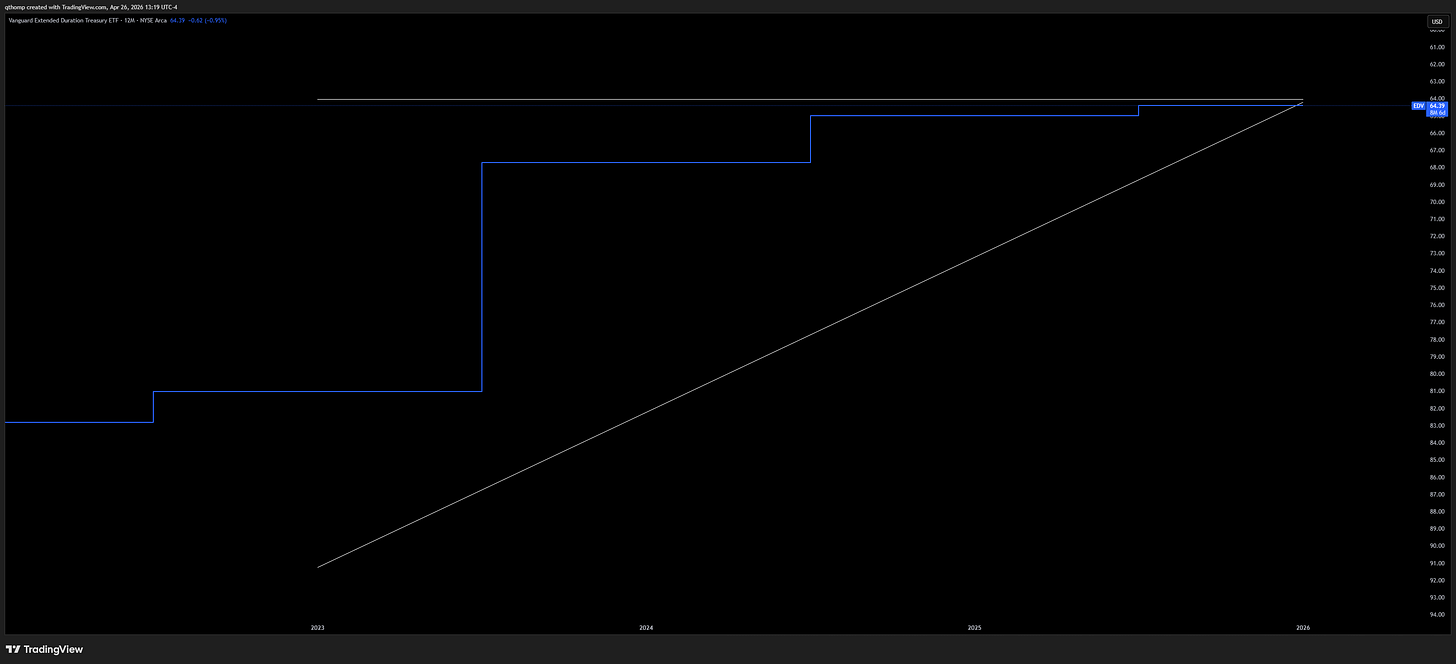

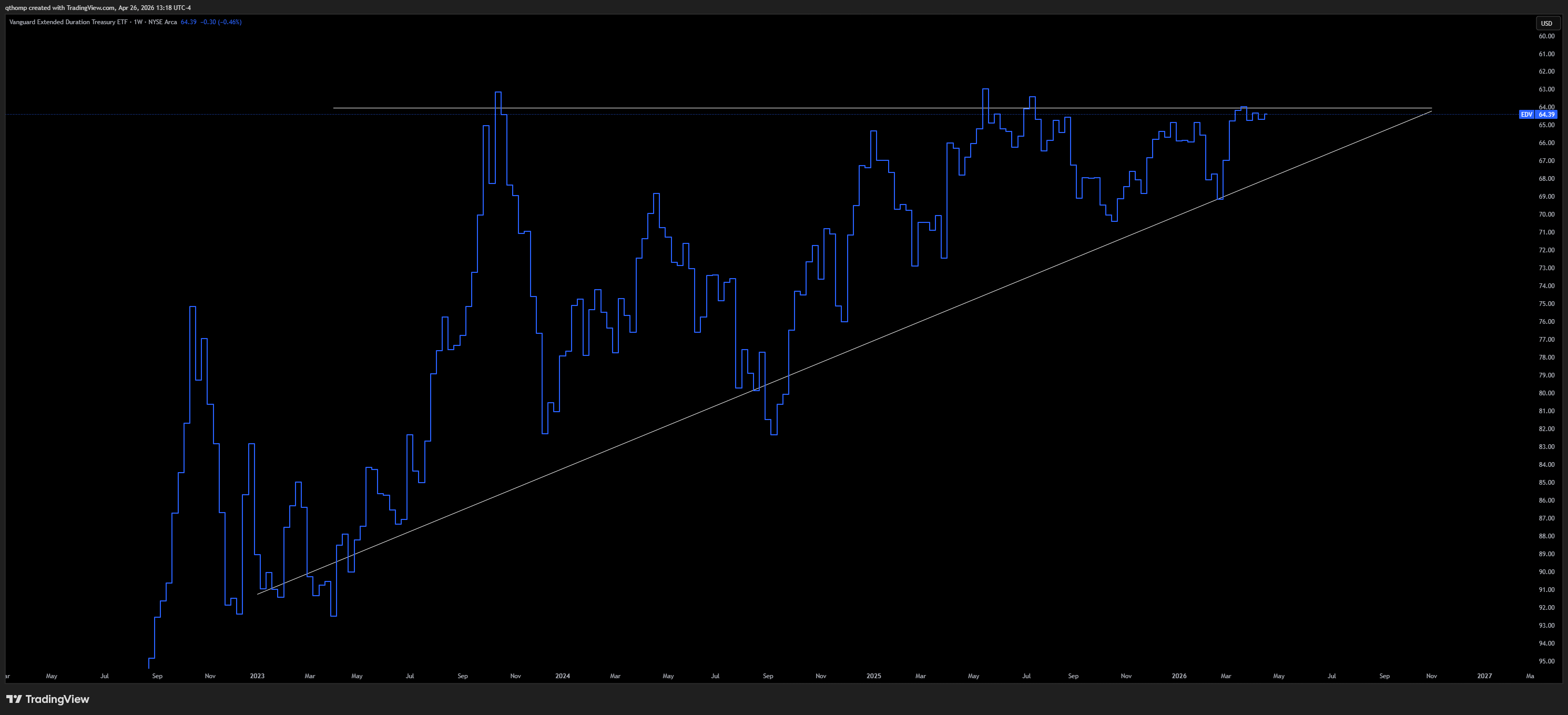

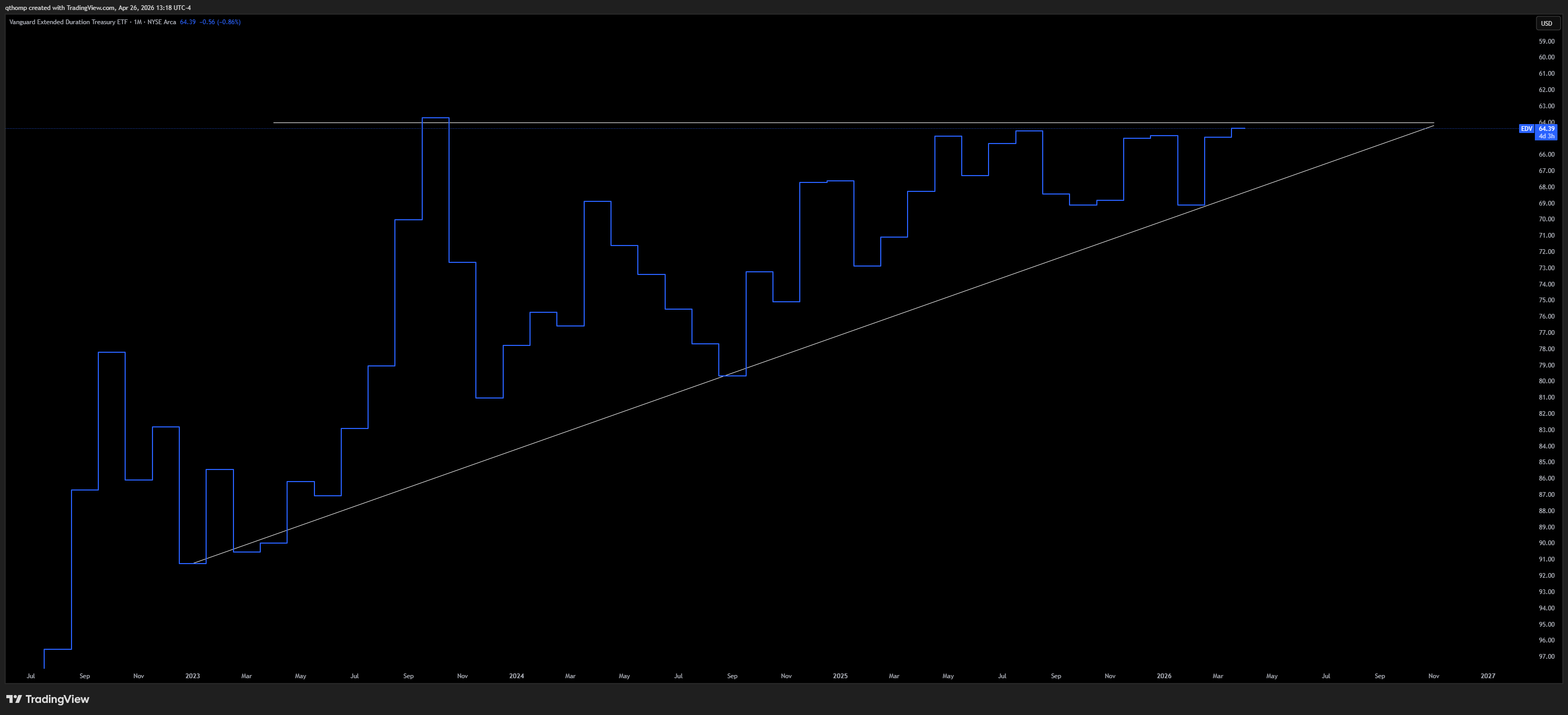

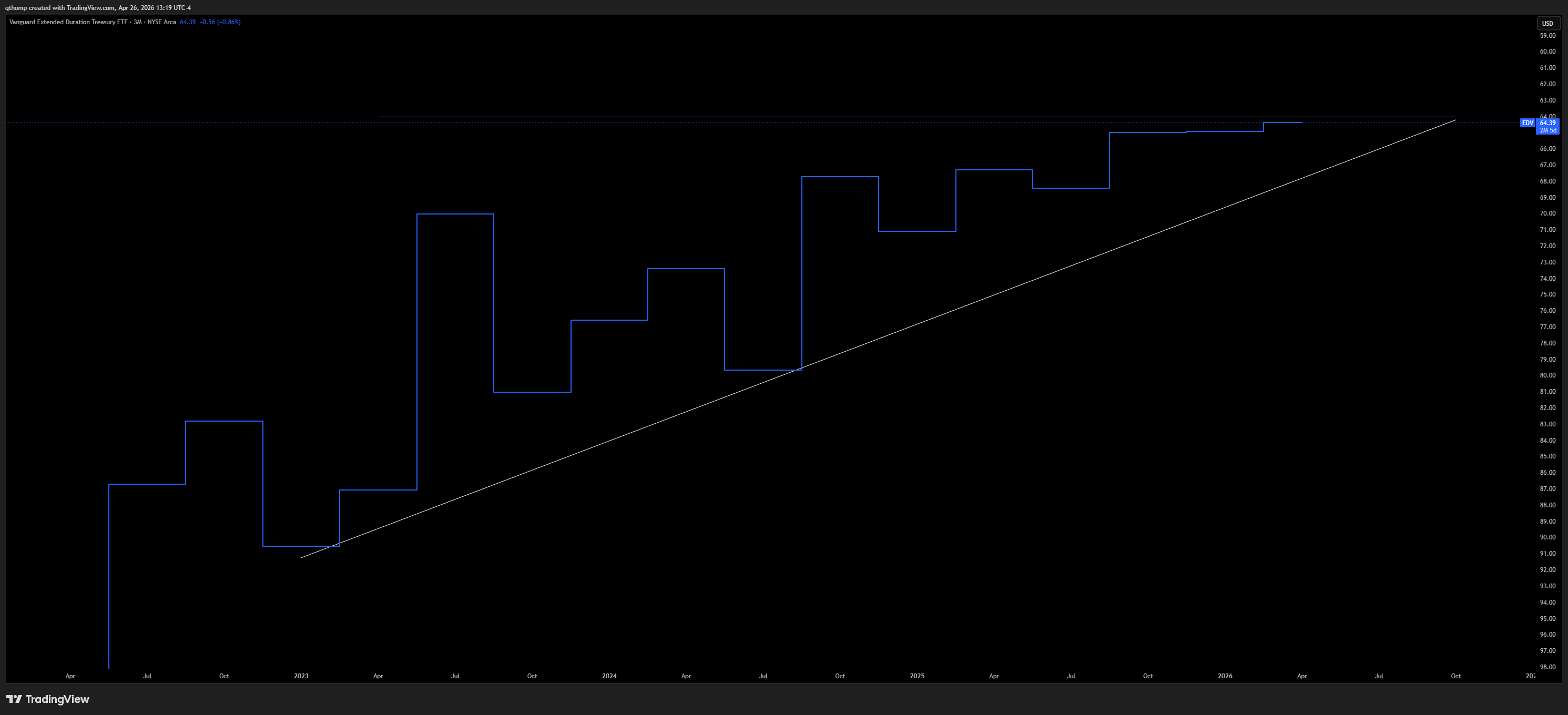

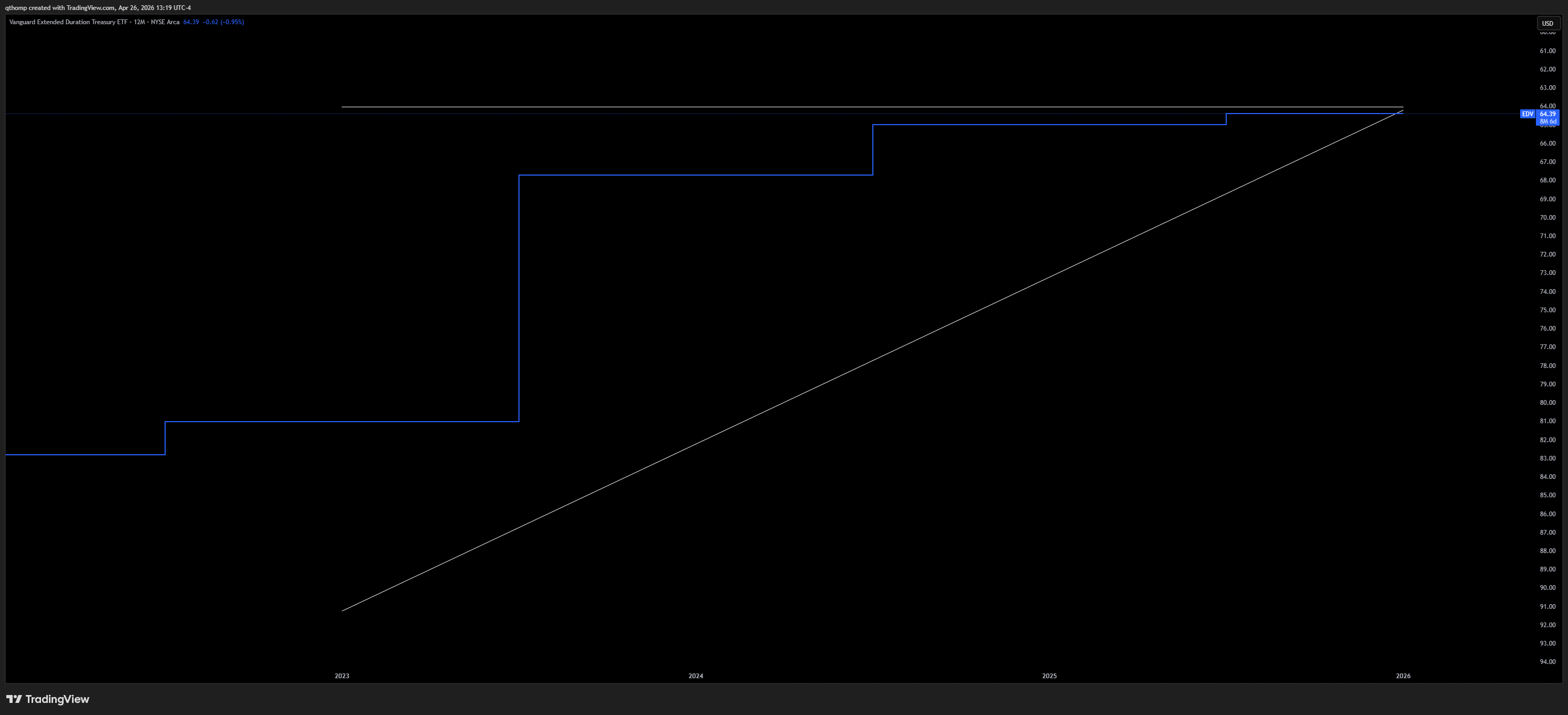

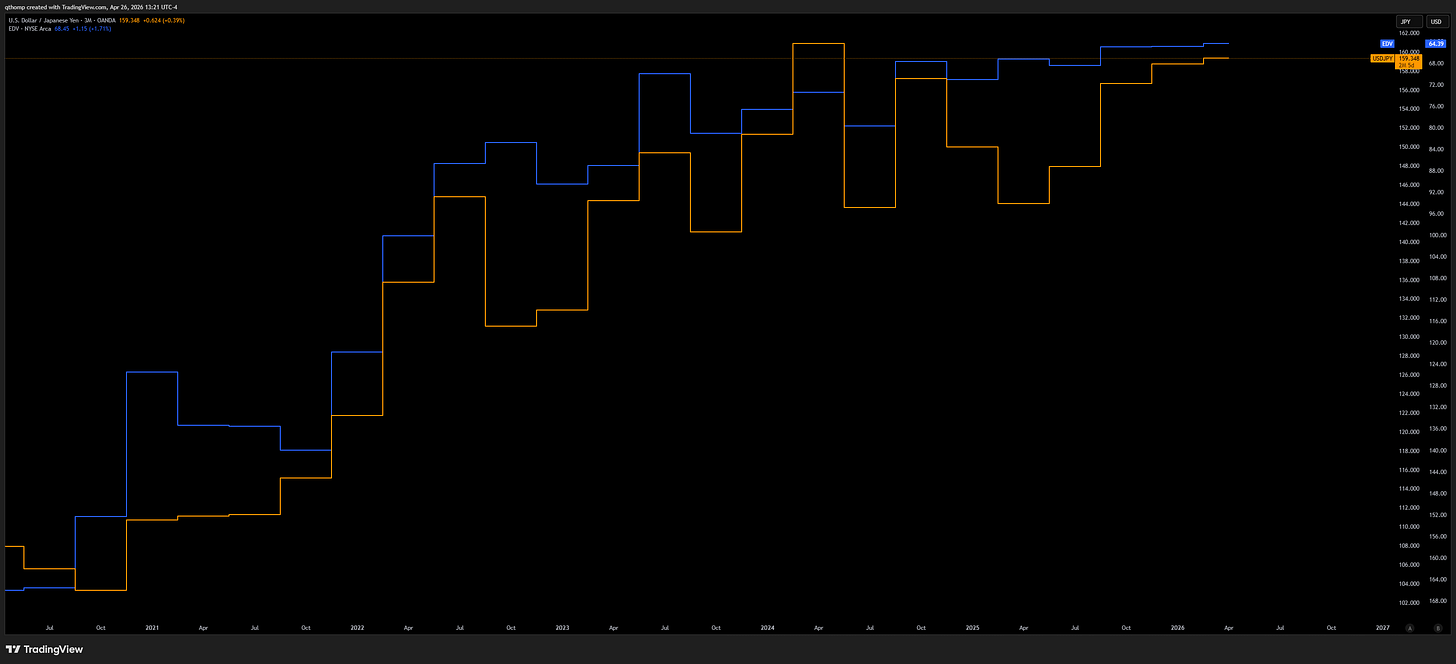

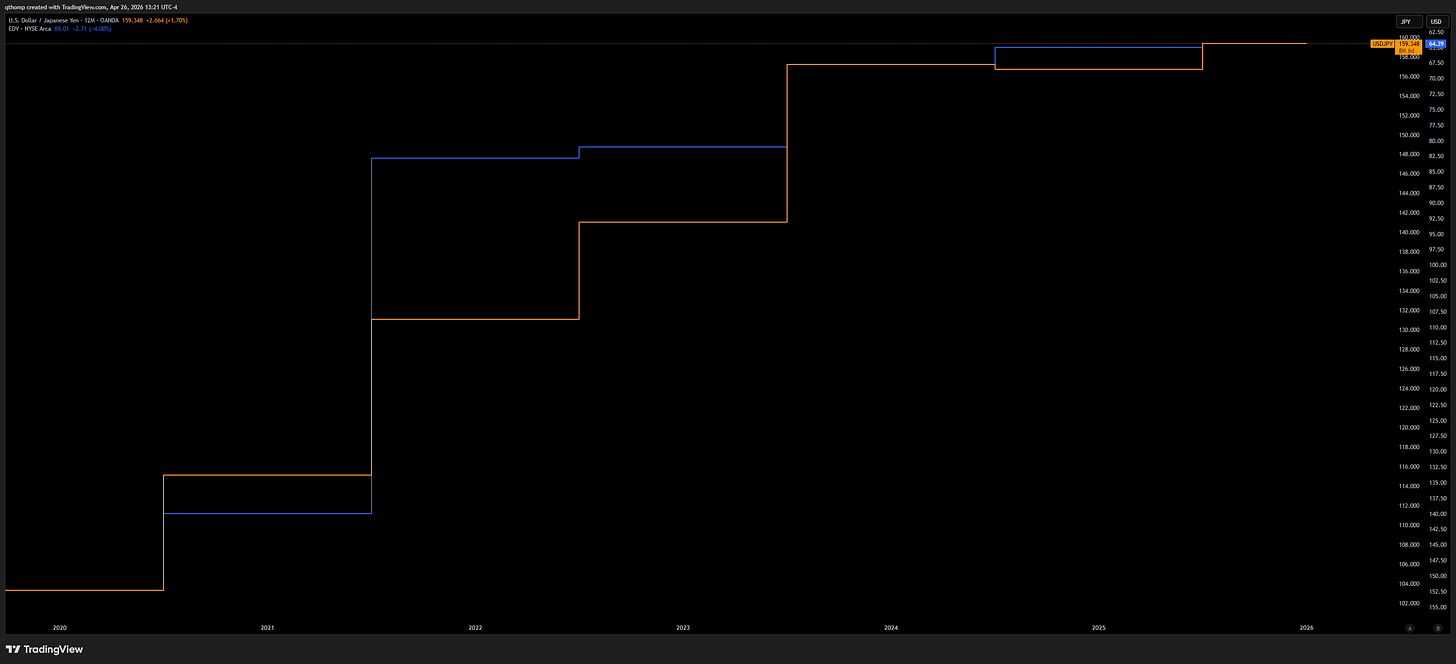

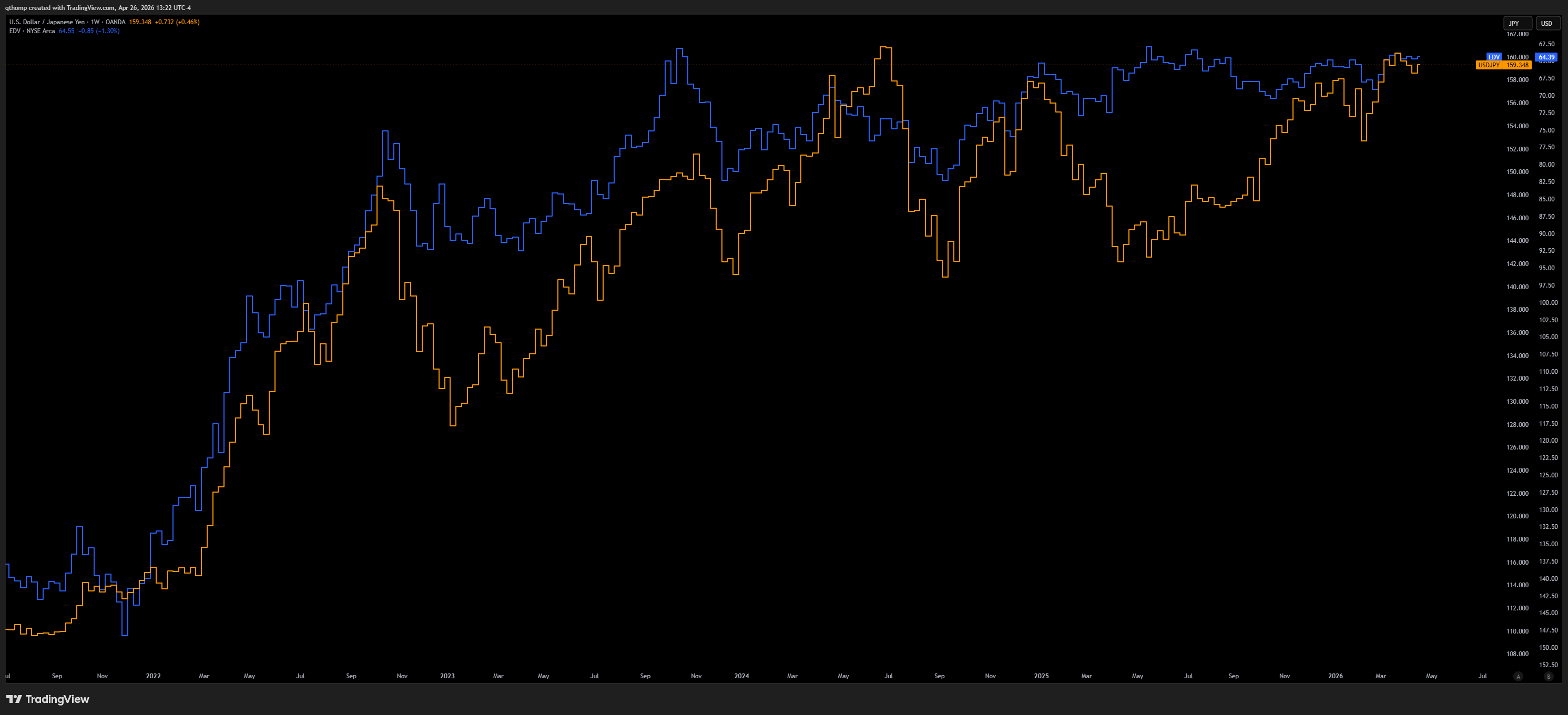

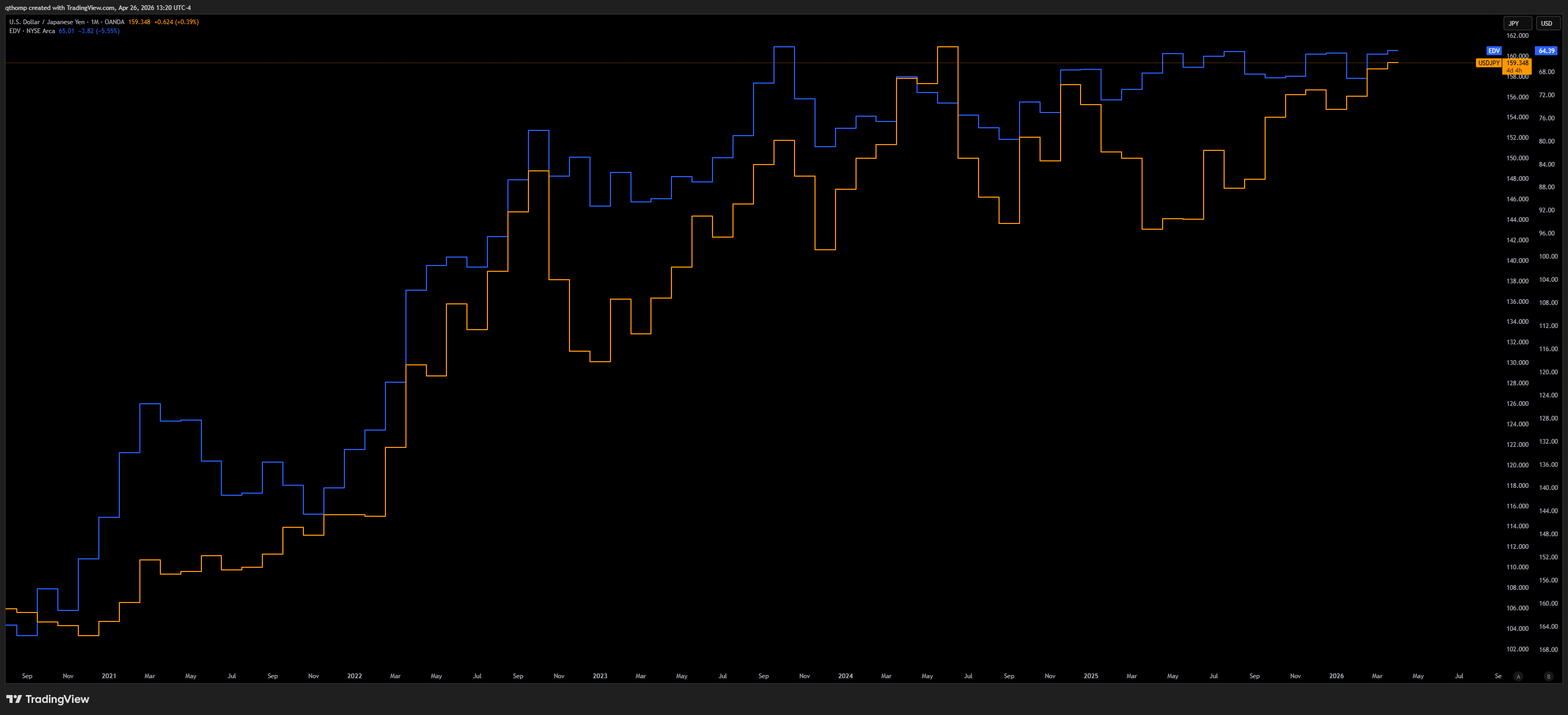

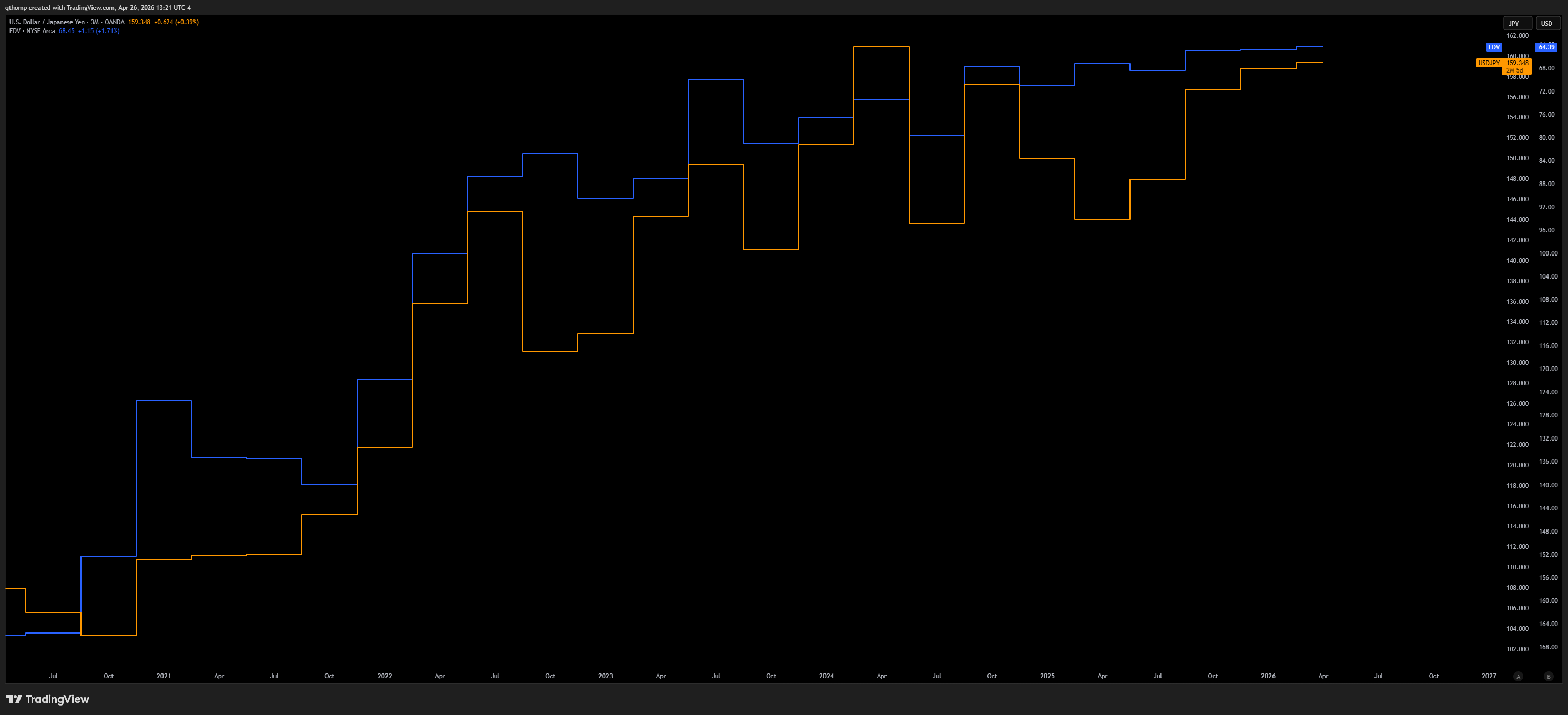

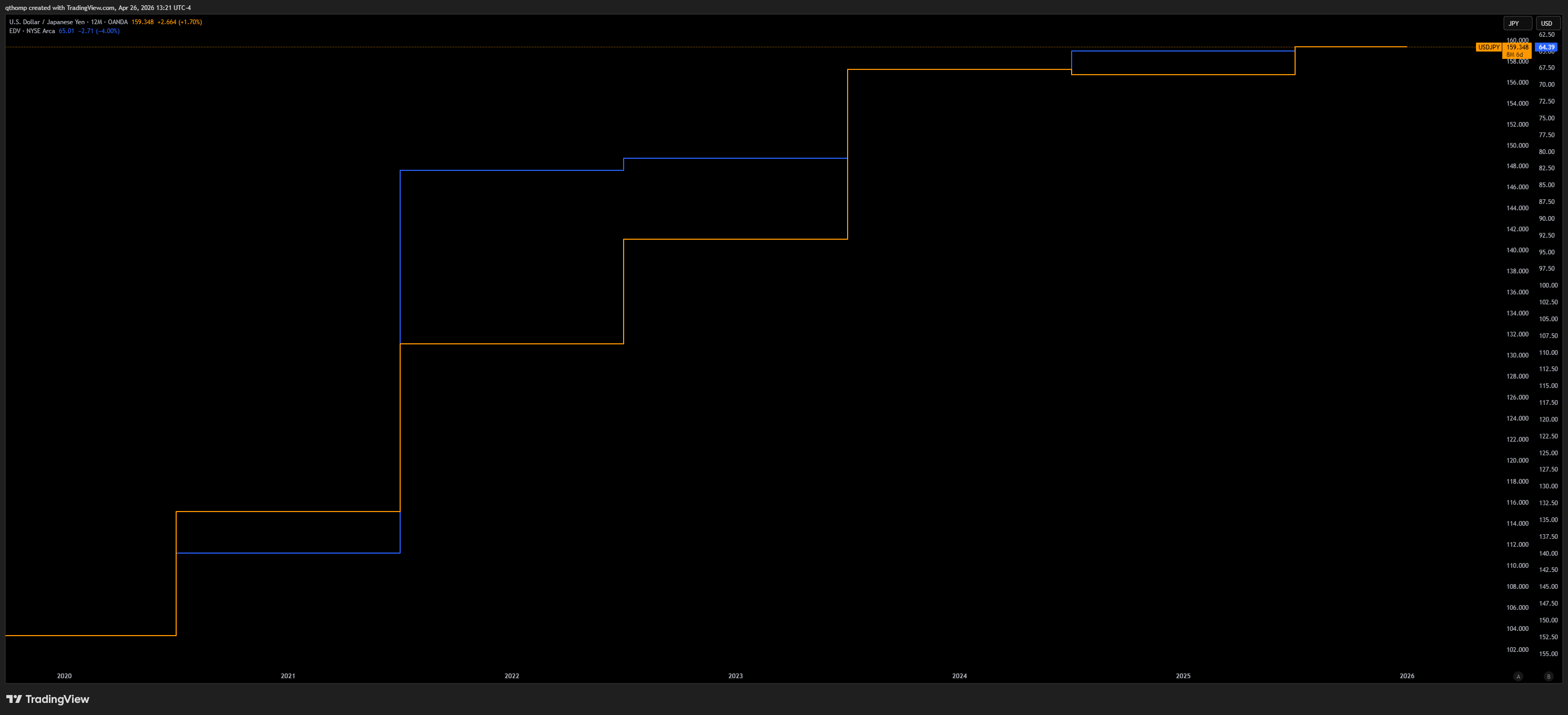

Here’s some fun chart art looking at $EDV, the Vanguard Extended Duration Treasury ETF. All of the below are inverted - so chart going up means price of the ETF is going down.

Weekly

Monthly

Quarterly

Annually

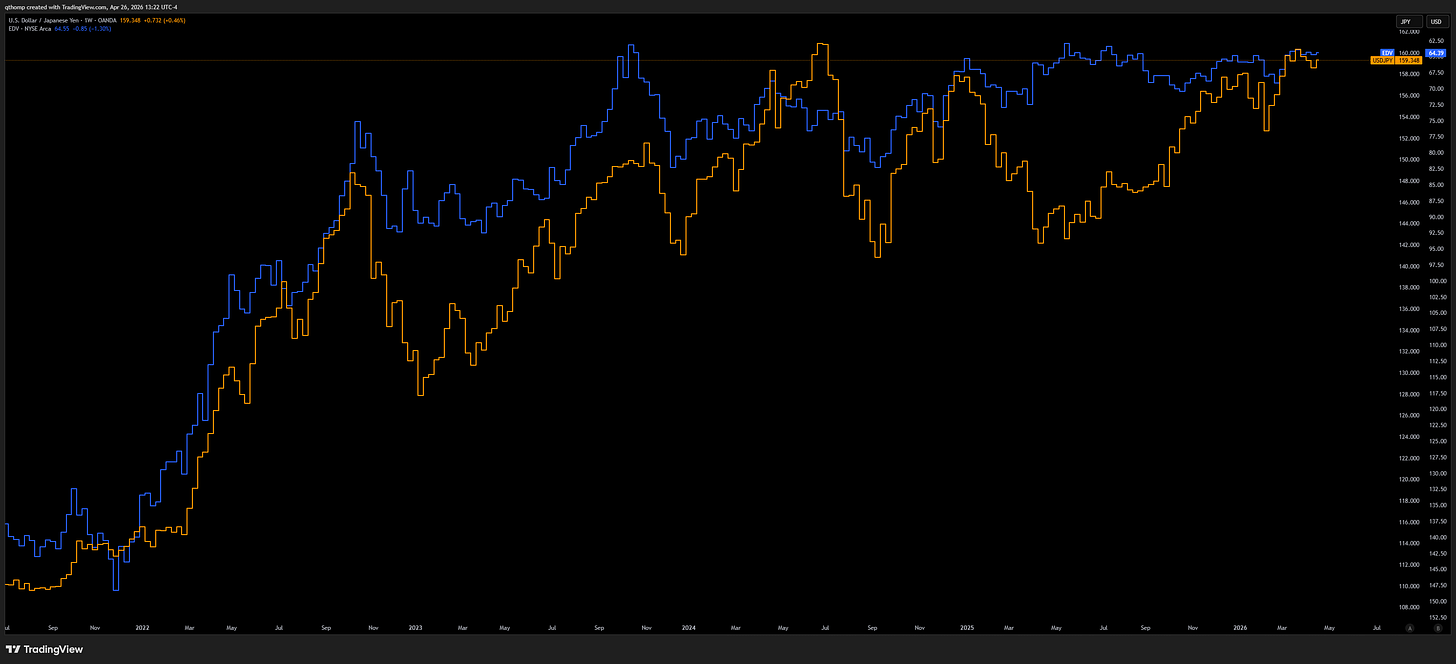

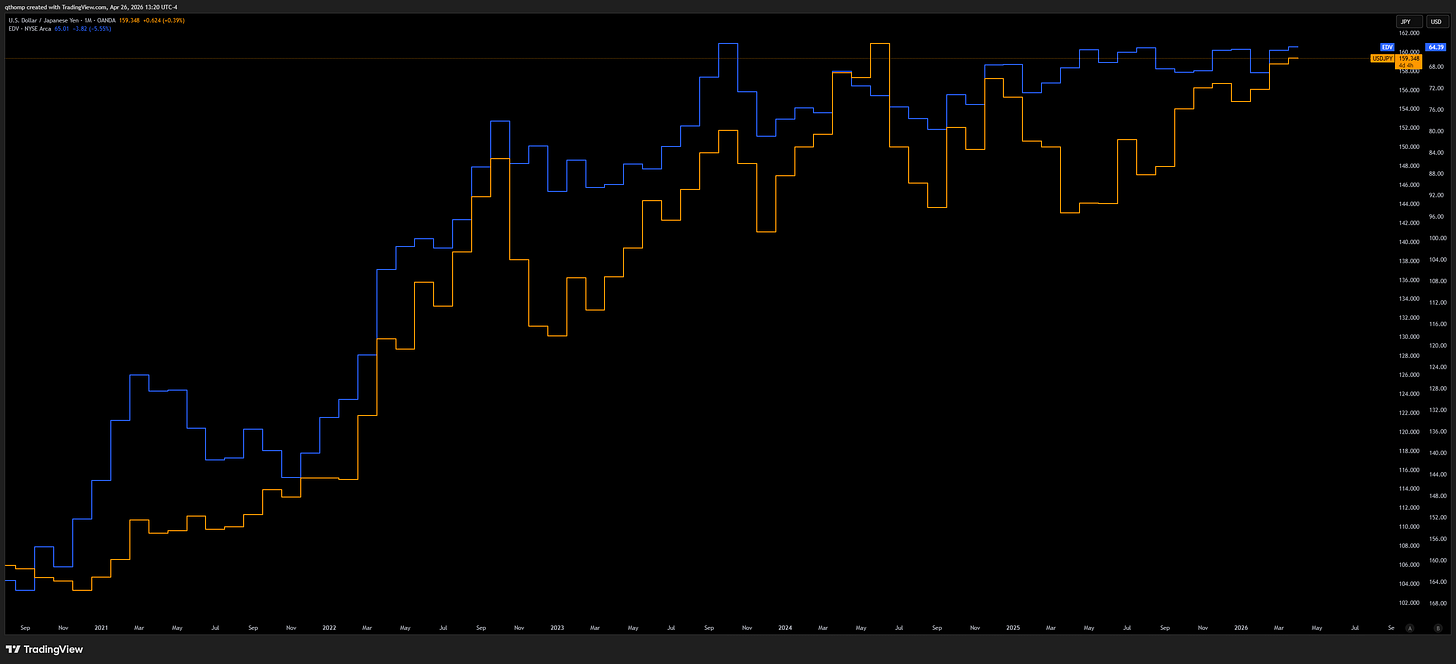

Now let me add USDJPY to it (in orange).

Weekly

Monthly

Quarterly

Annually

I’ll let you be the judge as to which way these are headed.

Recapping our April 10th, post-TACO, Scouting the Tape.

Bid December oil futures (although make sure this is Brent, not WTI, due to the risk of US export controls).

Look for positive mean reversion across Mag7, AI and semiconductor complex into early summer.

A clear mind, independent thoughts and seeking out all possible signal while removing noise is key in these markets.

Thanks for reading and good luck out there.